Asia Pacific Operational Technology Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

6.34 Billion

USD

10.82 Billion

2025

2033

USD

6.34 Billion

USD

10.82 Billion

2025

2033

| 2026 –2033 | |

| USD 6.34 Billion | |

| USD 10.82 Billion | |

| % | |

|

Asia-Pacific Operational Technology Market Segmentation, By Component (Hardware, Software/Platform, and Services), Deployment (On Premise, Hybrid, and Cloud), Organization Size (Small & Medium Business and Large Enterprises), Connectivity (Wired and Wireless), Technology (Supervisory Control and Data Acquisition (SCADA), Distributed Control Systems (DCS), Process Control Domains (PCD), Programmable Logic Controllers (PLC), Safety Instrumented Systems (SIS), and Building Management/Automation Systems (BAS)), End-user (Automotive and Transportation, Building and Infrastructure, Energy and Utilities, Food and Beverage, Life Sciences, Marine and Ports, Metals and Mining, Oil & Gas, Chemicals, Pulp and Paper, and Others) - Industry Trends and Forecast to 2033

Asia-Pacific Operational Technology Market Size

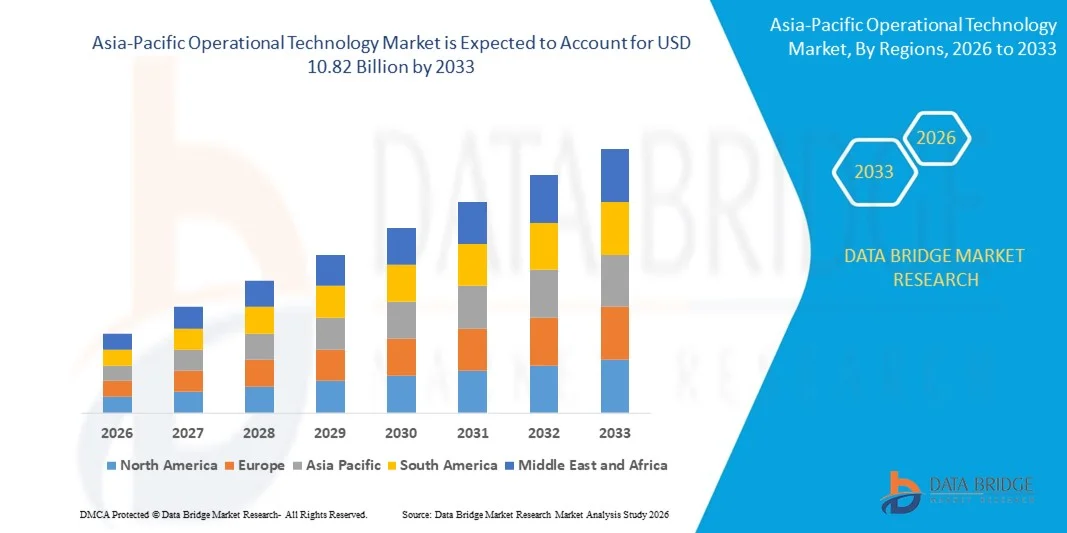

- The Asia-Pacific operational technology market size was valued at USD 6.34 billion in 2025 and is expected to reach USD 10.82 billion by 2033, at a CAGR of 6.9% during the forecast period

- The market growth is largely fueled by the accelerating adoption of industrial automation, Industry 4.0 initiatives, and digital transformation across manufacturing, energy, and infrastructure sectors, leading to deeper integration of IT and OT systems in mission-critical environments

- Furthermore, rising demand for real-time monitoring, predictive maintenance, and enhanced cybersecurity for critical infrastructure is establishing operational technology as the backbone of modern industrial operations. These converging factors are accelerating deployment of advanced control systems, industrial IoT platforms, and secure connectivity solutions, thereby significantly boosting the industry's growth

Asia-Pacific Operational Technology Market Analysis

- Operational technology, encompassing hardware and software systems such as PLCs, SCADA, and distributed control systems that monitor and control physical processes, has become essential for ensuring operational efficiency, safety, and reliability across industrial environments due to its capability to deliver real-time data visibility and automated process control

- The escalating demand for operational technology is primarily driven by increasing industrial digitization, modernization of legacy infrastructure, growing need for asset performance optimization, and heightened focus on safeguarding critical systems against evolving cyber threats

- China dominated the operational technology market in 2025, due to its vast industrial base, strong manufacturing ecosystem, and large-scale investments in smart factories and industrial automation

- India is expected to be the fastest growing country in the operational technology market during the forecast period due to rapid industrialization, infrastructure expansion, and increasing government focus on digital transformation

- On premise segment dominated the market with a market share of around 50% in 2025, due to strong demand for localized control, security, and compliance with industry-specific regulatory requirements. Many organizations prefer on-premise solutions to maintain full control over sensitive operational data, reduce latency, and ensure system reliability in mission-critical applications. The segment is widely adopted across traditional industrial sectors where downtime or breaches can have severe consequences

Report Scope and Operational Technology Market Segmentation

|

Attributes |

Operational Technology Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Asia-Pacific Operational Technology Market Trends

Increasing Integration of Industrial IoT and AI-Driven Analytics

- A significant trend in the operational technology market is the increasing integration of Industrial IoT and AI-driven analytics into industrial control environments, driven by the need for real-time monitoring, predictive insights, and improved operational visibility across manufacturing, energy, and utilities sectors. This integration is transforming traditional OT systems into intelligent, data-driven infrastructures that enhance productivity and asset performance

- For instance, Siemens AG integrates Industrial IoT and AI analytics through its Industrial Edge and MindSphere platforms to enable predictive maintenance and performance optimization across industrial plants. These solutions allow operators to analyze machine data in real time and improve decision-making accuracy within critical production environments

- The convergence of OT and IT systems is accelerating as organizations seek unified data platforms that connect programmable logic controllers, distributed control systems, and enterprise software. This is enabling seamless data exchange and strengthening cross-functional visibility across complex industrial ecosystems

- Energy and utilities providers are deploying AI-enabled monitoring systems within substations and grid infrastructure to detect anomalies and optimize load distribution. This trend is reinforcing the role of advanced analytics in maintaining operational stability and minimizing downtime across critical infrastructure networks

- Manufacturers are embedding smart sensors and connected devices within production lines to capture granular process data and enhance quality control. This shift is supporting continuous improvement strategies and driving higher levels of automation across industrial facilities

- The growing reliance on real-time analytics and interconnected systems is redefining operational efficiency standards across industries. This ongoing integration of Industrial IoT and AI-driven intelligence is positioning operational technology as a central pillar of modern industrial digital transformation

Asia-Pacific Operational Technology Market Dynamics

Driver

Rising Demand for Industrial Automation and Digital Transformation

- The rising demand for industrial automation and digital transformation initiatives is driving growth in the operational technology market as enterprises seek to improve efficiency, reduce manual intervention, and enhance production reliability. Industries are increasingly investing in advanced control systems, robotics, and digital monitoring platforms to modernize legacy infrastructure

- For instance, Schneider Electric delivers EcoStruxure-based automation and control solutions that support digital transformation across manufacturing and energy facilities. These deployments enable integrated monitoring, automated process control, and improved asset lifecycle management within complex industrial environments

- The expansion of smart factories is accelerating the deployment of distributed control systems and supervisory control and data acquisition platforms to support synchronized operations. This movement toward interconnected automation frameworks is strengthening operational transparency and performance consistency

- Heavy industries are upgrading to digitally enabled control architectures to improve safety standards and regulatory compliance. These investments are enabling real-time diagnostics and faster response to operational disruptions across mission-critical facilities

- The sustained push toward automation and digital modernization across global industries continues to reinforce this driver. The need for optimized productivity, reduced downtime, and smarter asset utilization is firmly positioning operational technology as a strategic enabler of industrial progress

Restraint/Challenge

Growing Cybersecurity Risks Across Critical Infrastructure

- The operational technology market faces significant challenges due to growing cybersecurity risks across critical infrastructure, as increased connectivity exposes industrial control systems to sophisticated cyber threats. The integration of IT and OT networks expands the attack surface and raises concerns regarding data integrity and operational continuity

- For instance, the ransomware attack on Colonial Pipeline in 2021 disrupted fuel supply operations and highlighted vulnerabilities within interconnected operational systems. This incident underscored the urgent need for robust cybersecurity frameworks to safeguard industrial environments against malicious intrusions

- Industrial facilities are increasingly targeted by advanced persistent threats that aim to disrupt production processes and compromise sensitive operational data. Such risks create hesitation among enterprises when expanding network connectivity across legacy control systems

- Compliance requirements and regulatory mandates are becoming more stringent as governments emphasize the protection of critical infrastructure sectors. Organizations must allocate substantial resources to implement secure communication protocols and continuous threat monitoring solutions

- The complexity of securing heterogeneous OT environments, which often include aging equipment and proprietary protocols, adds further operational challenges. These cybersecurity concerns collectively act as a restraint, compelling market participants to balance digital expansion with strengthened security measures to ensure resilient industrial operations

Asia-Pacific Operational Technology Market Scope

The market is segmented on the basis of component, deployment, organization size, connectivity, technology, and end-user.

- By Component

On the basis of component, the operational technology market is segmented into hardware, software/platform, and services. The hardware segment dominated the market with the largest revenue share in 2025, driven by the high demand for robust and reliable industrial devices, sensors, controllers, and networking equipment essential for OT infrastructure. Hardware adoption is further supported by the increasing modernization of industrial facilities and the need for enhanced monitoring, control, and operational efficiency across sectors. Organizations prioritize hardware solutions due to their long lifespan, compatibility with legacy systems, and critical role in ensuring system reliability and safety. The segment also benefits from rising investments in upgrading industrial machinery with advanced OT hardware to support Industry 4.0 initiatives.

The software/platform segment is anticipated to witness the fastest growth from 2026 to 2033, fueled by increasing adoption of cloud-based monitoring, analytics, and digital twin solutions. For instance, Siemens offers advanced software platforms that enable predictive maintenance, real-time monitoring, and remote management of OT systems, enhancing operational efficiency and decision-making. Software solutions facilitate integration across various OT components, improving scalability, security, and system optimization. Their ability to deliver actionable insights and streamline industrial processes positions them as a key growth driver in the market.

- By Deployment

On the basis of deployment, the OT market is segmented into on-premise, hybrid, and cloud. The on-premise deployment segment dominated the market with the largest share of around 50% in 2025 due to strong demand for localized control, security, and compliance with industry-specific regulatory requirements. Many organizations prefer on-premise solutions to maintain full control over sensitive operational data, reduce latency, and ensure system reliability in mission-critical applications. The segment is widely adopted across traditional industrial sectors where downtime or breaches can have severe consequences.

The cloud deployment segment is expected to witness the fastest growth from 2026 to 2033, driven by the increasing shift toward remote monitoring, real-time analytics, and AI-enabled industrial automation. For instance, Honeywell’s cloud-based OT solutions allow organizations to centralize control and leverage predictive analytics to optimize operations across multiple sites. Cloud deployment enables scalability, cost-effectiveness, and seamless integration with enterprise IT systems, supporting smarter and more flexible industrial operations.

- By Organization Size

On the basis of organization size, the OT market is segmented into small & medium business (SMB) and large enterprises. Large enterprises dominated the market in 2025 with the largest revenue share due to their extensive industrial operations, high investment capacity, and strong focus on automation, operational efficiency, and safety compliance. Enterprises implement complex OT solutions to manage large-scale processes, integrate legacy and modern systems, and ensure consistent production quality. The segment also benefits from partnerships with leading OT vendors for customized solutions, long-term service agreements, and digital transformation initiatives.

The SMB segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing accessibility of cost-effective and scalable OT solutions. For instance, Rockwell Automation provides modular OT solutions tailored for SMBs, enabling real-time monitoring, predictive maintenance, and remote control at a lower entry cost. SMBs are increasingly adopting OT to improve competitiveness, reduce operational risks, and optimize resource utilization, which supports rapid market expansion in this segment.

- By Connectivity

On the basis of connectivity, the OT market is segmented into wired and wireless. The wired connectivity segment dominated the market in 2025 due to its high reliability, minimal interference, and consistent performance in mission-critical industrial environments. Wired solutions are widely preferred in sectors such as energy, chemicals, and metals, where robust and secure connections are essential for continuous monitoring and control. Industrial protocols such as Modbus, Profibus, and Ethernet/IP further strengthen the adoption of wired systems.

The wireless connectivity segment is anticipated to witness the fastest growth from 2026 to 2033, driven by increasing adoption of Industrial IoT (IIoT), remote monitoring, and flexible deployment requirements. For instance, ABB offers wireless OT solutions that enable seamless connectivity for distributed assets and sensors in large industrial plants. Wireless connectivity reduces installation costs, enhances scalability, and allows integration of mobile or hard-to-reach assets, supporting rapid adoption across multiple industrial domains.

- By Technology

On the basis of technology, the OT market is segmented into Supervisory Control and Data Acquisition (SCADA), Distributed Control Systems (DCS), Process Control Domains (PCD), Programmable Logic Controllers (PLC), Safety Instrumented Systems (SIS), and Building Management/Automation Systems (BAS). The PLC segment dominated the market in 2025 due to its versatility, reliability, and critical role in automating industrial processes across manufacturing, energy, and infrastructure sectors. PLCs are widely used for precise control of machines, processes, and safety systems, providing operational efficiency and integration capabilities.

The SCADA segment is expected to witness the fastest growth from 2026 to 2033, driven by demand for centralized monitoring, real-time data visualization, and predictive analytics in distributed industrial networks. For instance, Schneider Electric’s SCADA solutions enable operators to control multiple processes remotely, optimize production, and detect anomalies early. SCADA systems are increasingly integrated with cloud platforms and AI-based analytics, offering enhanced process visibility, operational optimization, and cost reduction opportunities.

- By End-user

On the basis of end-user, the OT market is segmented into automotive and transportation, building and infrastructure, energy and utilities, food and beverage, life sciences, marine and ports, metals and mining, oil & gas, chemicals, pulp and paper, and others. The energy and utilities segment dominated the market in 2025 due to the critical requirement for efficient process control, real-time monitoring, and system reliability in power generation, transmission, and distribution operations. OT solutions in this sector enhance grid management, reduce operational risks, and support regulatory compliance.

The building and infrastructure segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing smart building projects, IoT-enabled automation, and energy management initiatives. For instance, Johnson Controls provides integrated OT solutions for modern infrastructure that optimize HVAC, lighting, and security systems while enabling centralized control. The adoption of smart building automation improves energy efficiency, occupant comfort, and operational cost savings, which drives rapid growth in this end-user segment.

Asia-Pacific Operational Technology Market Regional Analysis

- China dominated the operational technology market with the largest revenue share in 2025, driven by its vast industrial base, strong manufacturing ecosystem, and large-scale investments in smart factories and industrial automation

- Rapid expansion of power generation capacity, oil & gas infrastructure, and large-scale infrastructure projects, combined with government-backed digital transformation initiatives such as Made in China 2025, reinforce China’s leadership in the regional market

- The presence of major domestic automation providers, strategic collaborations with global industrial technology companies, and increasing deployment of SCADA, DCS, and PLC systems across utilities and manufacturing continue to consolidate China’s dominant position during the forecast period

Japan Operational Technology Market Insight

The Japan market is anticipated to grow steadily from 2026 to 2033, supported by its advanced manufacturing sector and early adoption of robotics and industrial automation technologies. Japanese industries emphasize precision, reliability, and system integration, which accelerates deployment of PLC, DCS, and safety instrumented systems across automotive and electronics production. Strong regulatory standards and continuous modernization of aging infrastructure further support OT investments. Ongoing R&D initiatives and partnerships between domestic automation leaders and global technology providers reinforce the market’s stable growth outlook. Japan’s focus on operational efficiency, cybersecurity resilience, and technological innovation underpins its strong regional positioning.

India Operational Technology Market Insight

India is projected to register the fastest CAGR in the Asia Pacific operational technology market during 2026–2033, fueled by rapid industrialization, infrastructure expansion, and increasing government focus on digital transformation. Initiatives such as Digital India and smart city projects are accelerating adoption of automation, remote monitoring, and process control solutions across utilities and manufacturing sectors. Rising investments in renewable energy, oil & gas, and transportation infrastructure are driving demand for advanced OT systems. Growing awareness of operational efficiency, predictive maintenance, and cybersecurity is encouraging enterprises to modernize legacy systems. Government incentives, foreign direct investment inflows, and expanding industrial corridors ensure India’s emergence as the fastest-growing market in the region.

Asia-Pacific Operational Technology Market Share

The operational technology industry is primarily led by well-established companies, including:

- Fortinet, Inc. (U.S.)

- Gray Matter Systems LLC (U.S.)

- Forcepoint (U.S.)

- IBM Corporation (U.S.)

- ABB (Sweden)

- General Electric (U.S.)

- Schneider Electric (France)

- Rockwell Automation, Inc. (U.S.)

- Emerson Electric Co. (U.S.)

- Advantech Co., Ltd. (Taiwan)

- Honeywell International Inc. (U.S.)

- Huawei Technologies Co., Ltd. (China)

- Oracle (U.S.)

- Wipro Limited (India)

- SCADAfence (Ireland)

- SAP SE (Germany)

- Cisco Systems (U.S.)

- Accenture (Ireland)

- Wunderlich-Malec Engineering, Inc. (U.S.)

- Yokogawa Electric Corporation (Japan)

Latest Developments in Asia-Pacific Operational Technology Market

- In February 2026, Schneider Electric expanded its EcoStruxure Automation platform with advanced AI-driven predictive maintenance and integrated cybersecurity features for industrial environments. This enhancement strengthens real-time monitoring, anomaly detection, and secure remote operations across energy, utilities, and manufacturing sectors. The development reinforces the convergence of IT and OT systems, accelerating digital transformation initiatives and increasing demand for secure, scalable OT platforms across critical infrastructure markets

- In January 2026, ABB launched an upgraded industrial cybersecurity portfolio integrated with its distributed control systems and PLC platforms. The solution enhances network segmentation, threat detection, and lifecycle management for operational assets in power generation, oil & gas, and process industries. This initiative supports organizations in mitigating cyber risks while ensuring operational continuity, thereby strengthening market adoption of integrated and security-centric OT architectures

- In March 2025, Fortinet introduced significant upgrades to its OT Security Platform during the Gartner Digital Workplace Summit, enhancing protection for critical infrastructure against evolving cyber threats. The updates improved network visibility, micro-segmentation, and secure connectivity tailored for transportation, energy, and manufacturing sectors. This advancement accelerates enterprise investment in unified OT cybersecurity solutions, reinforcing Fortinet’s position in securing industrial control environments

- In March 2025, TXOne Networks released Version 3.2 of its Stellar solution, expanding its capabilities from endpoint protection to comprehensive detection and response in operational technology environments. The upgrade strengthens proactive threat hunting, real-time monitoring, and incident response across industrial systems. This development increases demand for specialized OT-native security solutions and supports the shift toward integrated detection and response frameworks in industrial cybersecurity

- In March 2025, Armis completed the acquisition of OTORIO to enhance its cyber exposure management capabilities in OT and cyber-physical systems security. By integrating OTORIO’s Titan platform into Armis’ Centrix cloud-based platform, the company strengthens its end-to-end visibility and risk management across industrial assets. This strategic move expands competitive capabilities in the OT cybersecurity landscape and drives consolidation within the operational technology security market

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.