Global Dermatology Diagnostic Devices Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

18.94 Billion

USD

50.72 Billion

2024

2032

USD

18.94 Billion

USD

50.72 Billion

2024

2032

| 2025 –2032 | |

| USD 18.94 Billion | |

| USD 50.72 Billion | |

| % | |

|

Global Dermatology Diagnostic Devices Market Segmentation, By Diagnostic Device (Imaging Device, Dermatoscope, and Microscope), Treatment Device (Electrosurgical, Cryotherapy, and Laser), Type (Dermatoscopes, Imaging Equipment, Microscopes and Trichoscopes, Biopsy Devices, and Others), Application (Skin Care and Others), End-User (Hospitals, Clinics, and Others) - Industry Trends and Forecast to 2032

Dermatology Diagnostic Devices Market Size

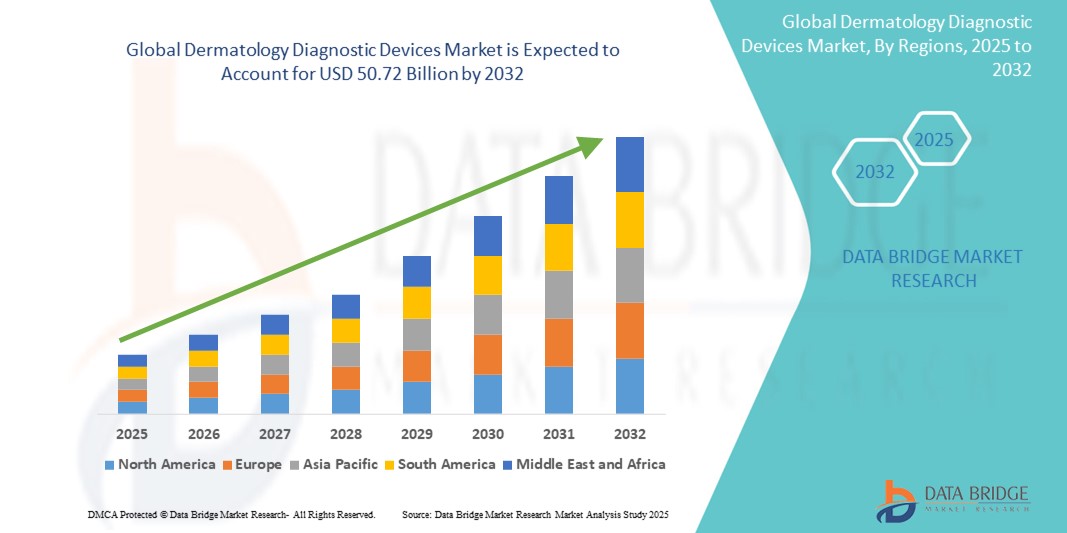

- The global Dermatology Diagnostic Devices market size was valued atUSD 18.94 billion in 2024and is expected to reachUSD 50.72 billion by 2032, at aCAGR of 13.10%during the forecast period

- This growth is driven by factors such as the increasing prevalence of skin disorders, advancements in diagnostic technologies, and the rising adoption of tele dermatology services

Dermatology Diagnostic Devices Market Analysis

- Growing consciousness among the individuals to look good in public, thereby resulting in the feeling of confidence and courage, has carved the way for the growth of innovations in the dermatology department.

- Growing number of product innovations by the major manufacturers has resulted in the availability of high grade and high quality dermatology diagnostic devices all around the globe.

- North America is expected to dominate the dermatology diagnostic devices market with 43.5% due to increasing prevalence of skin cancer and other skin diseases such as acne, eczema & rosacea and increasing adoption of cosmetic procedures are some of the major factors contributing to the growth of the market in this region

- Asia-Pacific expected to be the fastest growing region in the dermatology diagnostic devices market during the forecast period due to population growth, urbanization, and increasing disposable income and medical tourism

- Laser segment is expected to dominate the market with a market share of 79.3% due to its high prevalence and demand for precision. In addition, the launch of novel technologies in the laser device category is also attributed to the high segment growth

Report Scope and Dermatology Diagnostic Devices Market Segmentation

|

Attributes |

Dermatology Diagnostic Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Dermatology Diagnostic Devices Market Trends

“Integration of Whole-Body 3D Imaging”

- The dermatology diagnostic devices market is witnessing a significant trend towards the adoption of whole-body 3D imaging systems. These advanced technologies enable comprehensive skin assessments, facilitating early detection and monitoring of skin conditions

- For Instance, In June 2023, Hoag Hospital in the U.S. introduced the VECTRA WB360, the world's first whole-body 3D photographic imaging system. This system employs 92 cameras to capture a patient's entire skin surface in less than a second, creating a 3D avatar mapping all moles and lesions with high-resolution fidelity

- The integration of AI-powered imaging software with these systems enhances diagnostic accuracy and efficiency, enabling healthcare providers to detect skin abnormalities at an early stage

- The adoption of whole-body 3D imaging is expected to drive market growth by improving patient outcomes and reducing the need for invasive procedures

- As technology continues to advance, the trend towards non-invasive, comprehensive diagnostic tools is likely to become more prevalent, shaping the future of dermatology diagnostics

Dermatology Diagnostic Devices Market Dynamics

Driver

“Increasing Incidence of Skin Cancer”

- Skin cancer, particularly melanoma, is on the rise globally. According to the American Academy of Dermatology Association, the incidence of melanoma has been increasing steadily, highlighting the need for effective diagnostic tools

- The growing prevalence of skin cancer has led to an increased demand for dermatology diagnostic devices, as early detection is crucial for effective treatment

- In response to this demand, companies are developing advanced diagnostic devices, such as AI-powered imaging systems, to improve detection accuracy and speed

- The rising incidence of skin cancer places a significant burden on healthcare systems, necessitating the development and adoption of efficient diagnostic solutions

- The increasing incidence of skin cancer is a primary driver of market growth, as healthcare providers seek advanced diagnostic tools to manage the rising number of cases

Opportunity

“Expansion in Emerging Markets”

- Emerging markets, particularly in Asia-Pacific and Latin America, present significant growth opportunities for the dermatology diagnostic devices market. These regions have large populations with increasing awareness of skin health issues

- Improving healthcare infrastructure and rising disposable incomes in these regions are facilitating the adoption of advanced diagnostic technologies

- Companies expanding their presence in emerging markets can tap into a large, underserved customer base, driving revenue growth

- Governments in emerging markets are implementing policies to enhance healthcare access, creating a favorable environment for the introduction of new diagnostic devices

- The expansion into emerging markets offers long-term growth prospects, as these regions continue to develop economically and healthcare access improves

Restraint/Challenge

“High Cost of Diagnostic Devices”

- The high cost of advanced dermatology diagnostic devices poses a significant barrier to their widespread adoption, particularly in low-resource settings

- In addition to initial costs, ongoing maintenance and operational expenses further strain budgets, limiting access to these technologies

- The cost factor exacerbates healthcare disparities, as patients in economically disadvantaged regions may not afford necessary diagnostic services

- High costs restrict the market potential, as only well-funded healthcare facilities can invest in such technologies, leaving a significant portion of the population underserved

- While technological advancements are crucial, the challenge remains to develop cost-effective solutions that can be accessible to a broader population without compromising quality

Dermatology Diagnostic Devices Market Scope

The market is segmented on the basis diagnostic device, treatment device, type, application and end-User.

|

Segmentation |

Sub-Segmentation |

|

By Diagnostic Device |

|

|

Treatment Device |

|

|

By Type |

|

|

By Application |

|

|

By End-User |

|

In 2025, the laser is projected to dominate the market with a largest share in treatment device segment

The laser segment is expected to dominate the Dermatology Diagnostic Devices market with the largest share of 79.3% in 2025 due to its high prevalence and demand for precision. In addition, the launch of novel technologies in the laser device category is also attributed to the high segment growth. This is mainly due to the availability of wide applications of dermatology treatment

The skin care is expected to account for the largest share during the forecast period in application market

In 2025, the skin care segment is expected to dominate the market with the largest market share of 11.8% due to particularly laser devices have been proved to be safer for all skin tones and hair colour and facilitate less painful treatment procedures, thereby propelling the market. A rise in demand for cosmetic laser treatments such as tattoo removal, skin resurfacing and skin tightening has significantly increased the adoption of dermatology devices.

Dermatology Diagnostic Devices Market Regional Analysis

“North America Holds the Largest Share in the Dermatology Diagnostic Devices Market”

- North America holds a dominant position in the global dermatology diagnostic devices market, with the U.S. accounting for the highest share of 43.5%

- The region exhibits an 88% adoption rate of AI-driven dermatology tools, significantly enhancing diagnostic accuracy

- Robust healthcare infrastructure and substantial investments in research and development contribute to the region's market leadership

- There is a growing preference for non-invasive and minimally invasive diagnostic technologies, reflecting an increasing focus on early detection of skin disorders

“Asia-Pacific is Projected to Register the Highest CAGR in the Dermatology Diagnostic Devices Market”

- The Asia-Pacific region is experiencing the fastest growth in the dermatology diagnostic devices market,

- There has been rise in demand for dermatology treatments, driven by increasing disposable income and medical tourism

- AI-driven dermatology tools have seen an 87% adoption rate, improving diagnostic accuracy

- The region has witnessed an expansion in cosmetic dermatology, fueled by beauty-conscious consumers

- With growing awareness of skin health, rising healthcare expenditures, and expanding healthcare infrastructure, the region is poised for continued growth in the dermatology diagnostic devices market

Dermatology Diagnostic Devices Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Agfa-Gevaert Group(Belgium)

- Carl Zeiss AG(Germany)

- STRATA Skin Sciences(U.S.)

- Hologic, Inc. (U.S.)

- Illumina, Inc. (U.S.)

- Spindletop Capital (U.S.)

- Heine Optotechnik (Germany)

- GENERAL ELECTRIC COMPANY (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Leica Microsystems (Germany)

- Bruker (U.S.)

- Solta Medical (U.S.)

- CANDELA CORPORATION (U.S.)

- Ambicare Health (U.K.)

- Siemens Healthcare Private Limited (Germany)

- Welch Allyn (U.S.)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- Galderma laboratories (U.S.)

- Michelson Diagnostics Inc. (U.K.)

- Canfield Scientific, Inc. (U.S.)

Latest Developments in Global Dermatology Diagnostic Devices Market

- In July 2023,Canfield Scientifichad announced the 25th World Congress of Dermatology, which was held from the 4th to the 7th of July at the Suntec Singapore Convention & Exhibition Centre. It comprised in-person demonstrations of its advanced and latest dermatology devices and solutions, including IntelliStudio, VEOS, DermaGraphix, and VECTRA WB360

- In June 2023,Hoag Hospitalin the U.S. introduced theVECTRA WB360, the world's first whole-body 3D photographic imaging system. This system employs 92 cameras to capture a patient's entire skin surface in less than a second, creating a 3D avatar mapping all moles and lesions with high-resolution fidelity

- In February 2023, Candela Corporation, a global manufacturer of medical aesthetic devices announced that the dual-wavelength Frax Pro non-ablative fractional laser platform and the Nordlys multi-application platform with Selective Waveband Technology (SWT) were licensed and made available by Health Canada.

- In January 2021,Casio Computer Co., Ltd. announced the upcoming release of the DZ-D100 DERMOCAMERA that allows close-up shots with the lens directly touching the skin as well as ordinary shots, all using a single camera.

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.