Asia Pacific Dental Instruments Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

2.23 Billion

USD

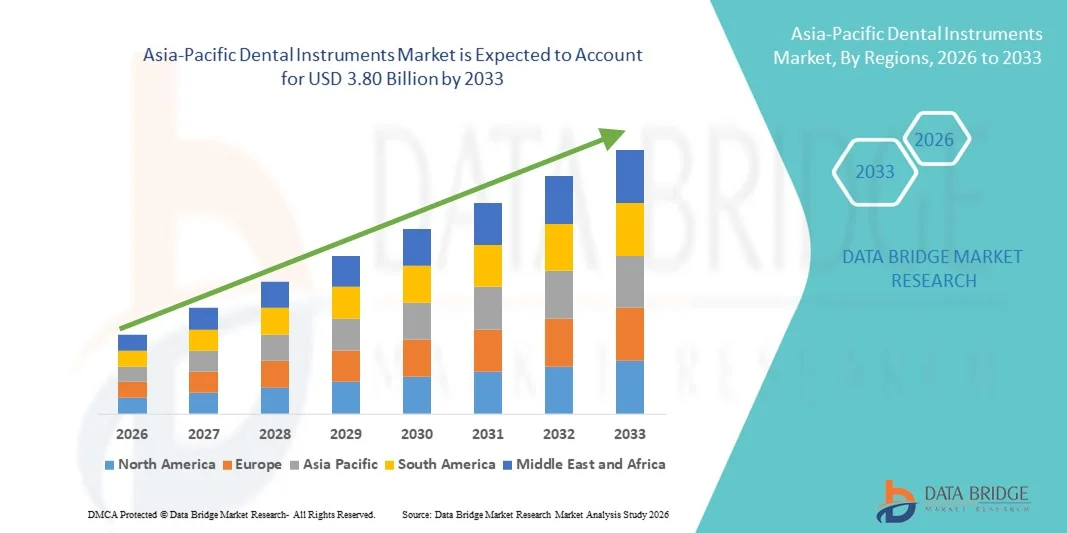

3.80 Billion

2025

2033

USD

2.23 Billion

USD

3.80 Billion

2025

2033

| 2026 –2033 | |

| USD 2.23 Billion | |

| USD 3.80 Billion | |

| % | |

|

아시아 태평양 치과 기구 시장 세분화: 제품별(치주/구강외과, 위생, 진단, 근관치료, 수술 및 기타), 기구 유형별(검사 기구, 절삭 기구 및 기타), 최종 사용자별(병원, 클리닉, 치과 기공소, 과학 연구 기관 및 기타), 유통 채널별(직접 입찰, 제3자 유통업체 및 소매 판매) - 산업 동향 및 2033년까지의 전망

아시아 태평양 치과 기기 시장 규모

- 아시아 태평양 치과 기기 시장 규모는 2025년 22억 3천만 달러 였으며 , 예측 기간 동안 연평균 성장률(CAGR) 6.90% 로 성장하여 2033년에는 38억 달러 에 이를 것으로 예상됩니다 .

- 시장 성장은 주로 치과 질환의 유병률 증가, 구강 위생에 대한 인식 제고, 치과 진료 장비의 기술 발전으로 인해 병원, 의원 및 전문 치과 센터 전반에 걸쳐 첨단 치과 기기의 도입이 확대됨에 따라 촉진되고 있습니다.

- 더욱이, 심미 및 보철 치과 시술에 대한 수요 증가, 의료비 지출 증가, 그리고 최소 침습 및 정밀 치과 기기의 지속적인 혁신은 치과 기기를 현대 치의학에서 필수적인 도구로 자리매김하게 하고 있습니다. 이러한 여러 요인이 복합적으로 작용하여 치과 기기 솔루션의 도입을 가속화하고 있으며, 이는 업계의 성장을 크게 촉진하고 있습니다.

아시아 태평양 치과 기기 시장 분석

- 다양한 진단, 예방, 복원 및 수술 도구를 포함하는 치과 기구는 정확한 진단, 정밀한 치료 및 환자 결과 개선에 중요한 역할을 하므로 병원, 치과 병원 및 학술 기관을 포함한 현대 구강 건강 관리 제공의 필수 구성 요소입니다.

- 치과 기구에 대한 수요 증가는 주로 충치, 치주 질환 및 치아 상실의 유병률 증가와 구강 위생에 대한 인식 제고, 심미 치과 시술에 대한 수요 증가, 그리고 최소 침습적이고 인체공학적인 기구 설계 분야의 지속적인 기술 발전에 기인합니다.

- 중국은 방대한 환자 인구, 성장하는 중산층, 빠른 도시화, 그리고 의료 인프라에 대한 상당한 투자에 힘입어 2025년까지 아시아 태평양 치과 기기 시장에서 31.8%의 최대 매출 점유율을 기록하며 주도적인 위치를 차지할 것으로 예상됩니다. 중국 내 민간 치과 병원 네트워크의 확장, 구강 위생에 대한 인식 제고, 그리고 심미 및 보철 치과 시술에 대한 수요 증가는 첨단 기술과 경제성을 갖춘 치과 기기의 도입을 더욱 촉진할 것입니다.

- 인도는 치과 관광 증가, 가처분 소득 증가, 치과 교육 기관 확충, 도시 및 준도시 지역의 구강 건강 관리 서비스 접근성 향상 등에 힘입어 예측 기간 동안 아시아 태평양 지역에서 가장 빠르게 성장하는 치과 기기 시장이 될 것으로 예상됩니다. 인도는 2025년까지 아시아 태평양 지역 시장 점유율의 약 18.6%를 차지할 것으로 전망되며, 최첨단 치과 기술에 대한 지속적인 투자와 병원 확장이 시장 성장을 더욱 가속화하고 있습니다.

- 검사 기기 부문은 일상적인 치과 진단 및 검진에서 필수적인 역할을 담당함에 따라 2025년에 34.8%의 가장 큰 시장 매출 점유율을 차지했습니다.

보고서 범위 및 치과 기기 시장 세분화

|

속성 |

치과 기기 시장 주요 분석 |

|

포함되는 부문 |

|

|

대상 국가 |

아시아태평양

|

|

주요 시장 참여자 |

|

|

시장 기회 |

|

|

부가가치 데이터 정보세트 |

데이터 브리지 마켓 리서치에서 제공하는 시장 보고서는 시장 가치, 성장률, 시장 세분화, 지리적 범위 및 주요 업체와 같은 시장 시나리오에 대한 통찰력 외에도 심층적인 전문가 분석, 환자 역학, 파이프라인 분석, 가격 분석 및 규제 체계에 대한 정보를 포함합니다. |

아시아 태평양 치과 기기 시장 동향

첨단 및 최소 침습 치과 기술의 도입 증가

- A significant and accelerating trend in the dental instruments market is the growing adoption of advanced, precision-based, and minimally invasive dental technologies across clinics and hospitals. Dental professionals are increasingly shifting toward high-performance instruments that enhance procedural accuracy, reduce patient discomfort, and improve overall treatment outcomes. This transition is being supported by technological advancements in rotary instruments, digital imaging-compatible tools, ergonomic handpieces, and laser-assisted dental devices

- For instance, several leading dental clinics in Germany and France have upgraded to next-generation electric handpieces and precision endodontic instruments that enable faster root canal procedures with improved accuracy and reduced chair time. Such upgrades are improving workflow efficiency while enhancing patient satisfaction

- The increasing focus on cosmetic dentistry, including veneers, teeth whitening, and smile correction procedures, is further accelerating the demand for specialized dental instruments designed for aesthetic precision

- In addition, the integration of digital dentistry solutions, such as CAD/CAM-supported restorative tools and implantology instrument kits, is enabling more accurate and customized treatment planning

- The growing emphasis on infection control and sterilization standards in European dental practices is also encouraging the adoption of high-quality stainless steel and autoclavable instruments that ensure safety and regulatory compliance

- This trend toward technologically advanced, ergonomic, and procedure-specific dental instruments is reshaping clinical practices across Europe, prompting manufacturers to continuously innovate and expand their product portfolios

Asia-Pacific Dental Instruments Market Dynamics

Driver

Increasing Prevalence of Dental Disorders and Growing Geriatric Population

- The rising prevalence of dental conditions such as dental caries, periodontal diseases, tooth loss, and oral infections is a major driver for the Dental Instruments market. Poor dietary habits, tobacco consumption, and inadequate oral hygiene practices continue to increase the burden of oral diseases across

- For instance, according to European oral health reports, a significant proportion of adults suffer from untreated dental caries and gum disease, prompting governments and healthcare providers to expand preventive and restorative dental services. This growing patient pool directly increases the demand for diagnostic, surgical, and restorative dental instruments

- The rapidly growing geriatric population in countries further contributes to market expansion, as older individuals are more prone to tooth decay, edentulism, and implant procedures

- Increasing awareness campaigns promoting preventive dental check-ups and early diagnosis are encouraging more frequent dental visits, thereby boosting procedural volumes and instrument demand

- Furthermore, the expansion of private dental clinics and cosmetic dentistry centers is increasing procurement of advanced dental surgical tools, implant kits, orthodontic instruments, and restorative devices

Restraint/Challenge

High Equipment Costs and Stringent Regulatory Requirements

- The high cost of advanced dental instruments, particularly specialized surgical kits, implantology systems, and digital-compatible tools, remains a significant challenge for small and mid-sized dental practices

- For instance, premium implant surgical instrument systems and precision rotary tools require substantial capital investment, limiting adoption among newly established clinics or independent practitioners

- Strict regulatory requirements under European medical device regulations (MDR) impose rigorous quality, safety, and documentation standards on manufacturers, increasing compliance costs and extending product approval timelines

- In addition, the need for continuous training and skill development to effectively use advanced dental instruments can create operational challenges for clinics lacking adequate technical expertise

- Economic uncertainties and reimbursement limitations in certain European countries may also reduce discretionary spending on cosmetic dental procedures, indirectly affecting the procurement of specialized dental instruments

- Overcoming these challenges through cost-effective product development, regulatory compliance strategies, and training initiatives will be essential for sustained market growth across the region

Asia-Pacific Dental Instruments Market Scope

The market is segmented on the basis of product, instrument type, end user, and distribution channel.

- By Product

On the basis of product, the Dental Instruments market is segmented into Perio/Oral Surgery, Hygiene, Diagnostic, Endodontic, Operative, and Others. The Hygiene segment dominated the largest market revenue share of 29.4% in 2025, driven by the rising global emphasis on preventive dental care and routine oral check-ups. Increasing awareness regarding oral health and gum diseases has significantly boosted the demand for scaling and cleaning instruments. Dental hygienists frequently use ultrasonic scalers, curettes, and polishing instruments in routine procedures, ensuring consistent demand. The growth of cosmetic dentistry and teeth whitening procedures further supports segment expansion. Government initiatives promoting preventive dental care programs have also strengthened hygiene instrument adoption. Technological advancements in ultrasonic and air-polishing devices have improved efficiency and patient comfort. The segment benefits from high procedure frequency compared to surgical treatments. Dental clinics increasingly invest in advanced hygiene tools to enhance operational productivity. The rise in dental insurance coverage for preventive services further stimulates demand. Expanding dental tourism markets also contribute to higher procedure volumes. Continuous product innovation and ergonomic instrument design improve practitioner comfort and efficiency. The growing aging population susceptible to periodontal diseases further solidifies its leading position.

The Endodontic segment is anticipated to witness the fastest CAGR of 8.6% from 2026 to 2033, fueled by the increasing prevalence of dental caries and root canal procedures worldwide. Rising consumption of sugary foods and beverages has led to higher incidences of pulp infections, driving procedural demand. Advancements in rotary endodontic systems and nickel-titanium instruments have significantly improved treatment precision and reduced procedure time. Growing awareness about tooth preservation rather than extraction is encouraging patients to opt for endodontic treatments. Increased access to dental care facilities in emerging economies further supports segment growth. Technological integration such as digital apex locators and endodontic motors enhances clinical outcomes. Dental professionals increasingly prefer minimally invasive root canal techniques, boosting instrument adoption. Expansion of dental clinics and specialty practices contributes to higher demand. The segment also benefits from rising dental insurance reimbursement policies. Educational training programs for advanced endodontic techniques increase practitioner adoption rates. Improved sterilization standards encourage replacement demand for endodontic files and tools. Growing geriatric populations prone to pulp-related disorders further accelerate growth momentum.

- By Instrument Type

On the basis of instrument type, the Dental Instruments market is segmented into Examination Instruments, Cutting Instruments, and Others. The Examination Instruments segment held the largest market revenue share of 34.8% in 2025, driven by their essential role in routine dental diagnostics and check-ups. Instruments such as mouth mirrors, explorers, and probes are fundamental tools used in nearly every dental visit. The increasing frequency of preventive dental examinations globally sustains consistent demand. Rising awareness regarding early diagnosis of oral diseases further strengthens segment growth. Technological improvements in diagnostic accuracy and ergonomic design enhance usability. Government-supported oral screening programs boost procurement across public healthcare facilities. Growing dental clinic networks worldwide contribute to higher instrument volumes. Examination tools are cost-effective yet indispensable, ensuring steady replacement cycles. Increased dental insurance penetration promotes regular patient visits. Expanding dental education institutions also procure examination kits in bulk. The rise in cosmetic dentistry consultations further increases diagnostic procedures. Continuous product innovation in anti-fog mirrors and lightweight materials improves efficiency and durability.

The Cutting Instruments segment is projected to witness the fastest CAGR of 9.1% from 2026 to 2033, supported by increasing restorative and surgical dental procedures. Rising cases of tooth decay and periodontal surgeries significantly drive demand for burs, chisels, and surgical blades. Technological advancements in carbide and diamond burs enhance cutting precision and longevity. Growing adoption of minimally invasive dentistry supports innovation in high-performance cutting tools. Dental implant procedures are increasing globally, further accelerating demand. Expansion of cosmetic and reconstructive dentistry contributes to higher usage rates. Improved sterilization and infection control standards promote frequent instrument replacement. Rising disposable income in emerging markets boosts access to advanced dental treatments. Continuous R&D investments enhance product efficiency and reduce chair time. Dental professionals increasingly seek durable and high-speed instruments for improved workflow. The growth of ambulatory dental surgical centers further supports expansion. Increased training in advanced surgical techniques accelerates adoption of specialized cutting tools.

- By End User

On the basis of end user, the Dental Instruments market is segmented into Hospitals, Clinics, Dental Laboratories, Scientific Research, and Others. The Clinics segment accounted for the largest market revenue share of 41.6% in 2025, driven by the high volume of outpatient dental procedures performed globally. Independent and group dental practices handle routine check-ups, cosmetic treatments, and minor surgeries. Increasing urbanization has led to a surge in private dental clinics. Clinics often invest in advanced instruments to enhance patient satisfaction and service efficiency. Rising dental insurance coverage encourages patients to seek clinical treatments. Growing dental tourism markets further boost clinic-based procedures. Technological upgrades in clinic infrastructure increase procurement rates. Flexible appointment systems in clinics attract higher patient footfall. The expansion of franchise-based dental chains strengthens purchasing power. Preventive and aesthetic dentistry trends further support consistent demand. Clinics typically maintain faster instrument replacement cycles compared to hospitals. The growth of specialized dental clinics contributes significantly to market dominance.

The Hospitals segment is expected to witness the fastest CAGR of 7.9% from 2026 to 2033, driven by the increasing integration of dental departments within multispecialty hospitals. Rising complex oral surgeries and trauma cases boost hospital-based dental procedures. Hospitals are equipped with advanced surgical infrastructure supporting high-end dental instruments. Growing healthcare investments in emerging economies strengthen hospital expansion. Increasing collaborations between dental specialists and medical professionals support integrated treatments. Government funding for public hospitals increases procurement budgets. Rising geriatric populations requiring surgical dental interventions further fuel growth. Hospitals often manage severe oral disease cases requiring advanced tools. Technological adoption in hospital settings enhances instrument demand. Expanding medical tourism also contributes to higher hospital admissions for dental treatments. Improved reimbursement frameworks for surgical procedures encourage patient inflow. Continuous modernization of healthcare infrastructure accelerates instrument procurement.

- By Distribution Channel

On the basis of distribution channel, the Dental Instruments market is segmented into Direct Tender, Third Party Distributors, and Retail Sales. The Third Party Distributors segment dominated the largest market revenue share of 46.2% in 2025, owing to their extensive supply networks and strong relationships with dental clinics and hospitals. Distributors provide a wide portfolio of brands and product options under one channel. They ensure timely delivery and after-sales service support. Bulk purchasing capabilities enable competitive pricing for end users. Expanding dental infrastructure in emerging regions strengthens distributor presence. Distributors often provide product demonstrations and technical training. Their established logistics systems enhance market penetration. Smaller clinics rely heavily on distributors for consistent supply. Inventory management services offered by distributors improve operational efficiency. Partnerships with international manufacturers expand product availability. Flexible credit policies further encourage procurement. Regional distribution networks ensure deeper rural and semi-urban market reach.

The Direct Tender segment is projected to register the fastest CAGR of 8.3% from 2026 to 2033, driven by increasing government and institutional procurement activities. Public hospitals and large dental chains prefer direct contracts for cost efficiency. Direct tenders allow bulk purchasing at negotiated prices, improving budget optimization. Growing healthcare infrastructure investments strengthen institutional buying power. Manufacturers increasingly participate in government bids to expand market share. Transparent procurement processes encourage large-scale purchases. Direct supply agreements reduce intermediary costs and improve margins. Expanding public oral healthcare programs further stimulate tender-based purchases. Institutional buyers demand advanced and standardized instruments. Large hospitals prefer long-term supplier contracts for consistency. Growing regulatory compliance requirements favor established manufacturers. The expansion of universal healthcare coverage further boosts direct procurement demand.

Asia-Pacific Dental Instruments Market Regional Analysis

- The Asia-Pacific dental instruments market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by the increasing prevalence of dental disorders, rising demand for cosmetic and restorative procedures, and growing awareness regarding oral hygiene across emerging and developed economies. Rapid urbanization, improving healthcare infrastructure, and expanding dental insurance coverage in select countries are further contributing to steady market expansion across the region

- The expansion of public and private dental healthcare systems across Asia-Pacific countries, along with continuous technological advancements in precision-based, ergonomically designed, and minimally invasive dental instruments, is fostering sustained growth. Increasing investments in advanced dental clinics, the integration of digital dentistry solutions such as CAD/CAM systems, and the adoption of infection control standards are further supporting instrument demand across general dentistry, orthodontics, implantology, prosthodontics, and endodontics applications

- The region is witnessing consistent growth across hospitals, private dental clinics, dental chains, and specialty centers, with modern and automated dental instruments being incorporated into both new practice establishments and existing facility upgrades. Rising dental tourism in countries such as India and Thailand is also creating additional opportunities for advanced instrument adoption

China Dental Instruments Market Insight

The China dental instruments market dominated the Asia-Pacific region with the largest revenue share of 31.8% in 2025 and is anticipated to grow at a noteworthy CAGR during the forecast period. This dominance is supported by a large patient pool, an expanding middle-class population, rapid urbanization, and significant investments in healthcare infrastructure. The country’s growing network of private dental clinics, rising awareness regarding oral hygiene, and increasing demand for cosmetic and restorative procedures such as dental implants, orthodontics, and teeth whitening are strengthening the adoption of advanced and cost-effective dental instruments. Furthermore, supportive government initiatives to modernize healthcare facilities and the presence of domestic manufacturers offering competitively priced products are expected to further reinforce China’s leading position in the regional market.

India Dental Instruments Market Insight

The India dental instruments market is expected to be the fastest-growing market in the Asia-Pacific region during the forecast period. India accounted for approximately 18.6% of the regional market share in 2025, reflecting its expanding contribution to the overall Asia-Pacific dental instruments landscape. Market growth is supported by increasing dental tourism, rising disposable incomes, expanding dental education institutions, and improving access to oral healthcare services across urban and semi-urban areas. Continuous investments in modern dental technologies, rapid growth of private dental chains, and increasing awareness of preventive and aesthetic dentistry are accelerating the adoption of advanced dental instruments. In addition, favorable demographic trends and ongoing clinic expansion initiatives are expected to further propel market growth across the country.

Asia-Pacific Dental Instruments Market Share

The Dental Instruments industry is primarily led by well-established companies, including:

- Dentsply Sirona (U.S.)

- Straumann Group (Switzerland)

- Danaher Corporation (U.S.)

- 3M Company (U.S.)

- Henry Schein, Inc. (U.S.)

- Zimmer Biomet (U.S.)

- Ivoclar Vivadent (Liechtenstein)

- GC Corporation (Japan)

- Hu-Friedy Mfg. Co., LLC (U.S.)

- Brasseler USA (U.S.)

- VDW GmbH (Germany)

- Septodont Holding (France)

- Ultradent Products, Inc. (U.S.)

- Coltene Group (Switzerland)

- Planmeca Group (Finland)

- A-dec Inc. (U.S.)

- Yoshida Dental Mfg. Co., Ltd. (Japan)

- NSK Ltd. (Japan)

- Morita Holdings Corporation (Japan)

- Osstem Implant Co., Ltd. (South Korea)

Latest Developments in Asia-Pacific Dental Instruments Market

- In March 2023, the Straumann Group unveiled a range of advanced digital implantology and orthodontic solutions at the International Dental Show (IDS) in Cologne, including the Straumann Falcon navigation system, Smilecloud design platform, and ClearCorrect mobile collaboration tools, enhancing clinical workflows and patient care across European dental practices. This launch highlighted Europe’s growing leadership in digital dentistry and adoption of integrated solutions to improve dental restoration and procedural accuracy

- In June 2024, Planmeca launched the Planmeca European Roadshow, a touring showcase of its latest dental technologies — including digital imaging systems, AI-powered Romexis software, and 3D printing solutions — visiting dental practices across multiple European countries to demonstrate cutting-edge equipment and support practitioner adoption of digital workflows. This initiative helped accelerate knowledge transfer and equipment uptake among dental professionals throughout Europe

- In June 2024, Danaher Corporation introduced a new line of ergonomically designed surgical hand instruments for dental professionals in Europe, aimed at improving comfort and efficiency during complex oral procedures and strengthening the company’s presence in high-growth markets such as Germany and France. This product launch highlighted the ongoing modernization of core dental instrument portfolios to enhance practitioner performance

- In June 2024, Dentsply Sirona also expanded its regional logistics network by establishing a dedicated distribution center in Milan, Italy, to enhance supply chain efficiency and ensure faster delivery of surgical instruments to both urban and rural dental clinics across Europe. This development demonstrated strategic investment to support market growth and timely access to essential dental instruments

- In September 2024, Mectron S.p.A. introduced a series of educational workshops across Germany and Switzerland focused on piezoelectric surgical techniques, aiming to increase awareness and adoption of its advanced piezoelectric dental instruments among specialist dental surgeons. These training campaigns supported deeper market penetration of innovative surgical tools in key European markets

- In November 2024, KaVo Dental (a division of Envista Holdings) opened a state-of-the-art surgical instrument production facility in the Netherlands, strengthening local manufacturing capabilities and enhancing supply reliability for high-quality instruments used across European dental practices. This investment underscored continued regional infrastructure growth in dental instrument production

- In March 2025, LM-Dental expanded its ergonomic hand instrument portfolio with new additions to the LM-Arte product line showcased at the IDS 2025 exhibition in Cologne, Germany, featuring the LM-Arte Replica Anterior instrument designed to simplify composite restorations in anterior dental work. This development underscored ongoing innovation in precision restorative instruments by European manufacturers to meet clinician needs for improved handling and restoration outcomes

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.