Europe Angiography Devices Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

3.75 Billion

USD

5.60 Billion

2024

2032

USD

3.75 Billion

USD

5.60 Billion

2024

2032

| 2025 –2032 | |

| USD 3.75 Billion | |

| USD 5.60 Billion | |

| % | |

|

유럽 혈관조영술 장비 시장 세분화, 제품별(혈관조영술 시스템, 혈관조영술 조영제, 혈관 폐쇄 장치, 혈관조영술 풍선, 혈관조영술 카테터, 혈관조영술 가이드와이어, 혈관조영술 부속품), 기술별(X선 혈관조영술, CT 혈관조영술, MRA 혈관조영술, 기타), 시술별(관상동맥 혈관조영술, 혈관내 혈관조영술, 신경혈관 혈관조영술, 종양 혈관조영술, 기타), 적응증(관상동맥 질환, 판막성 심장 질환, 선천성 심장 질환, 울혈성 심부전, 기타 적응증), 응용 분야(진단, 치료), 최종 사용자(병원 및 진료소, 진단 및 영상 센터, 연구소) - 산업 동향 및 2032년까지의 전망

혈관조영술 장치 시장 규모

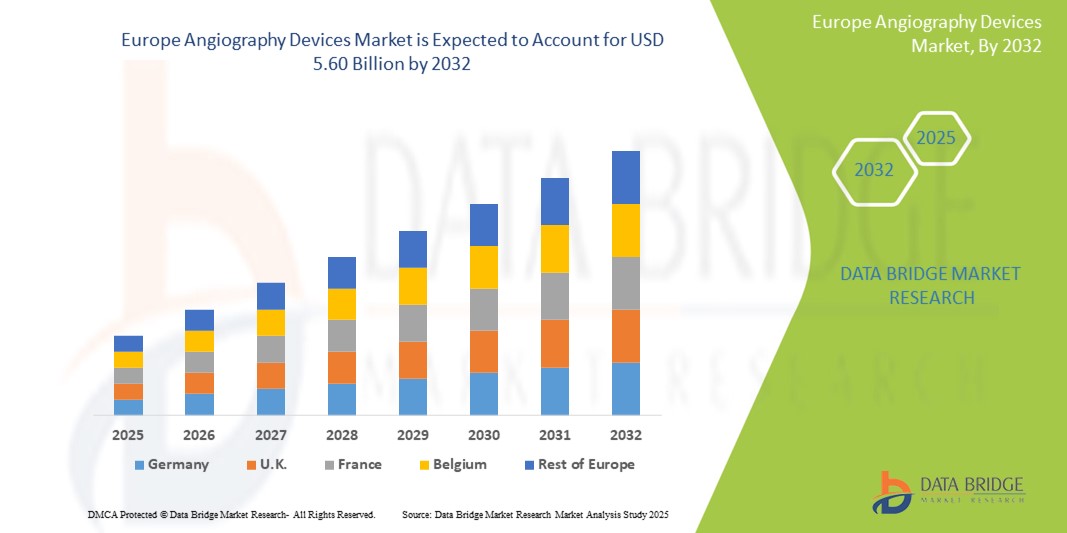

- 유럽 혈관조영술 장비 시장 규모는 2024년에 37억 5천만 달러 로 평가되었으며 예측 기간 동안 5.8%의 CAGR 로 2032년까지 56억 달러 에 도달할 것으로 예상됩니다 .

- 시장 성장은 주로 심혈관 질환의 발생률 증가, 인구 고령화, 혈관 질환의 조기 정확한 진단에 대한 수요 증가에 힘입은 것입니다.

- 더욱이, 3D 영상 기능 및 첨단 내비게이션 시스템과 같은 혈관조영술 시스템의 기술 발전이 시장 확대를 촉진하고 있습니다. 이러한 융합 요인들은 다양한 의료 분야에서 혈관조영술 장비 도입을 가속화하여 산업 성장을 크게 촉진하고 있습니다.

혈관조영술 장비 시장 분석

- 혈관조영술 장비 시장은 혈관과 장기를 시각화하는 데 사용되는 다양한 의료 영상 장비 및 소모품을 포함합니다. 여기에는 혈관조영술 시스템(C-암, 카테터실), 카테터, 가이드 와이어, 조영제 주입기 및 기타 액세서리가 포함됩니다. 이러한 장비는 다양한 심혈관, 신경 및 말초 혈관 질환의 진단 및 치료에 필수적입니다. 이 시장은 심혈관 질환 유병률 증가, 영상 기술의 발전, 그리고 최소 침습 시술에 대한 수요 증가에 의해 주도되고 있습니다.

- 혈관조영술 장비에 대한 수요가 급증하는 주된 이유는 중재적 심장학 및 영상의학 시술의 증가, 최소 침습 기술의 도입 증가, 혈관 질환의 조기 진단 및 중재의 이점에 대한 인식이 높아지고 있기 때문입니다.

- 영국은 2025년 유럽 혈관조영술 기기 시장에서 87.45%의 가장 큰 매출 점유율을 기록하며 시장을 장악할 것으로 예상됩니다. 이는 탄탄한 의료 인프라, 최소 침습 시술 도입률 증가, 심혈관 질환 유병률 증가, 그리고 중재적 심장학에 대한 적극적인 투자 덕분입니다. 주요 제조업체들의 입지와 높은 R&D 투자는 시장 성장을 더욱 뒷받침합니다.

- 영국은 고령 인구 증가, 유리한 보험급여 정책, 그리고 평판 검출기 및 3D 회전 혈관조영술 시스템과 같은 첨단 기기에 대한 수요 증가로 인해 유럽 혈관조영술 기기 시장에서 가장 빠르게 성장하는 국가가 될 것으로 예상됩니다. 지속적인 임상 발전과 주요 업체 간의 전략적 협력 또한 시장 확대에 기여하고 있습니다.

- 혈관조영술 카테터는 혈관 상태를 영상화하는 데 있어 정밀하고, 관상동맥 및 말초 혈관조영술 시술에 널리 적용되며, 최소 침습성과 임상적 효능으로 인해 진단 및 중재적 심장학에서 채택이 증가하고 있어 2025년에 시장 점유율 38.2%로 유럽 혈관조영술 장비 시장을 지배할 것으로 예상됩니다.

보고서 범위 및 혈관조영술 장치 시장 세분화

|

속성 |

혈관조영술 장치 주요 시장 통찰력 |

|

다루는 세그먼트 |

|

|

포함 국가 |

유럽

|

|

주요 시장 참여자 |

|

|

시장 기회 |

|

|

부가가치 데이터 정보 세트 |

Data Bridge Market Research에서 큐레이팅한 시장 보고서에는 시장 가치, 성장률, 세분화, 지리적 적용 범위, 주요 기업 등 시장 시나리오에 대한 통찰력 외에도 심층적인 전문가 분석, 가격 분석, 브랜드 점유율 분석, 소비자 설문 조사, 인구 통계 분석, 공급망 분석, 가치 사슬 분석, 원자재/소모품 개요, 공급업체 선택 기준, PESTLE 분석, Porter 분석 및 규제 프레임워크가 포함되어 있습니다. |

혈관조영술 장비 시장 동향

“3D 이미징과 첨단 내비게이션 시스템의 통합 ”

- 첨단 영상 및 내비게이션 기술의 통합: 유럽 혈관조영술 장비 시장의 주요 추세는 첨단 영상 기술과 내비게이션 기술의 통합이 심화되고 있다는 것입니다. 이러한 융합은 복잡한 중재적 시술에서 진단 정확도, 시술 효율성, 그리고 환자 안전을 크게 향상시키고 있습니다.

- 예를 들어, 최신 혈관조영술 시스템은 2D 투시 검사와 3D 영상 기능(예: CT 유사 영상 또는 회전 혈관조영술)을 결합하여 포괄적인 해부학적 영상을 제공합니다. 이를 통해 임상의는 복잡한 혈관 구조를 시각화하고 더욱 정확하게 시술을 계획할 수 있습니다.

- 로봇 보조 혈관조영술 및 전자기 추적을 포함한 첨단 내비게이션 시스템의 개발은 카테터 조작성을 향상시키고 환자와 의료진 모두의 방사선 노출을 줄이고 있습니다. 또한, 환자 데이터 관리 시스템(PACS/HIS)과의 원활한 통합을 통해 워크플로우를 간소화하고 실시간 의사 결정을 용이하게 합니다.

- 더욱 지능적이고 통합적이며 정밀한 혈관조영술 시스템을 지향하는 이러한 추세는 중재적 심장학 및 영상의학 진료를 근본적으로 변화시키고 있습니다. 따라서 기업들은 향상된 자동화 및 실시간 안내 기능을 갖춘 차세대 혈관조영술 플랫폼을 개발하기 위해 R&D에 막대한 투자를 하고 있습니다.

- 최적의 환자 결과와 시술 효율성을 우선시하는 임상의들이 늘어나면서, 첨단 영상과 내비게이션을 원활하게 통합하는 혈관조영술 장비에 대한 수요가 병원과 심장/혈관 전문 센터에서 빠르게 증가하고 있습니다.

혈관조영술 장비 시장 동향

운전사

“심혈관 질환 발병률 증가”

- 유럽에서 심혈관 질환(CVD)의 발생률이 증가하는 것은 혈관조영술 장비 시장 성장을 촉진하는 주요 요인입니다.

- 예를 들어, 미국심장협회(AHA)에 따르면 심혈관 질환(CVD)은 영국에서 이환율과 사망률의 주요 원인으로 남아 있으며, 이로 인해 많은 양의 진단 및 중재적 시술이 필요합니다. 혈관조영술은 관상동맥 질환, 말초동맥 질환 및 기타 혈관 질환을 진단하고 중재적 치료를 결정하는 데 중요한 역할을 합니다.

- 인구 고령화와 비만, 당뇨, 고혈압과 같은 생활 습관 요인이 결합되어 심혈관 질환 부담이 증가하고 있으며, 이로 인해 혈관조영술에 대한 수요도 증가하고 있습니다.

- Furthermore, advancements in interventional techniques and the growing preference for minimally invasive procedures are fueling the adoption of advanced angiography devices.

- Increasing awareness about early diagnosis and treatment of vascular diseases is also driving market growth

Restraint/Challenge

“High Cost of Angiography Systems and Reimbursement Issues”

- The high cost of advanced angiography systems and the complexities associated with reimbursement pose a significant challenge to broader market adoption, particularly for smaller healthcare facilities and those with budget constraints.

- For instance, a state-of-the-art angiography system can cost several million dollars, representing a substantial capital investment for hospitals and diagnostic centers. This high initial cost can limit access to advanced angiography technologies, especially in underserved areas.

- The need for specialized infrastructure, such as dedicated cath labs, and highly trained personnel (interventional cardiologists, radiologists, and technologists) further adds to the operational burden.

- Additionally, variations in reimbursement policies across different healthcare systems and insurance providers can create financial uncertainty, potentially limiting the volume of procedures performed.

- Addressing these challenges requires efforts to reduce manufacturing costs, develop more cost-effective solutions, and advocate for favorable reimbursement policies to ensure wider accessibility of angiography procedures

Angiography Devices Market Scope

The market is segmented on the basis product, technology, procedure, indication, application and end user.

- By Product

On the basis of product, the Europe angiography devices market is segmented into angiography systems, angiography contrast media, vascular closure devices, angiography balloons, angiography catheters, angiography guidewires and angiography accessories. The Angiography Catheters segment dominates the largest market revenue share of 38.2% in 2025, driven by high demand for advanced imaging platforms that provide precise visualization of vascular structures. These systems are integral in both diagnostic and interventional procedures and are continually evolving with innovations such as flat-panel detectors, rotational angiography, and hybrid OR integration.

The vascular closure devices segment is anticipated to witness the fastest growth rate of 9.6% from 2025 to 2032, due to the growing shift toward minimally invasive procedures. These devices enable rapid hemostasis and early ambulation, reducing patient discomfort and improving hospital workflow efficiency.

- By technology

On the basis of technology, the market is segmented into X-ray angiography, CT angiography, and MRA angiography and other. X-ray angiography is further segmented into image Intensifiers and flat-panel detectors. X-ray angiography segment held the largest market revenue share in 2025, due to its established use in coronary and peripheral vascular assessments, and its compatibility with catheter-based procedures. It remains the backbone of interventional cardiology owing to its real-time visualization capabilities and precision.

The CT angiography segment is expected to witness the fastest CAGR from 2025 to 2032, fueled by advancements in multi-slice CT systems, increased preference for non-invasive imaging, and broader applications in detecting aortic aneurysms, pulmonary embolism, and peripheral artery disease.

- By Procedure

On the basis of procedure, the market segmented into coronary angiography, endovascular angiography, neurovascular angiography, onco-angiography and other. The Coronary angiography segment accounted for the largest market revenue share in 2025, owing to the high burden of coronary artery disease in the region and the growing demand for timely diagnosis and treatment. This procedure remains a critical diagnostic step before interventions such as angioplasty or stenting.

The Neurovascular angiography segment is projected to witness the fastest CAGR from 2025 to 2032, attributed to increasing incidence of stroke and cerebrovascular anomalies, along with expanding access to specialized neurological centers and interventional neuroradiology capabilities.

- By Indication

On the basis of Indication, the market segmented into coronary artery disease, valvular heart disease, congenital heart disease, congestive heart failure, and other indications. The Coronary artery disease segment accounted for the largest market revenue share in 2025, driven by lifestyle-related risk factors, an aging population, and widespread screening initiatives across Europe.

The Congestive heart failure segment is projected to witness the fastest CAGR from 2025 to 2032, as angiography increasingly supports both diagnosis and interventional planning in patients with complex heart failure conditions, particularly in the elderly.

- By Application

On the basis of Application, the market segmented into diagnostics and therapeutics. The diagnostics segment accounted for the largest market revenue share in 2025, as angiography remains the cornerstone for identifying vascular obstructions, aneurysms, and structural anomalies. Its high sensitivity and ability to guide subsequent interventions support its leading role.

The therapeutics segment is projected to witness the fastest CAGR from 2025 to 2032, reflecting the rise in image-guided procedures such as angioplasty, stenting, and embolization therapies—supported by hybrid ORs and improved device compatibility.

- By End User

On the basis of end user, the market is segmented into hospitals and clinics, diagnostic and imaging centers and research institutes. The Hospitals and clinics segment holds the largest market revenue share in 2025, due to their capacity to perform complex angiographic procedures, access to high-end imaging systems, and multidisciplinary expertise. These facilities are central to both routine diagnostics and emergency cardiovascular care.

The Diagnostic and imaging centers segment is expected to witness the fastest growth from 2025 to 2032, driven by the increasing preference for outpatient diagnostics, shorter patient wait times, and cost-effectiveness. Technological advancements enabling high-quality non-invasive angiographic imaging also support this trend.

Angiography Devices Market Regional Analysis

- U.K. dominates the Angiography Devices market with the largest revenue share of 87.45% in 2024, primarily driven by a high burden of cardiovascular diseases, robust diagnostic infrastructure, and strong reimbursement frameworks.

- The widespread adoption of advanced imaging systems—including digital flat-panel detectors and AI-assisted angiography platforms—continues to enhance procedural accuracy and clinical outcomes.

- Government initiatives such as the Million Hearts program and the American Heart Association’s screening campaigns have led to greater uptake of preventive and diagnostic cardiovascular imaging, boosting demand for angiography procedures.

- The presence of major industry players like GE HealthCare, Siemens Healthineers, and Philips, along with aggressive investments in R&D and product innovation, strengthens the U.K. market.

- Additionally, the shift toward minimally invasive and outpatient-based interventions—supported by ambulatory surgical centers—is accelerating the use of catheter-based angiography devices across multiple clinical settings.

Germany Angiography Devices Market Insight

The Germany Angiography Devices market is projected to expand at a substantial CAGR throughout the forecast period, driven by the growing incidence of breast cancer and increased investments in public health diagnostics. Germany’s national health strategy emphasizes early cancer detection, and provinces have rolled out organized breast screening programs (such as Ontario Breast Screening Program), boosting demand for advanced biopsy systems. Additionally, rising awareness about the benefits of minimally invasive biopsies over surgical alternatives and the growing availability of MRI-guided and stereotactic-guided techniques in diagnostic centers are contributing to market expansion.

France Angiography Devices Market Insight

프랑스 혈관조영술 기기 시장은 의료 인프라의 지속적인 개선과 심혈관 건강에 대한 정부의 관심 증가에 힘입어 예측 기간 동안 주목할 만한 연평균 성장률(CAGR)로 성장할 것으로 예상됩니다. 과체중, 비만, 당뇨병 예방 및 관리를 위한 국가 전략과 같은 사업은 혈관조영술을 포함한 심혈관 진단에 대한 수요를 증가시켰습니다. 첨단 중재적 시술 시스템 접근성은 여전히 도시 3차 의료기관에 국한되어 있지만, 민관 협력 및 국제 협력을 통해 2차 및 농촌 의료 환경에서의 기술 보급이 점차 확대되고 있습니다. 조기 심혈관 위험 선별 검사에 대한 인식 제고와 심장내과 전문의 및 영상의학과 전문의 교육 프로그램 개선은 카테터 기반 혈관조영술 및 CT/MR 혈관조영술의 광범위한 도입을 뒷받침하고 있습니다.

혈관조영술 장비 시장 점유율

혈관조영술 장비 산업은 주로 다음을 포함한 기존 기업들이 주도하고 있습니다.

- 지멘스 헬시니어스(독일)

- GE 헬스케어(미국)

- 필립스 헬스케어(네덜란드)

- 캐논 메디컬 시스템즈 주식회사(일본)

- 보스턴 사이언티픽 코퍼레이션(미국)

- 메드트로닉(아일랜드)

- 애보트 연구소(미국)

- 테루모 주식회사(일본)

- 코디스(미국)

- 시마즈 주식회사(일본)

유럽 혈관조영술 장비 시장의 최신 동향

-

2024년 3월, 지멘스 헬시니어스는 첨단 3D 영상과 AI 기반 영상 처리 기능을 갖춘 차세대 혈관조영술 시스템을 출시했습니다. 이 시스템은 복잡한 혈관 구조의 시각화를 향상시켜 진단 정확도와 중재적 시술 계획을 개선하며, 특히 신경혈관 및 말초혈관 시술에서 더욱 효과적입니다. 또한, 임상의가 고도의 예민한 환경에서 실시간 의사 결정과 최적화된 워크플로우를 통해 환자를 지원합니다.

- 2024년 2월, GE 헬스케어는 뛰어난 조종성과 어려운 해부학적 부위 접근성을 위해 설계된 새로운 혈관조영 카테터를 출시했습니다. 말초 혈관 중재술 시 내비게이션을 개선하도록 설계된 이 카테터는 임상적 정확도를 높이고, 시술 시간을 단축하며, 복잡한 혈관 병변 치료에서 향상된 결과를 지원합니다.

- 2024년 1월, 필립스 헬스케어는 로봇 수술 분야를 선도하는 기업과 전략적 파트너십을 체결하여 로봇 보조 혈관조영술 시스템을 공동 개발한다고 발표했습니다. 이 협력은 신경혈관 시술에서 카테터 내비게이션 정확도와 제어력을 향상시키고, 필립스의 영상 전문 지식과 로봇 정밀성을 결합하여 최소 침습 혈관 중재술을 실현하는 것을 목표로 합니다.

- 2023년 12월, 보스턴 사이언티픽은 향상된 윤활성과 향상된 팁 유연성을 갖춘 최신 가이드 와이어에 대한 FDA 승인을 받았습니다. 복잡한 관상동맥 해부학적 구조를 탐색하도록 설계된 이 장치는 고위험 관상동맥 중재술에서 시술 성공률을 높이고 합병증 발생률을 낮추는 것을 목표로 합니다.

- 2023년 11월, 메드트로닉은 차세대 선량 관리 기능과 환자 정보 시스템과의 완벽한 통합을 제공하는 새로운 조영제 주입 시스템을 출시했습니다. 워크플로우 효율성을 높이고 조영제 사용을 최적화하도록 설계된 이 시스템은 진단 및 중재적 혈관조영술 시술 시 영상 안전성과 정밀도를 향상시킵니다.

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.