グローバルタンク断熱市場規模、シェア、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

3.84 Billion

USD

10.30 Billion

2024

2032

USD

3.84 Billion

USD

10.30 Billion

2024

2032

| 2025 –2032 | |

| USD 3.84 Billion | |

| USD 10.30 Billion | |

| % | |

|

世界のタンク絶縁材の区分、タイプによって(貯蔵および交通機関)、物質的なタイプ(拡大されたポリスチレン(EPS)、Rockwoolのセルラー ガラス、ガラス繊維、エラストマーの泡、ポリウレタン(PU)および他)、温度のタイプ(熱絶縁材および冷たい絶縁材)、タンク タイプ(縦タンク、横のタンク、固定タンクおよび取付けられたタンク)、タンク端(パラボリック皿および平たい箱)、エンド ユーザー(オイル及びガスの傾向およびエネルギー、食糧および廃物、食糧および廃物、食糧および廃物および廃物、食糧および廃物への2032、食糧および廃物。

Tank Insulation Market Size

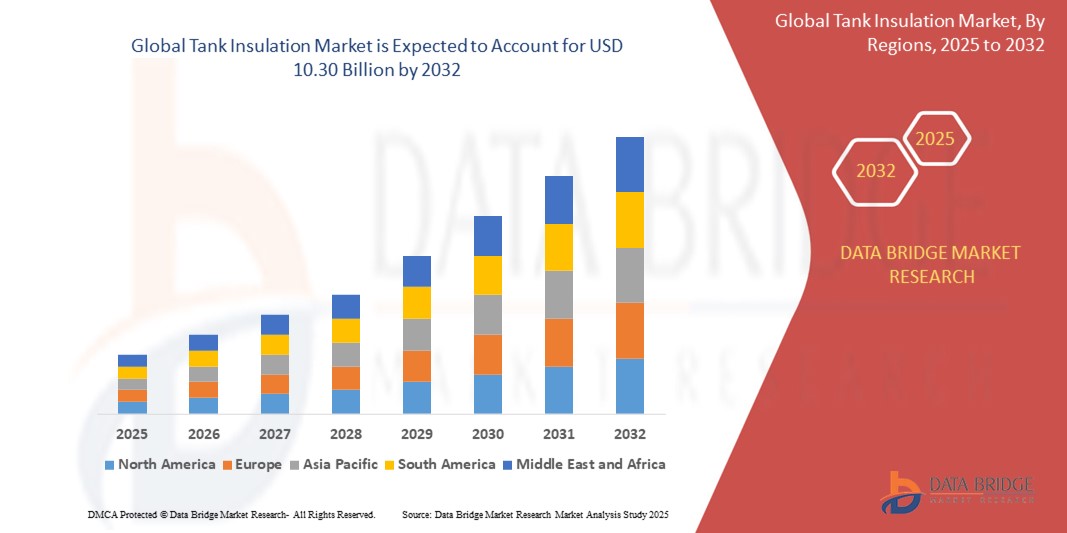

- The global tank insulation market size was valued atUSD 3.84 billion in 2024and is expected to reachUSD 10.30 billion by 2032, at aCAGR of 5.25%during the forecast period

- This growth is driven by factors such as the increasing demand for energy-efficient insulation solutions in industries such as oil & gas, energy, and chemicals

Tank Insulation Market Analysis

- Tank insulation is defined as the process in which different chemicals and materials are applied to the inside of tank and also to the surface, to maintain the temperature throughout its usage period

- Tank insulation is done to preserve the temperature inside the tank in order to minimize the heat loss

- North America is expected to dominate the tank insulations market due to its advanced infrastructure and continuous focus on technological innovations in insulation materials

- Asia-Pacific is expected to be the fastest growing region in the tank insulation market during the forecast period due to rapid industrialization and urbanization, which is driving significant demand for tank insulation solutions

- Rockwool and polyurethane (PU) segment is expected to dominate the market with a market share of 31.5% due to their high thermal insulation properties and versatility. These materials are widely used in industries such as oil and gas, chemicals, and energy due to their excellent ability to maintain the required temperature levels while ensuring energy efficiency

Report Scope and Tank Insulation Market Segmentation

|

Attributes |

Tank Insulation Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Tank Insulation Market Trends

“Advancements in Sustainable Insulation Materials”

- In recent years, there has been a significant trend towards the use of sustainable and eco-friendly insulation materials in tank insulation. Industries are increasingly focused on minimizing their environmental footprint and improving energy efficiency. Manufacturers are developing insulation solutions that are not only thermally efficient but also made from renewable or recyclable materials

- For Instance, Rockwool International A/S, which has been at the forefront of developing insulation products made from sustainable materials. Their mineral wool insulation solutions are designed to be highly energy-efficient while being recyclable, aligning with growing global sustainability goals

- The transition to a circular economy is influencing the tank insulation market. Companies are investing in materials that can be reused or recycled, reducing waste and fostering sustainability in the supply chain

- Many governments around the world are implementing stricter regulations related to energy efficiency in industrial sectors. This is pushing companies to adopt more advanced and sustainable insulation solutions that reduce energy consumption and improve temperature control for storage tanks

- Manufacturers of tank insulation are increasingly obtaining environmental certifications for their products, ensuring compliance with international standards such as LEED (Leadership in Energy and Environmental Design) and BREEAM (Building Research Establishment Environmental Assessment Method)

Tank Insulation Market Dynamics

Driver

“Increasing Energy Efficiency Demands”

- The primary driver of growth in the global tank insulation market is the increasing demand for energy efficiency. Insulated tanks help reduce energy loss during the storage and transportation of liquids, gases, and chemicals by maintaining temperature control. This is especially critical in sectors such as oil and gas, chemicals, and food processing, where temperature-sensitive materials are involved

- As the global energy crisis intensifies, industries are under pressure to optimize their energy consumption. Tank insulation solutions help minimize energy waste by maintaining the desired temperature, leading to significant energy savings

- Governments are implementing stricter regulations regarding energy use, particularly in high-consumption industries.

- For instance, the European Union's Energy Efficiency Directive mandates the reduction of energy use across industries, pushing companies to adopt solutions such as tank insulation to comply with these regulations

- Tank insulation reduces the need for additional energy resources by preventing heat loss or gain. This directly results in lower energy bills for companies that adopt these solutions, making it a cost-effective measure

- The oil and gas industry is one of the largest consumers of insulated tanks. With the growing focus on reducing operational costs, the demand for advanced insulation solutions is surging to ensure that thermal energy is not wasted during storage and transportation processes

Opportunity

“Growth in Emerging Markets”

- Emerging markets, particularly in regions such as Asia-Pacific, Latin America, and the Middle East, offer significant growth opportunities for the global tank insulation market. As these regions industrialize at a rapid pace, there is an increasing demand for tank insulation solutions across various sectors, including chemicals, oil and gas, and pharmaceuticals

- Countries in the Middle East and Asia are investing heavily in infrastructure development, including energy production and petrochemical plants. This creates opportunities for the tank insulation market, as these facilities require highly efficient thermal insulation for storage tanks to optimize energy use

- Governments in emerging markets are encouraging foreign investments and providing incentives for companies to adopt energy-efficient technologies. These incentives are a key opportunity for manufacturers of tank insulation solutions to expand their reach in these regions

- As renewable energy projects such as wind, solar, and bioenergy grow in emerging markets, there is an increasing need for efficient storage solutions. Insulated tanks are crucial in ensuring that energy storage systems function optimally, which presents an opportunity for insulation companies to cater to the renewable energy sector

- The growing food processing and pharmaceutical industries in emerging markets create new opportunities for tank insulation providers, as these industries require insulated storage tanks for temperature-sensitive materials

Restraint/Challenge

“High Initial Investment Costs”

- The installation of advanced tank insulation systems, particularly those made from high-performance materials, involves significant upfront capital investment. For many small and medium-sized enterprises (SMEs), this high initial cost can be a major barrier to adopting tank insulation solutions

- The return on investment (ROI) for insulated tanks, although positive in terms of energy savings, can take several years to materialize. This long payback period discourages many companies from making the initial investment, especially in industries with tighter profit margins

- Retrofitting existing tanks with new insulation systems can be complex and costly. Many companies face challenges when integrating insulation into their pre-existing infrastructure, leading to higher operational costs during the installation process

- The prices of raw materials used in insulation, such as fiberglass, mineral wool, and polyurethane, can fluctuate significantly. This price volatility can increase the overall cost of insulation systems and create uncertainty in the market

- In some developing regions, the awareness of the benefits of tank insulation is still low. Companies may not fully realize the long-term energy savings and operational efficiency gains that can be achieved through proper insulation, which limits market growth in these areas

Tank Insulation Market Scope

The market is segmented on the basis type, material type, temperature type, tank type, tank ends, and end-user.

|

Segmentation |

Sub-Segmentation |

|

By Type |

|

|

By Material Type |

|

|

By Temperature Type |

|

|

By Tank Type |

|

|

By Tank Ends |

|

|

By End-User |

|

In 2025, the rockwool and polyurethane (PU) is projected to dominate the market with a largest share in material type segment

The rockwool and polyurethane (PU) segment is expected to dominate the tank insulation market with the largest share of 31.5% in 2025 due to their high thermal insulation properties and versatility. These materials are widely used in industries such as oil and gas, chemicals, and energy due to their excellent ability to maintain the required temperature levels while ensuring energy efficiency.

The hot insulation is expected to account for the largest share during the forecast period in temperature market

In 2025, the got insulation segment is expected to dominate the market with the largest market share of 51.31% due to preventing heat loss and protecting equipment, ensuring that industrial processes remain within safe temperature limits. Hot insulation solutions help companies save on heating costs and reduce energy consumption, making this a highly demanded segment across various industries.

Tank Insulation Market Regional Analysis

“North America Holds the Largest Share in the Tank Insulation Market”

- North America remains a dominant player in the global tank insulation market due to its advanced infrastructure and continuous focus on technological innovations in insulation materials. The region is home to a highly developed chemical, oil & gas, and energy sector, all of which rely heavily on insulated tanks for storage and transportation of liquids and gases

- Stringent regulations related to energy efficiency and safety standards have prompted companies in North America to adopt tank insulation solutions. These regulations not only ensure operational safety but also contribute to energy conservation and reduction of carbon footprints

- The oil & gas sector, especially in the U.S. and Canada, is a major consumer of tank insulation, where insulated tanks are essential to maintaining temperature control for both storage and transportation. The sector's growth, driven by the need for storage tanks for crude oil and natural gas, further bolsters market demand

- North America has well-established manufacturing capabilities for tank insulation materials such as polyurethane, polystyrene, and fiberglass, enabling a strong supply chain to meet local and international demand

- Increasing investments in energy efficiency across various industries, especially in power generation and industrial manufacturing, have further driven the demand for insulated tanks in this region, making North America a market leader

“Asia-Pacific is Projected to Register the Highest CAGR in the Tank Insulation Market”

- The Asia-Pacific region, particularly countries such as China, India, and South Korea, is experiencing rapid industrialization and urbanization, which is driving significant demand for tank insulation solutions. Industries such as chemicals, oil & gas, and food processing are growing rapidly, creating a high need for insulated tanks

- Several governments in APAC are focusing on enhancing industrial infrastructure, which includes the construction of storage facilities and refineries that require tank insulation solutions. Government incentives for energy-efficient solutions and compliance with environmental regulations are contributing to the region's growth in this market

- As energy consumption in the region rises, particularly in emerging economies such as India and China, there is a growing need to store and transport energy-efficient materials, requiring the installation of insulated tanks to maintain temperature stability and minimize energy losses

- APAC is seeing significant growth in its petrochemical industry, with major projects coming online, particularly in countries such as China and India. These industries are among the biggest consumers of tank insulation systems to store chemicals at safe temperatures

- The adoption of more affordable and locally manufactured insulation materials, such as fiberglass and mineral wool, is driving market growth in the APAC region. The lower costs of production and raw materials have made insulated tank solutions more accessible to a larger number of companies in this region

Tank Insulation Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Commercial Thermal Solutions, Inc. (U.S.)

- Dow(U.S.)

- GILSULATE INTERNATIONAL, INC. (U.S.)

- ITW INSULATION SYSTEMS(U.S.)

- J.H. Ziegler GmbH(Germany)

- Knauf Insulation (U.S.)

- PolarClad Tank Insulation (U.S.)

- ARMACELL LLC (U.S.)

- Kingspan Group (Ireland)

- Synavax (U.S.)

- Johns Manville (U.S.)

- Mayes Coatings & Insulation, Inc. (U.S.)

- Thermacon (U.S.)

- Gulf Cool Therm Factory LTD (UAE)

- ROCKWOOL International A/S (Denmark)

- Cabot Corporation (U.S.)

- SPX Transformer Solutions Inc. (U.S.)

- DUNMORE (U.S.)

- T.F. Warren Group (U.S.)

- Saint-Gobain (France)

- Huntsman International LLC (U.S.)

- Corrosion Resistant Technologies, Inc. (U.S.)

- Röchling (Germany)

Latest Developments in Global Tank Insulation Market

- In May 2025, Rockwool International A/S Expands Product Line, the new products are designed with improved fire resistance and better thermal performance, catering to industries with stringent regulatory requirements

- In March 2025, Dow Launches New Polyurethane-Based Insulation, designed to enhance the performance and energy efficiency of tank insulation systems. The new product features improved thermal resistance properties and lower environmental impact due to the use of renewable materials

- In January 2025, Knauf Insulation Partners with Large Industrial Clients, to supply tank insulation materials for large-scale oil and gas refineries and chemical plants. The collaboration aims to enhance the energy efficiency of storage and transportation tanks used in these industries

- In December 2024, ITW Insulation Systems Launches Advanced Insulation Solutions for High-Temperature Applications, designed for hot tanks in the petrochemical industry. The products feature enhanced resistance to thermal stress and are designed to improve energy conservation in high-demand environments

- In September 2024, Johns Manville Introduces Recyclable Insulation Products, made from sustainable materials. These products are aimed at companies looking to reduce their environmental impact while maintaining high insulation performance

- In June 2024, Armacell LLC Expands Operations in Asia-Pacific, expanded its operations in the Asia-Pacific region by opening a new production facility in India. This facility will cater to the growing demand for tank insulation in industries such as oil & gas and chemicals

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

目次

グローバル・タンク・インシュレーション・マーケット

1 導入事例

1.1 スタディのOBJECTIVES 1.2 マーケットデファインション 1.3 グローバル・タンク・インシュレーション・マーケットの概観 1.4 レンタルおよび価格 1.5 制限 1.6 市場展開

2 市場調査

2.1 市場は、2.2 GEOGRAPHICAL SCOPE 2.3 年は、STUDY 2.4 CURRENCY と PRICING 2.5 DBMR TRIPOD DATA VALIDATION MODEL 2.6 テクノロジ LIFE LINE CURVE 2.7 MULTIVARIATE MODELLING 2.8 PRIMARY INTERVIEWS with KEY OPINION LEADERS 2.9 DBMR MARKET POSITION GRID 2.10 MARKET APPLICATION COVERS 2.7 DUSTAGEMENTS DUSTRIES 2.15 DUSTRUCTION DUSTRUCTION DUSTRIES 2.15 DUSTRIES

3 マーケット・オーバービュー

3.1 ドライバー

3.1.1 石油およびガス産業の3.1.2から開発を増加させ、LNGの貯蔵および輸送のCRYOGENICSの統合のために開発しました。 3.1.3 温度の制御パッケージの改良の低下 3.1.4 潜水艦を生産するタンクのMICAの区域の低下 3.1.4

3.2 削除

3.2.1 打撃の原料価格 3.2.2 タンクスの金属を造る鉄および鋼鉄企業のための重大な構造の変化の非可燃性 3.2.3 の非可燃性の材料の非可燃性 3.2.4 タンクスの金属を造る金属を造る鉄および鋼鉄企業のための非可燃性の材料 3.2.4 変化

3.3 機会

3.3.1 中国およびインド3.3.2の石油化学産業に成長するべきタンクのための高度のデマンド 3.3.2 増加する多国籍企業のための水タンクの器械の器械の器械の消費および商業建物の3.3.3増加の器械の消費の消費の減少 3.3.3

3.4 チャレンジ

3.4.1 TANK 3.4.2の消費物質との化学的作用に対する直観的かつ拡張の必要性。

4 エグゼクティブ ミーティング 5 プレミアムINSIGHTS 6つの企業INSIGHTS 7つの全体的なタンクの統合の市場、タイプによって

7.1 OVERVIEW 7.2 ストレージ 7.3 輸送

8つの全体的なタンクの絶縁の市場、物質的なタイプによって

8.1 OVERVIEW 8.2 拡張ポリスチレン(EPS) 8.3 ROCKWOOL 8.4 セルラー ガラス 8.5 ファイバーグラス 8.6 エラスティック フォーム 8.7 ポリウレタン (PU) 8.8 その他

9 全体的なタンクの絶縁材の市場、温度によって

9.1 概要 9.2 熱い絶縁材 9.3 冷たい絶縁材

10 全体的なタンクの絶縁の市場、タンク タイプによって

10.1 オーバービュー 10.2 垂直タンク 10.3 水平タンク 10.4 固定タンク 10.5 回転タンク

11 グローバル・タンク・インシュレーション・マーケット、タンク・エンズ

11.1 OVERVIEW 11.2 パラボリックディッシュ 11.3 FLAT

エンドユーザーによる12のグローバルタンクの統合の市場、

12.1オーバービュー 12.2 オイルとガス

12.2.1 オイル

12.2.1.1 原油 12.2.1.2 石油化学 12.2.1.3 その他の原油 DERIVATIVES

12.2.2 ガス

12.2.2.1 ナチュラルガス 12.2.2.2 SYNTHETIC GAS

12.3 エネルギーおよび力 12.4 化学 12.5 食糧および飲料

12.5.1 食品 12.5.2 飲料

12.5.2.1 アルコール飲料 12.5.2.2 乳製品 12.5.2.3 乾燥液 12.5.2.4 ジュースと赤水 12.5.2.5 その他

12.6 水質浄化

12.6.1 商業ビル 12.6.2 ミュンヘン 12.6.3 居住ビル

12.7 廃水処理

12.7.1 商業ビル 12.7.2 ミュンヘン 12.7.3 居住ビル

12.8 その他

13 グローバル・タンク・インシュレーション・マーケット、GEOGRAPHY

13.1 OVERVIEW 13.2 ノースアメリカ

13.2.1 米国 13.2.2 カナダ 13.2.3 メキシコ

13.3 ヨーロッパ

13.3.1 ドイツ 13.3.2 U.K 13.3.3 イタリア 13.3.4 フランス 13.3.5 スペイン 13.3.6 スイス 13.3.7 ロシア 13.3.8 トルコ 13.3.8 トルコ 13.3.10 オランダ EUROPEの 13.3.11 REST

13.4 アジアパシフィック

13.4.1 中国 13.4.2 インド 13.4.3 南アフリカ 13.4.4 日本 13.4.5 オーストラリア 13.4.6 シンガポール 13.4.7 タイ 13.4.7 インドネシア 13.4.9 マレーシア 13.4.10 フィリピン 13.4.11 アジアパシフィックのREST

13.5 南アフリカ

13.5.1 ブラジル 13.5.2 アルゼンチン 13.5.3 南アフリカ共和国の残りの部分

13.6 中東とアフリカ

13.6.1 UAE 13.6.2 サウジアラビア 13.6.3 イスラエル 13.6.4 南アフリカ 13.6.5 エジプト イーストとアフリカの 13.6.6 REST

14 グローバル・タンク・インシュレーション・マーケット、カンパニー・ランドスケープ

14.1 会社の SHARE ANALYSIS: グローバル14.2 カンパニー シャール分析: 北アメリカ14.3 カンパニー シャール分析: EUROPE 14.4 カンパニー シャール分析: ASIA- PACIFIC 14.5 測定器 & 機器 14.6 新製品開発とアプリケーション 14.7 機器 14.8 部品およびその他 STRATEGIC 開発

15 会社案内

15.1 BASFのSE

15.1.1 会社案内 15.1.2 SWOT分析 15.1.3 リアルタイム分析 15.1.4 会社案内 15.1.5 GEOGRAPHICAL PRESENCE 15.1.6 製品ポートフォリオ 15.1.7 リリース予定 15.1.8 データブリッジ市場分析

15.2 DOWケミカルカンパニー

15.2.1 会社案内 15.2.2 SWOT分析 15.2.3 リアルタイム分析 15.2.4 会社案内 15.2.5 地理的プレゼンス 15.2.6 製品PORTFOLIO 15.2.7 最近の開発 15.2.8 データブリッジ市場分析

15.3 サイント・ゴーベン

15.3.1 会社案内 15.3.2 SWOT分析 15.3.3 リアルタイム分析 15.3.4 会社案内 15.3.5 地理的プレゼンス 15.3.6 製品PORTFOLIO 15.3.7 最近の開発 15.3.8 データブリッジ市場分析

15.4 ヒトインターナショナル合同会社

15.4.1 会社案内 15.4.2 SWOT分析 15.4.3 到着分析 15.4.4 会社案内 分析 15.4.5 地理的プレゼンス 15.4.6 製品PORTFOLIO 15.4.7 最近の開発 15.4.8 データブリッジ市場分析

15.5 キングスパングループ

15.5.1 会社案内 15.5.2 SWOT分析 15.5.3 リアルタイム分析 15.5.4 会社案内 15.5.5 地理的プレゼンス 15.5.6 製品ポートフォリオ 15.5.7 最近の開発 15.5.8 データブリッジ市場分析

15.6 アルマセル合同会社

15.6.1 会社案内 15.6.2 到着分析 15.6.3 GEOGRAPHICAL プレゼンス 15.6.4 製品ポートフォリオ 15.6.5 リリース開発

15.7 キャボット株式会社

15.7.1 会社案内 15.7.2 到着分析 15.7.3 ジオグラフィック プレゼンス 15.7.4 製品ポートフォリオ 15.7.5 リリース開発

15.8 商業施設

15.8.1 会社の SNAPSHOT 15.8.2 プロダクト PORTFOLIO 15.8.3 最近の開発

15.9 CORROSION RESISTANTの技術、株式会社。

15.9.1 会社 SNAPSHOT 15.9.2 製品PORTFOLIO 15.9.3 最近の開発

15.10 ダンモア

15.10.1 会社の SNAPSHOT 15.10.2 の GEOGRAPHICAL のプレゼンス 15.10.3 プロダクト PORTFOLIO 15.10.4 の現在の進歩

15.11 GILSULATE INTERNATIONAL, INC. 株式会社ジルレートインターナショナル

15.11.1 会社 SNAPSHOT 15.11.2 プロダクト PORTFOLIO 15.11.3 最近の開発

15.12 ガルフクールサーム工場株式会社

15.12.1 会社 SNAPSHOT 15.12.2 プロダクト PORTFOLIO 15.12.3 最近の開発

15.13 ITWシステム

15.13.1 会社 SNAPSHOT 15.13.2 GEOGRAPHICAL PRESENCE 15.13.3 PRODUCT PORTFOLIO 15.13.4 最近の開発

15.14 ジョンズ・マニビル

15.14.1 会社 SNAPSHOT 15.14.2 GEOGRAPHICAL PRESENCE 15.14.3 プロダクト PORTFOLIO 15.14.4 最近の開発

15.15 J.H. ZIEGLER GMBHの特長

15.15.1 会社の SNAPSHOT 15.15.2 ジオグラフィック プレゼンス 15.15.3 プロダクト PORTFOLIO 15.15.4 最近の開発

15.16 KNAUF の絶縁

15.16.1 Company SNAPSHOT 15.16.2 GEOGRAPHICAL PRESENCE 15.16.3 PRODUCT PORTFOLIO 15.16.4 リリース予定

15.17 メイズコーティング&インシュレーション株式会社

15.17.1 企業 SNAPSHOT 15.17.2 プロダクト PORTFOLIO 15.17.3 最近の開発

15.18 オーウェンズ コーニング

15.18.1 会社の SNAPSHOT 15.18.2 到着分析 15.18.3 GEOGRAPHICAL プレゼンス 15.18.4 プロダクト PORTFOLIO 15.18.5 最近の開発

15.19 ポーラッド・タンク・インシュレーション

15.19.1 会社 SNAPSHOT 15.19.2 製品PORTFOLIO 15.19.3 最近の開発

15.20 ローチリンググループ

15.20.1 会社の SNAPSHOT 15.20.2 ジオグラフィック プレゼンス 15.20.3 プロダクト PORTFOLIO 15.20.4 最近の開発

15.21 ROCKWOOL 国際A/S

15.21.1 会社案内 SNAPSHOT 15.21.2 到着分析 15.21.3 GEOGRAPHICAL プレゼンス 15.21.4 プロダクト PORTFOLIO 15.21.5 最近の開発

15.22 SPXトランスソリューションズ株式会社

15.22.1 会社 SNAPSHOT 15.22.2 PRODUCT PORTFOLIO 15.22.3 最近の開発

15.23 シンボル

15.23.1 会社 SNAPSHOT 15.23.23.2 ソリューションPORTFOLIO 15.23.3 最近の開発

15.24 サーマコン

15.24.1 会社の SNAPSHOT 15.24.2 プロダクト PORTFOLIO 15.24.3 最近の開発

15.25 T.F.WARRENグループ

15.25.1 会社 SNAPSHOT 15.25.25.2 地理的存在 15.25.3 プロダクト PORTFOLIO 15.25.4 最近の開発

16 質問会議 17 コンセプト 18 関連するレポート

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。