Global Friction Reducers Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

2.28 Billion

USD

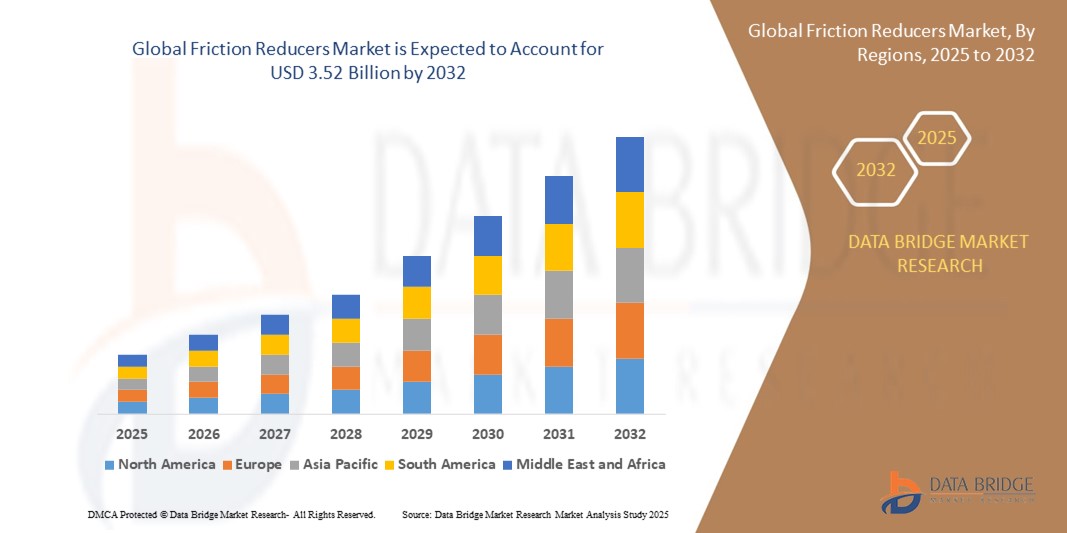

3.52 Billion

2024

2032

USD

2.28 Billion

USD

3.52 Billion

2024

2032

| 2025 –2032 | |

| USD 2.28 Billion | |

| USD 3.52 Billion | |

| % | |

|

글로벌 마찰 감소기 시장 세분화, 유형별(합성 마찰 감소기 및 유기 마찰 감소기, 조합 마찰 감소기), 입자 크기(나노 스케일 마찰 감소기, 마이크로 스케일 마찰 감소기 및 거시 스케일 마찰 감소기), 이온 전하(음이온 마찰 감소기, 양이온 마찰 감소기, 비이온 마찰 감소기 및 양쪽성 마찰 감소기), 기능(저항 감소 및 마모 감소), 농도(저농도 및 고농도), 형태(액체 마찰 감소기, 분말 마찰 감소기 및 에멀젼 마찰 감소기), 응용 분야(수압 파쇄, 드릴링 유체, 자극 유체, 시멘팅 유체, 우물 자극 및 향상된 석유 회수(EOR)), 유통 채널(직접 판매, 유통업체/도매업체, 온라인 소매업체 및 기타) - 산업 동향 및 2032년까지의 예측

마찰 감소기 시장 규모

- 글로벌 마찰 감소제 시장 규모는 2024년에 22억 8천만 달러 로 평가되었으며 예측 기간 동안 5.6%의 CAGR 로 2032년까지 35억 2천만 달러에 도달할 것으로 예상됩니다 .

- 시장 성장은 주로 향상된 석유 및 가스 회수 기술에 대한 수요 증가와 주요 생산 지역에서의 첨단 시추 기술 도입 증가에 의해 촉진됩니다.

- 석유 및 가스 산업에서 에너지 소비와 운영 비용 절감에 대한 강조가 커지면서 마찰 감소제 사용이 늘어나고 있으며, 이로 인해 전반적인 효율성과 생산성이 향상되고 있습니다.

마찰 감소기 시장 분석

- 마찰 감소제 시장은 석유 및 가스 산업처럼 효율적인 유체 이동이 필요한 산업의 수요 증가로 꾸준히 성장하고 있습니다. 기업들은 제품 성능을 개선하고 더욱 엄격한 산업 표준을 충족하기 위한 첨단 제형 개발에 주력하고 있습니다.

- 마찰 감소 기술의 혁신은 다양한 유체와의 호환성을 향상시켜 적용 범위를 확대하고 있습니다. 이는 제조업체들이 경쟁력을 유지하고 변화하는 시장 요구에 부응하기 위해 연구 개발에 투자하도록 장려하고 있습니다.

- 북미는 2024년 38.5%의 가장 큰 매출 점유율로 마찰 감소제 시장을 장악했으며, 이는 광범위한 석유 및 가스 탐사 활동과 고급 수압 파쇄 기술의 채택 증가에 힘입은 것입니다.

- 아시아 태평양 지역은 석유 및 가스 탐사 활동의 급속한 확장, 수압 파쇄 작업 증가, 에너지 개발을 촉진하는 정부 지원 이니셔티브에 힘입어 글로벌 마찰 감소제 시장에서 가장 높은 성장률을 보일 것으로 예상됩니다.

- 합성 부문은 2024년에 52.5%의 가장 큰 매출 점유율로 시장을 지배했으며, 이는 높은 효율성과 수압 파쇄 작업에서의 광범위한 사용에 기인합니다.

보고서 범위 및 마찰 감소기 시장 세분화

|

속성 |

마찰 감소기 주요 시장 통찰력 |

|

다루는 세그먼트 |

|

|

포함 국가 |

북아메리카

유럽

아시아 태평양

중동 및 아프리카

남아메리카

|

|

주요 시장 참여자 |

|

|

시장 기회 |

|

|

부가가치 데이터 정보 세트 |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Friction Reducers Market Trends

“Growing Adoption of Environmentally Friendly Friction Reducers”

- There is an increasing trend toward the development and use of eco-friendly friction reducers, driven by stricter environmental regulations and sustainability goals across industries

- Manufacturers are investing in bio-based and biodegradable friction reducers to reduce the environmental impact of hydraulic fracturing and other industrial processes

- For instance, companies such as Halliburton and Baker Hughes have introduced greener formulations that minimize toxic residues and improve biodegradability, catering to eco-conscious clients

- The shift towards sustainable products also helps companies comply with regional regulations, such as those in North America and Europe, where environmental standards are more stringent

- This trend not only supports environmental protection but also opens new market opportunities, encouraging further innovation in greener friction reducer technologies and applications

Friction Reducers Market Dynamics

Driver

“Increasing Demand for Efficient Oil and Gas Extraction Techniques”

- The growing demand for enhanced oil and gas extraction efficiency is driving the friction reducers market, as these additives reduce friction between fracturing fluid and the wellbore, enabling higher flow rates and lower pumping pressures

- This improved efficiency results in faster drilling times, reduced energy consumption, and lower operational costs, which is essential for maximizing profitability in energy production

- Oil and gas companies are increasingly investing in advanced technologies to optimize production from existing reservoirs and unlock unconventional resources

- For instance, ExxonMobil’s expansion in the Permian Basin where friction reducers support high-volume hydraulic fracturing operations

- The rising use of horizontal drilling and multi-stage fracturing techniques, especially in shale-rich regions such as the U.S. Marcellus Shale, further boosts demand for friction reducers to handle complex well designs and higher fluid volumes

- Friction reducers enhance fluid mobility and hydrocarbon recovery rates, making them indispensable in modern drilling operations aiming to meet growing global energy needs while controlling costs and improving sustainability

Restraint/Challenge

“Environmental Concerns and Regulatory Challenges Related to Friction Reducers”

- 마찰 감소제 시장의 중요한 과제 중 하나는 마찰 감소제를 포함한 수압 파쇄 유체와 관련된 환경 문제입니다. 마찰 감소제는 종종 환경에 지속될 수 있고 토양 및 수질을 위험에 빠뜨릴 수 있는 합성 폴리머를 포함합니다.

- 친환경 제형의 발전에도 불구하고 파쇄 폐수의 적절한 폐기 및 처리에는 여전히 많은 비용이 들고 복잡하며, 엄격한 규정으로 인해 석유 및 가스 회사의 규정 준수 비용이 증가하고 있습니다.

- 민감한 지역에서 화학 물질 사용에 대한 규제 제한으로 인해 일부 마찰 감소제 유형의 적용이 제한되어 시장 접근성과 성장 잠재력에 영향을 미칠 수 있습니다.

- 예를 들어 펜실베이니아와 영국과 같은 지역에서 물 오염 우려에 대한 시위와 같은 대중의 반대는 업계가 더 안전하고 덜 해로운 제품을 개발하도록 압력을 가중시킵니다.

- 제조업체는 효율성을 유지하면서 생태적 영향을 줄이는 마찰 감소제 혁신을 위한 연구에 투자하여 고성능 요구 사항과 환경적 지속 가능성 간의 균형을 맞춰야 하는 과제에 직면해 있으며, 이를 달성하지 못하면 프로젝트 지연, 도입 감소 및 운영 비용 증가의 위험이 있습니다.

마찰 감소기 시장 범위

시장은 유형, 입자 크기, 이온 전하, 기능, 농도, 형태, 응용 분야 및 유통 채널을 기준으로 세분화됩니다.

- 유형별

마찰 감소제 시장은 유형별로 합성 마찰 감소제, 유기 마찰 감소제, 그리고 복합 마찰 감소제로 구분됩니다. 합성 마찰 감소제는 높은 효율성과 수압파쇄 작업에서의 광범위한 사용으로 인해 2024년 52.5%의 가장 큰 매출 점유율을 기록하며 시장을 장악했습니다.

유기 마찰 감소제는 환경에 대한 우려가 커지면서 2025년부터 2032년까지 가장 빠른 성장을 보일 것으로 예상되며, 복합 마찰 감소제는 다양한 응용 분야에서 균형 잡힌 성능과 다용성 덕분에 2025년부터 2032년까지 가장 빠른 속도로 성장할 것으로 예상됩니다.

- 입자 크기별

입자 크기에 따라 시장은 나노, 마이크로, 매크로 마찰 저감기로 구분됩니다. 나노 부문은 향상된 항력 감소 특성과 유체 안정성에 힘입어 2024년 45.3%의 매출 점유율을 기록하며 가장 큰 매출 점유율을 기록했습니다. 마이크로 마찰 저감기는 비용 효율적인 성능에 대한 꾸준한 수요를 유지하고 있습니다.

거시적 마찰 저감제는 더 큰 입자를 필요로 하는 특정 시추 환경에 적합하기 때문에 2025년부터 2032년까지 가장 빠른 성장을 보일 것으로 예상됩니다. 까다로운 지층에서도 효과적으로 작동할 수 있어 복잡한 유정을 관리하는 운영자들에게 점점 더 선호되고 있습니다.

- 이온 충전으로

이온 전하를 기준으로 시장은 음이온성, 양이온성, 비이온성, 그리고 양쪽성 마찰 감소제로 구분됩니다. 음이온성 마찰 감소제는 2024년 48.7%의 시장 점유율로 시장을 주도했으며, 고염도 유체와의 호환성으로 선호되었습니다.

양쪽성 마찰 저감제는 다양한 pH 수준과 저류층 조건에 대한 적응성을 바탕으로 2025년부터 2032년까지 가장 빠른 성장을 보일 것으로 예상됩니다. 이러한 다재다능함은 다양한 지역 및 유체 화학 분야에 적용 가능하여 시장 채택률을 확대할 것입니다.

- 기능별로

기능성을 기준으로 시장은 항력 감소 및 마모 감소 부문으로 구분됩니다. 항력 감소 마찰 감소제는 유체 마찰을 줄여 수압파쇄 효율을 향상시켜 2024년 시장 매출 점유율 61.2%로 가장 큰 비중을 차지했습니다.

마모 감소 마찰 저감 장치는 2025년부터 2032년까지 장비 보호 및 유지보수 비용 절감을 위해 가장 빠른 성장을 보일 것으로 예상되며, 예측 기간 동안 강력한 성장을 보일 것으로 예상됩니다. 마모 감소 마찰 저감 장치는 장비 수명 연장 및 가동 중단 최소화에 기여하며, 이는 운영 효율성에 매우 중요합니다.

- 농도에 따라

시장은 농도 기준으로 저농도 마찰 감소제와 고농도 마찰 감소제로 구분됩니다. 고농도 마찰 감소제는 2024년 시장 점유율 57.8%로 더 큰 비중을 차지했으며, 장기간의 파쇄 단계에서 탁월한 항력 감소 효과를 보였습니다.

저농도 유형은 비용 효율성과 특정 운영 시나리오에서의 화학물질 사용량 감소로 인해 2025년부터 2032년까지 가장 빠른 성장을 보일 것으로 예상됩니다. 따라서 성능 저하 없이 지속 가능한 솔루션을 추구하는 운영자에게 매력적인 선택입니다.

- 형태로

마찰 감소제 시장은 형태에 따라 액상, 분말, 에멀전형으로 구분됩니다. 2024년에는 액상 마찰 감소제가 54.9%의 시장 점유율을 차지하며 압도적인 우위를 차지했는데, 이는 취급 용이성과 유체 내 빠른 용해성이 장점으로 평가받았기 때문입니다.

에멀젼 마찰 저감제는 파쇄 유체에 안정적으로 분산되기 때문에 2025년부터 2032년까지 가장 빠른 성장을 보일 것으로 예상됩니다. 다양한 유체 시스템과의 호환성이 향상되어 전반적인 파쇄 효율이 향상되고 운영 위험이 감소합니다.

- 응용 프로그램별

시장은 응용 분야별로 수압파쇄, 시추 유체, 시추 자극 유체, 시추 시추 유체, 시추 자극 유체, 그리고 석유 회수 증진으로 구분됩니다. 수압파쇄는 비전통 자원 채굴의 증가에 힘입어 2024년 전체 매출의 62.7%를 차지하며 가장 큰 비중을 차지했습니다.

석유 회수 증진은 운영자들이 저류층 생산량 극대화에 집중함에 따라 2025년부터 2032년까지 가장 빠른 성장을 보일 것으로 예상됩니다. 에너지 안보에 대한 수요 증가로 마찰 저감제에 크게 의존하는 첨단 회수 기술의 도입이 촉진되고 있습니다.

- 유통 채널별

유통 채널을 기준으로 시장은 직접 판매, 유통업체/도매업체, 온라인 소매업체 등으로 세분화됩니다. 직접 판매는 주요 유전 기업과의 탄탄한 제조업체 관계 덕분에 2024년 시장 점유율 50.3%로 압도적인 우위를 점했습니다.

Distributors and online retailers is expected to witness the fastest growth from 2025 to 2032, catering to wider geographic and smaller-scale customers. Their expanding reach improves accessibility of friction reducers to remote or emerging markets, driving overall market expansion.

Friction Reducers Market Regional Analysis

- North America dominated the friction reducers market with the largest revenue share of 38.5% in 2024, driven by extensive oil and gas exploration activities and the increasing adoption of advanced hydraulic fracturing technologies

- The region’s focus on improving extraction efficiency and reducing environmental impact encourages the use of high-performance friction reducers in shale formations

- Supportive regulatory frameworks and investment in upstream technologies further bolster market growth, with major players emphasizing sustainable formulations and optimized chemical usage

U.S. Friction Reducers Market Insight

The U.S. friction reducers market captured the largest revenue share of 82% in North America in 2024, propelled by the rapid growth of unconventional oil and gas production. Operators prioritize friction reducers that enhance fluid flow and reduce operational costs in hydraulic fracturing. The rising demand for eco-friendly and cost-effective chemical additives, combined with stringent environmental regulations, drives innovation in friction reducer formulations. In addition, the presence of leading chemical manufacturers and ongoing drilling activities contribute significantly to market expansion.

Europe Friction Reducers Market Insight

The Europe friction reducers market is expected to witness the fastest growth from 2025 to 2032, supported by increasing offshore drilling projects and the shift toward environmentally compliant fracturing fluids. Rising emphasis on reducing chemical waste and improving operational efficiency propels the adoption of friction reducers. The market also benefits from government policies promoting cleaner technologies and the increasing use of bio-based and synthetic friction reducers in conventional and unconventional wells.

U.K. Friction Reducers Market Insight

The U.K. friction reducers market is expected to witness the fastest growth from 2025 to 2032, driven by offshore oil and gas exploration in the North Sea and rising investments in well stimulation techniques. The focus on reducing environmental footprint through optimized chemical additives encourages the use of advanced friction reducers. Regulatory compliance and operational cost management remain key factors influencing market demand in the region.

Germany Friction Reducers Market Insight

The Germany friction reducers market is expected to witness the fastest growth from 2025 to 2032, fuelled by growing investments in upstream oil and gas infrastructure and increasing demand for efficient fracturing fluids. Germany’s strong chemical industry base supports innovation in friction reducer technologies, including biodegradable and environmentally friendly formulations. In addition, rising awareness of ecological impacts and regulatory pressures drive the adoption of safer and high-performance friction reducers.

Asia-Pacific Friction Reducers Market Insight

The Asia-Pacific friction reducers market is expected to witness the fastest growth from 2025 to 2032, led by expanding oil and gas exploration in China, India, and Southeast Asia. Increasing government support for unconventional resource development and rising energy demand boost market growth. The region benefits from growing local manufacturing capabilities and cost-effective chemical solutions, facilitating wider adoption across onshore and offshore drilling operations.

China Friction Reducers Market Insight

The China’s friction reducers market is growing rapidly due to intensified shale gas development and the adoption of advanced hydraulic fracturing technologies. The government’s push for energy security and cleaner extraction methods supports the demand for efficient friction reducers. Moreover, collaborations between international and local chemical manufacturers help improve product quality and availability, driving market expansion.

Japan Friction Reducers Market Insight

The Japan friction reducers market is expected to witness the fastest growth from 2025 to 2032, driven by the country’s emphasis on enhancing oil and gas production efficiency amid limited domestic reserves. Japan’s advanced technological landscape and focus on innovation support the adoption of high-performance friction reducers in well stimulation and hydraulic fracturing operations. In addition, increasing investments in offshore energy projects and strict environmental regulations encourage the use of environmentally friendly friction reducer formulations. The aging energy infrastructure also fuels demand for chemicals that improve operational safety and equipment longevity.

Friction Reducers Market Share

The Friction Reducers industry is primarily led by well-established companies, including:

- CLARIANT (Switzerland)

- BASF SE (Germany)

- Croda International Plc (U.K.)

- Evonik Industries AG (Germany)

- The Lubrizol Corporation (U.S.)

- Dow (U.S.)

- SLB (U.S.)

- Halliburton (U.S.)

- Baker Hughes Company (U.S.)

- SNF (France)

- Kemira (Finland)

- Ashland (U.S.)

- Innospec (U.S.)

- Evonik Industries AG (Germany)

- Akzo Nobel N.V. (Netherlands)

- Solvay (Belgium)

- GEO (U.S.)

- Stepan Company (U.S.)

- Nouryon (Netherlands)

- Cabot Corporation (U.S.)

- SELECT WATER SOLUTIONS (U.S.)

- R.T. Vanderbilt Holding Company, Inc. (U.K.)

- Italmatch Chemicals (Italy)

- PfP Industries (U.S.)

- Aquaness Chemicals (U.A.E.)

- Di-Corp, Inc. (Canada)

- Rocanda (U.S.)

- Trican (Canada)

- Aisling Chem (Canada)

- Shrieve (U.S.)

- Rishabh Metals & Chemicals (India)

- ChemEOR, Inc. (U.S.)

- CONDAT (France)

- TETRA Technologies, Inc. (U.S.)

Latest Developments in Global Friction Reducers Market

- In May 2022, Innospec Oilfield Services launched AquaBourne, a new water-based friction reducer designed without oil or surfactants. This formulation uses a water carrier fully compatible with fresh, flowback, or high TDS produced water, resulting in a clear, colorless solution with very low suspended solids. This innovation offers improved environmental compatibility and enhanced performance in hydraulic fracturing operations, supporting cleaner and more efficient extraction processes in the oil and gas market

- In June 2021, Kemira completed the installation of advanced production units for emulsion polymers and biobased acrylamide monomers at its Mobile, Alabama manufacturing facility. These emulsion polymers are mainly targeted for water-intensive applications such as friction reducers used in the oil and gas sector. This development strengthens Kemira’s production capacity and supports the supply of high-quality, sustainable chemicals, contributing to the growing demand for efficient and eco-friendly friction reduction solutions

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.