Asia Pacific Research Antibodies Reagents Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

2.08 Billion

USD

3.65 Billion

2024

2032

USD

2.08 Billion

USD

3.65 Billion

2024

2032

| 2025 –2032 | |

| USD 2.08 Billion | |

| USD 3.65 Billion | |

| % | |

Asia-Pacific Research Antibodies Reagents Market, By Type (Antibodies and Reagents), Application (Enzyme-Linked Immunosorbent Assay, Western Blotting, Immunohistochemistry, Flow Cytometry, Polymerase Chain Reaction, and Others), Research Area (Immunology, Cell & Molecular Biology, Neuroscience, Genomics & Proteomics, Biotechnology & Drug Discovery, Microbiology, and Others), End User (Pharmaceutical and Biopharmaceutical Manufacturers, Academic And Research Institutes, Contract Research Organizations (CROs), Hospitals & Diagnostic Laboratories, and Others), Distribution Channel (Direct Sales, Third Party Sales, and Others)– Industry Trends and Forecast to 2032

Asia-Pacific Research Antibodies Reagents Market Analysis

The Asia-Pacific research antibodies reagents market is a rapidly growing segment within the life sciences and biotechnology industries. Antibodies reagents are crucial tools in research applications, including diagnostics, drug development, disease understanding, and biomarker discovery. The market has witnessed significant growth due to the increasing demand for personalized medicine, advancements in genomics and proteomics, and the rising prevalence of chronic diseases like cancer, diabetes, and autoimmune disorders.

Asia-Pacific Research Antibodies Reagents Market Size

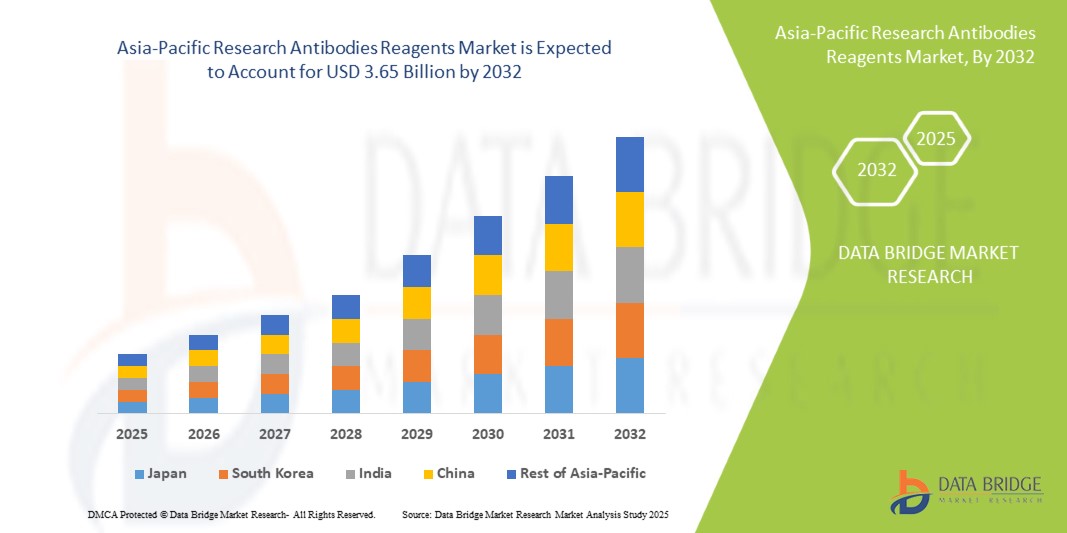

Asia-Pacific research antibodies reagents market size was valued at USD 2.08 billion in 2024 and is projected to reach USD 3.65 billion by 2032, growing with a CAGR of 7.5% during the forecast period of 2025 to 2032.

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework.

Asia-Pacific Research Antibodies Reagents Market Trends

“Increasing Demand for Personalized Medicine and Targeted Therapies”

One significant trend in the Asia-Pacific research antibodies reagents market is the increasing demand for personalized medicine and targeted therapies, which is driving innovation in antibody development. As researchers and pharmaceutical companies focus on developing customized treatments based on individual patient profiles, there is a rising need for high-specificity and affinity antibodies that can accurately target specific biomarkers associated with various diseases. This trend is further fueled by advancements in technologies such as monoclonal antibody production, recombinant DNA technology, and CRISPR, leading to the introduction of novel antibody reagents that enhance the effectiveness of diagnostic and therapeutic applications. Additionally, the growth of biobanks and precision research initiatives contributes to a broader array of available reagents, supporting the evolution of the market toward more specialized and effective research tools.

Report Scope and Asia-Pacific Research Antibodies Reagents Market Segmentation

|

Attributes |

Asia-Pacific Research Antibodies Reagents Market Insights |

|

Segments Covered |

|

|

Countries Covered |

China, Japan, India, South Korea, Australia, Singapore, Thailand, Malaysia, Indonesia, Philippines, and Rest of Asia-Pacific |

|

Key Market Players |

Thermo Fisher Scientific (U.S.), MilliporeSigma (U.S.), Santa Cruz Biotechnology (U.S.), Danaher (U.S.), Perkinelmer Inc (U.S.), F.Hoffmann La Roche Ltd.(Switzerland), Rockland Immunochemicals Inc (U.S.), Johnsons & Johnsons (U.S.), Agilent Technologies Inc. (U.S.), Eli Lily and Company (U.S.), BD (U.S.), Genscript Biotech Corporation (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Asia-Pacific Research Antibodies Reagents Market Definition

The Asia-Pacific research antibodies reagents market refers to the commercial sector involving the production, distribution, and utilization of antibodies and related reagents used in research applications across various fields, including biotechnology, pharmaceuticals, and academic research. This market encompasses a wide range of products, including monoclonal and polyclonal antibodies, secondary antibodies, antibody fragments, and conjugated antibodies, which are essential tools for a variety of applications such as immunohistochemistry, Western blotting, Enzyme-Linked Immunosorbent Assays (ELISA), and flow cytometry. The market is driven by the growing need for innovative research tools to support drug discovery, disease diagnosis, and personalized medicine, as well as advancements in antibody technologies and increasing funding for research in life sciences.

Asia-Pacific Research Antibodies Reagents Market Dynamics

Drivers

- Increase in Technological Advancements

Technological advancements play a crucial role in driving the Asia-Pacific research antibodies reagents market by enabling the development of more specific, efficient, and diverse antibody products. Innovations such as monoclonal antibody production processes, phage display technology, and recombinant DNA technologies have significantly improved the ability to produce high-quality antibodies with enhanced specificity and affinity. These technologies allow researchers to create antibodies that are tailored to specific targets, which is essential in various applications, including drug development, diagnostics, and basic research. The continuous evolution of high-throughput screening techniques and the integration of bioinformatics tools further accelerate the discovery and validation of novel antibodies, leading to a broader range of reagents available on the market and meeting the diverse needs of the scientific community.

For instance,

- In November 2024, according to an article published in the National Library of Medicine, breakthroughs in genetic engineering have enabled the production of humanized antibodies and the advances in Fc engineering, thereby increasing therapeutic efficacy. The discovery of immune checkpoints and cytokines revolutionized the treatment of cancer and autoimmune diseases

- In February 2021, according to an article published in the National Library of Medicine, currently, more than 500 antibodies are in early stages of research, while more than 50 mAbs are in the final stages of clinical development, most of which are directed at combating cancer and autoimmune or inflammatory diseases such as melanoma, lupus, and rheumatoid arthritis

Increasing Prevalence of Neurodegenerative Diseases

The increasing prevalence of neurodegenerative diseases, such as Alzheimer's, Parkinson's, and amyotrophic lateral sclerosis (ALS), is significantly driving demand for research antibodies reagents in the global market. As the incidence of these diseases rises due to factors such as aging populations and lifestyle changes, there is an urgent need for ongoing research to uncover their underlying mechanisms, identify biomarkers for early diagnosis, and develop effective treatments. Antibodies play a critical role in this research, as they are essential tools for studying the pathological processes involved in neurodegenerative diseases. This growing focus on understanding and combating neurodegenerative conditions is fuelling investment in the development of specific antibodies to target proteins associated with these diseases, thus expanding the market for research antibodies reagents.

For instance,

- In February 2021, according to an article published in the National Library of Medicine, neurological disorders are the leading cause of physical and cognitive disability across the globe, currently affecting approximately 15% of the worldwide population. Absolute patient numbers have considerably climbed over the past 30 years. Moreover, the burden of chronic neurodegenerative conditions is expected to at least double over the next two decades

Moreover, the increased funding and resources being allocated to neuroscience research—both by government bodies and private organizations—create a conducive environment for the growth of the antibodies reagents market. As pharmaceutical and biotechnology companies ramp up their efforts to develop new therapies, including monoclonal antibodies and other biologics for treating neurodegenerative diseases, the demand for high-quality research antibodies and reagents to support preclinical and clinical studies is on a rise. This trend translates into opportunities for companies specializing in antibody production and related reagents, enabling them to enhance their product offerings and contribute to the advancement of treatments for neurodegenerative diseases, ultimately benefiting patients and healthcare systems.

Opportunities

- Growing Demand for Personalized Medicine

The growing demand for personalized medicine presents a significant opportunity in the market. Personalized medicine, which tailors treatment based on an individual’s genetic makeup, lifestyle, and environment, has gained momentum due to its potential to improve patient outcomes and reduce adverse effects. This trend is fueling the need for advanced diagnostic tools and biomarker discovery, which rely heavily on antibodies and reagents.

Antibodies play a crucial role in personalized medicine, particularly in identifying and targeting specific biomarkers associated with diseases. Monoclonal and polyclonal antibodies are instrumental in developing precision therapies and companion diagnostics, which are integral to personalized treatment plans. For example, in cancer research, antibodies can target specific tumor antigens, allowing for the development of therapies that are more effective and less toxic than traditional treatments. Similarly, in autoimmune diseases, antibodies can be used to identify specific immune markers that guide treatment decisions.

As more research institutions and pharmaceutical companies focus on developing personalized therapies, there is an increasing demand for high-quality antibodies and reagents to aid in the discovery and validation of biomarkers. These tools are essential for creating diagnostic tests that determine the most appropriate treatments for individual patients, thereby improving therapeutic outcomes.

- Research Growth in Autoimmune and Infectious Diseases

With increasing advancements in biotechnology and the rising global burden of infectious diseases, there is a greater need for precise diagnostic tools and targeted therapies. The demand for antibodies and reagents is particularly high in this field due to their critical role in diagnosing and treating a variety of infectious diseases, such as COVID-19, tuberculosis, HIV, and emerging pathogens like Ebola and monkeypox.

In the case of infectious diseases, antibodies are vital for the development of rapid diagnostic tests that detect specific pathogens or their biomarkers. Monoclonal antibodies, in particular, are essential in developing tests and treatments for various infectious diseases by targeting antigens specific to the disease-causing microorganisms. Furthermore, antibodies play a key role in the development of vaccines, helping to identify and neutralize pathogens before they cause harm. With the increasing focus on pandemic preparedness, antibody-based reagents are critical for the rapid identification and isolation of infectious agents.

Research into autoimmune diseases, which occur when the immune system attacks the body’s own cells, is also gaining significant attention. Conditions such as rheumatoid arthritis, lupus, and multiple sclerosis are increasingly being studied using antibodies that specifically target immune cells involved in disease processes. These developments are crucial for developing more effective and less toxic therapies, offering new treatment options for patients. The growing interest in immunotherapy, which uses antibodies to modulate immune responses, is also expanding research in this area.

Restraints/Challenges

- Growing Use of Alternative Technologies

The growing use of alternative therapies poses significant challenges for the global research antibodies reagents market. As research shifts towards emerging therapeutic modalities, such as gene therapies, cell therapies, and RNA-based treatments, there may be a decreased reliance on traditional antibody-based approaches. This shift can lead to fluctuations in demand for conventional research antibodies, as funding and research priorities increasingly favour these innovative alternatives over established methodologies, potentially leading to market contraction for antibody reagent suppliers. Furthermore, the rapid development of alternative therapies may outpace the ability of antibody manufacturers to adapt, creating a gap between the needs of researchers and the available products.

For instance,

- In May 2024, according to the article, ‘Recent Advances in Gene Therapy for Haemophilia: Projecting the Perspectives’, gene therapy is considered to be the most promising method as it may overcome the problems associated with more traditional treatments

- In April 2020, according to U.S. Government Accountability Office, scientists are using CRISPR/ CAS9 technology to develop diagnostic tests that may rapidly identify diseases such as sickle cell anaemia and some types of cancer. They help in controlling certain diseases by altering the traits of insects or other organisms that can transmit disease

Additionally, the complexity and specificity associated with newer therapies can further challenge the antibodies market. As researchers explore novel approaches that require highly specialized or engineered antibodies, there may be difficulties in sourcing the appropriate reagents to meet these new demands. This creates pressure on manufacturers to invest in research and development for new types of antibodies and reagents that are tailored for these advanced therapies. Such investments may not yield immediate returns, leading to financial strain on companies that have traditionally relied on the sale of standard research antibodies. As a result, the growing demand for alternative therapies could compel antibody suppliers to either diversify their product offerings or face the risk of obsolescence in an evolving therapeutic landscape.

- Need for Expertise Associated With the Handling of Antibodies Reagents

The need for specialized expertise in the handling of antibody reagents presents a significant challenge for the research antibodies reagents market. Antibodies are complex molecules that require meticulous handling, storage, and application to maintain their stability and functionality. Researchers must be well-versed in various protocols, including dilution, labelling, and conjugation techniques, to ensure that they achieve reliable and reproducible results in their experiments. This necessity for expertise can create barriers for organizations, particularly smaller labs or those in developing regions, which may lack access to adequately trained personnel or resources. As a consequence, the effective utilization of antibody reagents may be compromised, leading to suboptimal research outcomes and potential wastage of costly materials, ultimately challenging the overall growth of the market.

For instance,

- In August 2024, according to an article published by MBL International Corporation, Proper storage and handling of antibody reagents are crucial for maintaining their effectiveness over time. Antibodies degrade or lose activity if not stored under optimal conditions

- In May 2024, according to an article published by AByntek Biopharma S.L., The development of a successful diagnostic test or assay requires a secure supply chain of high-quality reagents. Recombinant antibody technology enables the production of highly reliable antibodies adapted to your specific assay, providing superior performance throughout the lifespan of your diagnosis

Moreover, the evolving landscape of antibody technologies, including advancements in humanization, engineering, and validation, necessitates continuous education and training for researchers. Moreover, as regulatory standards become increasingly stringent for antibody-based diagnostics and therapeutics, researchers must ensure compliance, which adds another layer of complexity in both research and applications. This reliance on expertise may limit the scalability of the market, as it could result in unequal access to advanced antibody reagents, stifling innovation and collaborations among various research institutions and industries. Consequently, the need for specialized knowledge in handling antibody reagents and constrains market growth and restricts the potential for new discoveries in biomedical research.

Asia-Pacific Research Antibodies Reagents Market Scope

The market is segmented on the basis of type, application, research area, end user and distribution channel. The growth amongst these segments will help you analyze meagre growth segments in the industries and provide the users with a valuable market overview and market insights to help them make strategic decisions for identifying core market applications.

By Type

- Antibodies

- Antibodies, By Products

- Primary Antibodies

- Secondary Antibodies

- Antibodies, By Source

- Mouse

- Rabbit

- Goat

- Rat

- Others

- Antibodies, Based on Origin

- Monoclonal Antibodies

- Polyclonal Antibodies

- Recombinant Antibodies

- Antibodies, By Products

- Reagents

- Reagents, By Type

- Buffers & Solution

- Chemiluminescent Reagents

- Buffers & Solution, By Type

- PBS (Phosphate Buffered Saline)

- Blocking Buffers

- Dilution Buffers

- Wash Buffers

- Reagents, By Type

By Application

- Enzyme-Linked Immunosorbent Assay

- Western Blotting

- Immunohistochemistry

- Flow Cytometry

- Polymerase Chain Reaction

- Others

By Research Area

- Immunology

- Cell & Molecular Biology

- Neuroscience

- Genomics & Proteomics

- Biotechnology & Drug Discovery

- Microbiology

- Others

By End User

- Pharmaceutical and Biopharmaceutical Manufacturers

- Academic And Research Institutes

- Contract Research Organizations (CROs)

- Hospitals & Diagnostic Laboratories

- Others

By Distribution Channel

- Direct Sales

- Third Party Sales

- Others

Asia-Pacific Research Antibodies Reagents Market Regional Analysis

The market is segmented on the basis of type, application, research area, end user and distribution channel.

The countries covered in the market are China, Japan, India, South Korea, Australia, Singapore, Thailand, Malaysia, Indonesia, Philippines, and rest of Asia-Pacific.

China is expected to dominate the market due to increasing research activities, government support, and the expansion of biotechnology and pharmaceutical industries.

The country section of the report also provides individual market impacting factors and changes in regulation in the market domestically that impacts the current and future trends of the market. Data points like down-stream and upstream value chain analysis, technical trends and porter's five forces analysis, case studies are some of the pointers used to forecast the market scenario for individual countries. Also, the presence and availability of Asia-Pacific brands and their challenges faced due to large or scarce competition from local and domestic brands, impact of domestic tariffs and trade routes are considered while providing forecast analysis of the country data.

Asia-Pacific Research Antibodies Reagents Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, Asia-Pacific presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

Asia-Pacific Research Antibodies Reagents Market Leaders Operating in the Market Are:

- Thermo Fisher Scientific (U.S.)

- MilliporeSigma (U.S.)

- Santa Cruz Biotechnology (U.S.)

- Danaher (U.S.)

- Perkinelmer Inc (U.S.)

- F.Hoffmann La Roche Ltd. (Switzerland)

- Rockland Immunochemicals Inc (U.S.)

- Johnsons & Johnsons (U.S.)

- Agilent Technologies Inc. (U.S.)

- Eli Lily and Company (U.S.)

- BD (U.S.)

- Genscript Biotech Corporation (U.S.)

Latest Developments in Asia-Pacific Research Antibodies Reagents Market

- In November 2024, Sigma-Aldrich has announced the winners of its Emerging Biotech Grant Program, which supports innovative biotech startups and researchers. The program aims to foster the development of groundbreaking technologies in life sciences. Winners receive funding, resources, and mentorship to accelerate their research and product development, contributing to advancements in biotechnology

- In September 2024, Sigma-Aldrich has introduced the **Mobius™ ADC** (antibody-drug conjugate) platform, designed to streamline the development and manufacturing of biologics. This advanced platform offers a comprehensive solution for the efficient production of ADCs, enabling faster, more scalable, and cost-effective creation of targeted therapies, enhancing the development of innovative cancer treatments

- In December 2024, Thermo Fisher Scientific has launched CTS Detachable Dynabeads CD4 and CTS Detachable Dynabeads CD8 to support cell therapy development and production. These innovative tools enhance T cell isolation and expansion processes, improving the efficiency and scalability of cell therapies, offering new opportunities for advanced immunotherapies and personalized treatments

- In October 2024, Thermo Fisher Scientific highlighted its expanded biopharma services at CPhI Milan 2024, showcasing innovations designed to support the development and production of complex biologics and cell therapies. These advancements focus on improving the scalability, efficiency, and speed of biopharmaceutical manufacturing, underscoring Thermo Fisher's commitment to accelerating biopharma solutions

- In November 2024, Eli Lilly and Company announced the election of Jon Moeller to its board of directors. Karen Walker resigned from the board, , but will collaborate on digital commercial activities in 2025

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

목차

1 서론

1.1 연구 목적

1.2 시장 정의

1.3 아시아 태평양 연구용 항체 시약 시장 개요

1.4 대상 시장

2 시장 세분화

2.1 대상 시장

2.2 지리적 범위

연구에 2.3년이 고려됨

2.4 통화 및 가격

2.5 DBMR TRIPOD 데이터 검증 모델

2.6 다변량 모델링

2.7 주요 여론 선도자와의 1차 인터뷰

2.8 DBMR 시장 위치 그리드

2.9 2차 소스

2.1 가정

3 요약

4가지 프리미엄 인사이트

4.1 PESTAL 분석

4.2 포터의 5가지 힘 분석

5 규정 적용 범위

6 시장 개요

6.1 드라이버

6.1.1 기술적 진보의 증가

6.1.2 신경퇴행성 질환의 유병률 증가

6.1.3 정부 자금 지원 및 이니셔티브

6.1.4 진단 사용 증가

6.2 제약

6.2.1 대체 기술의 사용 증가

6.2.2 항체 시약 취급과 관련된 전문성의 필요성

6.3 기회

6.3.1 개인화된 의학에 대한 수요 증가

6.3.2 자가면역 및 감염성 질환에 대한 연구 증가

6.3.3 전 세계 의료 분야 확장

6.4 과제

6.4.1 항체의 높은 비용으로 인한 시장 접근성 제한

6.4.2 규제 문제로 인해 제품 승인이 지연되고 시장 진입이 지연됨

7 아시아 태평양 연구 항체 시약 시장, 유형별

7.1 개요

7.2 항체

7.2.1 1차 항체

7.2.2 2차 항체

7.2.2.1 마우스

7.2.2.2 토끼

7.2.2.3 염소

7.2.2.4 쥐

7.2.2.5 기타

7.2.3 단일클론 항체

7.2.4 다클론 항체

7.2.5 재조합 항체

7.3 시약

7.3.1 버퍼 및 솔루션

7.3.2 화학 발광 시약

8 아시아 태평양 연구 항체 시약 시장, 응용 분야별

8.1 개요

8.2 효소 결합 면역 흡착 시험

8.3 웨스턴 블로팅

8.4 면역조직화학

8.5 유세포 분석

8.6 중합효소 연쇄 반응

8.7 기타

9 아시아 태평양 연구 항체 시약 시장, 연구 분야별

9.1 개요

9.2 면역학

9.3 세포 및 분자 생물학

9.4 신경과학

9.5 유전체학 및 단백체학

9.6 생명공학 및 약물 발견

9.7 미생물학

9.8 기타

10 아시아 태평양 연구 항체 시약 시장, 최종 사용자별

10.1 개요

10.2 제약 및 생물제약 제조업체

10.3 학술 및 연구 기관

10.4 계약 연구 조직(CROS)

10.5 병원 및 진단 실험실

10.6 기타

11 아시아 태평양 연구 항체 시약 시장, 유통 채널별

11.1 개요

11.2 직접 판매

11.3 제3자 판매

11.4 기타

12 아시아 태평양 연구 항체 시약 시장, 지역별

12.1 아시아 태평양

12.1.1 중국

12.1.2 일본

12.1.3 인도

12.1.4 대한민국

12.1.5 호주

12.1.6 싱가포르

12.1.7 태국

12.1.8 말레이시아

12.1.9 인도네시아

12.1.10 필리핀

12.1.11 기타 아시아

13 아시아 태평양 기타 시장: 회사 환경

13.1 회사 점유율 분석: 아시아 태평양

14 SWOT 분석

15개 회사 프로필

15.1 머크 주식회사

15.1.1 회사 스냅샷

15.1.2 수익 분석

15.1.3 회사 점유율 분석

15.1.4 제품 포트폴리오

15.1.5 최근 개발

15.2 써모 피셔 사이언티픽 주식회사

15.2.1 회사 스냅샷

15.2.2 수익 분석

15.2.3 회사 점유율 분석

15.2.4 제품 포트폴리오

15.2.5 최근 개발

15.3 산타크루즈 바이오테크놀로지 주식회사

15.3.1 회사 스냅샷

15.3.2 회사 점유율 분석

15.3.3 제품 포트폴리오

15.3.4 최근 개발

15.4 다나허

15.4.1 회사 스냅샷

15.4.2 수익 분석

15.4.3 회사 점유율 분석

15.4.4 제품 포트폴리오

15.4.5 최근 개발

15.5 퍼키넬머 주식회사

15.5.1 회사 스냅샷

15.5.2 수익 분석

15.5.3 회사 점유율 분석

15.5.4 제품 포트폴리오

15.5.5 최근 개발

15.6 애질런트 테크놀로지스 주식회사

15.6.1 회사 스냅샷

15.6.2 수익 분석

15.6.3 제품 포트폴리오

15.6.4 최근 개발

15.7 바이오라드 연구소 주식회사

15.7.1 회사 스냅샷

15.7.2 수익 분석

15.7.3 제품 포트폴리오

15.7.4 최근 개발

15.8 바이오테크네 주식회사

15.8.1 회사 스냅샷

15.8.2 수익 분석

15.8.3 제품 포트폴리오

15.8.4 최근 개발

15.9 BD(BECTON, DICKINSON AND COMPANY)

15.9.1 회사 스냅샷

15.9.2 수익 분석

15.9.3 제품 포트폴리오

15.9.4 최근 개발

15.1 바이오레전드 주식회사

15.10.1 회사 스냅샷

15.10.2 수익 분석

15.10.3 제품 포트폴리오

15.10.4 최근 개발

15.11 엘리 릴리 앤 컴퍼니

15.11.1 회사 스냅샷

15.11.2 수익 분석

15.11.3 제품 포트폴리오

15.11.4 최근 개발

15.12 F. 호프만-라 로슈 유한회사

15.12.1 회사 스냅샷

15.12.2 수익 분석

15.12.3 제품 포트폴리오

15.12.4 최근 개발

15.13 젠스크립트

15.13.1 회사 스냅샷

15.13.2 수익 분석

15.13.3 제품 포트폴리오

15.13.4 최근 개발

15.14 존슨앤존슨서비스 주식회사

15.14.1 회사 스냅샷

15.14.2 제품 포트폴리오

15.14.3 최근 개발

15.15 론자

15.15.1 회사 스냅샷

15.15.2 수익 분석

15.15.3 제품 포트폴리오

15.15.4 최근 개발

15.16 록랜드 면역화학 주식회사

15.16.1 회사 스냅샷

15.16.2 제품 포트폴리오

15.16.3 최근 개발

15.17 테바제약산업주식회사

15.17.1 회사 스냅샷

15.17.2 수익 분석

15.17.3 제품 포트폴리오

15.17.4 최근 개발

16 설문지

17 관련 보고서

표 목록

표 1 규제 범위

표 2 아시아 태평양 연구용 항체 시약 시장, 유형별, 2018-2032년(백만 달러)

표 3 아시아 태평양 항체 연구용 항체 시약 시장, 지역별, 2018-2032 (백만 달러)

표 4 아시아 태평양 항체 연구용 항체 시약 시장, 제품별, 2018-2032(백만 달러)

표 5 아시아 태평양 항체 연구용 항체 시약 시장, 출처별, 2018-2032(백만 달러)

표 6 아시아 태평양 항체 연구용 항체 시약 시장, 출처 기준, 2018-2032 (백만 달러)

표 7 아시아 태평양 지역 연구용 항체 시약 시장 시약, 지역별, 2018-2032 (백만 달러)

표 8 아시아 태평양 연구용 시약 항체 시약 시장, 유형별, 2018-2032(백만 달러)

표 9 아시아 태평양 버퍼 및 솔루션 연구용 항체 시약 시장, 유형별, 2018-2032 (백만 달러)

표 10 아시아 태평양 연구용 항체 시약 시장, 응용 분야별, 2018-2032년(백만 달러)

표 11 아시아 태평양 지역별 효소연계면역흡착시험 항체 시약 시장, 지역별, 2018-2032 (백만 달러)

표 12 아시아 태평양 지역 연구용 웨스턴 블로팅 항체 시약 시장, 지역별, 2018-2032 (백만 달러)

표 13 아시아 태평양 면역조직화학 연구 항체 시약 시장, 지역별, 2018-2032 (백만 달러)

표 14 아시아 태평양 지역별 연구용 흐름 세포 분석 항체 시약 시장, 2018-2032년 지역별(백만 달러)

표 15 아시아 태평양 지역별 연구용 중합효소 연쇄 반응 항체 시약 시장, 지역별, 2018-2032 (백만 달러)

표 16 아시아 태평양 기타 연구용 항체 시약 시장, 지역별, 2018-2032 (백만 달러)

표 17 아시아 태평양 연구 항체 시약 시장, 연구 분야별, 2018-2032 (백만 달러)

표 18 아시아 태평양 면역학 연구 항체 시약 시장, 지역별, 2018-2032 (백만 달러)

표 19 아시아 태평양 세포 및 분자 생물학 연구 항체 시약 시장, 지역별, 2018-2032 (백만 달러)

표 20 아시아 태평양 신경과학 연구 항체 시약 시장, 지역별, 2018-2032 (백만 달러)

표 21 아시아 태평양 유전체학 및 단백질체학 연구 항체 시약 시장, 지역별, 2018-2032 (백만 달러)

표 22 아시아 태평양 생명공학 및 연구용 항체 시약 시장에서의 약물 발견, 지역별, 2018-2032 (백만 달러)

표 23 아시아 태평양 미생물학 연구 항체 시약 시장, 지역별, 2018-2032 (백만 달러)

표 24 아시아 태평양 기타 연구용 항체 시약 시장, 지역별, 2018-2032 (백만 달러)

표 25 아시아 태평양 연구용 항체 시약 시장, 최종 사용자별, 2018-2032년(백만 달러)

표 26 아시아 태평양 제약 및 바이오 제약 제조업체 연구용 항체 시약 시장, 지역별, 2018-2032 (백만 달러)

표 27 아시아 태평양 학술 및 연구 기관의 연구 항체 시약 시장, 지역별, 2018-2032 (백만 달러)

표 28 아시아 태평양 계약 연구 기관(CROS) 연구 항체 시약 시장, 지역별, 2018-2032(백만 달러)

표 29 아시아 태평양 병원 및 진단 실험실 연구 항체 시약 시장, 지역별, 2018-2032 (백만 달러)

표 30 아시아 태평양 기타 연구용 항체 시약 시장, 지역별, 2018-2032 (백만 달러)

표 31 아시아 태평양 연구용 항체 시약 시장, 유통 채널별, 2018-2032년(백만 달러)

표 32 아시아 태평양 지역 연구용 항체 시약 시장 직접 판매, 지역별, 2018-2032(백만 달러)

표 33 아시아 태평양 지역 연구용 항체 시약 시장의 제3자 판매, 지역별, 2018-2032 (백만 달러)

표 34 아시아 태평양 기타 연구용 항체 시약 시장, 지역별, 2018-2032 (백만 달러)

표 35 아시아 태평양 연구용 항체 시약 시장, 국가별, 2018-2032 (백만 달러)

표 36 아시아 태평양 연구용 항체 시약 시장, 유형별, 2018-2032 (백만 달러)

표 37 아시아 태평양 항체 연구용 항체 시약 시장, 제품별, 2018-2032(백만 달러)

표 38 아시아 태평양 항체 연구용 항체 시약 시장, 출처별, 2018-2032(백만 달러)

표 39 아시아 태평양 항체 연구용 항체 시약 시장, 출처 기준, 2018-2032 (백만 달러)

표 40 아시아 태평양 연구용 시약 항체 시약 시장, 유형별, 2018-2032(백만 달러)

표 41 아시아 태평양 버퍼 및 솔루션 연구용 항체 시약 시장, 유형별, 2018-2032 (백만 달러)

표 42 아시아 태평양 연구용 항체 시약 시장, 응용 분야별, 2018-2032(백만 달러)

표 43 아시아 태평양 연구 항체 시약 시장, 연구 분야별, 2018-2032 (백만 달러)

표 44 아시아 태평양 연구용 항체 시약 시장, 최종 사용자별, 2018-2032년(백만 달러)

표 45 아시아 태평양 연구용 항체 시약 시장, 유통 채널별, 2018-2032년(백만 달러)

표 46 중국 연구 항체 시약 시장, 유형별, 2018-2032 (백만 달러)

표 47 중국 항체 연구용 항체 시약 시장, 제품별, 2018-2032(백만 달러)

표 48 중국 항체 연구용 항체 시약 시장, 출처별, 2018-2032(백만 달러)

표 49 중국 항체 연구용 항체 시약 시장, 출처 기준, 2018-2032(백만 달러)

표 50 중국 연구용 항체 시약 시장, 유형별, 2018-2032(백만 달러)

표 51 중국 버퍼 및 솔루션 연구용 항체 시약 시장, 유형별, 2018-2032(백만 달러)

표 52 중국 연구 항체 시약 시장, 응용 분야별, 2018-2032(백만 달러)

표 53 중국 연구 항체 시약 시장, 연구 분야별, 2018-2032 (백만 달러)

표 54 중국 연구 항체 시약 시장, 최종 사용자별, 2018-2032(백만 달러)

표 55 중국 연구 항체 시약 시장, 유통 채널별, 2018-2032 (백만 달러)

표 56 일본 연구 항체 시약 시장, 유형별, 2018-2032 (백만 달러)

표 57 일본 항체 연구용 항체 시약 시장, 제품별, 2018-2032(백만 달러)

표 58 일본 항체 연구용 항체 시약 시장, 출처별, 2018-2032(백만 달러)

표 59 일본 항체 연구용 항체 시약 시장, 출처 기준, 2018-2032 (백만 달러)

표 60 일본 연구용 시약 항체 시약 시장, 유형별, 2018-2032(백만 달러)

표 61 일본 버퍼 및 연구용 항체 시약 시장, 유형별, 2018-2032(백만 달러)

표 62 일본 연구 항체 시약 시장, 응용 분야별, 2018-2032 (백만 달러)

표 63 일본 연구 항체 시약 시장, 연구 분야별, 2018-2032 (백만 달러)

표 64 일본 연구 항체 시약 시장, 최종 사용자별, 2018-2032(백만 달러)

표 65 일본 연구 항체 시약 시장, 유통 채널별, 2018-2032 (백만 달러)

표 66 인도 연구 항체 시약 시장, 유형별, 2018-2032(백만 달러)

표 67 인도 항체 연구용 항체 시약 시장, 제품별, 2018-2032(백만 달러)

표 68 인도 항체 연구용 항체 시약 시장, 출처별, 2018-2032(백만 달러)

표 69 인도 항체 연구용 항체 시약 시장, 출처 기준, 2018-2032(백만 달러)

표 70 인도 연구용 시약 항체 시약 시장, 유형별, 2018-2032(백만 달러)

표 71 인도 버퍼 및 솔루션 연구용 항체 시약 시장, 유형별, 2018-2032(백만 달러)

표 72 인도 연구 항체 시약 시장, 응용 분야별, 2018-2032(백만 달러)

표 73 인도 연구 항체 시약 시장, 연구 분야별, 2018-2032(백만 달러)

표 74 인도 연구 항체 시약 시장, 최종 사용자별, 2018-2032(백만 달러)

표 75 인도 연구 항체 시약 시장, 유통 채널별, 2018-2032년(백만 달러)

표 76 한국 연구용 항체 시약 시장, 유형별, 2018-2032 (백만 달러)

표 77 한국 항체 연구용 항체 시약 시장, 제품별, 2018-2032 (백만 달러)

표 78 한국 항체 연구용 항체 시약 시장, 출처별, 2018-2032 (백만 달러)

표 79 한국 항체 연구용 항체 시약 시장, 출처 기준, 2018-2032 (백만 달러)

표 80 한국 연구용 항체 시약 시장, 유형별, 2018-2032(백만 달러)

표 81 한국 버퍼 및 솔루션 연구용 항체 시약 시장, 유형별, 2018-2032 (백만 달러)

표 82 한국 연구용 항체 시약 시장, 응용 분야별, 2018-2032 (백만 달러)

표 83 한국 연구용 항체 시약 시장, 연구 분야별, 2018-2032 (백만 달러)

표 84 한국 연구용 항체 시약 시장, 최종 사용자별, 2018-2032 (백만 달러)

표 85 한국 연구용 항체 시약 시장, 유통 채널별, 2018-2032 (백만 달러)

표 86 호주 연구 항체 시약 시장, 유형별, 2018-2032(백만 달러)

표 87 호주 항체 연구용 항체 시약 시장, 제품별, 2018-2032(백만 달러)

표 88 호주 항체 연구 항체 시약 시장, 출처별, 2018-2032(백만 달러)

표 89 호주 항체 연구용 항체 시약 시장, 출처 기준, 2018-2032(백만 달러)

표 90 호주 연구용 시약 항체 시약 시장, 유형별, 2018-2032(백만 달러)

표 91 호주 버퍼 및 연구용 항체 시약 시장, 유형별, 2018-2032(백만 달러)

표 92 호주 연구 항체 시약 시장, 응용 분야별, 2018-2032(백만 달러)

표 93 호주 연구 항체 시약 시장, 연구 분야별, 2018-2032 (백만 달러)

표 94 호주 연구 항체 시약 시장, 최종 사용자별, 2018-2032(백만 달러)

표 95 호주 연구 항체 시약 시장, 유통 채널별, 2018-2032(백만 달러)

표 96 싱가포르 연구용 항체 시약 시장, 유형별, 2018-2032년(백만 달러)

표 97 싱가포르 항체 연구용 항체 시약 시장, 제품별, 2018-2032(백만 달러)

표 98 싱가포르 항체 연구용 항체 시약 시장, 출처별, 2018-2032(백만 달러)

표 99 싱가포르 항체 연구용 항체 시약 시장, 출처 기준, 2018-2032(백만 달러)

표 100 싱가포르 연구용 항체 시약 시장, 유형별, 2018-2032(백만 달러)

표 101 싱가포르 버퍼 및 솔루션 연구용 항체 시약 시장, 유형별, 2018-2032(백만 달러)

표 102 싱가포르 연구 항체 시약 시장, 응용 분야별, 2018-2032(백만 달러)

표 103 싱가포르 연구 항체 시약 시장, 연구 분야별, 2018-2032 (백만 달러)

표 104 싱가포르 연구용 항체 시약 시장, 최종 사용자별, 2018-2032년(백만 달러)

표 105 싱가포르 연구용 항체 시약 시장, 유통 채널별, 2018-2032년(백만 달러)

표 106 태국 연구 항체 시약 시장, 유형별, 2018-2032 (백만 달러)

표 107 태국 항체 연구용 항체 시약 시장, 제품별, 2018-2032(백만 달러)

표 108 태국 항체 연구 항체 시약 시장, 출처별, 2018-2032(백만 달러)

표 109 태국 항체 연구 항체 시약 시장, 출처별, 2018-2032(백만 달러)

표 110 태국 연구용 항체 시약 시장, 유형별, 2018-2032(백만 달러)

표 111 태국 버퍼 및 연구용 항체 시약 시장, 유형별, 2018-2032(백만 달러)

표 112 태국 연구 항체 시약 시장, 응용 분야별, 2018-2032(백만 달러)

표 113 태국 연구 항체 시약 시장, 연구 분야별, 2018-2032 (백만 달러)

표 114 태국 연구 항체 시약 시장, 최종 사용자별, 2018-2032(백만 달러)

표 115 태국 연구 항체 시약 시장, 유통 채널별, 2018-2032(백만 달러)

표 116 말레이시아 연구용 항체 시약 시장, 유형별, 2018-2032년(백만 달러)

표 117 말레이시아 항체 연구용 항체 시약 시장, 제품별, 2018-2032(백만 달러)

표 118 말레이시아 항체 연구용 항체 시약 시장, 출처별, 2018-2032(백만 달러)

표 119 말레이시아 항체 연구용 항체 시약 시장, 원산지 기준, 2018-2032년(백만 달러)

표 120 말레이시아 연구용 시약 항체 시약 시장, 유형별, 2018-2032(백만 달러)

표 121 말레이시아 버퍼 및 용액 연구용 항체 시약 시장, 유형별, 2018-2032(백만 달러)

표 122 말레이시아 연구 항체 시약 시장, 응용 분야별, 2018-2032(백만 달러)

표 123 말레이시아 연구 항체 시약 시장, 연구 분야별, 2018-2032 (백만 달러)

표 124 말레이시아 연구용 항체 시약 시장, 최종 사용자별, 2018-2032년(백만 달러)

표 125 말레이시아 연구용 항체 시약 시장, 유통 채널별, 2018-2032년(백만 달러)

표 126 인도네시아 연구용 항체 시약 시장, 유형별, 2018-2032 (백만 달러)

표 127 인도네시아 항체 연구용 항체 시약 시장, 제품별, 2018-2032(백만 달러)

표 128 인도네시아 항체 연구용 항체 시약 시장, 출처별, 2018-2032(백만 달러)

표 129 인도네시아 항체 연구용 항체 시약 시장, 원산지 기준, 2018-2032년(백만 달러)

표 130 인도네시아 연구용 시약 항체 시약 시장, 유형별, 2018-2032(백만 달러)

표 131 인도네시아 버퍼 및 용액 연구용 항체 시약 시장, 유형별, 2018-2032(백만 달러)

표 132 인도네시아 연구 항체 시약 시장, 응용 분야별, 2018-2032(백만 달러)

표 133 인도네시아 연구 항체 시약 시장, 연구 분야별, 2018-2032 (백만 달러)

표 134 인도네시아 연구용 항체 시약 시장, 최종 사용자별, 2018-2032년(백만 달러)

표 135 인도네시아 연구용 항체 시약 시장, 유통 채널별, 2018-2032년(백만 달러)

표 136 필리핀 연구 항체 시약 시장, 유형별, 2018-2032 (백만 달러)

표 137 필리핀 항체 연구용 항체 시약 시장, 제품별, 2018-2032(백만 달러)

표 138 필리핀 항체 연구용 항체 시약 시장, 출처별, 2018-2032(백만 달러)

표 139 필리핀 항체 연구용 항체 시약 시장, 원산지 기준, 2018-2032년(백만 달러)

표 140 필리핀 연구용 항체 시약 시장, 유형별, 2018-2032(백만 달러)

표 141 필리핀 버퍼 및 연구용 항체 시약 시장, 유형별, 2018-2032(백만 달러)

표 142 필리핀 연구 항체 시약 시장, 응용 분야별, 2018-2032(백만 달러)

표 143 필리핀 연구 항체 시약 시장, 연구 분야별, 2018-2032 (백만 달러)

표 144 필리핀 연구 항체 시약 시장, 최종 사용자별, 2018-2032(백만 달러)

표 145 필리핀 연구 항체 시약 시장, 유통 채널별, 2018-2032 (백만 달러)

표 146 아시아 태평양 연구용 항체 시약 시장 나머지 지역, 유형별, 2018-2032년(백만 달러)

그림 목록

그림 1 아시아 태평양 연구 항체 시약 시장: 세분화

그림 2 아시아 태평양 연구 항체 시약 시장: 데이터 삼각 측량

그림 3 아시아 태평양 연구 항체 시약 시장: DROC 분석

그림 4 아시아 태평양 연구 항체 시약 시장: 아시아 태평양 대 지역 시장 분석

그림 5 아시아 태평양 연구 항체 시약 시장: 회사 연구 분석

그림 6 아시아 태평양 연구 항체 시약 시장: 다변량 모델링

그림 7 아시아 태평양 연구 항체 시약 시장: 인터뷰 인구 통계

그림 8 아시아 태평양 연구 항체 시약 시장: DBMR 시장 위치 그리드

그림 9 아시아 태평양 연구 항체 시약 시장: 세분화

그림 10 요약

그림 11 전략적 결정

그림 12 아시아 태평양 연구 항체 시약 시장

그림 13 항체 세그먼트는 2025년~2032년 아시아 태평양 연구용 항체 시약 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다.

그림 14 DROC 분석

그림 15 아시아 태평양 연구 항체 시약 시장: 유형별, 2024

그림 16 아시아 태평양 연구 항체 시약 시장: 유형별, 2025-2032(백만 달러)

그림 17 아시아 태평양 연구 항체 시약 시장: 유형별, CAGR(2025-2032)

그림 18 아시아 태평양 연구 항체 시약 시장: 유형별, 수명선 곡선

그림 19 아시아 태평양 연구 항체 시약 시장: 응용 분야별, 2024

그림 20 아시아 태평양 연구 항체 시약 시장: 응용 분야별, 2025-2032(백만 달러)

그림 21 아시아 태평양 연구 항체 시약 시장: 응용 분야별, CAGR(2025-2032)

그림 22 아시아 태평양 연구 항체 시약 시장: 응용 분야별, 수명선 곡선

그림 23 아시아 태평양 연구 항체 시약 시장: 연구 분야별, 2024

그림 24 아시아 태평양 연구 항체 시약 시장: 연구 분야별, 2025-2032(백만 달러)

그림 25 아시아 태평양 연구 항체 시약 시장: 연구 분야별, CAGR(2025-2032)

그림 26 아시아 태평양 연구 항체 시약 시장: 연구 분야별, 수명선 곡선

그림 27 아시아 태평양 연구 항체 시약 시장: 최종 사용자별, 2024

그림 28 아시아 태평양 연구용 항체 시약 시장: 최종 사용자별, 2025-2032년(백만 달러)

그림 29 아시아 태평양 연구용 항체 시약 시장: 최종 사용자별, CAGR(2025-2032)

그림 30 아시아 태평양 연구 항체 시약 시장: 최종 사용자별, 수명선 곡선

그림 31 아시아 태평양 연구 항체 시약 시장: 유통 채널별, 2024

그림 32 아시아 태평양 연구 항체 시약 시장: 유통 채널별, 2025-2032년(백만 달러)

그림 33 아시아 태평양 연구 항체 시약 시장: 유통 채널별, CAGR(2025-2032)

그림 34 아시아 태평양 연구 항체 시약 시장: 유통 채널별, 수명선 곡선

그림 35 아시아 태평양 연구 항체 시약 시장: 스냅샷(2024)

그림 36 아시아 태평양 연구 항체 시약 시장: 회사 점유율 2024(%)

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.