Global Steering Wheel Armature Market Size, Share and Trends Analysis Report

Market Size in USD Billion

CAGR :

%

USD

106.30 Billion

USD

184.01 Billion

2025

2033

USD

106.30 Billion

USD

184.01 Billion

2025

2033

| 2026 –2033 | |

| USD 106.30 Billion | |

| USD 184.01 Billion | |

| % | |

|

Global Steering Wheel Armature Market Segmentation, By Material Type (Magnesium or Magnesium Alloy, Steel or Steel Alloy, Aluminium or Aluminium Alloy, and Carbon Fiber), Number of Spokes (One Spoke, Two Spokes, Three Spokes, Four Spokes, and Six Spokes), Vehicle Type (Passenger Cars, Compact Cars, Mid-Size, SUV, Luxury, Light Commercial Vehicles (LCV), Heavy Commercial Vehicle (HCV), Trucks & Trailers, and Buses & Coaches), Sales Channel (Original Equipment Manufacturer (OEM), and Aftermarket),- Industry Trends and Forecast to 2033

Steering Wheel Armature Market Size

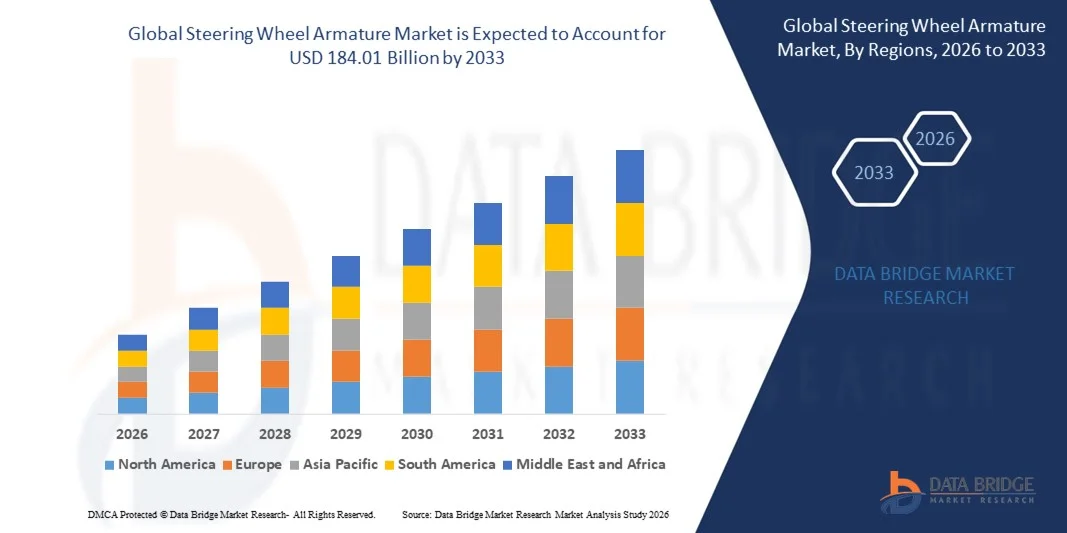

- The global steering wheel armature market size was valued at USD 106.30 billion in 2025 and is expected to reach USD 184.01 billion by 2033, at a CAGR of 7.10% during the forecast period

- The market growth is largely fuelled by increasing demand for advanced automotive safety systems, rising production of passenger and commercial vehicles, and the integration of smart technologies such as haptic feedback and multifunctional controls in steering wheels

- Growing adoption of electric and hybrid vehicles, which require advanced steering components for energy efficiency and precise control, is also driving market expansion

Steering Wheel Armature Market Analysis

- The market is witnessing strong growth due to increased vehicle production globally, especially in regions such as North America, Europe, and Asia-Pacific, where automotive manufacturing and technological integration are rapidly advancing

- Manufacturers are investing in R&D to develop lightweight, durable, and multifunctional steering wheel armatures that enhance vehicle safety, comfort, and user experience, thereby strengthening competitive positioning and market presence

- North America dominated the global steering wheel armature market with the largest revenue share in 2025, driven by the growing demand for advanced vehicle safety features and premium automotive components

- Asia-Pacific region is expected to witness the highest growth rate in the global steering wheel armature market, driven by rising automotive production, growing disposable incomes, urbanization, and government initiatives promoting vehicle safety and local manufacturing

- The aluminium or aluminium alloy segment held the largest market revenue share in 2025, driven by its lightweight properties, high strength, and cost-effectiveness. Aluminium armatures are widely preferred for passenger and commercial vehicles due to their durability, corrosion resistance, and ability to support multifunctional and electronic integrations. Manufacturers are investing in advanced casting and machining techniques to improve precision and reduce weight, enhancing fuel efficiency and overall vehicle performance

Report Scope and Steering Wheel Armature Market Segmentation

|

Attributes |

Steering Wheel Armature Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Steering Wheel Armature Market Trends

Rising Demand for Advanced Safety and Smart Vehicle Features

- The growing focus on vehicle safety, driver comfort, and connectivity is significantly shaping the steering wheel armature market, as automakers increasingly adopt components that integrate electronic controls, airbags, and multifunctional interfaces. Steering wheel armatures are gaining traction due to their ability to enhance driver control, safety, and ergonomic performance without compromising vehicle aesthetics. This trend strengthens their adoption across passenger, commercial, and off-road vehicles, encouraging manufacturers to innovate with advanced designs and integrated functionalities

- Increasing awareness around vehicle safety standards, regulatory compliance, and connected vehicle technologies has accelerated the demand for steering wheel armatures with multifunctional capabilities in passenger cars, electric vehicles, and commercial vehicles. Consumers and fleet operators are actively seeking vehicles with advanced control interfaces, prompting automakers to focus on durable, high-performance steering wheel systems. This has also led to collaborations between OEMs and component suppliers to develop innovative, lightweight, and technologically advanced armatures

- Safety regulations and smart vehicle trends are influencing purchasing decisions, with manufacturers emphasizing compliance, performance, and integration of electronic features such as cruise control, infotainment, and steering-based sensors. These factors are helping brands differentiate vehicles in a competitive market and build consumer trust, while also driving adoption of steering wheel technologies in electric and hybrid vehicles. Companies are increasingly highlighting these features in marketing campaigns to reinforce brand positioning and appeal to technology-oriented consumers

- For instance, in 2024, Toyota in Japan and Ford in the U.S. expanded their vehicle portfolios by incorporating multifunctional steering wheel armatures in new car models and SUVs. These launches responded to rising consumer preference for advanced driver assistance systems (ADAS) and ergonomic controls, with distribution across global retail and online sales channels. The products were also marketed as enhancing safety, driving experience, and smart vehicle capabilities, strengthening brand loyalty among target audiences

- While demand for steering wheel armatures is growing, sustained market expansion depends on continuous R&D, cost-effective production, and maintaining functional performance under varying vehicle conditions. Manufacturers are also focusing on improving scalability, supply chain reliability, and developing innovative solutions that balance cost, quality, and advanced features for broader adoption

Steering Wheel Armature Market Dynamics

Driver

Growing Preference for Advanced Safety, Multifunctional, and Connected Vehicle Features

- Rising consumer demand for vehicles with advanced safety, multifunctional controls, and connected interfaces is a major driver for the steering wheel armature market. Manufacturers are increasingly integrating steering wheel components with electronic systems, airbag modules, and driver-assist technologies to meet safety standards and improve user experience. This trend is also pushing research into lightweight, high-strength materials for improved vehicle efficiency and performance

- Expanding applications across passenger cars, commercial vehicles, electric vehicles, and off-road vehicles are influencing market growth. Steering wheel armatures help enhance driver control, safety, and ergonomic performance while supporting integration with infotainment, ADAS, and telematics systems. The increasing adoption of electric and autonomous vehicle technologies globally further reinforces this trend

- OEMs and component manufacturers are actively promoting steering wheel armature innovations through product development, safety certifications, and marketing campaigns. These efforts are supported by the growing consumer preference for technologically advanced, safe, and connected vehicles, and they also encourage partnerships between automakers and suppliers to improve performance and reduce vehicle weight

- For instance, in 2023, Honda in Japan and General Motors in the U.S. reported increased integration of multifunctional steering wheel armatures in passenger cars and commercial vehicle models. This expansion followed higher consumer demand for ADAS-enabled and ergonomic designs, driving repeat purchases and product differentiation. Both companies also highlighted safety, connectivity, and comfort in marketing campaigns to strengthen consumer trust and brand loyalty

- Although rising safety and smart vehicle trends support growth, wider adoption depends on cost optimization, component availability, and scalable production processes. Investment in advanced materials, supply chain efficiency, and innovative designs will be critical for meeting global demand and maintaining competitive advantage

Restraint/Challenge

High Manufacturing Cost And Complex Integration Challenges

- The relatively higher cost of advanced steering wheel armatures compared to conventional designs remains a key challenge, limiting adoption among price-sensitive automakers. High material costs, precision manufacturing, and integration with electronic systems contribute to elevated pricing. In addition, complex assembly requirements and adherence to stringent safety regulations can further affect production timelines and market penetration

- Consumer and manufacturer awareness of multifunctional steering wheel benefits varies, particularly in emerging markets where vehicle technology adoption is still growing. Limited understanding of ergonomic and safety advantages restricts adoption across certain vehicle segments, slowing innovation uptake in developing regions where educational initiatives on advanced steering technologies are minimal

- Supply chain and integration challenges also impact market growth, as steering wheel armatures require sourcing from specialized suppliers and compliance with strict quality standards. Logistical complexities and precise installation requirements increase operational costs. Companies must invest in advanced manufacturing, testing facilities, and efficient distribution networks to maintain product integrity

- For instance, in 2024, component suppliers in India and Brazil supplying passenger car and commercial vehicle manufacturers reported slower uptake due to higher prices and limited awareness of multifunctional benefits compared to conventional steering systems. Assembly and integration complexities were additional barriers. These factors also prompted some OEMs to delay feature upgrades, affecting market growth

- Overcoming these challenges will require cost-efficient production, streamlined integration processes, and focused educational initiatives for manufacturers and consumers. Collaboration with OEMs, certification bodies, and automotive technology partners can help unlock the long-term growth potential of the global steering wheel armature market. Furthermore, developing cost-competitive, lightweight, and technologically advanced armatures will be essential for widespread adoption

Steering Wheel Armature Market Scope

The global steering wheel armature market is segmented on the basis of material type, number of spokes, vehicle type, and sales channel.

- By Material Type

On the basis of material type, the market is segmented into magnesium or magnesium alloy, steel or steel alloy, aluminium or aluminium alloy, and carbon fiber. The aluminium or aluminium alloy segment held the largest market revenue share in 2025, driven by its lightweight properties, high strength, and cost-effectiveness. Aluminium armatures are widely preferred for passenger and commercial vehicles due to their durability, corrosion resistance, and ability to support multifunctional and electronic integrations. Manufacturers are investing in advanced casting and machining techniques to improve precision and reduce weight, enhancing fuel efficiency and overall vehicle performance.

The carbon fiber segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by its superior strength-to-weight ratio and premium positioning in luxury and sports vehicles. Carbon fiber armatures are increasingly adopted in high-performance and electric vehicles, where weight reduction and enhanced steering responsiveness are critical. The rising focus on lightweight vehicles for energy efficiency and electric mobility is further driving innovation in carbon fiber production and reducing material costs.

- By Number of Spokes

On the basis of the number of spokes, the market is segmented into one spoke, two spokes, three spokes, four spokes, and six spokes. The three-spoke segment held the largest revenue share in 2025, providing an optimal balance between ergonomics, aesthetics, and space for controls and airbags. This configuration is widely preferred in passenger cars and SUVs for comfort and enhanced functionality, supporting the integration of multimedia, safety, and driver assistance systems.

The four-spoke segment is projected to witness the fastest growth during 2026–2033, driven by its increasing adoption in commercial and heavy vehicles. The design allows the incorporation of multiple control interfaces, improving driver grip and operational safety. Growth in transportation and logistics sectors, along with the integration of advanced driver-assistance systems (ADAS), is boosting demand for robust and versatile four-spoke steering armatures.

- By Vehicle Type

On the basis of vehicle type, the market is segmented into passenger cars, compact cars, mid-size vehicles, SUVs, luxury vehicles, light commercial vehicles (LCV), heavy commercial vehicles (HCV), trucks & trailers, and buses & coaches. Passenger cars dominated the market in 2025 due to high production volumes, the widespread adoption of multifunctional steering systems, and growing demand for safety and infotainment features. OEMs are increasingly integrating steering armatures with airbag modules, controls, and sensors to enhance vehicle functionality and driver experience.

The SUV and luxury vehicle segments are expected to witness the fastest growth from 2026 to 2033, supported by rising consumer demand for ergonomics, comfort, and premium materials. These vehicles often feature advanced multifunctional armatures with integrated infotainment and safety controls. In addition, the push toward electric vehicles (EVs) in luxury and SUV segments is driving demand for lightweight, high-strength materials and technologically advanced steering solutions.

- By Sales Channel

On the basis of sales channel, the market is segmented into original equipment manufacturer (OEM) and aftermarket. The OEM segment held the largest market share in 2025, as steering wheel armatures are primarily integrated during vehicle manufacturing for optimized safety, performance, and design compatibility. OEMs continue to invest in research and development to improve material efficiency, durability, and compatibility with multifunctional systems, ensuring seamless vehicle integration.

The aftermarket segment is projected to witness strong growth from 2026 to 2033, driven by increasing vehicle customization trends, retrofitting of advanced multifunctional armatures, and replacement demand for aging vehicles. Consumers and fleet operators are increasingly opting for upgraded steering components to improve comfort, safety, and technology integration, creating opportunities for aftermarket suppliers and specialized service providers.

Steering Wheel Armature Market Regional Analysis

- North America dominated the global steering wheel armature market with the largest revenue share in 2025, driven by the growing demand for advanced vehicle safety features and premium automotive components

- The presence of major automotive manufacturers, high adoption of luxury and mid-size vehicles, and increasing consumer preference for ergonomically designed steering systems are key factors supporting market growth

- Furthermore, innovations in lightweight materials and integration with electronic control systems are enhancing vehicle performance and safety, establishing steering wheel armatures as critical components across passenger and commercial vehicles

U.S. Steering Wheel Armature Market Insight

The U.S. steering wheel armature market captured the largest revenue share in North America in 2025, fueled by rising vehicle production, strong demand for passenger cars and SUVs, and growing interest in aftermarket upgrades. Consumers are increasingly prioritizing vehicles equipped with electronically assisted steering systems and lightweight, durable steering components. Technological advancements in carbon fiber, magnesium, and aluminium steering armatures, combined with the adoption of safety and comfort features, are further propelling market growth. The integration of steering wheel armatures with advanced driver-assistance systems (ADAS) and in-vehicle electronics is also boosting demand.

Europe Steering Wheel Armature Market Insight

The Europe steering wheel armature market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by stringent automotive safety regulations, increased vehicle production, and the demand for premium and luxury cars. The adoption of lightweight and eco-friendly materials, such as aluminium and carbon fiber, is fostering innovation in steering components. European manufacturers are also emphasizing ergonomic designs and enhanced safety performance, supporting growth across passenger cars, SUVs, and commercial vehicles. Rising consumer awareness regarding vehicle safety and driving comfort is further stimulating demand for advanced steering wheel armatures.

U.K. Steering Wheel Armature Market Insight

The U.K. steering wheel armature market is projected to register strong growth from 2026 to 2033, fueled by increasing urbanization, higher disposable incomes, and a focus on vehicle safety and comfort. Consumers and manufacturers are showing growing interest in electric power-assisted steering systems and premium materials for steering armatures. The integration of steering wheel armatures with multifunctional controls and infotainment systems is driving demand, particularly in passenger cars and luxury vehicles. Robust automotive manufacturing infrastructure and the growing aftermarket segment also contribute to market expansion.

Germany Steering Wheel Armature Market Insight

The Germany steering wheel armature market is expected to witness rapid growth from 2026 to 2033, driven by strong automotive manufacturing, high technological adoption, and increasing demand for lightweight and durable steering components. German consumers prioritize vehicle safety, ergonomics, and performance, prompting OEMs to innovate in steering armature design. The integration of armatures with electronic control systems, ADAS, and smart features in passenger and commercial vehicles is enhancing market prospects. Moreover, government initiatives promoting eco-friendly and energy-efficient vehicles further encourage adoption.

Asia-Pacific Steering Wheel Armature Market Insight

The Asia-Pacific steering wheel armature market is expected to register the highest growth rate from 2026 to 2033, driven by rising vehicle production, expanding passenger car and SUV segments, and growing adoption of electric and hybrid vehicles in countries such as China, India, and Japan. Government initiatives promoting vehicle safety and localization of automotive components are supporting market expansion. The region’s cost-effective manufacturing capabilities and increasing demand for lightweight and technologically advanced steering systems are making steering wheel armatures more accessible across passenger and commercial vehicles.

China Steering Wheel Armature Market Insight

The China steering wheel armature market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rapid urbanization, growth in vehicle ownership, and strong domestic automotive production. The demand for lightweight, durable, and technologically integrated steering wheel armatures is rising across passenger cars, SUVs, and commercial vehicles. Local manufacturers are innovating with aluminium, magnesium, and carbon fiber materials, while the push for electric and hybrid vehicles is further enhancing market opportunities. The integration of steering components with in-vehicle electronics, safety systems, and ADAS is also driving market expansion.

Japan Steering Wheel Armature Market Insight

The Japan steering wheel armature market is expected to witness significant growth from 2026 to 2033, driven by the country’s high automotive manufacturing standards, rapid adoption of advanced driver assistance technologies, and consumer preference for safe and ergonomic vehicles. The market growth is further supported by innovations in lightweight materials and multifunctional steering systems, which enhance driving comfort and safety. The expansion of electric vehicles and compact cars in Japan is also contributing to the increasing demand for sophisticated steering wheel armatures.

Steering Wheel Armature Market Share

The Steering Wheel Armature industry is primarily led by well-established companies, including:

- GETAC (U.S.)

- Tianjin Liuhe Magnesium Product Co., Ltd. (China)

- Lunt Manufacturing (U.S.)

- NIHON PLAST CO., LTD. (Japan)

- GSK In Tek Co., Ltd. (South Korea)

- ROS INDUSTRIE SRL (Italy)

- MZW Motor (Germany)

- STARION CO., LTD (Japan)

- SUMMIT STEERING WHEEL CO., LTD. (China)

- Magpulse Technologies Pvt. Ltd. (India)

- Shanghai Fangle Auto Parts Co., Ltd. (China)

- TaiHangChangQing Automobile Safety System Co., Ltd. (China)

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。