North America Data Center Interconnect Market Size, Share, and Trends Analysis Report

Market Size in USD Billion

CAGR :

%

USD

3.37 Billion

USD

8.43 Billion

2025

2033

USD

3.37 Billion

USD

8.43 Billion

2025

2033

| 2026 –2033 | |

| USD 3.37 Billion | |

| USD 8.43 Billion | |

| % | |

|

North America Data Center Interconnect Market Segmentation, By Product (Software, and Services), Technology (CSPs, CNPs/ICPs, Government, and Enterprises), Application (Real-Time Disaster Recovery and Business Continuity, Shared Data and Resources/Server High-Availability Clusters (Geoclustering) Consumer and Workload (VM), and Data (Storage) Mobility) - Industry Trends and Forecast to 2033

North America Data Center Interconnect Market Size

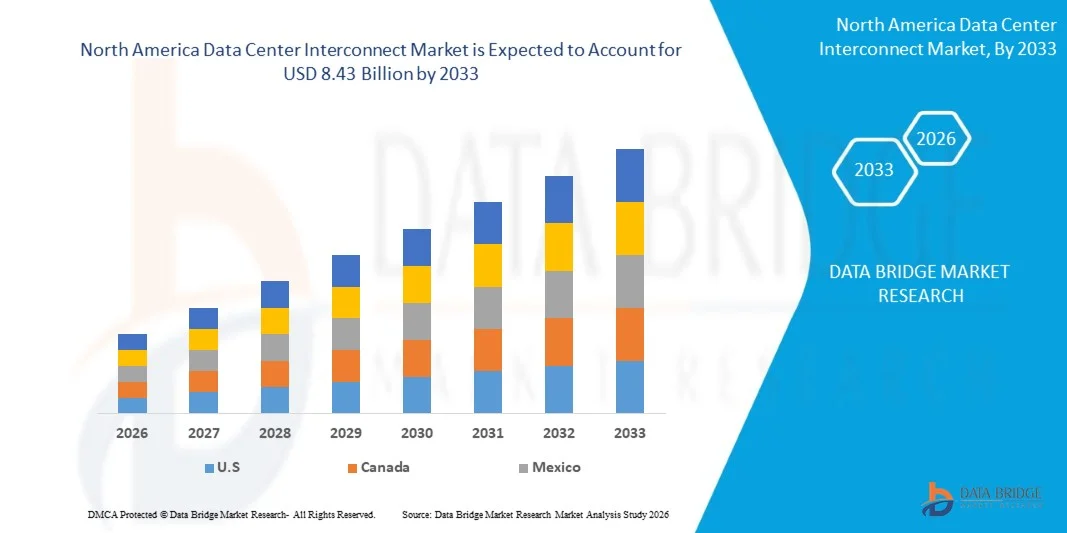

- The North America Data Center Interconnect Market size was valued at USD 3.37 billion in 2025 and is expected to reach USD 8.43 billion by 2033, at a CAGR of 12.15% during the forecast period

- The market growth is largely fueled by the rapid expansion of cloud computing, increasing data traffic, and the growing need for high-speed and low-latency connectivity between geographically dispersed data centers, driving significant investments in advanced interconnect infrastructure across industries

- Furthermore, the rising adoption of hybrid and multi-cloud architectures along with the increasing demand for real-time data processing and seamless workload mobility is positioning data center interconnect solutions as a critical component of modern digital infrastructure, thereby accelerating overall market growth

North America Data Center Interconnect Market Analysis

- Data center interconnect solutions, enabling high-capacity data transfer and seamless connectivity between multiple data centers, are becoming essential for organizations to ensure efficient data management, business continuity, and scalable IT operations across distributed environments

- The growing demand for data center interconnect is primarily driven by the surge in digital transformation initiatives, increasing reliance on cloud services, and the need for secure and reliable data transmission, supporting the continuous evolution of enterprise networking and global data exchange infrastructure

- U.S. dominated the North America Data Center Interconnect Market in 2025, due to the strong presence of hyperscale data centers, rapid adoption of cloud computing, and increasing demand for high-speed data transfer across enterprises and service providers, supported by advanced digital infrastructure and early adoption of interconnect technologies

- Canada is expected to be the fastest growing country in the North America Data Center Interconnect Market during the forecast period due to increasing investments in hyperscale data centers, rising adoption of cloud services, and growing demand for secure and low-latency connectivity solutions

- Software segment dominated the market with a market share of 59.1% in 2025, due to the rising demand for network virtualization, automation, and intelligent traffic management across distributed data center environments. Organizations are increasingly adopting software-defined interconnect solutions to enable flexible bandwidth allocation, real-time analytics, and improved network visibility. The growing shift toward hybrid and multi-cloud architectures further strengthens the demand for software platforms that can seamlessly orchestrate connectivity between geographically dispersed data centers

Report Scope and North America Data Center Interconnect Market Segmentation

|

Attributes |

Data Center Interconnect Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

North America Data Center Interconnect Market Trends

“Increasing Adoption of Software-Defined Data Center Interconnect Solutions”

- A significant trend in the North America Data Center Interconnect Market is the increasing adoption of software-defined solutions that enable dynamic bandwidth allocation, automated traffic management, and enhanced network visibility across distributed data center environments. This trend is transforming traditional interconnect architectures into more flexible and scalable systems capable of supporting evolving digital workloads

- For instance, Juniper Networks offers software-defined networking solutions through its Apstra platform, enabling automated data center fabric management and optimized interconnect performance across multi-site environments. Such implementations improve operational efficiency and reduce manual configuration complexities in large-scale networks

- Enterprises are increasingly deploying SDN-based interconnect solutions to support hybrid and multi-cloud strategies where seamless workload mobility and real-time data exchange are critical. This is enhancing the ability of organizations to manage distributed infrastructure with greater control and agility

- Cloud service providers are integrating intelligent orchestration tools within interconnect frameworks to ensure efficient resource utilization and low-latency connectivity. This is strengthening the role of software-defined approaches in enabling high-performance cloud services across global regions

- The growing demand for automation and analytics-driven network management is encouraging the integration of AI and machine learning capabilities within interconnect platforms. This is improving predictive maintenance, fault detection, and overall network reliability in complex environments

- The market is witnessing a steady transition toward programmable and scalable interconnect architectures that support rapid deployment and efficient scaling of data center operations. This trend is reinforcing the shift toward software-driven networking models and strengthening the overall evolution of modern digital infrastructure

North America Data Center Interconnect Market Dynamics

Driver

“Rising Demand for High-Speed and Low-Latency Data Transmission”

- The increasing volume of data generated from cloud computing, streaming services, and enterprise applications is driving the demand for high-speed and low-latency interconnect solutions that ensure efficient data transfer between geographically distributed data centers. These solutions are essential for maintaining performance and responsiveness in data-intensive environments

- For instance, Ciena Corporation provides high-capacity optical interconnect solutions that enable hyperscale data centers to handle large-scale data traffic with minimal latency. These technologies support efficient data movement and enhance overall network performance across global infrastructures

- The expansion of hyperscale data centers is further accelerating the need for high-bandwidth connectivity solutions that can support increasing workloads and user demands. This is driving continuous innovation in optical networking technologies and interconnect architectures

- The adoption of emerging technologies such as 5G, artificial intelligence, and edge computing is increasing the requirement for real-time data processing and ultra-fast connectivity. These applications rely heavily on robust interconnect systems to ensure seamless performance and low latency

- The growing expectation for uninterrupted digital services and real-time data access continues to strengthen this driver. The need for faster and more reliable data transmission is positioning data center interconnect solutions as critical enablers of global digital transformation

Restraint/Challenge

“High Deployment Costs and Complex Network Management”

- The North America Data Center Interconnect Market faces challenges due to the high costs associated with deploying advanced networking infrastructure, including optical fiber systems, switching equipment, and high-capacity transmission technologies. These investments create financial barriers, particularly for small and medium-sized enterprises

- For instance, Nokia delivers high-performance optical transport solutions that require significant capital expenditure for deployment and integration within large-scale data center environments. These costs can limit adoption among organizations with constrained budgets

- Managing complex interconnect networks across multiple locations requires advanced technical expertise and sophisticated monitoring tools to ensure consistent performance and security. This increases operational complexity and demands continuous investment in skilled personnel and system upgrades

- The integration of legacy infrastructure with modern interconnect solutions presents additional challenges in achieving seamless connectivity and interoperability. Organizations often face difficulties in upgrading existing systems without disrupting ongoing operations

- The market continues to face constraints in balancing high-performance requirements with cost efficiency and operational simplicity. These challenges are influencing adoption rates and encouraging vendors to develop more cost-effective and user-friendly interconnect solutions

North America Data Center Interconnect Market Scope

The market is segmented on the basis of product, technology, and application.

• By Product

On the basis of product, the North America Data Center Interconnect Market is segmented into software and services. The software segment dominated the market with the largest revenue share of 59.1% in 2025, driven by the rising demand for network virtualization, automation, and intelligent traffic management across distributed data center environments. Organizations are increasingly adopting software-defined interconnect solutions to enable flexible bandwidth allocation, real-time analytics, and improved network visibility. The growing shift toward hybrid and multi-cloud architectures further strengthens the demand for software platforms that can seamlessly orchestrate connectivity between geographically dispersed data centers. In addition, advancements in SDN and NFV technologies continue to enhance scalability and operational efficiency, reinforcing the dominance of the software segment.

The services segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the increasing complexity of interconnect deployments and the need for specialized expertise in design, integration, and maintenance. Enterprises are relying on managed and professional services to ensure optimal performance, security, and compliance of their interconnect infrastructure. The rapid expansion of hyperscale data centers and cloud service providers is also driving demand for consulting and support services. Furthermore, continuous monitoring and optimization requirements are encouraging long-term service engagements, contributing to the accelerated growth of the services segment.

• By Technology

On the basis of technology, the North America Data Center Interconnect Market is segmented into CSPs, CNPs/ICPs, Government, and Enterprises. The CSPs segment dominated the market with the largest revenue share in 2025, driven by the massive investments of cloud service providers in expanding global data center footprints and ensuring high-speed connectivity. These providers require robust interconnect solutions to support large-scale data transfer, latency-sensitive applications, and seamless cloud service delivery. The increasing adoption of edge computing and content delivery networks further strengthens the demand for efficient interconnect technologies among CSPs. In addition, continuous innovation in optical networking and high-capacity transmission technologies enhances performance, reinforcing the leadership of this segment.

The CNPs/ICPs segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the rapid growth of digital content consumption, streaming services, and internet-based platforms. These players require scalable and high-bandwidth interconnect solutions to manage increasing data traffic and ensure uninterrupted user experience. The expansion of global internet penetration and rising demand for low-latency content delivery are further accelerating investments in interconnect infrastructure. Moreover, the need to support data-intensive applications and real-time services continues to propel the growth of this segment.

• By Application

On the basis of application, the North America Data Center Interconnect Market is segmented into Real-Time Disaster Recovery and Business Continuity, Shared Data and Resources/Server High-Availability Clusters (Geoclustering), Consumer and Workload (VM), and Data (Storage) Mobility. The Real-Time Disaster Recovery and Business Continuity segment dominated the market with the largest revenue share in 2025, driven by the critical need for uninterrupted operations and data protection across enterprises. Organizations are increasingly deploying interconnect solutions to ensure instant data replication and failover capabilities between geographically dispersed data centers. The rising frequency of cyber threats, system failures, and natural disruptions further emphasizes the importance of resilient interconnect infrastructure. In addition, stringent regulatory requirements for data availability and security are reinforcing the demand for real-time recovery solutions.

The Consumer and Workload (VM) segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the increasing adoption of virtualization, cloud computing, and dynamic workload management. Enterprises are leveraging interconnect solutions to enable seamless migration of virtual machines and applications across data centers for improved efficiency and scalability. The growing demand for flexible computing environments and optimized resource utilization is further driving this segment. Furthermore, the rise of containerization and microservices architectures is accelerating the need for efficient workload mobility, contributing to its rapid growth.

North America Data Center Interconnect Market Regional Analysis

- U.S. dominated the North America Data Center Interconnect Market with the largest revenue share in 2025, driven by the strong presence of hyperscale data centers, rapid adoption of cloud computing, and increasing demand for high-speed data transfer across enterprises and service providers, supported by advanced digital infrastructure and early adoption of interconnect technologies

- The demand for advanced data center interconnect solutions is supported by large-scale investments and deployments by companies such as Equinix, Inc. and Digital Realty Trust, enabling seamless connectivity across applications including cloud services, disaster recovery, content delivery, and enterprise networking

- The presence of major technology providers, continuous advancements in optical networking and software-defined networking, and increasing integration of multi-cloud and hybrid cloud environments reinforce the U.S. leadership position in the North America market

Canada North America Data Center Interconnect Market Insight

Canada is projected to register the fastest CAGR in the North America Data Center Interconnect Market from 2026 to 2033, supported by increasing investments in hyperscale data centers, rising adoption of cloud services, and growing demand for secure and low-latency connectivity solutions. The expansion of digital infrastructure and strong government support for data localization and data privacy are accelerating market growth. The development of advanced connectivity solutions and collaborations with companies such as Ciena Corporation are strengthening technological capabilities across the country. Growing emphasis on digital transformation, edge computing, and high-capacity data transfer positions Canada as the fastest-growing country in the region during the forecast period.

Mexico North America Data Center Interconnect Market Insight

Mexico is expected to grow steadily from 2026 to 2033, driven by increasing demand for cloud-based services, expansion of data center infrastructure, and rising adoption of digital technologies across enterprises. The country’s improving telecommunications infrastructure and growing internet penetration are supporting the deployment of interconnect solutions across industries. Collaborations with global technology providers and increasing investments in network modernization are enhancing connectivity capabilities. Major companies such as Megaport and Nokia are strengthening their presence in the region. These developments contribute to sustained growth of the North America Data Center Interconnect Market throughout the forecast period.

North America Data Center Interconnect Market Share

The data center interconnect industry is primarily led by well-established companies, including:

- Equinix, Inc. (U.S.)

- Digital Realty Trust (U.S.)

- Ciena Corporation (U.S.)

- Nokia (Finland)

- Huawei Technologies Co., Ltd. (China)

- ADVA Optical Networking (Germany)

- Juniper Networks, Inc. (U.S.)

- Colt Technology Services Group Limited (U.K.)

- Extreme Networks, Inc. (U.S.)

- Fiber Mountain, Inc. (U.S.)

- Pluribus Networks (U.S.)

- ZTE Corporation (China)

- RANOVUS Inc. (Canada)

- FUJITSU (Japan)

- Megaport (Australia)

Latest Developments in North America Data Center Interconnect Market

- In November 2024, Nokia Corporation partnered with Cloudbear to deploy an advanced data center networking infrastructure built on a Kubernetes environment. This implementation leverages Nokia’s high-performance data center fabric switching and gateway routers, enabling improved traffic management, scalability, and seamless orchestration of cloud-native applications. The deployment enhances Cloudbear’s ability to deliver customized and efficient hosting services while ensuring optimized workload distribution. The collaboration focuses on boosting speed, reliability, and security, helping Cloudbear meet evolving enterprise requirements and deliver consistent service performance across diverse customer environments

- In November 2024, Virgin Media O2 partnered with Ciena Corporation (U.S.) to successfully launch a Converged Interconnect Network (CIN), integrating its fixed and mobile networks to manage both types of traffic seamlessly. This next-generation network architecture enhances bandwidth efficiency and reduces latency by unifying infrastructure layers. The CIN is designed for high scalability, enabling the company to respond quickly to increasing data consumption and emerging digital services. By consolidating its networks, Virgin Media O2 strengthens operational resilience, improves service delivery, and enhances overall customer experience across both consumer and enterprise segments

- In November 2024, Adtran announced a strategic partnership with Sonic Fiber Internet (U.S.) to roll out 50Gbit/s passive optical network (50G PON) connectivity in California. This initiative significantly increases network capacity and enables ultra-fast data transmission speeds to support bandwidth-intensive applications. The collaboration enhances Sonic’s infrastructure to accommodate growing demand for high-speed broadband services across residential and commercial users. Leveraging Adtran’s advanced fiber access technology, Sonic is positioned to deliver improved service reliability, reduced latency, and scalable connectivity solutions aligned with future digital consumption trends

- In October 2024, Juniper Networks announced that Seoul Semiconductor (South Korea) has deployed its AI-Native Networking Platform to enhance both wired and wireless access services. Powered by Mist AI™, the platform enables intelligent automation, proactive issue detection, and real-time performance optimization. This upgrade supports increased employee productivity by ensuring consistent connectivity and minimizing network disruptions. Utilizing advanced AIOps and microservices-based cloud architecture, the solution reduces operational complexity and costs while delivering a highly reliable and measurable network experience for both users and IT teams

- In October 2024, Megaport expanded its footprint in Europe by adding 14 new data center locations across seven countries and forming strategic partnerships with Portus Data Centers, NorthC Data Centers, and Sipartech. This expansion strengthens Megaport’s ability to deliver its Network as a Service (NaaS) solutions with greater geographic reach and interconnection flexibility. Customers benefit from enhanced access to a broader ecosystem of cloud providers, enterprises, and network services. The initiative supports faster provisioning, improved scalability, and seamless connectivity, reinforcing Megaport’s position in the rapidly growing interconnect market

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。