Global Catheter Coatings Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

1.37 Billion

USD

2.19 Billion

2025

2033

USD

1.37 Billion

USD

2.19 Billion

2025

2033

| 2026 –2033 | |

| USD 1.37 Billion | |

| USD 2.19 Billion | |

| % | |

|

글로벌 카테터 코팅 시장 세분화: 유형별(금속, 폴리머, 라텍스 고무, 플라스틱 및 기타), 코팅 유형별(친수성 코팅, 약물 방출 코팅, 항균 코팅 및 기타), 응용 분야별(의료, 연구 및 기타) - 산업 동향 및 2033년까지의 전망

카테터 코팅 시장 규모

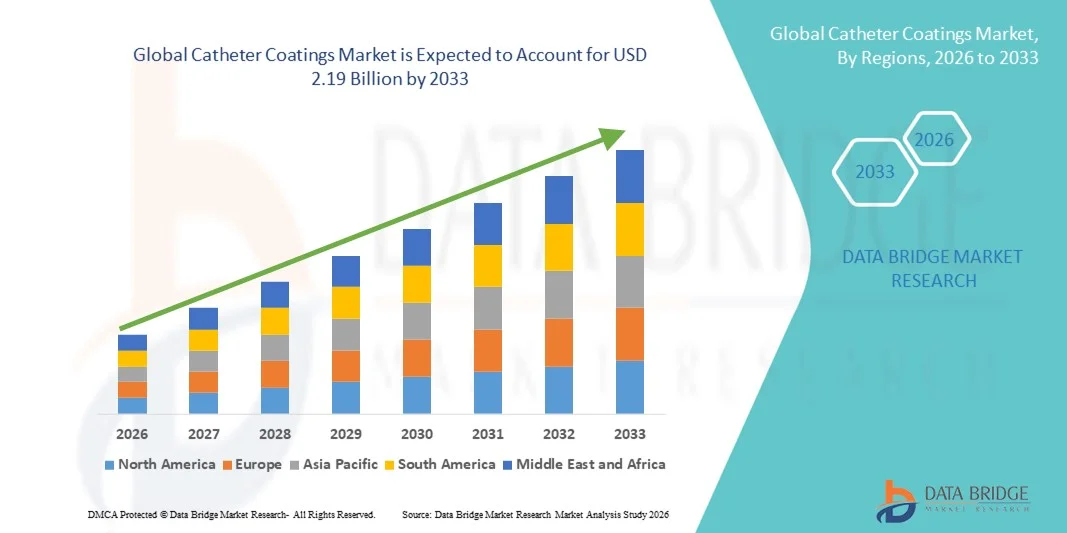

- 전 세계 카테터 코팅 시장 규모는 2025년 13억 7천만 달러 였으며 , 예측 기간 동안 연평균 6.09%의 성장률을 기록 하여 2033년에는 21억 9천만 달러 에 이를 것으로 예상됩니다.

- 시장 성장은 첨단 카테터 기술의 도입 증가, 카테터 관련 감염에 대한 인식 제고, 그리고 병원 및 진료 환경 모두에서 환자 친화적이고 안전한 비뇨기 및 혈관 기기에 대한 수요 증가에 힘입어 크게 촉진되고 있습니다.

- 카테터 코팅에 대한 수요 증가의 주요 원인은 친수성 및 항균 코팅 기술의 혁신, 요로 감염 및 카테터 관련 혈류 감염의 증가, 그리고 전 세계적으로 의료 인프라에 대한 투자 확대입니다.

카테터 코팅 시장 분석

- 카테터 코팅은 윤활성, 생체 적합성 및 항균성을 향상시켜 요로 및 혈관 카테터의 표면 특성을 개선하는 기술로, 환자의 불편함을 줄이고 감염 위험을 최소화하며 시술 효율성을 높이는 데 중요한 역할을 하므로 병원 및 임상 환경 모두에서 현대 의료 기기 솔루션의 핵심 요소로 자리 잡고 있습니다.

- 카테터 코팅에 대한 수요 증가는 주로 카테터 관련 감염의 증가, 최소 침습 시술의 도입 확대, 환자 안전 및 편안함에 대한 관심 증대, 그리고 전 세계 의료 시스템 전반에 걸친 친수성 및 항균 코팅 기술의 지속적인 발전으로 인해 발생하고 있습니다.

- 북미는 선진 병원 인프라, 높은 의료비 지출, 주요 의료기기 기업들의 존재에 힘입어 2025년까지 카테터 코팅 시장에서 약 38.7%의 최대 매출 점유율을 기록하며 시장을 주도할 것으로 예상됩니다. 특히 미국은 친수성 및 항균 코팅 카테터의 광범위한 도입과 지속적인 기술 혁신으로 인해 지역 매출의 대부분을 차지하고 있습니다.

- 아시아 태평양 지역은 향후 예측 기간 동안 카테터 코팅 시장에서 가장 빠르게 성장하는 지역으로, 의료 인프라 개선, 카테터 사용량 증가, 감염 예방에 대한 인식 제고, 그리고 중국, 인도, 일본과 같은 국가에서 첨단 코팅 카테터 기술의 도입이 확대됨에 따라 연평균 성장률(CAGR) 약 12.9%를 기록할 것으로 예상됩니다.

- 의료 부문은 2025년에 전체 시장 매출의 78.6%를 차지하며 가장 큰 비중을 차지할 것으로 예상됩니다. 이는 카테터가 병원, 클리닉, 외래 진료 기관에서 비뇨기, 심혈관 및 혈관 시술에 광범위하게 사용되기 때문입니다.

보고서 범위 및 카테터 코팅 시장 세분화

|

속성 |

카테터 코팅 주요 시장 분석 |

|

포함되는 부문 |

|

|

대상 국가 |

북아메리카

유럽

아시아태평양

중동 및 아프리카

남아메리카

|

|

주요 시장 참여자 |

|

|

시장 기회 |

|

|

부가가치 데이터 정보세트 |

데이터 브리지 마켓 리서치에서 제공하는 시장 보고서는 시장 가치, 성장률, 시장 세분화, 지리적 범위 및 주요 업체와 같은 시장 시나리오에 대한 통찰력 외에도 심층적인 전문가 분석, 환자 역학, 파이프라인 분석, 가격 분석 및 규제 체계에 대한 정보를 포함합니다. |

카테터 코팅 시장 동향

첨단 카테터 코팅 기술을 통한 향상된 편의성

- 전 세계 카테터 코팅 시장에서 중요하고 빠르게 성장하는 추세는 생체 적합성을 향상시키고 마찰을 줄이며 감염을 예방하는 첨단 코팅 개발입니다. 이러한 코팅은 환자의 안전을 강화하고 시술 효율성을 높이며 카테터 사용과 관련된 합병증을 줄여줍니다.

- 예를 들어, 2024년 3월 테루모(Terumo Corporation)는 비뇨기과 시술 중 요도 손상을 줄이고 환자의 불편함을 최소화하도록 설계된 차세대 친수성 카테터 코팅을 출시했습니다. 마찬가지로, 벡톤 디킨슨(BD)은 카테터 관련 요로 감염(CAUTI)을 예방하기 위해 항균 코팅 카테터를 도입하여 병원에 장기 카테터 삽입에 대한 더 안전한 선택지를 제공했습니다.

- 항균성, 친수성 및 약물 방출 코팅의 통합은 카테터의 세균 증식을 억제하고 삽입 용이성을 개선하며 입원 기간을 단축시킵니다. 예를 들어, 일부 차세대 카테터는 지속적인 항균 작용을 제공하기 위해 고분자 매트릭스와 결합된 은 이온 코팅을 사용합니다.

- 코팅 소재 및 표면 기술의 혁신으로 일회용 및 최소 침습 카테터의 사용이 확대되고 있으며, 이를 통해 의료진은 치료 결과를 최적화하고 시술 비용을 절감할 수 있습니다.

- 보다 안전하고 효율적이며 환자 친화적인 카테터 코팅에 대한 이러한 추세는 의료진과 병원의 기대치를 근본적으로 바꾸고 있습니다. 그 결과, CR Bard, Teleflex, Boston Scientific과 같은 기업들은 윤활성, 항균 활성 및 약물 방출 기능을 결합한 다기능 코팅 연구에 투자하고 있습니다.

- 병원과 의료기관들이 환자 안전, 시술 효율성 및 규정 준수를 점점 더 중요시함에 따라 비뇨기과, 심장내과 및 중환자 치료 분야에서 첨단 카테터 코팅에 대한 수요가 빠르게 증가하고 있습니다.

카테터 코팅 시장 동향

운전사

감염 예방 및 환자 안전에 대한 필요성 증가

- 카테터 관련 감염의 증가, 최소 침습 시술에 대한 수요 증가, 그리고 환자 안전에 대한 관심 증대는 카테터 코팅 시장의 주요 성장 동력입니다.

- 예를 들어, 2023년 6월 벡톤 디킨슨(Becton Dickinson)은 요로 감염(CAUTI) 발생률을 크게 줄여 병원 감염 관리 프로그램을 지원하도록 설계된 최신 항균 요도 카테터를 출시했습니다. 이처럼 주요 기업들의 제품 혁신은 예측 기간 동안 시장 성장을 견인할 것으로 예상됩니다.

- 병원과 진료소에서는 감염 위험을 줄이고 조직 자극을 최소화하며 환자 예후를 개선하는 코팅 카테터를 점점 더 많이 도입하고 있습니다.

- 전 세계적으로 비뇨기과, 심혈관과 및 중환자 치료 시술 건수가 증가함에 따라 시술 성공률을 높이는 친수성 및 항균성 코팅에 대한 수요가 증가하고 있습니다.

- 병원 내 감염(HAI) 감소에 대한 규제 강화와 의료 시설 내 감염 예방을 장려하는 정부 정책은 첨단 카테터 코팅 기술의 도입을 더욱 촉진하고 있습니다.

- 코팅 카테터의 장점(예: 불편함 감소 및 감염 위험 감소)에 대한 환자와 보호자의 인식이 높아짐에 따라 수요가 증가하고 있습니다.

- 가정 의료 및 외래 진료 서비스의 확대로 편의성과 안전성을 겸비한 일회용 코팅 카테터 사용이 증가하면서 시장 성장을 견인하고 있습니다.

- 카테터 제조업체와 제약 또는 재료 과학 회사 간의 전략적 협력은 신속한 연구 개발 및 혁신을 촉진하고 차세대 코팅 기술 출시를 가속화하고 있습니다.

- Emerging markets with rising healthcare expenditure and improving healthcare infrastructure, especially in India, China, and Brazil, are contributing to higher adoption rates of advanced catheter technologies

- Technological advancements in polymer science and nanomaterials are enabling multifunctional coatings that combine antimicrobial, lubricious, and drug-eluting properties, meeting the growing clinical demand for safer and more effective catheters

Restraint/Challenge

High Cost of Advanced Coatings and Regulatory Hurdles

- The relatively high cost of advanced catheter coatings compared to standard catheters can limit adoption in price-sensitive markets, particularly in developing countries or smaller hospitals

- For instance, premium hydrophilic and drug-eluting catheters can cost up to 3–5 times more than conventional catheters, posing a barrier for low-resource healthcare settings

- Strict regulatory requirements for coated medical devices, including safety and efficacy validation by the FDA, EMA, and other authorities, can prolong product development timelines

- Manufacturing complexities, such as uniform coating deposition, ensuring sterility, and quality control for multifunctional coatings, add operational costs and challenge scalability

- Supply chain constraints for specialized polymers or antimicrobial agents can disrupt production, causing delays in availability and increased costs

- Adoption may be slow in regions with limited hospital budgets or where traditional catheters are still considered clinically sufficient

- Lack of clinician awareness or training on the benefits of advanced coatings can reduce utilization rates in routine procedures

- Inconsistent reimbursement policies for premium catheter products in some healthcare systems can hinder widespread adoption

- While prices are gradually decreasing with technological advancement, perceived value versus cost can remain a concern, especially for outpatient or home-use catheters

- Overcoming these challenges through cost-effective coating technologies, faster regulatory approvals, robust clinician education programs, and evidence-based clinical studies demonstrating benefits will be vital for sustained market growth

Catheter Coatings Market Scope

The market is segmented on the basis of type, coating type, and application.

- By Type

On the basis of type, the Catheter Coatings market is segmented into metal, polymer, latex rubber, plastic, and others. The polymer segment dominated the largest market revenue share of 42.5% in 2025, driven by its versatility, biocompatibility, and ease of coating for multiple catheter types. Polymers such as polyurethane and silicone offer flexibility, low thrombogenicity, and superior mechanical properties, making them highly preferred in both short-term and long-term catheter applications. The growing demand for minimally invasive procedures and the expansion of the cardiovascular and urology segments further bolster polymer-based catheter adoption. Moreover, polymers’ compatibility with advanced coating technologies, such as drug-eluting and antimicrobial coatings, enhances their market presence. Hospitals and clinical centers favor polymer catheters due to reduced complications, patient comfort, and regulatory compliance in major markets like the U.S., Europe, and Asia-Pacific. The segment also benefits from ongoing R&D in hydrophilic and antimicrobial coatings integrated with polymers to reduce infection risks.

The latex rubber segment is anticipated to witness the fastest growth with a CAGR of 20.8% from 2026 to 2033, supported by rising demand in developing regions and improvements in hypoallergenic formulations. Latex catheters are cost-effective, widely available, and compatible with various coating technologies. Innovations in latex processing have reduced allergenic proteins, making them safer for long-term use. Emerging markets in Asia-Pacific and Latin America are increasingly adopting latex catheters for urinary and vascular applications due to affordability, ease of production, and growing healthcare infrastructure investments. The rapid increase in outpatient procedures, urological diagnostics, and catheterization labs contributes to the growth of this segment. Latex catheters with advanced coatings are expected to bridge cost-effectiveness with safety and performance, accelerating adoption.

- By Coating Type

On the basis of coating type, the Catheter Coatings market is segmented into hydrophilic coatings, drug-eluting coatings, anti-microbial coatings, and others. The hydrophilic coatings segment held the largest market revenue share of 44.1% in 2025, owing to their superior lubricity, reduced friction, and patient comfort during catheter insertion. Hydrophilic coatings are widely used in urinary and vascular catheters, reducing trauma, urethral irritation, and infection risks. Hospitals, outpatient centers, and diagnostic clinics prefer hydrophilic-coated catheters for both adult and pediatric populations. Adoption is further supported by regulatory approvals and clinical evidence demonstrating fewer complications compared to uncoated or standard catheters. The segment also benefits from rising demand in minimally invasive procedures and continuous innovations in polymeric hydrophilic surfaces for improved safety.

The drug-eluting coatings segment is expected to witness the fastest CAGR of 21.5% from 2026 to 2033, driven by the need for infection prevention and enhanced therapeutic delivery via catheters. Drug-eluting catheters, coated with antibiotics or antithrombotic agents, reduce hospital-acquired infections and improve patient outcomes. Growth is accelerated by increasing awareness of catheter-associated urinary tract infections (CAUTIs) and bloodstream infections (CLABSIs) globally. Research and development in controlled drug-release coatings is further fueling adoption in both developed and emerging markets. The segment sees strong uptake in cardiovascular, oncology, and urology applications due to the dual benefits of medical efficacy and patient safety.

- By Application

On the basis of application, the Catheter Coatings market is segmented into medical, research, and others. The medical segment accounted for the largest market revenue share of 78.6% in 2025, as catheters are extensively used in hospitals, clinics, and outpatient care for urinary, cardiovascular, and vascular procedures. The segment benefits from the growing prevalence of cardiovascular and urological disorders, aging populations, and the adoption of minimally invasive procedures. Advanced coatings improve safety, reduce infection risks, and enhance catheter performance, further increasing demand in healthcare settings. Regulatory approvals, reimbursement policies, and rising healthcare expenditure in developed countries contribute to the dominance of the medical application segment.

The research segment is expected to witness the fastest CAGR of 19.6% from 2026 to 2033, fueled by the rising use of catheters in preclinical studies, biomedical research, and pharmaceutical testing. Research applications often require specialized coatings for experimental drug delivery, antimicrobial testing, and biocompatibility studies. Academic institutes and biotech companies are investing in advanced catheter technologies for innovative studies, including tissue engineering and minimally invasive models. The increasing focus on R&D in catheter coatings and collaborations between universities and manufacturers accelerate growth in this segment.

Catheter Coatings Market Regional Analysis

- North America dominated the catheter coatings market with the largest revenue share of approximately 38.7% in 2025, supported by advanced hospital infrastructure, high healthcare expenditure, and the strong presence of leading medical device manufacturers

- Healthcare providers in the region place high importance on patient safety, infection prevention, and improved clinical outcomes, driving strong adoption of hydrophilic, antimicrobial, and drug-eluting catheter coatings

- This dominance is further reinforced by favorable reimbursement policies, high procedural volumes, and rapid adoption of technologically advanced coated catheters across hospitals, ambulatory surgical centers, and long-term care facilities

U.S. Catheter Coatings Market Insight

The U.S. catheter coatings market accounted for the majority share of North American revenue in 2025, driven by the high prevalence of chronic diseases, increasing catheterization procedures, and widespread adoption of advanced coated catheter technologies. Strong demand for hydrophilic and antimicrobial coatings to reduce catheter-associated infections, along with continuous product innovation by leading manufacturers, is significantly supporting market growth. Additionally, strict infection-control regulations and strong clinical awareness regarding hospital-acquired infections continue to boost the uptake of coated catheters across healthcare settings.

Europe Catheter Coatings Market Insight

The Europe catheter coatings market is projected to expand at a substantial CAGR during the forecast period, primarily driven by stringent regulatory standards for medical device safety and growing emphasis on infection prevention. Increasing surgical volumes, an aging population, and rising incidence of urological and cardiovascular disorders are supporting demand for advanced catheter coatings. European healthcare systems are increasingly adopting antimicrobial and lubricious coatings to enhance patient comfort and reduce post-procedural complications across hospitals and specialty clinics.

U.K. Catheter Coatings Market Insight

The U.K. catheter coatings market is anticipated to grow at a noteworthy CAGR over the forecast period, supported by rising healthcare investments and growing awareness of catheter-associated urinary tract infections (CAUTIs). National health initiatives focused on reducing hospital-acquired infections and improving patient outcomes are encouraging the adoption of coated catheters. Increased use of minimally invasive procedures and expanding use of catheters in home healthcare settings are further contributing to market growth in the country.

Germany Catheter Coatings Market Insight

The Germany catheter coatings market is expected to expand at a considerable CAGR during the forecast period, driven by a strong focus on medical innovation, patient safety, and advanced clinical practices. The country’s well-established healthcare infrastructure and emphasis on high-quality medical devices support the adoption of hydrophilic and antimicrobial catheter coatings. Growing demand from hospitals and specialty care centers for high-performance coated catheters is contributing to sustained market expansion.

Asia-Pacific Catheter Coatings Market Insight

The Asia-Pacific catheter coatings market is expected to be the fastest-growing region during the forecast period, registering a CAGR of around 12.9%, driven by improving healthcare infrastructure, rising catheter usage, and increasing awareness of infection prevention. Rapid growth in pharmaceutical and medical device manufacturing, combined with expanding access to healthcare services, is accelerating the adoption of advanced coated catheter technologies across the region. Government initiatives to strengthen healthcare systems are further supporting market growth.

Japan Catheter Coatings Market Insight

The Japan catheter coatings market is gaining steady momentum due to the country’s aging population, high prevalence of chronic diseases, and strong focus on patient safety. Increasing demand for long-term catheterization and minimally invasive procedures is driving adoption of hydrophilic and antimicrobial coatings. Japan’s emphasis on high-quality medical devices and infection-control practices continues to support the use of advanced catheter coatings in hospitals and home healthcare settings.

China Catheter Coatings Market Insight

The China catheter coatings market accounted for the largest revenue share in Asia-Pacific in 2025, supported by rapid healthcare infrastructure development, rising hospitalization rates, and increasing adoption of advanced medical technologies. Growing awareness of infection prevention, expanding access to healthcare services, and strong domestic manufacturing capabilities are driving demand for coated catheters across hospitals and clinics. Continued investments in healthcare modernization and rising procedural volumes are expected to further propel market growth in China.

Catheter Coatings Market Share

The Catheter Coatings industry is primarily led by well-established companies, including:

- Surmodics, Inc. (U.S.)

- DSM Biomedical (Netherlands)

- Hydromer, Inc. (U.S.)

- AST Products, Inc. (U.S.)

- BioCoat Incorporated (U.S.)

- Precision Coating Company, Inc. (U.S.)

- Covalon Technologies Ltd. (Canada)

- Harland Medical Systems, Inc. (U.S.)

- Aculon, Inc. (U.S.)

- Advanced Surface Technology, Inc. (U.S.)

- Biocoat Ltd. (U.K.)

- KISCO Ltd. (Japan)

- Applied Medical Coatings (U.S.)

- Formacoat LLC (U.S.)

- Medicoat AG (Switzerland)

- Surface Solutions Group (U.S.)

- Parylene Coatings Services (U.S.)

- Hemoteq AG (Germany)

- Specialty Coating Systems (U.S.)

- Royal DSM (Netherlands)

Latest Developments in Global Catheter Coatings Market

- In July 2023, Biocoat, a leading medical polymer and coating specialist, completed the acquisition of Chempilots, a custom polymers and production services firm, thereby broadening its biomaterials platform for hydrophilic and specialty catheter coatings used by OEMs in minimally invasive devices. This acquisition strengthened capabilities for customized coating solutions tailored to catheter applications

- 2023년 9월, 업계 보고서에 따르면 전 세계 카테터 코팅 시장은 2026년까지 15억 2천만 달러에 이를 것으로 전망되었습니다. 이는 심혈관 및 비뇨기과 시술에서 감염률을 낮추고 카테터 성능을 향상시키는 항균성, 친수성 및 윤활성 코팅에 대한 수요 증가에 힘입은 결과입니다. 이러한 전망은 카테터 표면 기술의 지속적인 혁신을 통해 시장 성장세와 추진력을 보여주고 있습니다.

- 2024년 11월, 메데올로직스는 바이오코트(Biocoat Incorporated)와의 전략적 파트너십을 통해 친수성 코팅 기술을 통합하여 카테터 제조 서비스를 확장했습니다. 이를 통해 자체적으로 첨단 코팅 기술을 적용하고 코팅 카테터 제품에 대한 규제 절차를 간소화할 수 있게 되었습니다. 확장된 서비스 범위는 제조 효율성을 높이고 제품 개발 기간을 단축하는 데 도움이 됩니다.

- 2024년 11월, 보스턴 사이언티픽은 암시노 인터내셔널과 차세대 항균 코팅 요도 카테터를 공동 개발 및 검증하기 위한 협력 계약을 발표했습니다. 이 협력은 코팅 내구성을 향상시키고 임상 환경에서 카테터 관련 감염률을 줄이는 것을 목표로 합니다. 이 계약은 감염 예방 기술에 대한 업계의 관심을 보여주는 사례입니다.

- 2025년 6월, 서페이스 솔루션 그룹(SSG)은 새로운 자동 정전기 로봇 코팅 라인을 설치하여 코팅 생산 능력을 확장했습니다. 이를 통해 카테터 윤활 및 항감염 기능을 포함한 의료기기 코팅에 대한 지역 시장의 증가하는 수요에 더욱 효과적으로 대응할 수 있게 되었습니다. 이번 투자는 카테터 표면 처리 분야의 생산 규모 확대를 의미합니다.

- 2025년 1월, 쿡 메디컬(Cook Medical)은 생체막 형성을 억제하고 기능 수명을 연장하여 카테터 관련 감염 문제를 해결하도록 설계된 새로운 은 이온 항균 코팅 요도 카테터를 출시했습니다. 이 제품 출시는 항균 표면 기술 분야의 지속적인 혁신을 반영합니다.

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.