Europe Intumescent Coatings For Fireproofing And Spray Applied Fire Resistive Materials Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

637.32 Million

USD

956.06 Million

2025

2033

USD

637.32 Million

USD

956.06 Million

2025

2033

| 2026 –2033 | |

| USD 637.32 Million | |

| USD 956.06 Million | |

| % | |

|

Europe Intumescent Coatings for Fireproofing and Spray-Applied Fire-Resistive Materials Market Segmentation, By Product Type (Intumescent Coatings for Fire Proofing and Spray Applied Fire Resistive Materials), Type (Thick-Film and Thin-Film), Resin (Epoxy, Acrylic, Alkyd, Polyurethane, and Others), Substrate (Structural Cast Iron and Cast Iron, Wood, Composite Elements, and Others), Technology (Epoxy Based, Water Based, Solvent Based, and Powder Based), Application (Hydrocarbon and Cellulosic), End-User (Building and Constructions, Oil and Gas, Industrial, Automotive, Aerospace, and Others) - Industry Trends and Forecast to 2033

What is the Europe Intumescent Coatings for Fireproofing and Spray-Applied Fire-Resistive Materials Market Size and Growth Rate?

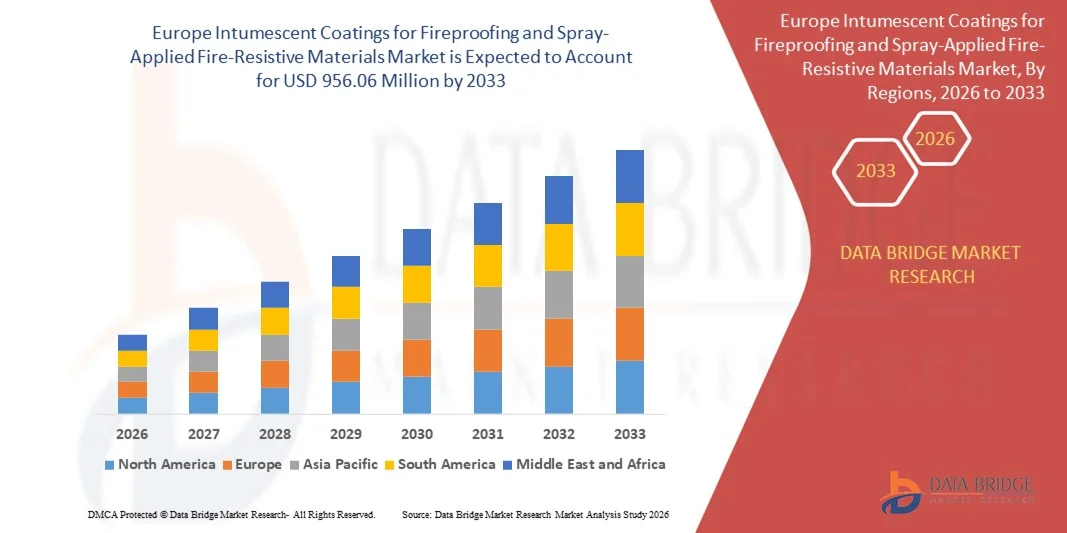

- The Europe intumescent coatings for fireproofing and spray-applied fire-resistive materials market size was valued at USD 637.32 million in 2025 and is expected to reach USD 956.06 million by 2033, at a CAGR of 5.20% during the forecast period

- The market growth is largely fueled by rising infrastructure development and stringent fire safety regulations across residential, commercial, and industrial sectors, driving the demand for passive fire protection solutions such as intumescent coatings and spray-applied fire-resistive materials

- Furthermore, increasing awareness of structural fire safety, combined with advancements in water-based and eco-friendly coating technologies, is accelerating the adoption of these materials in construction and manufacturing, thereby significantly boosting the market’s expansion

What are the Major Takeaways of Intumescent Coatings for Fireproofing and Spray-Applied Fire-Resistive Materials Market?

- Intumescent coatings and spray-applied fire-resistive materials are passive fire protection solutions applied to structural elements to enhance fire resistance by forming an insulating char layer when exposed to high temperatures, helping maintain structural integrity during fire events

- Growing implementation of fire safety codes, especially in high-rise buildings, oil & gas facilities, and public infrastructure, coupled with increasing use of steel and composite materials in construction, is propelling the demand for these coatings globally

- Germany dominated the Europe Intumescent Coatings for Fireproofing and Spray-Applied Fire-Resistive Materials market with an estimated 38.8% revenue share in 2025, driven by strong demand across automotive manufacturing, industrial machinery, building & construction, and renewable energy applications

- 프랑스는 건설 활동 증가, 인프라 개보수 프로젝트, 항공우주 및 자동차 분야, 그리고 공공 및 민간 인프라에 첨단 코팅 기술 도입이 확대됨에 따라 예측 기간 동안 7.36%의 가장 빠른 연평균 성장률(CAGR)을 기록할 것으로 예상됩니다.

- 내화성 팽창 코팅 부문은 미려한 외관, 간편한 시공, 그리고 건물의 시각적 아름다움을 해치지 않으면서 수동적인 방화 기능을 제공하는 능력 덕분에 2024년 가장 큰 시장 점유율을 차지했습니다.

보고서 범위 및 내화성 팽창 코팅과 스프레이 방식 내화 재료 시장 세분화

|

속성 |

내화성 팽창 코팅 및 스프레이 방식 내화 소재 주요 시장 분석 |

|

포함되는 부문 |

|

|

대상 국가 |

유럽

|

|

주요 시장 참여자 |

|

|

시장 기회 |

|

|

부가가치 데이터 정보세트 |

데이터 브리지 마켓 리서치에서 제공하는 시장 보고서는 시장 가치, 성장률, 시장 세분화, 지리적 범위 및 주요 업체와 같은 시장 시나리오에 대한 통찰력 외에도 심층적인 전문가 분석, 가격 분석, 브랜드 점유율 분석, 소비자 설문 조사, 인구 통계 분석, 공급망 분석, 가치 사슬 분석, 원자재/소모품 개요, 공급업체 선정 기준, PESTLE 분석, 포터 분석 및 규제 프레임워크를 포함합니다. |

내화성 팽창 코팅 및 스프레이 방식 내화 재료 시장의 주요 트렌드는 무엇입니까?

화재 안전 규제 강화

- 전 세계적으로 강화되는 화재 안전 규제는 팽창성 내화 코팅 및 스프레이형 내화 재료(SFRM) 시장 성장의 주요 원동력입니다. 고층 건물, 산업 구조물 및 공공 기반 시설에 대한 새로운 건축 법규는 첨단 수동식 화재 방호 기술의 사용을 점점 더 의무화하고 있으며, 이는 신축 및 리모델링 프로젝트 모두에서 수요를 촉진하고 있습니다.

- 예를 들어, 중국과 인도의 최근 고층 건물 화재 안전 규정과 같은 아시아 태평양 지역의 규제 체계는 이제 24m 이상의 고층 건물에 박막 팽창성 내화 코팅을 요구하며, 제3자 인증 및 규정 준수를 시장 진출의 필수 조건으로 삼고 있습니다. EU에서 저VOC(휘발성 유기 화합물) 배합 및 지속 가능성에 대한 요구가 증가하면서 기존 재료에서 현대적이고 환경 친화적인 팽창성 내화 코팅으로의 전환이 더욱 가속화되었습니다.

- 미국의 국가화재방지협회(NFPA)와 같은 화재 안전 당국은 화재 발생 건수가 지속적으로 증가하고 있음을 기록했으며, 이는 상업용, 산업용 및 주거용 건물에 대한 더욱 엄격한 화재 안전 기준과 검사 체계를 시행해야 할 필요성을 더욱 절실하게 만들고 있습니다.

- 나노 강화형, 그래핀 함유형, 수성 제형과 같은 팽창성 코팅의 발전으로 더 얇은 층으로도 더 높은 내화성을 구현할 수 있게 되어 현대 건축 설계와 변화하는 건축 규정 준수를 뒷받침하고 있습니다.

- 바이오 기반 수지 및 재활용 가능한 방화 시스템 사용을 포함한 지속가능성 목표는 환경 영향이 규제 체계 및 개발자 의사 결정의 중요한 요소가 됨에 따라 제품 혁신을 주도하고 있습니다.

- 수동형 코팅과 능동형 모니터링(IoT 센서, 스마트 코팅)을 결합한 하이브리드 솔루션이 등장하여 건물 수명 주기 전반에 걸쳐 유지 관리 및 성능 추적을 보장하고 있습니다.

내화성 팽창 코팅 및 스프레이 방식 내화 재료 시장의 주요 성장 동력은 무엇입니까?

- 전 세계적으로 산불의 빈도와 심각성이 증가함에 따라 방화 솔루션에 대한 투자가 눈에 띄게 가속화되고 있습니다. 산림-도시 경계 지역(WUI), 중요 기반 시설 및 위험 지역의 산업 시설은 자산을 보호하고 보험 및 규제 요건을 충족하기 위해 첨단 방화 소재를 우선적으로 도입하고 있습니다.

- 예를 들어, 미국 서부와 호주에서 기록적인 산불이 발생한 후, 정부와 민간 부문 모두 화재 방지 예산을 늘려 피해와 손실을 최소화하기 위해 외곽 구조물, 응급 대응 시설 및 교통 인프라에 팽창성 코팅과 방화재(SFRM)를 적용하도록 지정했습니다.

- 인공지능 기반 위험 모델링, 드론 기반 검사, 실시간 감지와 같은 기술 혁신은 고위험 지역의 방화 투자 대상을 선정하고 최적화하는 데 중요한 역할을 합니다.

- 화재 방호는 이제 신축 건물뿐 아니라 기존 건물의 개보수에도 필수적인 요건으로 인정받고 있으며, 특히 화재 발생 빈도가 높아짐에 따라 더욱 강력한 재난 복원력 및 대비 전략에 대한 필요성이 대두되고 있습니다.

- Policy incentives, stricter insurance coverage requirements, and funding for disaster mitigation are further fueling the market's expansion beyond traditional industrial sectors

Which Factor is Challenging the Growth of the Intumescent Coatings for Fireproofing and Spray-Applied Fire-Resistive Materials Market?

- Despite the advantages of intumescent coatings and SFRMs—including lighter weight, aesthetic flexibility, and superior performance for complex steel structures—traditional fireproofing materials such as cementitious sprays and mineral-fiber boards continue to pose significant competition, especially in price-sensitive and industrial-scale applications

- For instance, cementitious fireproofing is often preferred for large structural steel projects due to its lower upfront cost, ease of bulk application, and well-established regulatory acceptance—even though it can be bulky and may compromise space or design elegance

- Intumescent coatings typically require more specialized application techniques and can carry higher initial costs, which can deter adoption among budget-constrained projects or regions with less rigorous fire safety codes

- The established supply chains, contractor familiarity, and legacy specifications tied to traditional products make it challenging for newer formulations to gain rapid acceptance in conservative construction markets

- In some industrial and commercial settings, maintenance and environmental exposure concerns (such as humidity or impact damage) may tip the scales in favor of older, more robust—if less elegant—fireproofing solutions, despite innovation in intumescent technology. Addressing price sensitivity and improving awareness of lifecycle benefits remain key for advancing intumescent and spray-applied material adoption over legacy alternatives

How is the Intumescent Coatings for Fireproofing and Spray-Applied Fire-Resistive Materials Market Segmented?

The market is segmented on the basis of product type, type, resin, substrate, technology, application, and end-user.

- By Product Type

On the basis of product type, the market is segmented into intumescent coatings for fireproofing and spray-applied fire-resistive materials. The intumescent coatings for fireproofing segment accounted for the largest market share in 2024 due to its superior aesthetics, ease of application, and ability to provide passive fire protection without compromising the visual appearance of structures. Widely preferred in commercial and high-rise buildings, these coatings expand under heat to form a char layer that insulates the underlying material, thereby delaying structural collapse during a fire. Their growing use in steel-framed constructions and increasing regulatory compliance regarding fire safety standards are driving segment dominance.

The spray-applied fire-resistive materials (SFRM) segment is projected to witness the fastest growth from 2025 to 2032, spurred by its cost-effectiveness and extensive application in industrial and large-scale infrastructure projects. SFRMs are preferred for their quick installation and strong thermal insulation properties, especially in settings where fire protection must cover complex geometries or wide surface areas. Their growing use in retrofitting older buildings and in oil & gas facilities enhances their growth outlook.

- By Type

On the basis of type, the market is segmented into thick-film and thin-film coatings. The thick-film segment led the market with the highest revenue share in 2024, driven by its widespread application in hydrocarbon fire protection, particularly in high-risk environments such as petrochemical and energy plants. Thick-film coatings offer higher durability, superior thermal insulation, and longer fire-resistance duration, making them a critical choice for heavy-duty infrastructure.

The thin-film segment is expected to exhibit the fastest growth from 2025 to 2032, primarily due to its rising adoption in architectural applications where aesthetics are paramount. Thin-film coatings are favored in commercial buildings and offices for their smooth finish, low weight, and reliable performance under cellulosic fire conditions. Their compatibility with decorative topcoats and lower application thickness contribute to their growing preference among architects and contractors.

- By Resin

On the basis of resin type, the market is segmented into epoxy, acrylic, alkyd, polyurethane, and others. The epoxy segment held the largest market share of 59% in 2024 owing to its exceptional adhesion, corrosion resistance, and mechanical strength. Epoxy-based fireproof coatings are extensively used in oil & gas, marine, and industrial sectors where durability and chemical resistance are crucial. Their ability to perform under extreme environmental conditions supports their leadership in high-risk installations.

The acrylic segment is anticipated to grow at the highest CAGR from 2025 to 2032, fueled by demand for water-based, low-VOC coatings in green building projects. Acrylic resins offer rapid drying, cost-effectiveness, and environmental compliance, making them ideal for residential and light-commercial fireproofing applications. Their increasing use in thin-film systems and decorative coatings further boosts segment growth.

- By Substrate

On the basis of substrate, the market is segmented into structural cast iron and cast iron, wood, composite elements, and others. Structural cast iron and cast iron dominated the market in 2024, supported by their widespread use in large-scale steel frameworks and the urgent need for fire protection in such load-bearing components. The strong thermal conductivity of metal substrates necessitates advanced fire-resistive coatings to maintain structural integrity in fire scenarios.

The wood segment is expected to register the fastest growth rate from 2025 to 2032, driven by increasing applications in modular construction, residential buildings, and interior design. As wooden structures become more prominent in sustainable architecture, the need for fire retardant solutions that preserve aesthetics while ensuring safety is driving demand for specialized intumescent coatings compatible with wood.

- By Technology

On the basis of technology, the market is divided into epoxy-based, water-based, solvent-based, and powder-based. Epoxy-based coatings dominated the market in 2024 due to their exceptional performance in offshore and oil & gas applications. These coatings resist moisture, chemicals, and mechanical stress, making them ideal for harsh environments where fire hazards are combined with corrosive exposure.

Water-based coatings are projected to witness the highest growth from 2025 to 2032, supported by environmental regulations and the push for low-VOC and non-toxic fireproofing materials. Their user-friendly application, fast drying times, and minimal odor make them increasingly suitable for occupied buildings, schools, and healthcare settings.

- By Application

On the basis of application, the market is segmented into hydrocarbon and cellulosic fire protection. Hydrocarbon fire protection led the market in 2024 due to stringent safety norms in oil & gas, chemical processing, and offshore industries where high-temperature fires caused by fuel combustion pose severe structural risks. Coatings used in these applications are designed to withstand rapid temperature rise and maintain integrity under explosive conditions.

Cellulosic fire protection is anticipated to grow fastest over the forecast period as it finds rising usage in commercial and residential buildings. These fires, driven by wood, paper, and furniture, require effective and visually acceptable fireproofing solutions, making intumescent coatings a favorable choice for architects and developers.

- By End-User

On the basis of end-user, the market is segmented into building and constructions, oil and gas, industrial, automotive, aerospace, and others. The building and construction segment dominated the market in 2024, underpinned by expanding urban infrastructure, increasing focus on occupant safety, and rising adoption of fire safety codes across developed and developing regions. Fireproofing of steel and wooden structures in high-rise residential and commercial projects continues to propel demand.

The oil and gas segment is forecasted to experience the highest growth from 2025 to 2032, driven by heightened safety regulations, ongoing investments in refining and exploration, and the critical need to prevent catastrophic damage during fire incidents. Fire-resistive coatings in these settings protect lives and also ensure the continuity of operations in high-risk environments.

Which Region Holds the Largest Share of the Intumescent Coatings for Fireproofing and Spray-Applied Fire-Resistive Materials Market?

- Germany dominated the Europe Intumescent Coatings for Fireproofing and Spray-Applied Fire-Resistive Materials market with an estimated 38.8% revenue share in 2025, driven by strong demand across automotive manufacturing, industrial machinery, building & construction, and renewable energy applications

- Increasing focus on surface protection against corrosion, moisture, dust accumulation, and chemical exposure is significantly supporting market growth. Presence of advanced manufacturing hubs, strong R&D capabilities, and continuous investments in material science and surface engineering technologies are further accelerating adoption

- Emphasis on extending asset lifespan, reducing maintenance costs, improving energy efficiency, and meeting stringent environmental standards continues to drive market demand across Germany

France Intumescent Coatings for Fireproofing and Spray-Applied Fire-Resistive Materials Market Insight

France is projected to register the fastest CAGR of 7.36% during the forecast period, driven by rising construction activities, infrastructure renovation projects, aerospace and automotive applications, and growing adoption of advanced coatings in public and private infrastructure. Government initiatives supporting sustainable materials and smart infrastructure further enhance market growth.

Italy Intumescent Coatings for Fireproofing and Spray-Applied Fire-Resistive Materials Market Insight

Italy is witnessing steady growth, supported by demand from building restoration, automotive components, industrial equipment, and consumer goods manufacturing. Focus on surface durability, aesthetic preservation, and high-performance coating solutions is driving consistent adoption across the country.

Which are the Top Companies in Intumescent Coatings for Fireproofing and Spray-Applied Fire-Resistive Materials Market?

The Intumescent Coatings for Fireproofing and Spray-Applied Fire-Resistive Materials industry is primarily led by well-established companies, including:

- P2i Ltd. (U.K.)

- NEI Corporation (U.S.)

- UltraTech International Inc. (U.S.)

- Aculon Inc. (U.S.)

- Lotus Leaf Coatings, Inc. (U.S.)

- Rust-Oleum (U.S.)

- Cytonix (U.S.)

- NASIOL NANO COATINGS (Turkey)

- The President and Fellows of Harvard College (U.S.)

- LiquiGlide Inc. (U.S.)

- Surfactis Technologies (France)

- PearlNano (U.S.)

- Henkel AG & Co. KGaA (Germany)

- Keronite (U.K.)

- Nanoshel LLC (U.S.)

- Nanorh (U.S.)

What are the Recent Developments in Europe Intumescent Coatings for Fireproofing and Spray-Applied Fire-Resistive Materials market?

- In June 2025, Huntsman introduced the POLYRESYST EV5005 polyurethane-based intumescent coating system, designed specifically for automotive applications. This innovation addresses a critical fire safety challenge in electric vehicles by enhancing passive fire protection for metal and composite battery components without compromising design flexibility. The launch is expected to expand the application of intumescent coatings in the automotive sector, particularly in EV battery safety, reinforcing market growth in transportation-related fireproofing solutions

- In June 2023, Jotun expanded its Global Intumescent R&D Laboratory to boost product innovation and technology advancement. This expansion aims to enhance product development and fire testing capacity, accelerating the creation of innovations and advanced products. In addition, it provides certification support for Jotun's existing product range, strengthening its position in the intumescent coatings market

- In January 2022, PPG Industries unveiled the PPG AMERCOAT range of passive fire protection coatings tailored for steel structures. As water-based intumescent solutions, these coatings contribute to enhanced safety standards while aligning with growing environmental and regulatory expectations. The launch reinforced PPG’s role in supporting industrial and infrastructure fire safety, further advancing market adoption of sustainable fire-resistive materials

- In May 2020, Sherwin-Williams introduced Firetex M90/03, an intumescent coating capable of providing up to 90 minutes of fire resistance for both onsite and offsite applications. The product's adaptability to different construction environments supports the growing trend of modular and prefabricated building practices. This innovation helped broaden the use of fire-resistive coatings in versatile construction settings, supporting market expansion across both traditional and modern construction methods

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.