Global 3d Metrology Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

13.88 Billion

USD

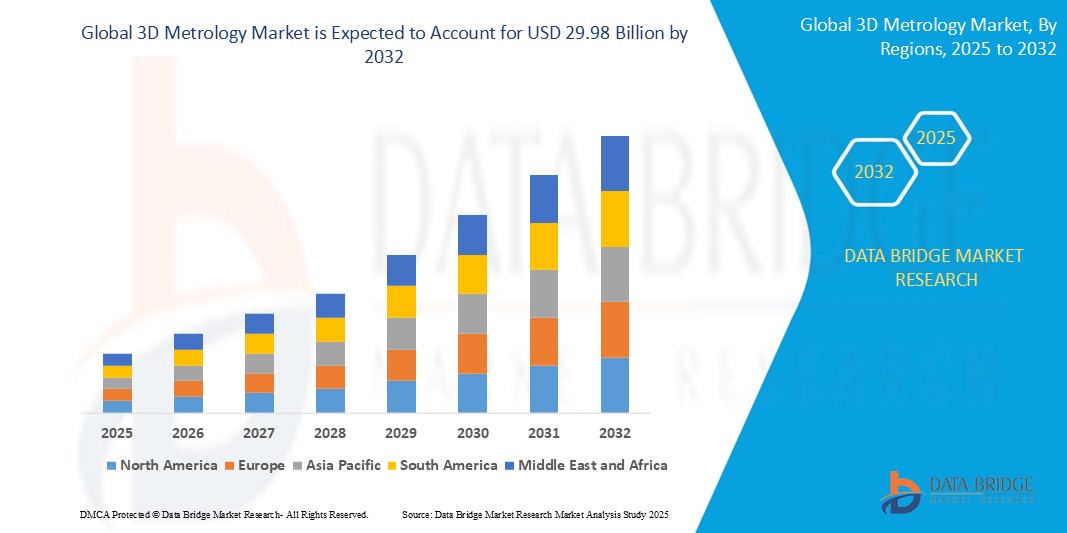

29.98 Billion

2024

2032

USD

13.88 Billion

USD

29.98 Billion

2024

2032

| 2025 –2032 | |

| USD 13.88 Billion | |

| USD 29.98 Billion | |

| % | |

|

글로벌 3D 계측 시장 세분화, 제품(하드웨어, 소프트웨어 및 서비스), 제품 유형(좌표 측정기(CMM), 운영 데이터 저장소, 가상 머신 관리자(VMM), 3D 자동 광학 검사 시스템, 형상 측정 등), 응용 분야(품질 관리 및 검사, 역설계, 가상 자극 등), 최종 사용 분야(항공우주 및 방위, 자동차, 건축 및 건설, 의료, 반도체 및 전자, 에너지 및 전력, 중장비, 광업 등) - 산업 동향 및 2032년까지의 전망

3D 계측 시장 규모

- 글로벌 3D 계측 시장 규모는 2024년에 138억 8천만 달러 로 평가되었으며 예측 기간 동안 10.10%의 CAGR 로 2032년까지 299억 8천만 달러에 도달할 것으로 예상됩니다 .

- 이러한 성장은 제조 부문 전반에 걸쳐 정밀 엔지니어링에 대한 수요 증가, 자동화된 품질 관리 시스템 도입 증가, 레이저 스캐너 및 좌표 측정기(CMM)와 같은 측정 솔루션의 지속적인 기술 발전과 같은 요인에 의해 촉진됩니다.

3D 계측 시장 분석

- 3D 계측 솔루션은 다양한 산업 분야에서 정밀한 치수 분석, 품질 관리 및 제품 검사에 사용되는 필수 도구입니다. 자동차 부품 검증, 항공우주 부품 검사, 전자 제조 등의 분야에서 매우 중요한 역할을 합니다.

- 3D 계측 시스템에 대한 수요는 제조 공정의 정확성, 품질 보증의 자동화, Industry 4.0 기술의 통합에 대한 강조가 커짐에 따라 크게 증가하고 있습니다.

- 북미는 강력한 산업 자동화 도입, 기술 발전 및 확립된 제조 기반 덕분에 34.9%의 가장 큰 시장 점유율로 3D 계측 시장을 지배할 것으로 예상됩니다.

- 아시아 태평양 지역은 산업 부문 확장, 정밀 제조에 대한 투자 증가, 자동차 및 전자 제품 생산 허브의 성장으로 인해 예측 기간 동안 3D 계측 시장에서 가장 빠르게 성장하는 지역이 될 것으로 예상됩니다.

- 자동차, 항공우주, 전자 산업에서 품질 관리를 위한 고정밀 측정 수요 증가로 하드웨어 부문이 67.2%의 시장 점유율로 시장을 장악할 것으로 예상됩니다. 이러한 성장은 하드웨어 부문의 성장을 촉진하고 있습니다. 이러한 부문에서 고정밀 측정 솔루션에 대한 수요는 엄격한 품질 기준을 충족하고 전반적인 제품 성능을 향상시키는 데 있어 하드웨어의 중요한 역할을 강조합니다.

보고서 범위 및 3D 계측 시장 세분화

|

속성 |

3D 계측 주요 시장 통찰력 |

|

다루는 세그먼트 |

|

|

포함 국가 |

북아메리카

유럽

아시아 태평양

중동 및 아프리카

남아메리카

|

|

주요 시장 참여자 |

|

|

시장 기회 |

|

|

부가가치 데이터 정보 세트 |

Data Bridge Market Research에서 큐레이팅한 시장 보고서에는 시장 가치, 성장률, 세분화, 지리적 범위, 주요 기업 등 시장 시나리오에 대한 통찰력 외에도 심층적인 전문가 분석, 지리적으로 대표되는 회사별 생산 및 용량, 유통업체 및 파트너의 네트워크 레이아웃, 자세하고 업데이트된 가격 추세 분석, 공급망 및 수요에 대한 부족 분석이 포함됩니다. |

3D 계측 시장 동향

“자동화 및 AI 기반 3D 계측 솔루션 도입”

- 3D 계측학 발전의 두드러진 추세 중 하나는 제조 환경에서 측정 속도, 정확도 및 의사 결정을 향상시키기 위해 자동화와 인공 지능(AI)의 통합이 증가하고 있다는 것입니다.

- 이러한 혁신을 통해 시스템은 수동 개입 없이 편차를 자동으로 감지하고 프로세스를 최적화할 수 있으므로 실시간 품질 관리가 가능해집니다.

- 예를 들어, AI 기반 3D 스캐닝 시스템은 복잡한 구성 요소의 결함이나 불일치를 자동으로 식별할 수 있으므로 항공우주, 자동차 및 의료 기기 제조와 같은 분야에서 매우 가치가 있습니다.

- 이러한 발전은 전통적인 계측 관행을 혁신하고, 인적 오류를 줄이고, 운영 효율성을 높이고, 글로벌 산업 전반에 걸쳐 지능형 자동화 3D 계측 시스템에 대한 수요를 촉진하고 있습니다.

3D 계측 시장 동향

운전사

“제조업의 정밀성과 품질에 대한 수요 증가”

- The increasing demand for high-precision components across industries such as automotive, aerospace, electronics, and healthcare is significantly driving the adoption of 3D metrology solutions

- As manufacturing processes become more advanced and tolerances tighter, companies are prioritizing dimensional accuracy and real-time quality control to reduce defects, optimize performance, and meet stringent regulatory standards

- In the automotive industry, complex parts like engine components, transmission systems, and safety features require precise measurements to ensure operational reliability and compliance with international safety norms

For instance,

- According to a 2023 report by the International Federation of Robotics, smart manufacturing and quality assurance systems are being rapidly deployed globally to improve production yields and reduce operational costs

- As a result, industries are increasingly turning to 3D metrology technologies—such as coordinate measuring machines (CMMs), laser scanners, and optical digitizers—to enhance measurement speed, accuracy, and integration within automated production lines

Opportunity

“Rising Adoption of Industry 4.0 and Smart Manufacturing Practices”

- The global shift toward Industry 4.0 is creating significant opportunities for the 3D metrology market, as manufacturers increasingly implement smart technologies to streamline operations and enhance precision

- 3D metrology systems, integrated with IoT, robotics, and cloud-based platforms, are being used for real-time monitoring, in-line inspection, and digital twin creation, enabling better process control and faster decision-making

- These systems support fully automated and connected production environments, reducing manual intervention and improving traceability across the product lifecycle

For instance,

- In the automotive sector, smart factories are leveraging 3D metrology to automate inspection of chassis, engine components, and safety-critical systems—significantly improving quality and reducing cycle time

- As more industries adopt digital manufacturing ecosystems, the demand for advanced 3D measurement solutions is expected to surge, offering strong growth prospects for technology providers

Restraint/Challenge

“High Equipment and Implementation Costs Limiting Market Adoption”

- The high initial investment required for 3D metrology equipment, such as coordinate measuring machines (CMMs), laser scanners, and optical digitizers, presents a substantial barrier for small- and medium-sized enterprises (SMEs), particularly in cost-sensitive regions

- In addition to hardware costs, the expenses associated with software integration, employee training, and ongoing system maintenance further amplify the financial burden for companies considering adoption

- These challenges can deter businesses from upgrading traditional measurement techniques or integrating advanced metrology into their production lines, slowing down the pace of digital transformation in quality control

For instance,

- According to industry reports, the cost of high-end 3D metrology solutions can exceed USD 100,000, excluding installation and training costs, making it difficult for smaller manufacturers to justify the ROI within a short timeframe

- As a result, limited affordability and lengthy implementation cycles can hinder market penetration, particularly in emerging economies, restricting the widespread adoption of 3D metrology technologies across diverse industrial sectors

3D Metrology Market Scope

The market is segmented on the basis of offerings, product type, application, and end use

|

Segmentation |

Sub-Segmentation |

|

By Offerings |

|

|

By Product Type |

|

|

By Application |

|

|

By End Use |

|

In 2025, the hardware is projected to dominate the market with a largest share in offerings segment

The hardware segment is expected to dominate the 3D metrology market with the largest share of 67.2%, due to rising demand for high-precision measurement for quality control in the automotive, aerospace, and electronics industries is fueling the growth of this segment. The demand for high-precision measurement solutions in these sectors underscores the critical role of hardware in meeting stringent quality standards and enhancing overall product performance

The aerospace and defense is expected to account for the largest share during the forecast period in end use segment

In 2025, the aerospace and defense segment is expected to dominate the market with the largest market share of approximately 30%, due to growing demand for precision in the manufacturing and assembly of complex aerospace and defense components. The need for high-accuracy measurements to ensure the structural integrity and performance of critical systems, such as aircraft and military equipment, is a significant factor

3D Metrology Market Regional Analysis

“North America Holds the Largest Share in the 3D Metrology Market”

- North America is the dominant region in the global 3D metrology market with largest market share of 34.9%, driven by well-established industries, cutting-edge manufacturing technologies, and strong adoption of advanced metrology solutions across key sectors such as aerospace, automotive, and electronics

- The U.S. holds a significant share of approximately 27.3%, due to its robust industrial base, increasing demand for precision measurements in sectors like aerospace and automotive, and continuous advancements in manufacturing technologies

- The availability of strong R&D investments, government initiatives to support high-tech manufacturing, and well-established infrastructure further strengthen the market

- In addition, the rising trend of automation and smart manufacturing in North America is fueling the demand for high-precision 3D metrology systems, which can offer real-time data and enhanced accuracy in production lines

“Asia-Pacific is Projected to Register the Highest CAGR in the3D Metrology Market”

- The Asia-Pacific region is expected to register the highest growth rate in the 3D metrology market, driven by rapid industrialization, increasing investments in manufacturing technologies, and growing awareness about quality control and precision

- Countries like China, India, and Japan are emerging as key markets, with Japan leading in the adoption of high-precision 3D metrology solutions, particularly in the automotive and electronics industries

- China and India, with their large-scale manufacturing capabilities and growing demand for quality control in production, are witnessing increased investments in 3D metrology technologies to enhance product quality and manufacturing efficiency

- The region’s expanding presence of global market players and the rapid adoption of advanced metrology solutions in key industries further contribute to market growth

3D Metrology Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Hexagon (Sweden)

- FARO (U.S.)

- Nikon Corporation (Japan)

- Carl Zeiss AG (Germany)

- KLA Corporation (U.S.)

- KEYENCE CORPORATION. (Japan)

- JENOPTIK AG (Germany)

- Renishaw plc. (U.K.)

- Mitutoyo South Asia Pvt. Ltd. (Japan)

- CREAFORM. (U.S.)

- GOM & COMPANY. (Germany)

- CHOTEST TECHNOLOGY INC. (China)

- Baker Hughes Company (U.S.)

- CyberOptics (U.S.)

- Trimble Inc. (U.S.)

- SGS SA (Switzerland)

- IKUSTEC (Spain)

Latest Developments in Global 3D Metrology Market

- 2023년 11월, 칼 자이스(Carl Zeiss AG)는 3D 측정 데이터의 검사 및 분석을 최적화하는 최첨단 솔루션인 자이스 인스펙트(Zeiss Inspect) 3D 계측 소프트웨어를 출시했습니다. 이 소프트웨어는 계측 애플리케이션의 데이터 수집 속도를 높이고 평가 효율성을 향상시키는 고급 기능을 통합했습니다. 이 혁신은 항공우주, 자동차, 제조 등 다양한 산업 분야에서 정밀도와 운영 생산성을 향상시켜 글로벌 3D 계측 시장 발전에 중요한 역할을 할 것으로 기대됩니다.

- 2023년 10월, Creaform은 대형 부품용으로 설계된 휴대성이 뛰어난 계측 등급 3D 스캐너인 HandySCAN 3D|MAX 시리즈를 출시했습니다. 이 획기적인 기술은 항공우주, 운송, 에너지, 광업, 중공업 등 다양한 산업 분야에서 성능과 사용성을 향상시키는 고급 기능을 통합했습니다. 이 휴대용 솔루션의 출시는 대형 부품 스캐닝의 정밀도와 효율성을 향상시켜 글로벌 3D 계측 시장에 큰 영향을 미칠 것으로 예상되며, 높은 정확도와 신뢰성이 요구되는 산업 분야에서 3D 계측 솔루션 도입을 더욱 가속화할 것입니다.

- 2023년 4월, 선도적인 소프트웨어 개발 기업인 InnovMetric은 제조업체의 3D 측정 프로세스 디지털 전환을 가속화하도록 설계된 주요 업그레이드 버전인 PolyWorks 2023을 출시했습니다. 최신 버전의 PolyWorks는 포괄적인 플랫폼 개선을 통해 3D 측정 팀의 효율성을 높이고, 운영을 간소화하며, 3D 측정 작업 관련 비용을 절감합니다. 이러한 혁신은 3D 측정 기술의 확장성, 경제성, 그리고 접근성을 향상시켜 다양한 제조 분야에서 도입을 확대함으로써 글로벌 3D 계측 시장에 상당한 영향을 미칠 것으로 예상됩니다.

- 2024년 4월, Hexagon의 Production Intelligence 사업부는 자동차 및 항공우주 생산 산업의 3D 측정에 혁명을 일으킬 혁신적인 모듈형 자동화 로봇 검사 셀 제품군인 PRESTO 시스템을 출시했습니다. 이 발전은 자동화를 강화하고, 효율성을 향상시키며, 수요가 높은 제조 분야에서 더욱 정밀한 품질 관리를 가능하게 함으로써 글로벌 3D 계측 시장의 성장을 견인할 것으로 예상됩니다.

- 2024년 1월, HighRES Inc.는 자사의 주력 제품인 ReverseEngineering.com이 새로운 SolidWorks 2024 Gold 인증 기준을 성공적으로 충족했다고 발표했습니다. 이번 성과는 직접 CAD 역설계 및 측정 소프트웨어 솔루션 분야에서 HighRES의 리더십을 보여주는 동시에, 다쏘시스템의 엄격한 기준을 충족하는 품질에 대한 헌신과 역량을 다시 한번 입증합니다. 이러한 이정표는 역설계 및 측정 도구의 기능을 향상시켜 산업 전반에 걸쳐 더욱 정확하고 효율적이며 원활한 3D 측정 프로세스를 구축함으로써 글로벌 3D 계측 시장에서 HighRES의 입지를 더욱 강화할 것입니다.

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.