Europe Dental Instruments Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

1.31 Billion

USD

1.98 Billion

2025

2033

USD

1.31 Billion

USD

1.98 Billion

2025

2033

| 2026 –2033 | |

| USD 1.31 Billion | |

| USD 1.98 Billion | |

| % | |

|

Europe Dental Instruments Market Segmentation, By Product (Perio/Oral Surgery, Hygiene, Diagnostic, Endodontic, Operative, and Others), Instrument Type (Examination Instruments, Cutting Instruments, and Others), End User (Hospitals, Clinics, Dental Laboratories, Scientific Research, and Others), Distribution Channel (Direct Tender, Third Party Distributors and Retail Sales) - Industry Trends and Forecast to 2033

Europe Dental Instruments Market Size

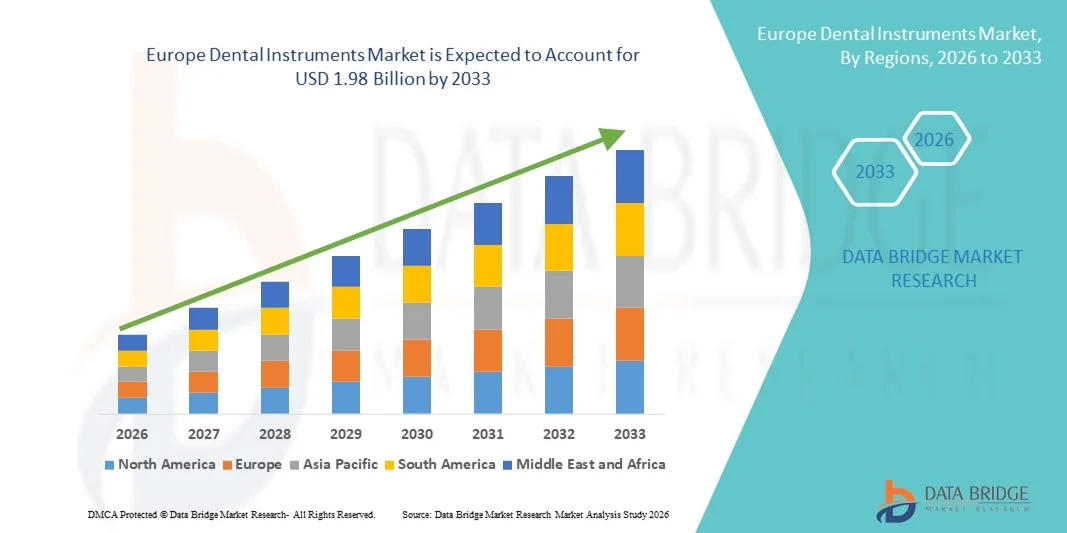

- The Europe dental instruments market size was valued at USD 1.31 billion in 2025 and is expected to reach USD 1.98 billion by 2033, at a CAGR of 5.30% during the forecast period

- The market growth is largely fueled by the increasing prevalence of dental disorders, rising awareness regarding oral hygiene, and technological advancements in dental care equipment, leading to greater adoption of advanced dental instruments across clinics, hospitals, and specialty dental centers

- Furthermore, growing demand for cosmetic and restorative dental procedures, increasing healthcare expenditure, and continuous innovation in minimally invasive and precision-based dental instruments are establishing dental instruments as essential tools in modern dentistry. These converging factors are accelerating the uptake of Dental Instruments solutions, thereby significantly boosting the industry's growth

Europe Dental Instruments Market Analysis

- Dental instruments, encompassing a wide range of diagnostic, preventive, restorative, and surgical tools, are fundamental components of modern oral healthcare delivery across hospitals, dental clinics, and academic institutes, owing to their critical role in accurate diagnosis, precision treatment, and improved patient outcomes

- The escalating demand for dental instruments is primarily fueled by the rising prevalence of dental caries, periodontal diseases, and tooth loss, along with increasing awareness of oral hygiene, growing demand for cosmetic dentistry procedures, and continuous technological advancements in minimally invasive and ergonomic instrument design

- The U.K. dominated the dental instruments market in Europe with the largest revenue share of 24.7% in 2025, supported by a well-established public and private dental care system, strong presence of advanced dental clinics, high awareness regarding oral hygiene, and consistent adoption of technologically advanced dental instruments. The country’s emphasis on preventive dentistry and cosmetic procedures, along with favorable healthcare spending, continues to drive steady demand for precision-based and minimally invasive dental instruments

- Germany is expected to be the fastest-growing market for dental instruments during the forecast period, owing to increasing demand for restorative and aesthetic dental procedures, rising geriatric population, growing dental tourism, and continuous investments in advanced dental technologies. Germany accounted for approximately 21.3% of the regional market share in 2025, and its strong manufacturing base and expanding private dental care sector are further accelerating market growth

- The Examination Instruments segment held the largest market revenue share of 34.8% in 2025, driven by their essential role in routine dental diagnostics and check-ups

Report Scope and Dental Instruments Market Segmentation

|

Attributes |

Dental Instruments Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Europe Dental Instruments Market Trends

Rising Adoption of Advanced and Minimally Invasive Dental Technologies

- A significant and accelerating trend in the dental instruments market is the growing adoption of advanced, precision-based, and minimally invasive dental technologies across clinics and hospitals. Dental professionals are increasingly shifting toward high-performance instruments that enhance procedural accuracy, reduce patient discomfort, and improve overall treatment outcomes. This transition is being supported by technological advancements in rotary instruments, digital imaging-compatible tools, ergonomic handpieces, and laser-assisted dental devices

- For instance, several leading dental clinics in Germany and France have upgraded to next-generation electric handpieces and precision endodontic instruments that enable faster root canal procedures with improved accuracy and reduced chair time. Such upgrades are improving workflow efficiency while enhancing patient satisfaction

- The increasing focus on cosmetic dentistry, including veneers, teeth whitening, and smile correction procedures, is further accelerating the demand for specialized dental instruments designed for aesthetic precision

- In addition, the integration of digital dentistry solutions, such as CAD/CAM-supported restorative tools and implantology instrument kits, is enabling more accurate and customized treatment planning

- The growing emphasis on infection control and sterilization standards in European dental practices is also encouraging the adoption of high-quality stainless steel and autoclavable instruments that ensure safety and regulatory compliance

- This trend toward technologically advanced, ergonomic, and procedure-specific dental instruments is reshaping clinical practices across Europe, prompting manufacturers to continuously innovate and expand their product portfolios

Europe Dental Instruments Market Dynamics

Driver

Increasing Prevalence of Dental Disorders and Growing Geriatric Population

- The rising prevalence of dental conditions such as dental caries, periodontal diseases, tooth loss, and oral infections is a major driver for the Dental Instruments market. Poor dietary habits, tobacco consumption, and inadequate oral hygiene practices continue to increase the burden of oral diseases across

- For instance, according to European oral health reports, a significant proportion of adults suffer from untreated dental caries and gum disease, prompting governments and healthcare providers to expand preventive and restorative dental services. This growing patient pool directly increases the demand for diagnostic, surgical, and restorative dental instruments

- The rapidly growing geriatric population in countries further contributes to market expansion, as older individuals are more prone to tooth decay, edentulism, and implant procedures

- Increasing awareness campaigns promoting preventive dental check-ups and early diagnosis are encouraging more frequent dental visits, thereby boosting procedural volumes and instrument demand

- Furthermore, the expansion of private dental clinics and cosmetic dentistry centers is increasing procurement of advanced dental surgical tools, implant kits, orthodontic instruments, and restorative devices

Restraint/Challenge

High Equipment Costs and Stringent Regulatory Requirements

- The high cost of advanced dental instruments, particularly specialized surgical kits, implantology systems, and digital-compatible tools, remains a significant challenge for small and mid-sized dental practices

- For instance, premium implant surgical instrument systems and precision rotary tools require substantial capital investment, limiting adoption among newly established clinics or independent practitioners

- Strict regulatory requirements under European medical device regulations (MDR) impose rigorous quality, safety, and documentation standards on manufacturers, increasing compliance costs and extending product approval timelines

- In addition, the need for continuous training and skill development to effectively use advanced dental instruments can create operational challenges for clinics lacking adequate technical expertise

- Economic uncertainties and reimbursement limitations in certain European countries may also reduce discretionary spending on cosmetic dental procedures, indirectly affecting the procurement of specialized dental instruments

- Overcoming these challenges through cost-effective product development, regulatory compliance strategies, and training initiatives will be essential for sustained market growth across the region

Europe Dental Instruments Market Scope

The market is segmented on the basis of product, instrument type, end user, and distribution channel.

- By Product

제품 유형을 기준으로 치과 기기 시장은 치주/구강외과, 위생, 진단, 근관치료, 수술 및 기타로 세분화됩니다. 위생 부문은 예방 치과 치료 및 정기 구강 검진에 대한 전 세계적인 관심 증가에 힘입어 2025년까지 29.4%의 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. 구강 건강 및 잇몸 질환에 대한 인식이 높아짐에 따라 스케일링 및 세척 기기에 대한 수요가 크게 증가했습니다. 치과 위생사들은 일상적인 시술에서 초음파 스케일러, 큐렛, 연마 기기를 자주 사용하기 때문에 꾸준한 수요가 발생하고 있습니다. 심미 치과 및 치아 미백 시술의 성장 또한 해당 부문의 확장을 뒷받침하고 있습니다. 예방 치과 치료 프로그램을 장려하는 정부 정책 또한 위생 기기 도입을 촉진하고 있습니다. 초음파 및 에어 폴리싱 장비의 기술 발전은 효율성과 환자 편의성을 향상시켰습니다. 위생 부문은 수술 치료에 비해 시술 빈도가 높다는 장점이 있습니다. 치과 병원들은 운영 생산성 향상을 위해 첨단 위생 도구에 대한 투자를 늘리고 있습니다. 예방 서비스에 대한 치과 보험 적용 범위 확대 또한 수요를 자극하고 있습니다. 치과 관광 시장의 성장 또한 시술량 증가에 기여하고 있습니다. 지속적인 제품 혁신과 인체공학적 기기 설계는 시술자의 편안함과 효율성을 향상시킵니다. 치주 질환에 취약한 고령 인구의 증가 추세는 이러한 장점들을 더욱 강화시켜 업계 선두 자리를 굳건히 합니다.

근관치료 분야는 전 세계적으로 충치와 근관치료 시술이 증가함에 따라 2026년부터 2033년까지 연평균 8.6%의 가장 빠른 성장률을 보일 것으로 예상됩니다. 당분이 함유된 식품과 음료의 섭취 증가로 치수 감염 발생률이 높아져 시술 수요가 증가하고 있습니다. 회전식 근관치료 시스템과 니켈-티타늄 기구의 발전으로 치료 정확도가 크게 향상되고 시술 시간이 단축되었습니다. 발치보다는 치아 보존에 대한 인식이 높아지면서 환자들이 근관치료를 선택하는 경향이 커지고 있습니다. 신흥 경제국에서 치과 진료 시설 접근성이 향상됨에 따라 근관치료 분야는 더욱 성장하고 있습니다. 디지털 근관장 측정기 및 근관치료용 모터와 같은 기술 통합은 임상 결과를 개선합니다. 치과 전문의들이 최소 침습 근관치료 기법을 선호함에 따라 관련 기구의 도입이 증가하고 있습니다. 치과 병원 및 전문 진료소의 확장은 수요 증가에 기여하고 있습니다. 또한 치과 보험 환급 정책의 확대도 근관치료 분야의 성장에 긍정적인 영향을 미치고 있습니다. 고급 근관치료 기법에 대한 교육 훈련 프로그램은 의료진의 기술 습득률을 높이고 있습니다. 멸균 기준의 향상은 근관 치료용 파일 및 도구의 교체 수요를 촉진합니다. 치수 관련 질환에 취약한 고령 인구의 증가는 이러한 성장세를 더욱 가속화합니다.

- 기기 종류별

치과 기기 시장은 기기 유형을 기준으로 검진 기기, 절삭 기기 및 기타 기기로 구분됩니다. 검진 기기 부문은 일상적인 치과 진단 및 검진에서 필수적인 역할을 하기 때문에 2025년까지 34.8%의 가장 큰 시장 점유율을 차지했습니다. 구강 거울, 탐침, 프로브와 같은 기기는 거의 모든 치과 진료에서 사용되는 필수 도구입니다. 전 세계적으로 예방 치과 검진 빈도가 증가함에 따라 꾸준한 수요가 유지되고 있습니다. 구강 질환의 조기 진단에 대한 인식이 높아짐에 따라 해당 부문의 성장이 더욱 강화되고 있습니다. 진단 정확도 및 인체공학적 디자인의 기술적 발전으로 사용 편의성이 향상되었습니다. 정부 지원 구강 검진 프로그램은 공공 의료 시설 전반에 걸쳐 기기 조달을 촉진합니다. 전 세계적으로 치과 진료 네트워크가 확장됨에 따라 기기 판매량이 증가하고 있습니다. 검진 도구는 비용 효율적이면서도 필수적이므로 꾸준한 교체 주기가 필요합니다. 치과 보험 가입률 증가는 환자의 정기적인 방문을 장려합니다. 치과 교육 기관의 확대 또한 검진 키트를 대량으로 구매합니다. 심미 치과 상담의 증가는 진단 절차의 증가를 더욱 촉진합니다. 김 서림 방지 거울 및 경량 소재 분야의 지속적인 제품 혁신을 통해 효율성과 내구성이 향상됩니다.

절삭기구 부문은 치과 보철 및 외과 시술 증가에 힘입어 2026년부터 2033년까지 연평균 9.1%의 가장 빠른 성장률을 기록할 것으로 예상됩니다. 충치 및 치주 수술 건수 증가로 버, 끌, 수술용 블레이드에 대한 수요가 크게 증가하고 있습니다. 초경 및 다이아몬드 버의 기술 발전은 절삭 정밀도와 내구성을 향상시키고 있습니다. 최소 침습 치과 치료의 확산은 고성능 절삭 공구의 혁신을 촉진하고 있습니다. 전 세계적으로 치과 임플란트 시술이 증가하면서 수요가 더욱 가속화되고 있습니다. 심미 및 재건 치과 치료의 확대는 절삭기구 사용률 증가에 기여하고 있습니다. 향상된 멸균 및 감염 관리 기준은 기구 교체 빈도를 높이고 있습니다. 신흥 시장의 가처분 소득 증가는 첨단 치과 치료에 대한 접근성을 높이고 있습니다. 지속적인 연구 개발 투자는 제품 효율성을 향상시키고 진료 시간을 단축합니다. 치과 전문의들은 업무 효율 향상을 위해 내구성이 뛰어나고 빠른 속도의 기구를 점점 더 선호하고 있습니다. 외래 치과 수술 센터의 성장은 시장 확대를 뒷받침하고 있습니다. 첨단 수술 기법에 대한 교육 증가는 특수 절삭 공구의 도입을 가속화하고 있습니다.

- 최종 사용자에 의해

최종 사용자를 기준으로 치과 기기 시장은 병원, 클리닉, 치과 기공소, 과학 연구 기관 및 기타로 세분화됩니다. 클리닉 부문은 전 세계적으로 외래 치과 시술 건수가 증가함에 따라 2025년까지 41.6%의 가장 큰 시장 점유율을 차지했습니다. 개인 및 그룹 치과에서는 정기 검진, 미용 치료 및 간단한 수술을 제공합니다. 도시화가 진행됨에 따라 개인 치과 클리닉이 증가하고 있습니다. 클리닉은 환자 만족도와 서비스 효율성을 높이기 위해 첨단 기기에 투자하는 경우가 많습니다. 치과 보험 적용 범위 확대는 환자들이 클리닉 치료를 받도록 유도하고 있습니다. 치과 관광 시장의 성장은 클리닉 기반 시술을 더욱 활성화합니다. 클리닉 인프라의 기술적 업그레이드는 구매율을 높입니다. 클리닉의 유연한 예약 시스템은 환자 방문을 증가시킵니다. 프랜차이즈 기반 치과 체인의 확장은 구매력을 강화합니다. 예방 및 심미 치과 트렌드는 지속적인 수요를 뒷받침합니다. 클리닉은 일반적으로 병원에 비해 기기 교체 주기가 더 빠릅니다. 전문 치과 클리닉의 성장은 시장 지배력에 크게 기여하고 있습니다.

병원 부문은 종합병원 내 치과 부서 통합이 증가함에 따라 2026년부터 2033년까지 연평균 7.9%의 가장 빠른 성장률을 보일 것으로 예상됩니다. 복잡한 구강 수술 및 외상 환자 증가로 병원 기반 치과 시술이 늘어나고 있습니다. 병원은 고급 치과 기구를 지원하는 첨단 수술 인프라를 갖추고 있습니다. 신흥 경제국의 의료 투자 증가는 병원 확장을 촉진합니다. 치과 전문의와 의료 전문가 간의 협력 증가는 통합 치료를 지원합니다. 공공 병원에 대한 정부 지원금 증가는 조달 예산을 늘립니다. 수술적 치과 치료가 필요한 고령 인구 증가는 성장을 더욱 가속화합니다. 병원은 종종 첨단 장비가 필요한 심각한 구강 질환 사례를 치료합니다. 병원 환경에서의 기술 도입은 기구 수요를 증가시킵니다. 의료 관광의 확대 또한 치과 치료를 위한 입원 증가에 기여합니다. 수술 절차에 대한 개선된 보험금 지급 체계는 환자 유입을 촉진합니다. 의료 인프라의 지속적인 현대화는 기구 조달을 가속화합니다.

- 유통 채널별

유통 채널을 기준으로 치과 기기 시장은 직접 구매, 제3자 유통업체, 소매 판매로 구분됩니다. 제3자 유통업체 부문은 광범위한 공급망과 치과 병원 및 의원과의 탄탄한 관계를 바탕으로 2025년까지 전체 시장 매출의 46.2%를 차지하며 가장 큰 비중을 차지했습니다. 유통업체는 다양한 브랜드와 제품 포트폴리오를 하나의 채널에서 제공하며, 적시 배송과 사후 서비스 지원을 보장합니다. 대량 구매를 통해 최종 사용자에게 경쟁력 있는 가격을 제공할 수 있습니다. 신흥 지역의 치과 인프라 확장은 유통업체의 입지를 강화합니다. 유통업체는 제품 시연 및 기술 교육을 제공하기도 합니다. 잘 구축된 물류 시스템을 통해 시장 침투력을 높입니다. 소규모 병원은 안정적인 공급을 위해 유통업체에 크게 의존합니다. 유통업체가 제공하는 재고 관리 서비스는 운영 효율성을 향상시킵니다. 해외 제조업체와의 파트너십은 제품 가용성을 확대합니다. 유연한 신용 정책은 구매를 더욱 촉진합니다. 지역 유통망은 농촌 및 준도시 시장까지 폭넓게 진출할 수 있도록 합니다.

직접 입찰 부문은 정부 및 기관 조달 활동 증가에 힘입어 2026년부터 2033년까지 연평균 8.3%의 가장 빠른 성장률을 기록할 것으로 예상됩니다. 공공 병원과 대형 치과 체인은 비용 효율성을 위해 직접 계약을 선호합니다. 직접 입찰을 통해 협상 가격으로 대량 구매가 가능해 예산 최적화에 도움이 됩니다. 의료 인프라 투자 확대는 기관의 구매력을 강화합니다. 제조업체들은 시장 점유율 확대를 위해 정부 입찰 참여를 늘리고 있습니다. 투명한 조달 절차는 대규모 구매를 장려합니다. 직접 공급 계약은 중간 유통 비용을 줄이고 마진을 개선합니다. 공공 구강 건강 관리 프로그램 확대는 입찰 기반 구매를 더욱 촉진합니다. 기관 구매자들은 첨단 표준화 장비를 요구합니다. 대형 병원은 안정적인 공급을 위해 장기 공급 계약을 선호합니다. 규제 준수 요건 강화는 기존 제조업체에 유리하게 작용합니다. 보편적 의료 보장 확대는 직접 조달 수요를 더욱 증가시킬 것입니다.

유럽 치과 기기 시장 지역 분석

- 유럽 치과기기 시장은 예측 기간 동안 상당한 연평균 성장률(CAGR)을 기록하며 성장할 것으로 예상됩니다. 이러한 성장은 주로 치과 질환 유병률 증가, 심미 및 복원 시술에 대한 수요 증가, 구강 위생에 대한 인식 제고에 힘입은 것입니다.

- 유럽 여러 국가에서 공공 및 민간 치과 의료 시스템이 확대되고, 정밀하고 최소 침습적인 치과 기기 기술이 지속적으로 발전함에 따라 시장의 꾸준한 성장이 촉진되고 있습니다. 첨단 치과 시설에 대한 투자 증가와 디지털 치과 솔루션의 도입은 일반 치과, 교정, 임플란트, 근관 치료 등 다양한 분야에서 디지털 치과 기술의 활용을 더욱 확대시키고 있습니다.

- 이 지역은 병원, 개인 진료소, 전문 치과 센터 전반에 걸쳐 꾸준한 성장을 보이고 있으며, 최신 치과 기기가 새로운 진료 환경 조성과 시설 개선에 모두 도입되고 있습니다.

영국 치과 기구 시장 분석

영국 치과기기 시장은 2025년 유럽 지역에서 24.7%의 매출 점유율로 가장 큰 비중을 차지했으며, 예측 기간 동안 주목할 만한 연평균 성장률(CAGR)을 기록할 것으로 예상됩니다. 이러한 시장 지배력은 잘 구축된 공공 및 민간 치과 의료 시스템, 첨단 기술을 갖춘 치과 병원의 강력한 입지, 그리고 국민들의 높은 구강 위생 의식에 힘입은 것입니다. 예방 치과 치료, 조기 진단, 그리고 치아 미백, 교정, 임플란트와 같은 심미 치료에 대한 영국의 관심은 정밀하고 최소 침습적인 치과기기에 대한 꾸준한 수요를 견인하고 있습니다. 또한, 우호적인 의료비 지출, 체계적인 의료비 상환 시스템, 그리고 지속적인 치과 기술 발전은 영국 시장의 성장을 더욱 촉진할 것으로 기대됩니다.

독일 치과 기기 시장 분석

독일 치과기기 시장은 예측 기간 동안 유럽에서 가장 빠르게 성장하는 시장이 될 것으로 예상됩니다. 이는 보철 및 심미 치과 시술에 대한 수요 증가, 고령 인구 증가, 그리고 치과 관광의 성장에 힘입은 결과입니다. 독일은 2025년까지 유럽 지역 시장 점유율의 약 21.3%를 차지하며 유럽 시장에서 강력한 입지를 확보할 것으로 전망됩니다. 첨단 치과 기술에 대한 지속적인 투자와 잘 발달된 민간 치과 진료 부문은 혁신적인 치과기기 도입을 가속화하고 있습니다. 또한, 독일의 탄탄한 제조 기반과 고품질 의료기기 생산에 대한 집중은 기술적으로 진보되고 정밀한 치과기기 공급을 촉진하여 독일 전역의 시장 성장을 견인하고 있습니다.

유럽 치과 기기 시장 점유율

치과 기구 산업은 주로 다음과 같은 오랜 역사를 자랑하는 기업들이 주도하고 있습니다.

- 덴츠플라이 시로나(미국)

- 스트라우만 그룹(스위스)

- 다나허 코퍼레이션(미국)

- 3M 회사(미국)

- 헨리 샤인 주식회사(미국)

- 짐머 바이오메트(미국)

- 이보클라 비바덴트(리히텐슈타인)

- GC 주식회사(일본)

- Hu-Friedy Mfg. Co., LLC (미국)

- 브래슬러 USA(미국)

- VDW GmbH(독일)

- 셉토돈트 홀딩(프랑스)

- 울트라덴트 프로덕츠(미국)

- 콜틴 그룹(스위스)

- 플란메카 그룹(핀란드)

- A-dec Inc.(미국)

- 요시다 치과 제조 주식회사 (일본)

- NSK 주식회사(일본)

- 모리타 홀딩스 주식회사(일본)

- 오스템 임플란트 주식회사 (대한민국)

유럽 치과기기 시장의 최신 동향

- In March 2023, the Straumann Group unveiled a range of advanced digital implantology and orthodontic solutions at the International Dental Show (IDS) in Cologne, including the Straumann Falcon navigation system, Smilecloud design platform, and ClearCorrect mobile collaboration tools, enhancing clinical workflows and patient care across European dental practices. This launch highlighted Europe’s growing leadership in digital dentistry and adoption of integrated solutions to improve dental restoration and procedural accuracy

- In June 2024, Planmeca launched the Planmeca European Roadshow, a touring showcase of its latest dental technologies — including digital imaging systems, AI-powered Romexis software, and 3D printing solutions — visiting dental practices across multiple European countries to demonstrate cutting-edge equipment and support practitioner adoption of digital workflows. This initiative helped accelerate knowledge transfer and equipment uptake among dental professionals throughout Europe

- In June 2024, Danaher Corporation introduced a new line of ergonomically designed surgical hand instruments for dental professionals in Europe, aimed at improving comfort and efficiency during complex oral procedures and strengthening the company’s presence in high-growth markets such as Germany and France. This product launch highlighted the ongoing modernization of core dental instrument portfolios to enhance practitioner performance

- In June 2024, Dentsply Sirona also expanded its regional logistics network by establishing a dedicated distribution center in Milan, Italy, to enhance supply chain efficiency and ensure faster delivery of surgical instruments to both urban and rural dental clinics across Europe. This development demonstrated strategic investment to support market growth and timely access to essential dental instruments

- In September 2024, Mectron S.p.A. introduced a series of educational workshops across Germany and Switzerland focused on piezoelectric surgical techniques, aiming to increase awareness and adoption of its advanced piezoelectric dental instruments among specialist dental surgeons. These training campaigns supported deeper market penetration of innovative surgical tools in key European markets

- In November 2024, KaVo Dental (a division of Envista Holdings) opened a state-of-the-art surgical instrument production facility in the Netherlands, strengthening local manufacturing capabilities and enhancing supply reliability for high-quality instruments used across European dental practices. This investment underscored continued regional infrastructure growth in dental instrument production

- In March 2025, LM-Dental expanded its ergonomic hand instrument portfolio with new additions to the LM-Arte product line showcased at the IDS 2025 exhibition in Cologne, Germany, featuring the LM-Arte Replica Anterior instrument designed to simplify composite restorations in anterior dental work. This development underscored ongoing innovation in precision restorative instruments by European manufacturers to meet clinician needs for improved handling and restoration outcomes

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.