Europe Orthopedic Surgical Robots Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

2.24 Billion

USD

13.18 Billion

2025

2033

USD

2.24 Billion

USD

13.18 Billion

2025

2033

| 2026 –2033 | |

| USD 2.24 Billion | |

| USD 13.18 Billion | |

| % | |

Europe Orthopedic Surgical Robots Market, By Product Type (Robotic System, Robotic Accessories, and Software and Services), End User (Hospital and Ambulatory Surgery Centers (ASCS)), Distribution Channel (Direct Tenders and Third Party Distributors) - Industry Trends and Forecast to 2029.

Europe Orthopedic Surgical Robots Market Analysis and Insight

The orthopedic surgical robots market is largely influenced by the surging focus of key players towards technological advances in molecular diagnostics and indulging towards collaboration and partnerships with other organizations. The first documented use of orthopedic surgery had started during the 15th century. Modern orthopedic surgery and musculoskeletal research makes surgery less invasive and to make implanted components better and more durable. The orthopedic surgical robots are used to correct the bone deformities and to restore the function of the human skeletal system. During the last few years, new innovative orthopedic surgical robots products have been developed for increasing the growth of orthopedic surgical robots market, and the market players are enhancing their product portfolio. Many market players are involved in the manufacturing of orthopedic surgical robots with innovations that pave the way for market growth.

Europe orthopedic surgical robots market report provides details of market share, new developments, and product pipeline analysis, impact of domestic and localized market players, analyses opportunities in terms of emerging revenue pockets, changes in market regulations, product approvals, strategic decisions, product launches, geographic expansions, and technological innovations in the market. To understand the analysis and the market scenario contact us for an analyst brief, our team will help you create a revenue impact solution to achieve your desired goal.

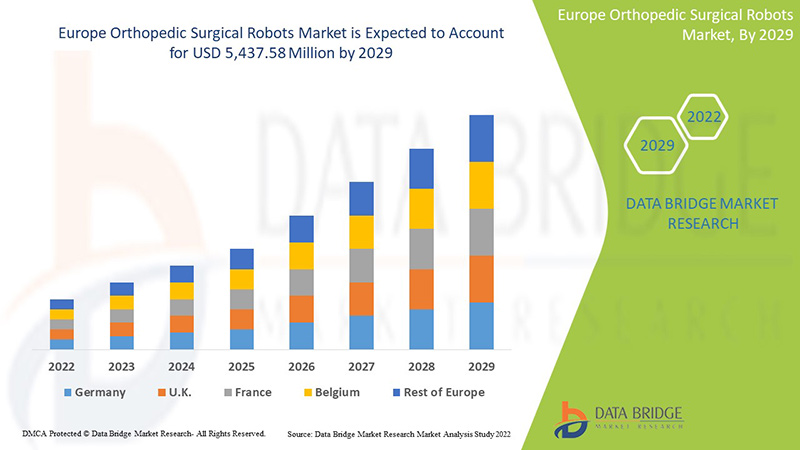

Data Bridge Market Research analyses that the orthopedic surgical robots market is expected to reach the value of USD 5,437.58 million by 2029, at a CAGR of 24.8% during the forecast period 2022-2029.

|

Report Metric |

Details |

|

Forecast Period |

2022 to 2029 |

|

Base Year |

2021 |

|

Historic Year |

2020 (Customizable to 2019-2014) |

|

Quantitative Units |

Revenue in USD Million, Pricing in USD |

|

Segments Covered |

By Product Type (Robotic System, Robotic Accessories, and Software and Services), End User (Hospital and Ambulatory Surgery Centers (ASCS)), Distribution Channel (Direct Tenders and Third Party Distributors) |

|

Countries Covered |

U.K., Germany, France, Spain, Italy, Netherlands, Switzerland, Russia, Belgium, Turkey, Rest of Europe in Europe. |

|

Market Players Covered |

Johnson & Johnson Services, Inc., Stryker, Zimmer Biomet, Smith & Nephew, Corin Group, NuVasive, Inc., Brainlab AG, Integrity Implants Inc. d/b/a/ Accelus, Beijing Tinavi Medical Technologies Co., Ltd, Medtronic, Globus Medical, Inc., Accuray Incorporated, THINK Surgical, Inc., CUREXO, INC. are among others. |

Market Definition

The orthopedic surgical robots are used to correct the bone deformities and to restore the function of the human skeletal system. It uses energy such as radiation, radio frequency, and ultrasound to seal the skin and bone tissue. The orthopedic surgical robots require an energy source, such as an electro surgery generator (ESU), and an instrument to transfer the energy to the patient. The important types include radio frequency (RF), modified electrical current, and ultrasound, which converts electrical current into mechanical motion. More specialized technologies include those that use argon gas, plasma, or a combination of technologies. The technological advancements used in the orthopedic surgical robots are ultrasound, radiofrequency, and radiation. The diagnostic technology used in the orthopedic surgical robots have permitted orthopedic surgeons to achieve new levels of precision and safety. It provides a surgeon to diagnose, plan, and expedite the orthopedic surgery for outstanding results.

Orthopedic Surgical Robots Market Dynamics

This section deals with understanding the market drivers, advantages, opportunities, restraints and challenges. All of this is discussed in detail as below:

DRIVERS

-

RISING PREVALENCE OF OSTEOPOROSIS

Osteoporosis is a chronic disease that suppresses the bones. If an individual has osteoporosis, he will be at a greater risk for sudden and unexpected bone fractures. In 2021, the World Health Organization (WHO) data stated that about 200 million people are predicted to have osteoporosis.

Though osteoporosis affects males and females, females are likely to develop more osteoporosis than men. For the treatment of osteoporosis, hip fractures and knee replacements are there, and it is important to understand the previous physical health conditions of elderly patients, such as reduced bone mass and bone fragility. The regularity of osteoporosis is increasing, so the surgical approach for osteoporosis is rising. The reamer-irrigator aspirator is a type of hand piece which are used among orthopedic surgeons. For example, the high torq power tool is a reamer used to treat osteoporosis.

With the rising prevalence of osteoporosis globally, the demand for early diagnosis of the disease is also increasing, with which the demand for care, services, and technologies is rising to treat chronic conditions in old age.

-

INCREASE IN NUMBER OF ORTHOPEDIC SURGERIES

The increase in the geriatric population and orthopedic disorders such as osteoporosis. Due to the increase in orthopedic disorders, the number of orthopedic-related surgeries is also increasing. The increased number of orthopedic surgeries would increase the number of orthopedic surgeons. This would increase the use of orthopedic surgical robots. It would increase the production and supply of orthopedic surgical robots.

Surgical robots are already transforming the healthcare market. As they capture a growing volume of surgical procedures, outpatient centers will force down prices on medtech devices and trigger changes for payers and providers. Hence, an increase in the number of orthopedic surgeries is expected to drive the growth of the orthopedic surgical robots market.

RESTRAINTS

- LACK OF AWARENESS ABOUT ORTHOPEDIC SURGERIES

Although orthopedic surgical energy devices have positioned themselves as a platform in the market of non-invasive devices, the non-existence of orthopedic surgeries is present in developing countries. This would result in delay and diagnosis of the orthopedic disease and the orthopedic surgical robots having a lower market position. The lack of awareness and self-efficacy also adds to the potential barriers and imperfect implementation.

-

RISKS OBSERVED IN ORTHOPEDIC SURGERIES

Orthopedic surgical are performed by orthopedics to cure orthopedic disorders, blood vessels, cut tissue, and stop bleeding. They are hand-held devices, so they must be operated as part of the doctor's instrument. Although they do not offer a diagnosis, they deliver medications that enable better treatment. However, there are certain risks observed while using orthopedic surgeries.

However, the variety of risks and health complications associated with orthopedic surgery and the need for further surgical intervention to fix some of them are expected to hamper its demand in the market. Thus, the health complications associated with orthopedic surgeries are expected to restrain the orthopedic surgical robots market.

OPPORTUNITIES

-

INCREASE IN GERIATRIC POPULATIONS

Knee disorders are common in the elderly population globally. Adults aged 60 years and above, particularly those living in long-term care facilities, are likely to suffer from chronic knee symptoms. As aging increases, the burden of knee disorders in the geriatric population may increase, which paves the way for the development of medications and implants in diagnostic and prevention strategies critical for improving the knee disorders of older adults.

As age increases, the susceptibility to knee disorders and other risk factors also increases. For some individuals, it may be hereditary, while for others, knee osteoarthritis can result from injury, infection, or even from being overweight. The increase in the geriatric population is expected to propel the market growth as it leads to greater use of robots in numerous surgeries. These robots were introduced to address the needs of geriatric people, including physical and medical care. Additionally, the senior population is greatly affected by chronic diseases can be a factor in the growth of the orthopedic surgical robots market.

-

RISING HEALTHCARE EXPENDITURE

The expense of money used by a country on its healthcare and its growth rate over time is inclined by a wide variety of economic and social factors, including the financing arrangements and structure of the organization for the health system. In particular, there is a strong association between the whole income level of a country and how much the country's population spends on health care.

Healthcare expenditure has increased across developed, and emerging countries as the disposable income of people are growing. The more money is spent on healthcare the healthier a country's population is. Moreover, to accomplish the population requirements, government bodies and healthcare organizations in different regions are taking the initiative to accelerate healthcare expenditure. Therefore, the rise in healthcare expenditure simultaneously helps healthcare organizations and government bodies to increase healthcare management services in various aspects.

CHALLENGES

-

LACK OF SKILLED PROFESSIONALS

The lack or shortage of skilled expertise would challenge the pace of recovery and growth in one place. Often, the unemployed people in one place have skills in short supply elsewhere. Moreover, rapid technological advancement in this field also leads to a lack of expertise. Despite the call to increase, the number of podiatrists and some residency training programs remains unknown.

Even as the revalidation process for orthopedic surgeons began in Switzerland, the United Kingdom, and other countries, some orthopedic and medical professionals elsewhere in Europe have not started to address the issue of CME and related requirements. As skill demands are too high, retaining and managing skill-specified professionals has become a challenge. Moreover, technological advancement is another aspect that leads to the increased demand for skilled professionals. Podiatrists report significant unmet supportive care needs and barriers in their centers, with only a small minority rating themselves as competently providing supportive care. There is an urgent need for the requirement of podiatrists and professionals to treat chronic knee disorders and procure available supportive care resources. Lack of trained and experienced professionals and persistent skill gaps limit the employability prospects and access to quality jobs. Therefore, this signifies that the lack of skilled professionals is a challenge to the growth of the orthopedic surgical robots market.

-

STRICT REGULATORY FRAMEWORKS

Regulation of medical devices plays a significant role in healthcare. Achieving the requisite approval for legal selling medical devices in such jurisdictions can entail significant financial expenditure, which could take months or years to complete. If these constraints are not understood or considered, delays can seriously jeopardize the likelihood of success in a highly competitive market. Medical robots are increasingly used in minimally invasive surgeries; assistive surgeries are important for treating various diseases. But their approval and marketing in various regions across different regions require a meeting of stringent regulatory standards and approvals by various regulatory bodies.

Post COVID-19 Impact on Orthopedic Surgical Robots Market

COVID-19 created a major impact on the orthopedic surgical robots market as almost every country has opted for the shutdown for every production facility except the ones dealing in producing the essential goods. The government has taken some strict actions such as the shutdown of production and sale of non-essential goods, blocked international trade, and many more to prevent the spread of COVID-19. The only business which is dealing in this pandemic situation is the essential services that are allowed to open and run the processes.

The growth of the Europe orthopedic surgical robots market is increasing prevalence of osteoporosis this sector has increased the demand because it targets patient who has the bone related disease. Other reasons driving the demand for these procedures are increasing aging people and rising requirement of healthcare facilities which can further result in decrease in burden on healthcare facilities. Hence, rise in demand for surgical robots procedure is estimated over the forecast period. However, factors such as inadequate availability of raw material to meet orthopedic surgical robots product production demand are restraining the market growth. The shutdown of production facilities during the pandemic situation has had a significant impact on the market.

Recent Developments

- In February 2022, Stryker completes the acquisition of Vocera Communications. This acquisition provides significant opportunities to advance innovations and accelerate our digital aspirations. Vocera brings a highly complementary and innovative portfolio to Stryker’s Medical division that will enhance the company’s Advanced Digital Healthcare offerings and further advance Stryker’s focus on preventing adverse events throughout the continuum of care.

- In March 2022, Corin Group has announced that the company is partnering with Efferent Health, LLC, a leader in medical operations automation technology, delivering innovative solutions that streamline key processes. This results in strengthening the portfolio of interoperability data services as well as expanding the company’s credibility in the market.

Europe Orthopedic Surgical Robots Market Scope

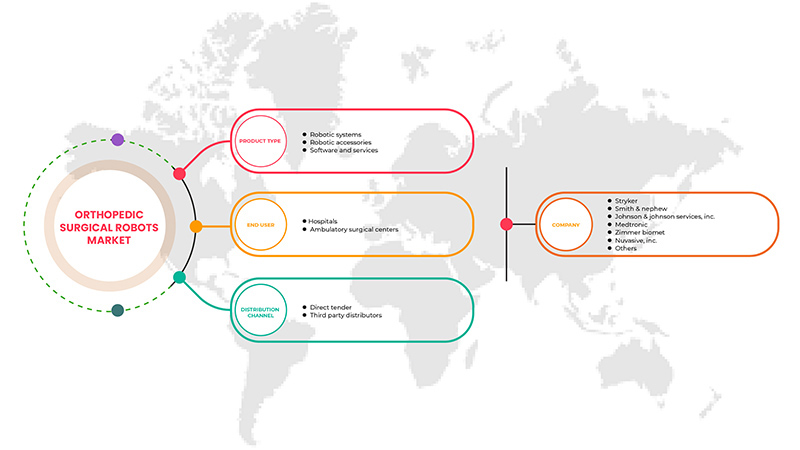

Europe orthopedic surgical robots market is segmented on the basis of product type, end user, and distribution channel. The growth amongst these segments will help you analyze major growth segments in the industries and provide the users with a valuable market overview and market insights to help them make strategic decisions for identifying core market applications.

By Product Type

- Robotic System

- Robotic Accessories

- Software and Services

On the basis of product type, the Europe orthopedic surgical robots market is segmented into robotic system, robotic accessories, and software and services.

By End User

- Hospitals

- Ambulatory Surgical Centers

On the basis of by end user, the Europe orthopedic surgical robots market has been segmented into hospitals, and ambulatory surgical centers.

By Distribution Channel

- Direct Tender

- Third Party Distributors

On the basis of by distribution channel, the Europe orthopedic surgical robots market has been segmented into direct tender, and third party distributors.

Orthopedic Surgical Robots Market Regional Analysis/Insights

The orthopedic surgical robots market is analyzed and market size insights and trends are provided by country, product type, end user, and distribution channel as referenced above.

The countries covered in the Europe orthopedic surgical robots market report are U.K., Germany, France, Spain, Italy, Netherlands, Switzerland, Russia, Belgium, Turkey, Rest of Europe in Europe.

Germany dominates the Europe orthopedic surgical robots market due to increasing technology and reliability of orthopedic surgical robots.

The country section of the report also provides individual market impacting factors and changes in market regulation that impact the current and future trends of the market. Data points like down-stream and upstream value chain analysis, technical trends and porter's five forces analysis, case studies are some of the pointers used to forecast the market scenario for individual countries. Also, the presence and availability of Europe brands and their challenges faced due to large or scarce competition from local and domestic brands, impact of domestic tariffs and trade routes are considered while providing forecast analysis of the country data.

Competitive Landscape and Orthopedic Surgical Robots Market Share Analysis

The orthopedic surgical robots market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, regional presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus on the orthopedic surgical robots market.

Some of the major players operating in the orthopedic surgical robots market are Johnson & Johnson Services, Inc., Stryker, Zimmer Biomet, Smith & Nephew, Corin Group, NuVasive, Inc., Brainlab AG, Integrity Implants Inc. d/b/a/ Accelus, Beijing Tinavi Medical Technologies Co., Ltd, Medtronic, Globus Medical, Inc., Accuray Incorporated, THINK Surgical, Inc., CUREXO, INC. are among others.

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

목차

1 서론

1.1 연구 목적

1.2 시장 정의

1.3 유럽 정형외과 수술 로봇 시장 개요

1.4 통화 및 가격

1.5 제한 사항

1.6 대상 시장

2 시장 세분화

2.1 대상 시장

2.2 지리적 범위

연구에 2.3년이 고려됨

2.4 통화 및 가격

2.5 DBMR TRIPOD 데이터 검증 모델

2.6 다변량 모델링

2.7 제품 수명 곡선

2.8 주요 여론 선도자와의 1차 인터뷰

2.9 DBMR 시장 위치 그리드

2.1 시장 적용 범위 그리드

2.11 공급업체 점유율 분석

2.12 2차 소스

2.13 가정

3 요약

4가지 프리미엄 인사이트

4.1 페스텔

4.2 포터의 5가지 힘

4.3 유럽의 정형외과 수술 로봇에 대한 임상 시험

4.4 전략적 이니셔티브

4.4.1 인구 통계적 추세

4.4.2 주요 특허 등록 전략

4.5 유럽 정형외과 수술 로봇 시장, 규제 프레임워크

5 시장 개요

5.1 드라이버

5.1.1 골다공증 유병률 증가

5.1.2 로봇 시스템의 기술적 진보 증가

5.1.3 정형외과 수술 건수 증가

5.1.4 스포츠 및 외상 부상 발생률 증가

5.2 제약

5.2.1 정형외과 수술에 대한 인식 부족

5.2.2 정형외과 수술에서 관찰되는 위험

5.2.3 정형외과 수술과 관련된 높은 비용

5.3 기회

5.3.1 노인 인구의 증가

5.3.2 증가하는 의료비 지출

5.3.3 파손 발생률 증가

5.4 과제

5.4.1 숙련된 전문가의 부족

5.4.2 엄격한 규제 프레임워크

6 유럽 정형외과 수술 로봇 시장, 제품 유형별

6.1 개요

6.2 로봇 시스템

6.2.1 무릎

6.2.1.1 수술 유형

6.2.1.1.1 총 무릎 관절 성형술

6.2.1.1.2 단일 구획 무릎 관절 성형술

6.2.1.1.3 전방십자인대 재건술

6.2.1.1.4 기타

6.2.1.1.5 로봇 유형

6.2.1.1.6 마코

6.2.1.1.7 코리

6.2.1.1.8 네비게이션

6.2.1.1.9 티로봇

6.2.1.1.10 T솔루션 1

6.2.1.1.11 기타

6.2.2 고관절

6.2.2.1 수술 유형

6.2.2.1.1 전체 고관절 인공관절수술

6.2.2.1.2 기타

6.2.2.1.3 로봇 유형

6.2.2.1.4 마코

6.2.2.1.5 T솔루션 1

6.2.2.1.6 기타

6.2.3 척추

6.2.3.1 수술 유형

6.2.3.1.1 척추 나사 이식

6.2.3.1.2 척추 증강술

6.2.3.1.3 복강경 전방 요추 척추간 융합술

6.2.3.1.4 척추 종양 절제 수술

6.2.3.1.5 수술 중 현지화

6.2.3.1.6 전방 요추 추간 융합술

6.2.3.1.7 기타

6.2.3.1.8 로봇 유형

6.2.3.1.9 마조르

6.2.3.1.9.1 르네상스

6.2.3.1.9.2 마조르 엑스

6.2.3.1.9.3 척추 보조

6.2.3.1.10 로사

6.2.3.1.11 CIRQ

6.2.3.1.12 엑셀시우스 GPS

6.2.3.1.13 기타

6.2.4 대퇴골

6.2.4.1 수술 유형

6.2.4.1.1 대퇴경부 캐뉼라 나사 배치

6.2.4.1.2 골수내 손톱 고정

6.2.4.1.3 대퇴골두의 핵심 감압

6.2.4.1.4 기타

6.2.4.1.5 로봇 유형

6.2.4.1.6 티로봇

6.2.4.1.7 기타

6.2.5 골반

6.2.5.1 수술 유형

6.2.5.1.1 대퇴경부 캐뉼라 나사 배치

6.2.5.1.2 골수내 손톱 고정

6.2.5.1.3 대퇴골두의 핵심 감압

6.2.5.1.4 기타

6.2.5.1.5 로봇 유형

6.2.5.1.6 티로봇

6.2.5.1.7 기타

6.2.6 손

6.2.6.1 수술 유형

6.2.6.1.1 대퇴경부 캐뉼라 나사 배치

6.2.6.1.2 골수내 손톱 고정

6.2.6.1.3 대퇴골두의 핵심 감압

6.2.6.1.4 기타

6.2.6.1.5 로봇 유형

6.2.6.1.6 티로봇

6.2.6.1.7 기타

6.2.7 팔꿈치

6.2.7.1 수술 유형

6.2.7.1.1 대퇴경부 캐뉼라 나사 배치

6.2.7.1.2 골수내 손톱 고정

6.2.7.1.3 대퇴골두의 핵심 감압

6.2.7.1.4 기타

6.2.7.1.5 로봇 유형

6.2.7.1.6 티로봇

6.2.7.1.7 기타

6.2.8 기타

6.3 로봇 액세서리

6.4 소프트웨어 및 서비스

7 유럽 정형외과 수술 로봇 시장, 최종 사용자별

7.1 개요

7.2 병원

7.2.1 ACTUE CARE 병원

7.2.2 장기요양병원

7.2.3 간호 시설

7.2.4 재활 센터

7.3 외래 수술 센터

8 유럽 정형외과 수술 로봇 시장, 유통 채널별

8.1 개요

8.2 직접 입찰

8.3 제3자 유통업체

9 유럽 정형외과 수술 로봇 시장, 지역별

9.1 유럽

9.1.1 독일

9.1.2 프랑스

9.1.3 영국

9.1.4 이탈리아

9.1.5 스페인

9.1.6 러시아

9.1.7 네덜란드

9.1.8 스위스

9.1.9 터키

9.1.10 벨기에

9.1.11 유럽의 나머지 지역

10 유럽 정형외과 수술 로봇 시장: 회사 환경

10.1 회사 점유율 분석: 유럽

11 SWOT 분석

12 회사 프로필

12.1 스트라이커

12.1.1 회사 스냅샷

12.1.2 수익 분석

12.1.3 회사 점유율 분석

12.1.4 제품 포트폴리오

12.1.5 최근 개발 사항

12.2 스미스 앤 네퓨

12.2.1 회사 스냅샷

12.2.2 수익 분석

12.2.3 회사 점유율 분석

12.2.4 제품 포트폴리오

12.2.5 최근 개발 사항

12.3 존슨앤존슨서비스 주식회사

12.3.1 회사 스냅샷

12.3.2 수익 분석

12.3.3 회사 점유율 분석

12.3.4 제품 포트폴리오

12.3.5 최근 개발 사항

12.4 메드트로닉

12.4.1 회사 스냅샷

12.4.2 수익 분석

12.4.3 회사 점유율 분석

12.4.4 제품 포트폴리오

12.4.5 최근 개발

12.5 짐머 바이오멧

12.5.1 회사 스냅샷

12.5.2 수익 분석

12.5.3 회사 점유율 분석

12.5.4 제품 포트폴리오

12.5.5 최근 개발 사항

12.6 ACCURAY 주식회사

12.6.1 회사 스냅샷

12.6.2 수익 분석

12.6.3 제품 포트폴리오

12.6.4 최근 개발

12.7 베이징 티나비 의료기술 유한회사

12.7.1 회사 스냅샷

12.7.2 제품 포트폴리오

12.7.3 최근 개발

12.8 브레인랩 AG

12.8.1 회사 스냅샷

12.8.2 제품 포트폴리오

12.8.3 최근 개발 사항

12.9 코린 그룹

12.9.1 회사 스냅샷

12.9.2 제품 포트폴리오

12.9.3 최근 개발

12.1 (주)큐렉소

12.10.1 회사 스냅샷

12.10.2 제품 포트폴리오

12.10.3 최근 개발 사항

12.11 글로버스 메디컬 주식회사

12.11.1 회사 스냅샷

12.11.2 수익 분석

12.11.3 제품 포트폴리오

12.11.4 최근 개발 사항

12.12 INTEGRITY IMPLANTS INC. D/B/A/ ACCELUS

12.12.1 회사 스냅샷

12.12.2 제품 포트폴리오

12.12.3 최근 개발

12.13 누바시브 주식회사

12.13.1 회사 스냅샷

12.13.2 수익 분석

12.13.3 제품 포트폴리오

12.13.4 최근 개발

12.14 씽크서지컬 주식회사

12.14.1 회사 스냅샷

12.14.2 제품 포트폴리오

12.14.3 최근 개발 사항

13 설문지

14 관련 보고서

표 목록

표 1 유럽 정형외과 수술 로봇 시장, 제품 유형별, 2021-2029년(백만 달러)

표 2 유럽 정형외과 수술 로봇 시장, 지역별, 2021-2029년(백만 달러)

표 3 유럽 정형외과 수술 로봇 시장 유형별 로봇 시스템, 2020-2029년(백만 달러)

표 4 유럽 무릎 정형외과 수술 로봇 시장, 수술 유형별, 2020-2029년(백만 달러)

표 5 유럽 무릎 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029년(백만 달러)

표 6 유럽 무릎 정형외과 수술 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 7 수술 유형별 유럽 고관절 수술 로봇 시장, 2020-2029년(백만 달러)

표 8 유럽 고관절 수술 로봇 시장, 로봇 유형별, 2020-2029년(백만 달러)

표 9 유럽 고관절 정형외과 수술 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 10 유럽 척추 정형외과 수술 로봇 시장, 수술 유형별, 2020-2029년(백만 달러)

표 11 유럽 척추 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029년(백만 달러)

표 12 유럽 척추 정형외과 수술 로봇 시장, 로봇 유형별, 볼륨, 2020-2029 볼륨, (단위)

표 13 수술 유형별 유럽 정형외과 수술 로봇 시장 주요 규모, 2020-2029년(백만 달러)

표 14 유럽 정형외과 수술 로봇 시장 주요 규모, 로봇 유형별, 규모, 2020-2029(단위)

표 15 유럽 대퇴골 정형외과 수술 로봇 시장, 수술 유형별, 2020-2029년(백만 달러)

표 16 유럽 대퇴골 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029년(백만 달러)

표 17 유럽 대퇴부 정형외과 수술 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 18 유럽 골반 수술 로봇 시장, 수술 유형별, 2020-2029년(백만 달러)

표 19 유럽 골반 수술 로봇 시장, 로봇 유형별, 2020-2029년(백만 달러)

표 20 유럽 골반 정형외과 수술 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 21 수술 유형별 정형외과 수술 로봇 시장에서 유럽의 영향력, 2020-2029년(백만 달러)

표 22 로봇 유형별 정형외과 수술 로봇 시장에서 유럽의 영향력, 2020-2029년(백만 달러)

표 23 유럽의 정형외과 수술 로봇 시장 점유율, 로봇 유형별, 양, 2020-2029(단위)

표 24 유럽 정형외과 수술 로봇 시장, 수술 유형별, 2020-2029년(백만 달러)

표 25 유럽 엘보우 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029년(백만 달러)

표 26 유럽 정형외과 수술용 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 27 유럽 정형외과 수술 로봇 시장의 로봇 액세서리, 지역별, 2021-2029 (백만 달러)

표 28 유럽 정형외과 수술 로봇 시장의 소프트웨어 및 장치, 지역별, 2021-2029년(백만 달러)

표 29 최종 사용자별 유럽 정형외과 수술 로봇 시장, 2020-2029년(백만 달러)

표 30 지역별 정형외과 수술 로봇 시장의 유럽 병원, 2020-2029년(백만 달러)

표 31 최종 사용자별 정형외과 수술 로봇 시장의 유럽 병원, 2020-2029년(백만 달러)

표 32 유럽 외래 수술 센터, 정형외과 수술 로봇 시장, 지역별, 2020-2029년(백만 달러)

표 33 유럽 정형외과 수술 로봇 시장, 유통 채널별, 2020-2029년(백만 달러)

표 34 2020-2029년 지역별 정형외과 수술 로봇 시장의 유럽 직접 입찰(백만 달러)

표 35 2020-2029년 지역별 정형외과 수술 로봇 시장의 유럽 제3자 유통업체(백만 달러)

표 36 국가별 유럽 정형외과 수술 로봇 시장, 2020-2029년(백만 달러)

표 37 제품 유형별 유럽 정형외과 수술 로봇 시장, 2020-2029년(백만 달러)

표 38 유럽 정형외과 수술 로봇 시장의 로봇 시스템, 응용 분야별, 2020-2029년(백만 달러)

표 39 수술 유형별 유럽 무릎 수술 로봇 시장, 2020-2029년(백만 달러)

표 40 유럽 무릎 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029년(백만 달러)

표 41 유럽 무릎 정형외과 수술 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 42 수술 유형별 유럽 고관절 수술 로봇 시장, 2020-2029년(백만 달러)

표 43 유럽 고관절 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029년(백만 달러)

표 44 유럽 고관절 정형외과 수술 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 45 유럽 척추 정형외과 수술 로봇 시장, 수술 유형별, 2020-2029년(백만 달러)

표 46 유럽 척추 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029년(백만 달러)

표 47 유럽 척추 정형외과 수술 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 48 유럽 정형외과 수술 로봇 시장 주요 규모, 로봇 유형별, 2020-2029년(백만 달러)

표 49 유럽 정형외과 수술 로봇 시장 주요 규모, 로봇 유형별, 규모, 2020-2029(단위)

표 50 유럽 대퇴골 정형외과 수술 로봇 시장, 수술 유형별, 2020-2029년(백만 달러)

표 51 유럽 대퇴골 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029년(백만 달러)

표 52 유럽 대퇴부 정형외과 수술 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 53 수술 유형별 유럽 골반 수술 로봇 시장, 2020-2029년(백만 달러)

표 54 유럽 골반 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029년(백만 달러)

표 55 유럽 골반 정형외과 수술 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 56 수술 유형별 정형외과 수술 로봇 시장에서 유럽의 영향력, 2020-2029년(백만 달러)

표 57 로봇 유형별 정형외과 수술 로봇 시장에서 유럽의 영향력, 2020-2029년(백만 달러)

표 58 유럽의 정형외과 수술 로봇 시장 점유율, 로봇 유형별, 양, 2020-2029(단위)

표 59 수술 유형별 유럽 엘보 수술 로봇 시장, 2020-2029년(백만 달러)

표 60 유럽 엘보우 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029년(백만 달러)

표 61 유럽 정형외과 수술용 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 62 최종 사용자별 유럽 정형외과 수술 로봇 시장, 2020-2029년(백만 달러)

표 63 최종 사용자별 정형외과 수술 로봇 시장의 유럽 병원, 2020-2029년(백만 달러)

표 64 유럽 정형외과 수술 로봇 시장, 유통 채널별, 2020-2029년(백만 달러)

표 65 독일 정형외과 수술 로봇 시장, 제품 유형별, 2020-2029년(백만 달러)

표 66 독일 정형외과 수술 로봇 시장의 로봇 시스템, 응용 분야별, 2020-2029년(백만 달러)

표 67 독일 무릎 수술 로봇 시장, 수술 유형별, 2020-2029(백만 달러)

표 68 로봇 유형별 독일 무릎 정형외과 수술 로봇 시장, 2020-2029(백만 달러)

표 69 로봇 유형별, 볼륨별, 2020-2029년(단위)의 독일 정형외과 수술용 로봇 시장 무릎

표 70 독일 고관절 수술 로봇 시장, 수술 유형별, 2020-2029(백만 달러)

표 71 로봇 유형별 독일 고관절 정형외과 수술 로봇 시장, 2020-2029년(백만 달러)

표 72 로봇 유형별, 볼륨별, 2020-2029년(단위)의 독일 정형외과 수술 로봇 시장 내 엉덩이

표 73 수술 유형별 독일 척추 정형외과 수술 로봇 시장, 2020-2029년(백만 달러)

표 74 로봇 유형별 독일 척추 정형외과 수술 로봇 시장, 2020-2029년(백만 달러)

표 75 로봇 유형별 독일 척추 정형외과 수술 로봇 시장, 볼륨, 2020-2029(단위)

표 76 로봇 유형별 정형외과 수술 로봇 시장에서 독일의 주요 업체, 2020-2029년(백만 달러)

표 77 로봇 유형별 정형외과 수술 로봇 시장, 규모, 2020-2029년(단위)별 독일 메이저

표 78 독일 대퇴골 정형외과 수술 로봇 시장, 수술 유형별, 2020-2029(백만 달러)

표 79 로봇 유형별 정형외과 수술 로봇 시장의 독일 대퇴골, 2020-2029년(백만 달러)

표 80 독일 대퇴골 정형외과 수술 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 81 수술 유형별 독일 골반 수술 로봇 시장, 2020-2029년(백만 달러)

표 82 로봇 유형별 정형외과 수술 로봇 시장에서의 독일 골반, 2020-2029년(백만 달러)

표 83 로봇 유형별, 볼륨별, 2020-2029년(단위)의 독일 골반 정형외과 수술 로봇 시장

표 84 수술 유형별 정형외과 수술 로봇 시장에서 독일의 영향력, 2020-2029년(백만 달러)

표 85 로봇 유형별 정형외과 수술 로봇 시장에서 독일의 영향력, 2020-2029년(백만 달러)

표 86 로봇 유형별 정형외과 수술 로봇 시장에서 독일의 점유율, 양, 2020-2029년(단위)

표 87 수술 유형별 독일 정형외과 수술 로봇 시장의 엘보, 2020-2029년(백만 달러)

표 88 로봇 유형별 정형외과 수술 로봇 시장에서의 독일 엘보, 2020-2029년(백만 달러)

표 89 로봇 유형별 정형외과 수술 로봇 시장의 독일 엘보, 양, 2020-2029(단위)

표 90 독일 정형외과 수술 로봇 시장, 최종 사용자별, 2020-2029년(백만 달러)

표 91 독일 병원의 정형외과 수술 로봇 시장, 최종 사용자별, 2020-2029(백만 달러)

표 92 독일 정형외과 수술 로봇 시장, 유통 채널별, 2020-2029년(백만 달러)

표 93 프랑스 정형외과 수술 로봇 시장, 제품 유형별, 2020-2029년(백만 달러)

표 94 프랑스 정형외과 수술 로봇 시장의 로봇 시스템, 응용 분야별, 2020-2029년(백만 달러)

표 95 수술 유형별 프랑스 무릎 수술 로봇 시장, 2020-2029(백만 달러)

표 96 로봇 유형별 정형외과 수술 로봇 시장의 프랑스 무릎, 2020-2029년(백만 달러)

표 97 정형외과 수술용 로봇 시장의 프랑스 무릎, 로봇 유형별, 볼륨, 2020-2029(단위)

표 98 수술 유형별 프랑스 엉덩이 수술 로봇 시장, 2020-2029년(백만 달러)

표 99 프랑스 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029(백만 달러)

표 100 프랑스 정형외과 수술 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 101 수술 유형별 프랑스 척추 정형외과 수술 로봇 시장, 2020-2029년(백만 달러)

표 102 로봇 유형별 프랑스 척추 정형외과 수술 로봇 시장, 2020-2029년(백만 달러)

표 103 로봇 유형별 프랑스 척추 정형외과 수술 로봇 시장, 볼륨, 2020-2029(단위)

표 104 프랑스 MAZOR의 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029년(백만 달러)

표 105 정형외과 수술 로봇 시장에서 프랑스 MAZOR, 로봇 유형별, 볼륨, 2020-2029(단위)

표 106 수술 유형별 프랑스 대퇴골 정형외과 수술 로봇 시장, 2020-2029년(백만 달러)

표 107 프랑스 대퇴골 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029년(백만 달러)

표 108 정형외과 수술 로봇 시장의 프랑스 대퇴부, 로봇 유형별, 볼륨, 2020-2029(단위)

표 109 수술 유형별 프랑스 골반 수술 로봇 시장, 2020-2029(백만 달러)

표 110 프랑스 골반 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029년(백만 달러)

표 111 프랑스 골반 정형외과 수술 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 112 수술 유형별 정형외과 수술 로봇 시장에서 프랑스의 점유율, 2020-2029년(백만 달러)

표 113 로봇 유형별 정형외과 수술 로봇 시장에서 프랑스의 점유율, 2020-2029년(백만 달러)

표 114 정형외과 수술 로봇 시장에서 프랑스의 점유율, 로봇 유형별, 볼륨, 2020-2029(단위)

표 115 수술 유형별 프랑스 정형외과 수술 로봇 시장(2020-2029년, 백만 달러)

표 116 프랑스 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029년(백만 달러)

표 117 정형외과 수술용 로봇 시장에서의 프랑스 엘보, 로봇 유형별, 볼륨, 2020-2029(단위)

표 118 최종 사용자별 프랑스 정형외과 수술 로봇 시장, 2020-2029년(백만 달러)

표 119 최종 사용자별 정형외과 수술 로봇 시장의 프랑스 병원, 2020-2029년(백만 달러)

표 120 프랑스 정형외과 수술 로봇 시장, 유통 채널별, 2020-2029년(백만 달러)

표 121 영국 정형외과 수술 로봇 시장, 제품 유형별, 2020-2029년(백만 달러)

표 122 영국 정형외과 수술 로봇 시장의 로봇 시스템, 응용 분야별, 2020-2029년(백만 달러)

표 123 영국 무릎 정형외과 수술 로봇 시장, 수술 유형별, 2020-2029년(백만 달러)

표 124 로봇 유형별 영국 무릎 정형외과 수술 로봇 시장, 2020-2029년(백만 달러)

표 125 로봇 유형별 영국 무릎 정형외과 수술 로봇 시장, 2020-2029년(백만 달러)

표 126 영국 고관절 정형외과 수술 로봇 시장, 수술 유형별, 2020-2029년(백만 달러)

표 127 로봇 유형별 영국 고관절 정형외과 수술 로봇 시장, 2020-2029년(백만 달러)

표 128 영국 정형외과 수술 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 129 영국 척추 정형외과 수술 로봇 시장, 수술 유형별, 2020-2029년(백만 달러)

표 130 로봇 유형별 영국 척추 정형외과 수술 로봇 시장, 2020-2029년(백만 달러)

표 131 로봇 유형별 영국 척추 정형외과 수술 로봇 시장, 볼륨, 2020-2029(단위)

표 132 로봇 유형별 영국 정형외과 수술 로봇 시장 주요 규모, 2020-2029년(백만 달러)

표 133 영국 정형외과 수술 로봇 시장 주요 규모, 로봇 유형별, 규모, 2020-2029(단위)

표 134 영국 대퇴골 정형외과 수술 로봇 시장, 수술 유형별, 2020-2029년(백만 달러)

표 135 로봇 유형별 영국 대퇴골 정형외과 수술 로봇 시장, 2020-2029년(백만 달러)

표 136 로봇 유형별 영국 대퇴골 정형외과 수술 로봇 시장, 2020-2029년(백만 달러)

표 137 수술 유형별 영국 골반 정형외과 수술 로봇 시장, 2020-2029년(백만 달러)

표 138 로봇 유형별 영국 골반 정형외과 수술 로봇 시장, 2020-2029년(백만 달러)

표 139 로봇 유형별 영국 골반 정형외과 수술 로봇 시장, 볼륨, 2020-2029(단위)

표 140 수술 유형별 영국 정형외과 수술 로봇 시장 점유율, 2020-2029년(백만 달러)

표 141 로봇 유형별 정형외과 수술 로봇 시장 점유율, 2020-2029년(백만 달러)

표 142 로봇 유형별 영국 정형외과 수술 로봇 시장 점유율, 양, 2020-2029(단위)

표 143 수술 유형별 영국 정형외과 수술 로봇 시장(2020-2029년) (백만 달러)

표 144 로봇 유형별 영국 정형외과 수술 로봇 시장, 2020-2029년(백만 달러)

표 145 로봇 유형별 영국 정형외과 수술용 로봇 시장, 양, 2020-2029(단위)

표 146 영국 정형외과 수술 로봇 시장, 최종 사용자별, 2020-2029년(백만 달러)

표 147 최종 사용자별 정형외과 수술 로봇 시장의 영국 병원, 2020-2029년(백만 달러)

표 148 영국 정형외과 수술 로봇 시장, 유통 채널별, 2020-2029년(백만 달러)

표 149 이탈리아 정형외과 수술 로봇 시장, 제품 유형별, 2020-2029년(백만 달러)

표 150 이탈리아 정형외과 수술 로봇 시장의 로봇 시스템, 응용 분야별, 2020-2029년(백만 달러)

표 151 이탈리아 무릎 수술 로봇 시장, 수술 유형별, 2020-2029(백만 달러)

표 152 로봇 유형별 이탈리아 무릎 정형외과 수술 로봇 시장, 2020-2029(백만 달러)

표 153 이탈리아 무릎 정형외과 수술 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 154 이탈리아 고관절 수술 로봇 시장, 수술 유형별, 2020-2029년(백만 달러)

표 155 이탈리아 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029년(백만 달러)

표 156 이탈리아 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029년(백만 달러)

표 157 수술 유형별 이탈리아 척추 정형외과 수술 로봇 시장, 2020-2029년(백만 달러)

표 158 로봇 유형별 이탈리아 척추 정형외과 수술 로봇 시장, 2020-2029년(백만 달러)

표 159 이탈리아 척추 정형외과 수술 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 160 이탈리아 MAZOR 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029(백만 달러)

표 161 이탈리아 정형외과 수술 로봇 시장 규모, 로봇 유형별, 규모, 2020-2029(단위)

표 162 이탈리아 대퇴골 정형외과 수술 로봇 시장, 수술 유형별, 2020-2029(백만 달러)

표 163 이탈리아 대퇴골 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029년(백만 달러)

표 164 이탈리아 대퇴골 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029년(백만 달러)

표 165 수술 유형별 이탈리아 골반 수술 로봇 시장, 2020-2029년(백만 달러)

표 166 이탈리아 골반 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029년(백만 달러)

표 167 이탈리아 골반 정형외과 수술 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 168 수술 유형별 정형외과 수술 로봇 시장에서 이탈리아의 점유율, 2020-2029년(백만 달러)

표 169 로봇 유형별 정형외과 수술 로봇 시장에서 이탈리아의 점유율, 2020-2029년(백만 달러)

표 170 로봇 유형별 정형외과 수술 로봇 시장에서 이탈리아의 점유율, 양, 2020-2029년(단위)

표 171 이탈리아 정형외과 수술 로봇 시장, 수술 유형별, 2020-2029년(백만 달러)

표 172 로봇 유형별 이탈리아 정형외과 수술 로봇 시장의 엘보, 2020-2029년(백만 달러)

표 173 이탈리아 정형외과 수술 로봇 시장의 엘보, 로봇 유형별, 볼륨, 2020-2029(단위)

표 174 이탈리아 정형외과 수술 로봇 시장, 최종 사용자별, 2020-2029년(백만 달러)

표 175 최종 사용자별 정형외과 수술 로봇 시장의 이탈리아 병원, 2020-2029년(백만 달러)

표 176 이탈리아 정형외과 수술 로봇 시장, 유통 채널별, 2020-2029년(백만 달러)

표 177 스페인 정형외과 수술 로봇 시장, 제품 유형별, 2020-2029년(백만 달러)

표 178 스페인 정형외과 수술 로봇 시장의 로봇 시스템, 응용 분야별, 2020-2029년(백만 달러)

표 179 스페인 무릎 수술 로봇 시장, 수술 유형별, 2020-2029(백만 달러)

표 180 스페인 무릎 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029(백만 달러)

표 181 스페인 정형외과 수술용 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 182 스페인 고관절 수술 로봇 시장, 수술 유형별, 2020-2029년(백만 달러)

표 183 스페인 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029년(백만 달러)

표 184 스페인 정형외과 수술 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 185 스페인 척추 정형외과 수술 로봇 시장, 수술 유형별, 2020-2029(백만 달러)

표 186 스페인 척추 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029년(백만 달러)

표 187 스페인 척추 정형외과 수술 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 188 스페인 MAZOR 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029(백만 달러)

표 189 스페인 정형외과 수술 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 190 스페인 대퇴골 정형외과 수술 로봇 시장, 수술 유형별, 2020-2029(백만 달러)

표 191 스페인 대퇴골 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029년(백만 달러)

표 192 스페인 대퇴부 정형외과 수술 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 193 스페인 골반 수술 로봇 시장, 수술 유형별, 2020-2029(백만 달러)

표 194 스페인 골반 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029(백만 달러)

표 195 스페인 골반 정형외과 수술 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 196 스페인의 정형외과 수술 로봇 시장 점유율, 수술 유형별, 2020-2029년(백만 달러)

표 197 스페인, 로봇 유형별 정형외과 수술 로봇 시장 점유율, 2020-2029년(백만 달러)

표 198 정형외과 수술 로봇 시장에서 스페인의 점유율, 로봇 유형별, 양, 2020-2029(단위)

표 199 스페인 정형외과 수술 로봇 시장, 수술 유형별, 2020-2029(백만 달러)

표 200 스페인 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029(백만 달러)

표 201 스페인 정형외과 수술 로봇 시장의 엘보, 로봇 유형별, 볼륨, 2020-2029(단위)

표 202 스페인 정형외과 수술 로봇 시장, 최종 사용자별, 2020-2029(백만 달러)

표 203 스페인 병원의 정형외과 수술 로봇 시장, 최종 사용자별, 2020-2029(백만 달러)

표 204 스페인 정형외과 수술 로봇 시장, 유통 채널별, 2020-2029년(백만 달러)

표 205 러시아 정형외과 수술 로봇 시장, 제품 유형별, 2020-2029년(백만 달러)

표 206 러시아 정형외과 수술 로봇 시장의 로봇 시스템, 응용 분야별, 2020-2029년(백만 달러)

표 207 러시아 무릎 수술 로봇 시장, 수술 유형별, 2020-2029(백만 달러)

표 208 러시아 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029년(백만 달러)

표 209 러시아 정형외과 수술용 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 210 러시아 정형외과 수술 로봇 시장, 수술 유형별, 2020-2029년(백만 달러)

표 211 러시아 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029년(백만 달러)

표 212 러시아 정형외과 수술 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 213 러시아 척추 정형외과 수술 로봇 시장, 수술 유형별, 2020-2029년(백만 달러)

표 214 러시아 척추 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029년(백만 달러)

표 215 러시아 정형외과 수술 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 216 러시아 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029년(백만 달러)

표 217 러시아 정형외과 수술 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 218 러시아 대퇴골 정형외과 수술 로봇 시장, 수술 유형별, 2020-2029(백만 달러)

표 219 러시아 대퇴골 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029(백만 달러)

표 220 러시아 대퇴부 정형외과 수술 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 221 러시아 골반 수술 로봇 시장, 수술 유형별, 2020-2029(백만 달러)

표 222 러시아 골반 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029(백만 달러)

표 223 러시아 골반 정형외과 수술 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 224 러시아의 정형외과 수술 로봇 시장 점유율, 수술 유형별, 2020-2029년(백만 달러)

표 225 로봇 유형별 정형외과 수술 로봇 시장에서 러시아의 점유율, 2020-2029년(백만 달러)

표 226 로봇 유형별 정형외과 수술 로봇 시장에서 러시아의 점유율, 양, 2020-2029년(단위)

표 227 러시아 정형외과 수술 로봇 시장, 수술 유형별, 2020-2029(백만 달러)

표 228 러시아 정형외과 수술 로봇 시장의 엘보, 로봇 유형별, 2020-2029년(백만 달러)

표 229 러시아 정형외과 수술 로봇 시장의 엘보, 로봇 유형별, 볼륨, 2020-2029(단위)

표 230 러시아 정형외과 수술 로봇 시장, 최종 사용자별, 2020-2029(백만 달러)

표 231 최종 사용자별 정형외과 수술 로봇 시장의 러시아 병원, 2020-2029년(백만 달러)

표 232 러시아 정형외과 수술 로봇 시장, 유통 채널별, 2020-2029년(백만 달러)

표 233 네덜란드 정형외과 수술 로봇 시장, 제품 유형별, 2020-2029년(백만 달러)

표 234 2020-2029년 응용 분야별 네덜란드 정형외과 수술 로봇 시장 로봇 시스템(백만 달러)

표 235 수술 유형별 네덜란드 무릎 수술 로봇 시장, 2020-2029년(백만 달러)

표 236 로봇 유형별 네덜란드 무릎 정형외과 수술 로봇 시장, 2020-2029년(백만 달러)

표 237 로봇 유형별 네덜란드 무릎 수술 로봇 시장, 볼륨, 2020-2029(단위)

표 238 수술 유형별 네덜란드 고관절 수술 로봇 시장, 2020-2029년(백만 달러)

표 239 로봇 유형별 네덜란드 고관절 정형외과 수술 로봇 시장, 2020-2029년(백만 달러)

표 240 로봇 유형별 네덜란드 고관절 수술 로봇 시장, 볼륨, 2020-2029(단위)

표 241 수술 유형별 네덜란드 척추 정형외과 수술 로봇 시장, 2020-2029년(백만 달러)

표 242 로봇 유형별 네덜란드 척추 정형외과 수술 로봇 시장, 2020-2029년(백만 달러)

표 243 로봇 유형별 네덜란드 척추 정형외과 수술 로봇 시장, 볼륨, 2020-2029(단위)

표 244 로봇 유형별 정형외과 수술 로봇 시장에서 네덜란드의 주요 시장, 2020-2029년(백만 달러)

표 245 로봇 유형별 네덜란드 정형외과 수술 로봇 시장 규모, 2020-2029년(단위)

표 246 수술 유형별 네덜란드 대퇴골 정형외과 수술 로봇 시장, 2020-2029년(백만 달러)

표 247 로봇 유형별 네덜란드 대퇴골 정형외과 수술 로봇 시장, 2020-2029년(백만 달러)

표 248 네덜란드 대퇴부 정형외과 수술 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 249 수술 유형별 네덜란드 골반 수술 로봇 시장, 2020-2029(백만 달러)

표 250 로봇 유형별 네덜란드 골반 정형외과 수술 로봇 시장, 2020-2029년(백만 달러)

표 251 로봇 유형별 네덜란드 골반 정형외과 수술 로봇 시장, 볼륨, 2020-2029(단위)

표 252 수술 유형별 정형외과 수술 로봇 시장 점유율 2020-2029년(백만 달러)

표 253 로봇 유형별 정형외과 수술 로봇 시장 점유율(네덜란드, 2020-2029년, 백만 달러)

표 254 로봇 유형별 정형외과 수술 로봇 시장 점유율, 규모, 2020-2029년(단위)

표 255 수술 유형별 네덜란드 엘보우 정형외과 수술 로봇 시장, 2020-2029(백만 달러)

표 256 로봇 유형별 네덜란드 엘보우 정형외과 수술 로봇 시장, 2020-2029년(백만 달러)

표 257 로봇 유형별 네덜란드 엘보우 정형외과 수술 로봇 시장, 볼륨, 2020-2029(단위)

표 258 네덜란드 정형외과 수술 로봇 시장, 최종 사용자별, 2020-2029년(백만 달러)

표 259 최종 사용자별 정형외과 수술 로봇 시장의 네덜란드 병원, 2020-2029년(백만 달러)

표 260 네덜란드 정형외과 수술 로봇 시장, 유통 채널별, 2020-2029년(백만 달러)

표 261 스위스 정형외과 수술 로봇 시장, 제품 유형별, 2020-2029년(백만 달러)

표 262 스위스 정형외과 수술 로봇 시장의 로봇 시스템, 응용 분야별, 2020-2029년(백만 달러)

표 263 수술 유형별 스위스 무릎 수술 로봇 시장, 2020-2029년(백만 달러)

표 264 스위스 무릎 수술 로봇 시장, 로봇 유형별, 2020-2029년(백만 달러)

표 265 스위스 정형외과 수술용 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 266 스위스 고관절 수술 로봇 시장, 수술 유형별, 2020-2029년(백만 달러)

표 267 스위스 고관절 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029년(백만 달러)

표 268 스위스 고관절 정형외과 수술 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 269 스위스 척추 정형외과 수술 로봇 시장, 수술 유형별, 2020-2029년(백만 달러)

표 270 로봇 유형별 스위스 척추 정형외과 수술 로봇 시장, 2020-2029년(백만 달러)

표 271 스위스 척추 정형외과 수술 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 272 스위스 MAZOR의 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029년(백만 달러)

표 273 스위스 정형외과 수술 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 274 스위스 대퇴골 정형외과 수술 로봇 시장, 수술 유형별, 2020-2029년(백만 달러)

표 275 스위스 대퇴골 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029년(백만 달러)

표 276 스위스 대퇴골 정형외과 수술 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 277 수술 유형별 스위스 골반 수술 로봇 시장, 2020-2029(백만 달러)

표 278 스위스 골반 수술 로봇 시장, 로봇 유형별, 2020-2029년(백만 달러)

표 279 스위스 골반 정형외과 수술 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 280 수술 유형별 정형외과 수술 로봇 시장에서 스위스의 점유율, 2020-2029년(백만 달러)

표 281 스위스, 로봇 유형별 정형외과 수술 로봇 시장 점유율, 2020-2029년(백만 달러)

표 282 스위스의 정형외과 수술 로봇 시장 점유율, 로봇 유형별, 규모, 2020-2029(단위)

표 283 수술 유형별 스위스 엘보우 정형외과 수술 로봇 시장, 2020-2029(백만 달러)

표 284 스위스 엘보 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029(백만 달러)

표 285 스위스 정형외과 수술용 로봇 시장, 로봇 유형별, 볼륨, 2020-2029(단위)

표 286 스위스 정형외과 수술 로봇 시장, 최종 사용자별, 2020-2029년(백만 달러)

표 287 최종 사용자별 정형외과 수술 로봇 시장의 스위스 병원, 2020-2029년(백만 달러)

표 288 스위스 정형외과 수술 로봇 시장, 유통 채널별, 2020-2029년(백만 달러)

표 289 터키 정형외과 수술 로봇 시장, 제품 유형별, 2020-2029년(백만 달러)

표 290 터키 정형외과 수술 로봇 시장의 로봇 시스템, 응용 분야별, 2020-2029년(백만 달러)

표 291 정형외과 수술 로봇 시장의 터키 무릎, 수술 유형별, 2020-2029년(백만 달러)

표 292 정형외과 수술 로봇 시장에서의 터키 무릎, 로봇 유형별, 2020-2029년(백만 달러)

표 293 정형외과 수술 로봇 시장에서의 터키 무릎, 로봇 유형별, 볼륨, 2020-2029(단위)

표 294 정형외과 수술 로봇 시장의 터키 엉덩이, 수술 유형별, 2020-2029(백만 달러)

표 295 정형외과 수술 로봇 시장의 터키 엉덩이, 로봇 유형별, 2020-2029년(백만 달러)

표 296 정형외과 수술 로봇 시장의 터키 엉덩이, 로봇 유형별, 볼륨, 2020-2029(단위)

표 297 정형외과 수술 로봇 시장의 터키 스파인, 수술 유형별, 2020-2029년(백만 달러)

표 298 로봇 유형별 정형외과 수술 로봇 시장의 터키 스파인, 2020-2029년(백만 달러)

표 299 정형외과 수술 로봇 시장에서의 터키 스파인, 로봇 유형별, 볼륨, 2020-2029(단위)

표 300 터키 메이저 정형외과 수술 로봇 시장, 로봇 유형별, 2020-2029(백만 달러)

표 301 정형외과 수술 로봇 시장에서의 터키 메이저, 로봇 유형별, 볼륨, 2020-2029(단위)

표 302 정형외과 수술 로봇 시장에서 터키 대퇴골, 수술 유형별, 2020-2029년(백만 달러)

표 303 정형외과 수술 로봇 시장에서의 터키 대퇴골, 로봇 유형별, 2020-2029년(백만 달러)

표 304 정형외과 수술 로봇 시장에서의 터키 대퇴골, 로봇 유형별, 볼륨, 2020-2029(단위)

표 305 정형외과 수술 로봇 시장의 터키 골반, 수술 유형별, 2020-2029년(백만 달러)

표 306 정형외과 수술 로봇 시장에서의 터키 골반, 로봇 유형별, 2020-2029년(백만 달러)

표 307 정형외과 수술 로봇 시장에서의 터키 골반, 로봇 유형별, 볼륨, 2020-2029(단위)

표 308 수술 유형별 정형외과 수술 로봇 시장에서 터키의 영향력, 2020-2029년(백만 달러)

표 309 로봇 유형별 정형외과 수술 로봇 시장에서 터키의 영향력, 2020-2029년(백만 달러)

표 310 로봇 유형별 정형외과 수술 로봇 시장에서 터키의 점유율, 양, 2020-2029년(단위)

표 311 정형외과 수술 로봇 시장의 터키 엘보, 수술 유형별, 2020-2029년(백만 달러)

표 312 정형외과 수술 로봇 시장의 터키 엘보, 로봇 유형별, 2020-2029년(백만 달러)

표 313 정형외과 수술 로봇 시장의 터키 엘보, 로봇 유형별, 볼륨, 2020-2029(단위)

표 314 터키 정형외과 수술 로봇 시장, 최종 사용자별, 2020-2029년(백만 달러)

표 315 최종 사용자별 정형외과 수술 로봇 시장의 터키 병원, 2020-2029년(백만 달러)

표 316 터키 정형외과 수술 로봇 시장, 유통 채널별, 2020-2029년(백만 달러)

표 317 벨기에 정형외과 수술 로봇 시장, 제품 유형별, 2020-2029년(백만 달러)

표 318 벨기에 정형외과 수술 로봇 시장의 로봇 시스템, 응용 분야별, 2020-2029년(백만 달러)

표 319 벨기에 무릎 수술 로봇 시장, 수술 유형별, 2020-2029(백만 달러)

표 320 로봇 유형별 정형외과 수술 로봇 시장의 벨기에 무릎, 2020-2029년(백만 달러)

표 321 로봇 유형별 정형외과 수술 로봇 시장의 벨기에 무릎, 양, 2020-2029(단위)

표 322 벨기에 고관절 수술 로봇 시장, 수술 유형별, 2020-2029(백만 달러)

표 323 로봇 유형별 정형외과 수술 로봇 시장의 벨기에 엉덩이, 2020-2029년(백만 달러)

표 324 로봇 유형별 정형외과 수술 로봇 시장의 벨기에 엉덩이, 양, 2020-2029(단위)

표 325 벨기에 척추 정형외과 수술 로봇 시장, 수술 유형별, 2020-2029(백만 달러)

표 326 로봇 유형별 정형외과 수술 로봇 시장에서 벨기에 척추, 2020-2029년(백만 달러)

표 327 로봇 유형별 정형외과 수술 로봇 시장의 벨기에 척추, 양, 2020-2029(단위)

표 328 로봇 유형별 정형외과 수술 로봇 시장에서 벨기에 MAZOR, 2020-2029(백만 달러)

표 329 로봇 유형별 정형외과 수술 로봇 시장에서 벨기에 메이저, 양, 2020-2029(단위)

표 330 벨기에 대퇴골 수술 로봇 시장, 수술 유형별, 2020-2029(백만 달러)

표 331 로봇 유형별 정형외과 수술 로봇 시장에서 벨기에 대퇴골, 2020-2029년(백만 달러)

표 332 로봇 유형별 정형외과 수술 로봇 시장의 벨기에 대퇴골, 양, 2020-2029(단위)

표 333 벨기에 골반 수술 로봇 시장, 수술 유형별, 2020-2029(백만 달러)

표 334 로봇 유형별 정형외과 수술 로봇 시장에서 벨기에 골반, 2020-2029년(백만 달러)

표 335 로봇 유형별 정형외과 수술 로봇 시장의 벨기에 골반, 양, 2020-2029(단위)

표 336 수술 유형별 정형외과 수술 로봇 시장에서 벨기에의 점유율, 2020-2029년(백만 달러)

표 337 로봇 유형별 정형외과 수술 로봇 시장에서 벨기에의 점유율, 2020-2029년(백만 달러)

표 338 로봇 유형별 정형외과 수술 로봇 시장에서 벨기에의 점유율, 양, 2020-2029년(단위)

표 339 벨기에 정형외과 수술 로봇 시장, 수술 유형별, 2020-2029(백만 달러)

표 340 로봇 유형별 정형외과 수술 로봇 시장에서의 벨기에 엘보, 2020-2029년(백만 달러)

표 341 로봇 유형별 정형외과 수술 로봇 시장의 벨기에 엘보, 양, 2020-2029(단위)

표 342 벨기에 정형외과 수술 로봇 시장, 최종 사용자별, 2020-2029(백만 달러)

표 343 최종 사용자별 정형외과 수술 로봇 시장의 벨기에 병원, 2020-2029년(백만 달러)

표 344 벨기에 정형외과 수술 로봇 시장, 유통 채널별, 2020-2029년(백만 달러)

표 345 유럽 기타 지역 정형외과 수술 로봇 시장, 제품 유형별, 2020-2029년(백만 달러)

그림 목록

그림 1 유럽 정형외과 수술 로봇 시장: 세분화

그림 2 유럽 정형외과 수술 로봇 시장: 데이터 삼각 측량

그림 3 유럽 정형외과 수술 로봇 시장: DROC 분석

그림 4 유럽 정형외과 수술 로봇 시장: 유럽 대 지역 시장 분석

그림 5 유럽 정형외과 수술 로봇 시장: 회사 연구 분석

그림 6 유럽 정형외과 수술 로봇 시장: 인터뷰 인구 통계

그림 7 유럽 정형외과 수술 로봇 시장: DBMR 시장 위치 그리드

그림 8 유럽 정형외과 수술 로봇 시장: 시장 최종 사용자 그리드

그림 9 유럽 정형외과 수술 로봇 시장: 공급업체 점유율 분석

그림 10 유럽 정형외과 수술 로봇 시장: 세분화

그림 11 골다공증 유병률 증가와 스포츠 및 외상 부상 발생률 증가가 2020년~2027년 예측 기간 동안 유럽 정형외과 수술 로봇 시장을 견인할 것으로 예상

그림 12 제품 유형은 2022년 및 2029년 유럽 정형외과 수술 로봇 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다.

그림 13 유럽 정형외과 수술 로봇 시장의 동인, 제약, 기회 및 과제

그림 14 현재 의료비 지출(GDP 대비 %) 2018-2019-

그림 15 유럽 정형외과 수술 로봇 시장: 제품 유형별, 2021

그림 16 유럽 정형외과 수술 로봇 시장: 제품 유형별, 2021-2029년(백만 달러)

그림 17 유럽 정형외과 수술 로봇 시장: 제품 유형별, CAGR(2021-2029)

그림 18 유럽 정형외과 수술 로봇 시장: 제품 유형별, 수명선 곡선

그림 19 유럽 정형외과 수술 로봇 시장: 최종 사용자별, 2021

그림 20 유럽 정형외과 수술 로봇 시장: 최종 사용자별, 2020-2029(백만 달러)

그림 21 유럽 정형외과 수술 로봇 시장: 최종 사용자별, CAGR(2022-2029)

그림 22 유럽 정형외과 수술 로봇 시장: 최종 사용자별, 수명선 곡선

그림 23 유럽 정형외과 수술 로봇 시장: 유통 채널별, 2021

그림 24 유럽 정형외과 수술 로봇 시장: 유통 채널별, 2022-2029년(백만 달러)

그림 25 유럽 정형외과 수술 로봇 시장: 유통 채널별, CAGR(2022-2029)

그림 26 유럽 정형외과 수술 로봇 시장: 유통 채널별, 수명선 곡선

그림 27 유럽 정형외과 수술 로봇 시장: 스냅샷(2021)

그림 28 유럽 정형외과 수술 로봇 시장: 국가별(2021년)

그림 29 유럽 정형외과 수술 로봇 시장: 국가별(2022년 및 2029년)

그림 30 유럽 정형외과 수술 로봇 시장: 국가별(2021년 및 2029년)

그림 31 유럽 정형외과 수술 로봇 시장: 제품 유형별(2022-2029)

그림 32 유럽 정형외과 수술 로봇 시장: 회사 점유율 2021(%)

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.