Global Electroceuticalsbioelectric Medicine Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

25.94 Billion

USD

50.00 Billion

2025

2033

USD

25.94 Billion

USD

50.00 Billion

2025

2033

| 2026 –2033 | |

| USD 25.94 Billion | |

| USD 50.00 Billion | |

| % | |

|

Global Electroceuticals/Bioelectric Medicine Market Segmentation, By Product (Implantable Cardioverter Defibrillators, Cardiac Pacemakers, Spinal Cord Stimulators, Cochlear Implants, Deep Brain Stimulators, Transcutaneous Electrical Nerve Stimulators, Vagus Nerve Stimulators, Sacral Nerve Stimulators, and Retinal Implants), Type of Device (Implantable Electroceutical, and Non-Invasive Electroceutical), End User (Hospitals, Clinics, Research Institutes, and Individual Users)- Industry Trends and Forecast to 2033

Electroceuticals/Bioelectric Medicine Market Size

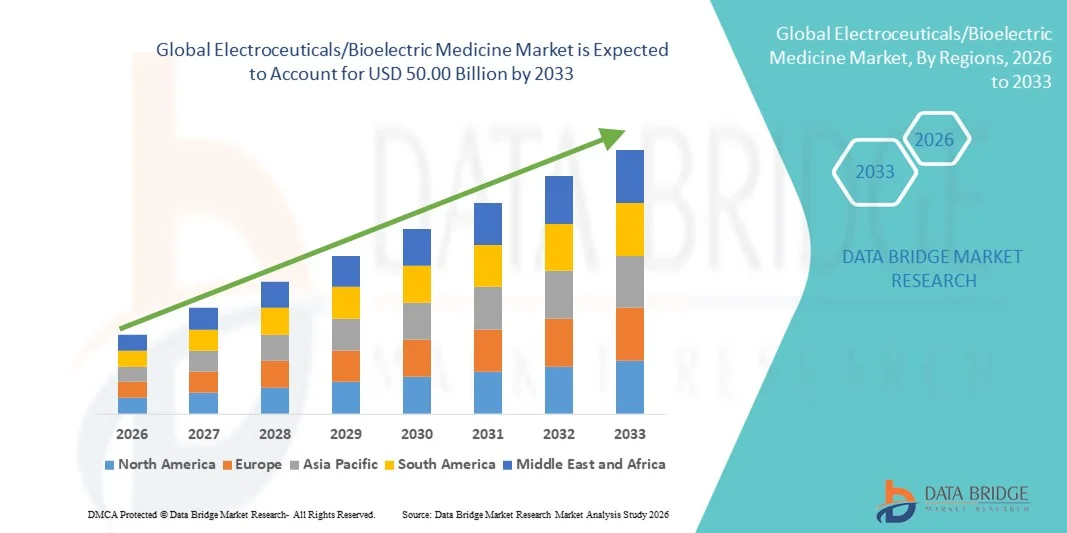

- The global electroceuticals/bioelectric medicine market size was valued at USD 25.94 billion in 2025 and is expected to reach USD 50.00 billion by 2033, at a CAGR of 8.55% during the forecast period

- The market growth is largely fueled by the increasing prevalence of chronic and acute diseases rapid technological advancements in bioelectronic therapies and neuromodulation devices, and continued R&D investments aimed at non‑pharmacological treatment modalities that offer targeted physiological modulation

- Furthermore, rising demand for minimally invasive and personalized treatment options that improve patient outcomes and reduce dependency on traditional drug therapies is establishing electroceutical and bioelectric medicine solutions as preferred alternatives across both clinical and homecare settings. These converging factors are accelerating the adoption of bioelectric therapies, thereby significantly boosting industry growth

Electroceuticals/Bioelectric Medicine Market Analysis

- Electroceuticals or bioelectric medicine devices, providing targeted electrical stimulation to modulate nerve and organ function, are increasingly vital components of modern healthcare, offering alternative or adjunct therapies for chronic and acute conditions such as cardiovascular, neurological, and inflammatory disorders due to their precision, minimally invasive nature, and potential to reduce drug dependency

- The escalating demand for electroceuticals is primarily fueled by the rising prevalence of chronic diseases, growing patient awareness of non-pharmacological therapies, and rapid technological advancements in neuromodulation, wearable stimulators, and implantable bioelectronic devices

- North America dominated the electroceuticals/bioelectric medicine market with the largest revenue share of 40% in 2025, characterized by early adoption of advanced medical technologies, high healthcare expenditure, and a strong presence of key industry players

- Asia-Pacific is expected to be the fastest-growing region in the electroceuticals market during the forecast period due to increasing healthcare infrastructure investments, rising patient awareness, and expanding adoption of advanced therapies in emerging economies such as China and India

- Implantable Cardioverter Defibrillators segment dominated the market with a share of 45.9% in 2025, driven by their established efficacy in managing chronic pain, cardiac arrhythmias, and other disorders, along with advancements enabling minimally invasive implantation and personalized stimulation protocols

Report Scope and Electroceuticals/Bioelectric Medicine Market Segmentation

|

Attributes |

Electroceuticals/Bioelectric Medicine Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Electroceuticals/Bioelectric Medicine Market Trends

Advancements Through AI-Enabled and Wearable Neuromodulation

- A significant and accelerating trend in the global electroceuticals market is the integration of artificial intelligence (AI) with implantable and wearable neuromodulation devices, enhancing precision therapy and personalized patient care

- For instance, the Cala Trio wearable neuromodulation device uses AI algorithms to optimize stimulation patterns for patients with essential tremor, providing targeted symptom relief without the need for invasive surgery

- AI-enabled devices can monitor physiological responses in real time, adjust stimulation intensity, and provide predictive insights for treatment efficacy, while wearable systems allow patients to manage therapy conveniently outside clinical settings

- The seamless connectivity of bioelectronic devices with digital health platforms enables centralized monitoring by physicians, remote adjustments, and integration with electronic health records, improving treatment adherence and outcomes

- This trend toward smarter, adaptive, and connected neuromodulation solutions is redefining patient expectations for chronic disease management. Consequently, companies such as SetPoint Medical are developing AI-enabled bioelectronic devices with adaptive stimulation protocols and remote monitoring capabilities

- The demand for electroceuticals with AI integration and wearable capabilities is rapidly increasing across both hospital and homecare settings, as patients and clinicians seek personalized, non-pharmacological therapies

- Growing interest in combining electroceuticals with other therapeutic modalities, such as physiotherapy and cognitive training, is creating hybrid solutions that improve treatment outcomes and patient satisfaction

Electroceuticals/Bioelectric Medicine Market Dynamics

DriverRising Prevalence of Chronic Diseases and Need for Targeted Therapies

- The growing prevalence of chronic conditions such as cardiovascular, neurological, and inflammatory disorders, along with increased patient preference for non-drug therapies, is a major driver for electroceutical adoption

- For instance, in March 2025, Boston Scientific announced an expanded clinical program for its spinal cord stimulation system targeting chronic pain patients, demonstrating the market potential of targeted neuromodulation

- As awareness of non-pharmacological therapies rises, electroceuticals provide advantages such as precise symptom control, minimized side effects, and improved quality of life compared to conventional treatments

- Furthermore, the rapid adoption of wearable and implantable neuromodulation devices is promoting integration with digital health platforms, allowing remote monitoring and real-time therapy optimization

- The ability to provide patient-specific, adjustable stimulation and non-invasive alternatives to traditional therapies is enhancing demand across hospitals, clinics, and homecare applications

- Increasing investments from venture capital and healthcare technology firms are accelerating R&D and commercial availability of novel electroceutical therapies

- Government initiatives and reimbursement policies for innovative, non-drug treatments in developed markets are further driving adoption of bioelectronic medicine

Restraint/Challenge

High Cost and Regulatory Complexity

- The high development and manufacturing costs, coupled with complex regulatory approval processes, pose significant challenges to wider market penetration of electroceutical devices

- For instance, long clinical trial durations and stringent FDA or CE mark requirements can delay product launches, increasing financial risk for companies developing novel bioelectronic therapies

- While electroceuticals offer significant clinical benefits, high device costs compared to conventional therapies can limit adoption, particularly in emerging markets with constrained healthcare budgets

- Additionally, concerns over device safety, long-term efficacy, and the need for specialized clinical training can create hesitation among healthcare providers and patients

- Addressing these challenges through cost optimization, streamlined regulatory pathways, and enhanced clinician and patient education will be critical to sustain market growth over the forecast period

- Interoperability issues with existing hospital IT infrastructure and electronic health record systems can hinder seamless adoption of electroceutical devices

- Potential patient apprehension toward implantable or wearable electrical devices, due to perceived discomfort or fear of side effects, remains a barrier to widespread acceptance

Electroceuticals/Bioelectric Medicine Market Scope

The market is segmented on the basis of product, type of device, and end user.

- By Product

On the basis of product, the electroceuticals market is segmented into implantable cardioverter defibrillators (ICDs), cardiac pacemakers, spinal cord stimulators (SCS), cochlear implants, deep brain stimulators (DBS), transcutaneous electrical nerve stimulators (TENS), vagus nerve stimulators (VNS), sacral nerve stimulators, and retinal implants. Spinal Cord Stimulators (SCS) dominated the market with the largest revenue share in 2025, driven by the growing prevalence of chronic pain and musculoskeletal disorders. SCS devices are widely adopted in hospitals and pain management clinics due to their proven clinical efficacy in reducing pain and improving quality of life for patients who are non-responsive to pharmacological therapy. The segment benefits from technological advancements such as rechargeable and MRI-compatible devices, enhancing patient convenience and adoption. Additionally, increasing awareness among physicians and patients about non-drug therapies is further boosting demand. Strong R&D investment and FDA approvals of next-generation SCS systems are supporting market growth. SCS devices also integrate with remote monitoring platforms, improving clinical outcomes and treatment adherence, making them highly preferred in advanced healthcare settings.

Cochlear Implants are anticipated to witness the fastest growth from 2026 to 2033, fueled by rising incidences of hearing loss across all age groups and improved accessibility of advanced auditory technologies. The segment is supported by continuous innovation, including smaller, less invasive implants and integration with wireless and AI-enabled audio processing. Cochlear implants are increasingly being adopted in emerging markets due to growing government and NGO programs for hearing impairment solutions. Awareness campaigns and reimbursement coverage in developed economies further accelerate adoption. Technological improvements such as smartphone compatibility and enhanced sound quality are increasing user acceptance. These factors collectively drive the rapid expansion of the cochlear implant subsegment in the global market.

- By Type of Device

On the basis of type, the market is segmented into implantable electroceuticals and non-invasive electroceuticals. Implantable Electroceuticals dominated the market in 2025 with a market share of 45.9% due to their proven effectiveness in treating severe chronic conditions such as cardiac arrhythmias, Parkinson’s disease, and chronic pain. Implantable devices, including ICDs, pacemakers, and DBS, offer targeted, continuous therapy, which enhances patient outcomes over traditional medications. The segment benefits from technological innovations such as smaller device footprints, rechargeable systems, and MRI-safe designs. Strong clinical adoption in developed countries and well-established reimbursement frameworks also contribute to high market penetration. Additionally, implantable devices often include remote monitoring capabilities, allowing physicians to track therapy in real-time. The segment’s reliability, long-term efficacy, and growing patient preference for minimally invasive solutions make it the dominant type in the market.

Non-Invasive Electroceuticals are expected to witness the fastest CAGR during 2026–2033, driven by growing preference for wearable and home-based therapies. Devices such as TENS, non-invasive vagus nerve stimulators, and wearable neuromodulators offer pain relief, mood regulation, and neurological therapy without the need for surgery. The segment is supported by the rise of telemedicine and digital health integration, enabling remote monitoring and therapy customization. Convenience, ease of use, and lower costs compared to implantable options drive adoption among individual users and outpatient settings. Increasing awareness of drug-free therapeutic alternatives and expanding consumer acceptance in emerging economies further accelerate growth. Continuous product innovation, such as smartphone-controlled stimulators and AI-enabled adaptive therapy, enhances the appeal of non-invasive electroceuticals.

- By End User

On the basis of end user, the market is segmented into hospitals, clinics, research institutes, and individual users. Hospitals dominated the market in 2025, accounting for the largest revenue share due to the high adoption of advanced electroceutical therapies for chronic pain, cardiac, and neurological disorders. Hospitals benefit from well-equipped surgical facilities, access to skilled medical professionals, and integration with electronic health record systems, enabling seamless implementation of implantable and non-invasive devices. The demand is also driven by large patient volumes, institutional procurement practices, and established reimbursement mechanisms. Hospitals often serve as primary centers for clinical trials and regulatory approvals, facilitating rapid adoption of innovative devices. Strategic partnerships with device manufacturers allow hospitals to access the latest technologies, further consolidating their dominance in the market.

Individual Users are expected to witness the fastest growth during 2026–2033, driven by rising awareness and adoption of wearable and home-based bioelectronic therapies. Non-invasive electroceuticals such as TENS and wearable neuromodulation devices empower patients to manage pain, stress, and neurological symptoms at home. Increasing integration with mobile apps, AI-enabled monitoring, and telehealth platforms makes therapy management easier and more personalized. Affordability improvements, growing consumer health awareness, and access to online healthcare resources are encouraging self-managed therapy adoption. Expansion of e-commerce channels and homecare services further accelerates the uptake of devices among individual users.

Electroceuticals/Bioelectric Medicine Market Regional Analysis

- North America dominated the electroceuticals/bioelectric medicine market with the largest revenue share of 40% in 2025, characterized by early adoption of advanced medical technologies, high healthcare expenditure, and a strong presence of key industry players

- Patients and healthcare providers in the region highly value the efficacy, precision, and minimally invasive nature of implantable and non-invasive bioelectronic devices for managing chronic pain, neurological, and cardiovascular disorders

- This widespread adoption is further supported by robust R&D investments, favorable reimbursement policies, early regulatory approvals, and a well-established network of hospitals and clinics, making North America a key market for both hospitals and individual users seeking advanced electroceutical therapies

U.S. Electroceuticals/Bioelectric Medicine Market Insight

The U.S. electroceuticals market captured the largest revenue share of 42% in 2025, driven by advanced healthcare infrastructure, early adoption of cutting-edge medical devices, and rising prevalence of chronic conditions such as cardiac, neurological, and musculoskeletal disorders. Patients and healthcare providers are increasingly prioritizing minimally invasive, non-drug therapies for pain management, cardiac care, and neurological treatment. Strong R&D investments, favorable reimbursement policies, and a large network of hospitals and specialty clinics further propel market growth. Moreover, the integration of bioelectronic devices with telemedicine, mobile health applications, and remote monitoring systems is significantly contributing to market expansion.

Europe Electroceuticals/Bioelectric Medicine Market Insight

The Europe electroceuticals market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising patient awareness, stringent healthcare regulations, and increasing demand for innovative therapeutic solutions. Urbanization, high healthcare expenditure, and adoption of advanced technologies are fostering growth across hospitals, clinics, and research institutes. European patients and providers value personalized, non-drug therapies that improve clinical outcomes and quality of life. Countries such as Germany, France, and the U.K. are witnessing growth in both implantable and non-invasive electroceutical adoption due to strong clinical infrastructure and reimbursement support.

U.K. Electroceuticals/Bioelectric Medicine Market Insight

The U.K. electroceuticals market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the increasing trend of personalized healthcare and demand for advanced pain management, cardiac, and neurological therapies. Concerns regarding chronic disease management and patient quality of life are encouraging healthcare providers and patients to adopt bioelectronic solutions. The U.K.’s strong clinical research network, digital health adoption, and well-developed e-health infrastructure are expected to continue stimulating market growth.

Germany Electroceuticals/Bioelectric Medicine Market Insight

The Germany electroceuticals market is expected to expand at a considerable CAGR during the forecast period, fueled by rising patient awareness, technological innovation, and a focus on precision, minimally invasive therapies. Germany’s advanced healthcare infrastructure, high expenditure on medical devices, and emphasis on clinical research promote the adoption of implantable and wearable electroceutical solutions. Integration with digital health platforms and real-time monitoring systems is becoming increasingly prevalent, with patients and providers favoring effective, reliable, and customizable therapies.

Asia-Pacific Electroceuticals/Bioelectric Medicine Market Insight

The Asia-Pacific electroceuticals market is poised to grow at the fastest CAGR of 25% during 2026–2033, driven by increasing prevalence of chronic diseases, rising healthcare infrastructure investment, and growing patient awareness in countries such as China, Japan, and India. The adoption of implantable and non-invasive devices is supported by government initiatives promoting digital health, smart hospitals, and homecare solutions. Additionally, as APAC becomes a hub for medical device manufacturing, affordability and accessibility of bioelectronic therapies are increasing, expanding the consumer base.

Japan Electroceuticals/Bioelectric Medicine Market Insight

The Japan electroceuticals market is gaining momentum due to the country’s advanced healthcare ecosystem, aging population, and high adoption of medical technology. Patients and healthcare providers emphasize non-drug therapies for pain management, cardiac rhythm disorders, and neurological conditions. Integration of wearable and implantable devices with telehealth and digital monitoring solutions is accelerating growth. Japan’s high-tech culture and rapid urbanization are further driving demand for convenient, effective, and patient-friendly bioelectronic therapies across hospitals and individual users.

India Electroceuticals/Bioelectric Medicine Market Insight

The India electroceuticals market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to rising prevalence of chronic diseases, expanding middle-class population, and rapid adoption of advanced medical technologies. Hospitals, clinics, and homecare users are increasingly adopting implantable and non-invasive devices for pain management, neurological disorders, and cardiac therapies. Government initiatives for smart healthcare infrastructure, growing awareness of non-drug therapies, and availability of cost-effective devices from domestic and international manufacturers are key factors propelling the market in India.

Electroceuticals/Bioelectric Medicine Market Share

The Electroceuticals/Bioelectric Medicine industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Boston Scientific Corporation (U.S.)

- Abbott (U.S.)

- LivaNova PLC (U.K.)

- Cochlear Limited (Australia)

- Neuronetics, Inc. (U.S.)

- electroCore, Inc. (U.S.)

- Galvani Bioelectronics (U.K.)

- Biotronik SE & Co. KG (Germany)

- Sonova Group (Switzerland)

- Axonics Modulation Technologies, Inc. (U.S.)

- NeuroPace, Inc. (U.S.)

- NeuroSigma, Inc. (U.S.)

- BioControl Medical Ltd. (Israel)

- Aleva Neurotherapeutics SA (Switzerland)

- MED EL Elektromedizinische Geräte GmbH (Austria)

- Nurotron Biotechnology Co., Ltd. (U.S.)

- tVNS Technologies GmbH (Germany)

- Pulsetto (Lithuania)

- BioWave Corporation (U.S.)

What are the Recent Developments in Global Electroceuticals/Bioelectric Medicine Market?

- In April 2025, Bay Area patients in the U.S. became some of the first routine recipients of adaptive deep‑brain stimulation (aDBS) for Parkinson’s disease following FDA approval, with several patients experiencing significant symptom improvements and reduced medication reliance

- In April 2025, the ExaStim neuromodulation device received CE Mark approval in the European Union for treating spinal cord injuries, representing a major regulatory milestone that clears the way for clinical use across Europe and underscores progress in bioelectronic therapies beyond traditional pain and neurological indications. This approval also highlights the translation of academic innovations into scalable medical solutions

- In March 2025, ElectroCore launched its next‑generation gammaCore Sapphire device a non‑invasive vagus nerve stimulator aimed at migraine and cluster headache patients, featuring enhanced stimulation precision, smartphone connectivity, and improved battery performance, reflecting strong industry focus on portable, home‑use bioelectronic solutions

- In February 2025, Medtronic received U.S. FDA approval for BrainSense™ Adaptive Deep Brain Stimulation (aDBS) technology for Parkinson’s disease patients, marking a breakthrough in personalized neurostimulation that automatically adjusts electrical therapy based on individual brain activity in real time. This adaptive system enhances symptom control and precision over conventional DBS

- In February 2023, LivaNova launched the SenTiva DUO implantable pulse generator an advanced vagus nerve stimulation (VNS) device for drug‑resistant epilepsy patients, featuring a dual‑pin design that expands therapy options for those with legacy VNS systems

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.