Global High Barrier Packaging Films Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

27.32 Billion

USD

49.83 Billion

2024

2032

USD

27.32 Billion

USD

49.83 Billion

2024

2032

| 2025 –2032 | |

| USD 27.32 Billion | |

| USD 49.83 Billion | |

| % | |

|

글로벌 고차단성 포장 필름 시장 세분화, 유형별(금속화 필름, 투명 필름, 유기 코팅 필름, 무기 산화물 코팅 필름 등), 재료별(플라스틱, 알루미늄, 산화물 등), 포장 유형별(파우치, 백, 뚜껑, 수축 필름, 라미네이트 튜브 등), 최종 사용자별(식품 및 음료, 제약, 전자 기기, 의료 기기, 농업, 화학 제품 등) - 산업 동향 및 2032년까지의 전망

고차단성 포장 필름 시장 규모

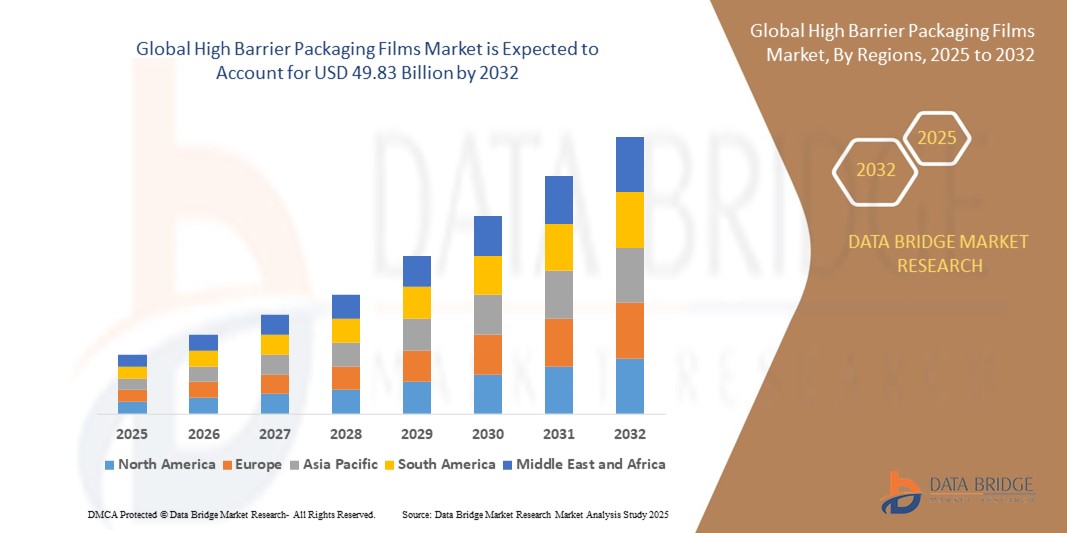

- 글로벌 고차단성 포장 필름 시장 규모는 2024년에 273억 2천만 달러 로 평가되었으며, 예측 기간 동안 7.8%의 CAGR 로 2032년까지 498억 3천만 달러에 도달할 것으로 예상됩니다 .

- 시장 성장은 주로 식품, 음료 및 제약품 포장 분야에서 보관 수명 연장 및 제품 보호에 대한 수요 증가에 의해 주도되고 있으며, 고차단 필름은 산소, 습기 및 기타 환경 요인에 대한 뛰어난 저항성을 제공합니다.

- 또한, 특히 개발도상국을 중심으로 지속 가능하고 가벼운 포장 솔루션으로의 전환이 증가함에 따라 고차단성 포장 필름의 채택이 더욱 가속화되고 있습니다. 다층 공압출 및 바이오 기반 필름의 기술 발전 또한 다양한 산업 분야에서 시장 확대를 뒷받침하고 있습니다.

고차단성 포장 필름 시장 분석

- 고차단성 포장 필름은 습기, 산소, 자외선 및 오염 물질에 대한 뛰어난 내성을 갖추고 있어 유통기한을 효과적으로 연장하고 제품 품질을 유지하므로 식품 및 음료, 제약, 개인 관리 등 다양한 산업에서 중요한 역할을 합니다.

- 편의식품, 의약품 안정성, 그리고 가볍고 지속 가능한 포장재에 대한 수요 증가로 고차단성 필름 도입이 가속화되고 있습니다. 바이오 기반 다층 구조와 재활용 가능한 필름을 포함한 기술 혁신은 가치 사슬 전반에 걸쳐 더욱 지속 가능한 솔루션으로의 전환을 촉진하고 있습니다.

- 북미 지역은 2025년 기준 약 41.5%의 매출 점유율로 세계 고차단성 포장 필름 시장을 장악하고 있습니다. 이는 포장재 소비 증가, 엄격한 식품 및 의약품 안전 규제 기준, 그리고 성숙된 포장 산업의 성장에 힘입은 것입니다. 미국은 Amcor, Sealed Air, Berry Global 등 주요 기업들의 지속 가능한 배리어 기술 투자 확대와 더불어 뛰어난 R&D 역량을 바탕으로 이 지역을 선도하고 있습니다.

- 아시아 태평양 지역은 급속한 산업화, 포장 및 가공 식품 수요 증가, 그리고 정부의 현지 제조 촉진 정책에 힘입어 가장 빠르게 성장하는 지역으로 예상됩니다. 중국, 인도, 인도네시아 등 주요 국가에서는 소비재 포장재 시장이 크게 성장하고 있으며, 이는 비용 효율적이고 내구성이 뛰어난 차단 필름의 수요를 견인하고 있습니다.

- 제조업체들이 산화, 부패, 향 손실을 방지하는 포장재를 우선시함에 따라, 식음료 부문은 2025년에 약 45.8%의 시장 점유율을 기록하며 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. 진공 파우치, 레토르트 백, MAP(치환가스 포장)와 같은 포장재는 선진국과 신흥국 모두에서 높은 수요를 보이고 있습니다.

보고서 범위 및 고차단성 포장 필름 시장 세분화

|

속성 |

고차단성 포장 필름 주요 시장 통찰력 |

|

다루는 세그먼트 |

|

|

포함 국가 |

북아메리카

유럽

아시아 태평양

중동 및 아프리카

남아메리카

|

|

주요 시장 참여자 |

|

|

시장 기회 |

|

|

부가가치 데이터 정보 세트 |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework |

High Barrier Packaging Films Market Trends

“Strategic Technological Advancements and Supply Chain Integration”

- A key and accelerating trend in the global high barrier packaging films market is the integration of advanced multilayer film manufacturing technologies, including nano-coating, co-extrusion, and vacuum metallization, to improve barrier performance while maintaining film flexibility, transparency, and recyclability. These technologies enhance shelf life and product safety in food, pharmaceutical, and electronic packaging

- For instance, in April 2024, Amcor introduced a recyclable high-barrier film using its proprietary AmLite technology, combining high oxygen and moisture resistance with recyclability under existing infrastructure, supporting both sustainability and performance goals for global FMCG clients

- Leading packaging companies are pursuing vertical integration strategies—from raw polymer processing to finished film conversion. In January 2024, Constantia Flexibles acquired a specialty PET film facility in Eastern Europe, allowing greater control over resin sourcing, coating, and lamination, while reducing supply chain disruptions and lead times for European customers

- The demand for eco-friendly and compliant packaging is driving the adoption of bio-based and mono-material barrier films. In March 2024, Toray Plastics (America) launched a new line of compostable high-barrier films targeting organic food packaging and personal care products, aligning with growing regulatory frameworks like the EU Packaging and Packaging Waste Regulation (PPWR)

- Digital supply chain technologies such as IoT-enabled packaging lines and AI-based quality control systems are being widely implemented. In June 2023, MULTIVAC deployed smart packaging equipment with predictive maintenance and defect detection capabilities, improving production efficiency and traceability across global operations

- Recycling and circular economy initiatives are emerging as strategic pillars. In 2024, Sonoco Products Company began scaling a chemical recycling pilot to recover high-barrier film components—such as EVOH and nylon—from multilayer structures, aiming to reduce landfill waste and improve material recovery for high-performance reuse

- These trends underscore a broader transformation in the high barrier packaging films market, where technological innovation, environmental stewardship, and integrated operations are critical to competitiveness. Industry leaders are investing in closed-loop systems, sustainable material innovation, and digital automation to future-proof their packaging strategies and meet rising global demand for safe, efficient, and eco-friendly solutions

High Barrier Packaging Films Market Dynamics

Driver

“Growing Demand for Product Protection, Shelf Life Extension, and Sustainable Packaging”

- The increasing need to protect perishable products—especially in the food & beverage, pharmaceutical, and electronics sectors—is a major driver for high barrier packaging films. These films offer superior resistance to oxygen, moisture, UV light, and contaminants, extending shelf life and reducing spoilage

- For instance, in February 2024, Sealed Air Corporation expanded its portfolio of multilayer vacuum barrier films for fresh meat and cheese packaging, citing rising consumer demand for longer shelf life and food safety assurance in both retail and e-commerce distribution

- The global push for sustainable packaging, particularly recyclable and lightweight alternatives to rigid containers, has led to accelerated adoption of high barrier flexible films. These films reduce packaging weight, lower carbon footprint, and support circular economy goals

- Emerging applications in nutraceuticals, dairy, and healthcare packaging are further driving market demand, especially in fast-growing regions such as Asia-Pacific and Latin America, where urbanization and packaged food consumption are rising

- In addition, advancements in film engineering, including mono-material and bio-based structures, are enabling manufacturers to meet both barrier performance and recyclability targets. Companies like Amcor and Constantia Flexibles are at the forefront of this innovation trend

- Overall, the dual need for performance and sustainability, along with stricter global packaging regulations (e.g., EU Packaging and Packaging Waste Regulation, FDA guidelines), continues to propel the high barrier packaging films market forward

Restraint/Challenge

“Material Complexity, Cost Pressures, and Recycling Limitations”

- A primary challenge in the high barrier packaging films market is the complexity of multilayer material structures, often combining polymers like EVOH, PA, PET, and aluminum. While these combinations enhance barrier properties, they significantly complicate recyclability and waste management

- For instances, multi-material flexible films are difficult to separate and reprocess, and many recycling systems lack the capability to handle them, leading to increased landfill waste and regulatory scrutiny

- Raw material price volatility, especially for specialty polymers and metalized components, poses cost pressure on manufacturers. In 2023–2024, supply chain disruptions and inflationary trends led to rising prices of PET, PA, and aluminum, affecting profit margins

- Regulatory challenges are intensifying, with the EU’s Green Deal, EPR (Extended Producer Responsibility) frameworks, and plastic taxation policies placing pressure on manufacturers to redesign packaging formats while managing costs and compliance.

- The capital expenditure required for high-tech barrier film production lines, including multilayer co-extrusion and vacuum metallization systems, is substantial. This limits entry for smaller players and makes capacity expansion expensive in developing regions

- In addition, supply chain integration remains uneven, with limited transparency across raw material sourcing, film conversion, and end-of-life disposal. The lack of closed-loop systems further undermines circularity goals

- To address these restraints, industry leaders are investing in design-for-recycling initiatives, AI-based sorting technologies, and mono-material barrier films that maintain performance while enabling recovery within standard recycling streams

High Barrier Packaging Films Market Scope

The market is segmented on the basis of type, material, packaging type, and end user.

By Type

On the basis of type, the High Barrier Packaging Films market is segmented into Metalized Films, Clear Films, Organic Coating Films, Inorganic Oxide Coating Films, and Others. The Metalized Films segment dominates the largest market revenue share in 2025, driven by its excellent barrier properties against oxygen, moisture, and light, making it highly suitable for food and pharmaceutical packaging applications

Metalized films are preferred for their cost-effectiveness and ability to provide extended shelf life, especially in snack foods, confectionery, and medical products. The market also witnesses strong demand for Clear Films due to their transparency and printability, which enhance product visibility and branding on retail shelves

• By Material

On the basis of material, the High Barrier Packaging Films market is segmented into Plastic, Aluminum, Oxides, and Others. The Plastic segment holds the largest revenue share in 2025, owing to its versatility, lightweight nature, and compatibility with various coating technologies. Plastics such as PET and PE provide excellent mechanical strength and flexibility, making them ideal for flexible packaging solution

Aluminum films are widely utilized for their superior barrier against moisture and oxygen, especially in pharmaceutical and electronic device packaging, where maximum protection is critical

• By Packaging Type

포장 유형별로 시장은 파우치, 백, 뚜껑, 수축 필름, 라미네이트 튜브, 기타로 구분됩니다. 파우치 부문은 편의성, 재밀봉성, 그리고 제품 신선도 유지 능력 덕분에 2025년 시장 매출 점유율이 가장 높을 것으로 예상됩니다. 파우치는 휴대성과 지속 가능성을 중시하는 소비자들의 선호도가 높아짐에 따라 식품, 음료, 제약 산업 전반에 걸쳐 광범위하게 사용되고 있습니다.

뚜껑과 수축 필름도 밀봉 기술의 혁신과 부패하기 쉬운 물품에 대한 향상된 차단 성능에 힘입어 급속히 도입되고 있습니다.

• 최종 사용자별

고차단성 포장 필름 시장은 최종 사용자 기준으로 식품 및 음료, 제약, 전자 기기, 의료 기기, 농업, 화학, 기타 등으로 세분화됩니다. 식품 부문은 2025년 가장 큰 매출 점유율을 기록하며 시장을 선도할 것으로 예상되는데, 이는 유통기한 연장과 부패 방지 기능이 필요한 포장 편의식품, 스낵, 즉석식품에 대한 수요 증가에 힘입은 것입니다.

의약품 부문 또한 약물 안전성과 효능 보장을 위한 엄격한 습기 및 산소 차단성 규제 요건에 힘입어 꾸준히 성장하고 있습니다. 전자기기 및 의료기기와 같은 신흥 산업에서는 부품 보호 및 멸균 포장을 위해 고차단 필름을 점점 더 많이 채택하고 있습니다.

고차단성 포장 필름 시장 지역 분석

- 북미 지역은 세계 고차단성 포장 필름 시장을 장악하고 있으며, 2025년에는 약 41.5%의 매출 점유율로 가장 큰 비중을 차지할 것으로 예상됩니다. 이는 주요 포장 제조업체들의 입지와 식음료, 제약, 의료기기 부문의 강력한 수요 덕분입니다. 북미 지역은 첨단 제조 인프라, 제품 안전에 대한 높은 소비자 인식, 그리고 우수한 차단성을 요구하는 엄격한 규제 기준 등의 이점을 누리고 있습니다.

- 북미 지역에서 지속 가능하고 재활용 가능한 포장 솔루션에 대한 수요가 증가함에 따라 제조업체들은 플라스틱 폐기물 감소 및 생산자 책임 확대에 대한 연방 및 주 차원 정책에 맞춰 단일 소재 고차단 필름 및 생물 기반 코팅을 개발해야 합니다.

- 또한, 전자상거래 확대와 포장 제품의 편의성과 신선도에 대한 소비자 선호도 변화로 인해 유연한 고차단 필름의 도입이 가속화되고 있습니다. 이 지역의 탄탄한 물류 네트워크와 공급망 통합은 효율적인 생산 및 유통을 더욱 뒷받침합니다.

일본 고차단성 포장 필름 시장 분석

일본 고차단성 포장 필름 시장은 일본의 첨단 포장 기술, 엄격한 품질 기준, 그리고 프리미엄 식품, 제약, 전자 제품 포장에 대한 높은 수요에 힘입어 성장하고 있습니다. 일본 제조업체들은 다층 필름 구조, 유기 및 무기 코팅, 그리고 뛰어난 차단 성능, 내습성, 내구성을 요구하는 틈새 시장 수요를 충족하는 지속 가능한 솔루션 혁신에 집중하고 있습니다. 또한, 친환경 포장재와 순환 경제 원칙을 중시하는 일본 정부의 정책은 재활용 및 생분해가 가능한 고차단성 필름에 대한 수요를 증가시키고 있습니다.

중국 고차단성 포장 필름 시장 분석

중국 고차단성 포장 필름 시장은 중국의 방대한 포장 산업, 식품 및 제약 생산 증가, 그리고 전자상거래 포장 수요의 급속한 성장에 힘입어 아시아 태평양 지역을 선도할 것으로 예상됩니다. 중국의 대규모 제조 역량과 금속화 및 코팅 필름 기술에 대한 투자는 소비재, 의료, 전자제품 등 다양한 분야에서 고차단성 포장 필름 도입을 촉진하고 있습니다. 주요 국내 생산업체들은 자동화 및 고급 품질 관리를 통해 생산 라인을 업그레이드하여 국내 및 수출용 고성능, 비용 효율적인 포장 필름에 대한 수요 증가를 충족하고 있습니다.

북미 고차단성 포장 필름 시장 통찰력

북미 고차단성 포장 필름 시장은 편의성 포장, 의료기기, 지속 가능한 포장 솔루션에 대한 소비자 수요 증가로 강력한 성장세를 보이고 있습니다. 미국은 다층 공압출, 유기 및 무기 산화물 코팅, 재활용 가능한 단일 소재 차단 필름 개발 분야의 기술 발전을 통해 이 지역을 선도하고 있습니다. Sealed Air, Sonoco, Amcor와 같은 주요 업체들은 친환경 포장에 대한 규제 요건과 소비자 선호도의 변화에 대응하기 위해 R&D 및 생산 시설 확장에 막대한 투자를 하고 있습니다.

미국 고차단성 포장 필름 시장 분석

미국 고차단성 포장 필름 시장은 2025년 북미에서 가장 큰 점유율을 차지할 것으로 예상되는데, 이는 성숙된 포장 산업과 식품, 제약, 의료 분야의 강력한 수요에 힘입은 것입니다. 제품 안전 및 환경 지속가능성에 대한 규제 강화는 산소, 수분, 향료 차단 기능이 뛰어난 차단 필름 혁신을 촉진하고 있습니다. 필름 압출 기술 및 코팅 공정 분야에서 미국이 선도적인 위치를 차지하고 있으며, 순환 포장 솔루션에 대한 투자도 증가하고 있어 공급망의 회복탄력성과 제품 차별화가 강화되고 있습니다.

유럽 고차단성 포장 필름 시장 통찰력

The Europe High Barrier Packaging Films market is projected to grow steadily, driven by strict regulatory frameworks such as the EU’s Green Deal and packaging waste directives. Countries including Germany, France, and the Netherlands are spearheading adoption of recyclable multilayer films, bio-based coatings, and metalized films to reduce environmental impact while maintaining high barrier properties. Collaboration between chemical companies, packaging converters, and brand owners is fostering innovation in sustainable packaging solutions, especially for food and pharmaceuticals

U.K. High Barrier Packaging Films Market Insight

The U.K. High Barrier Packaging Films market is gaining momentum due to rising demand in the food service, pharmaceutical, and cosmetic packaging sectors. Manufacturers are increasingly adopting organic coating films and clear barrier films for their superior aesthetics and performance. Government policies aimed at reducing plastic waste and promoting reusable packaging systems are encouraging investment in recyclable barrier film technologies. Industry initiatives on green chemistry and packaging eco-design are also driving growth in high-performance, low-impact films

Germany High Barrier Packaging Films Market Insight

The Germany High Barrier Packaging Films market is expanding significantly, supported by the country’s robust automotive, food, and pharmaceutical industries. German manufacturers emphasize development of inorganic oxide coating films and metalized films that offer exceptional barrier efficiency and durability under strict EU regulatory standards. Investment in sustainable packaging solutions and advanced film processing technologies is rising to meet the demand for recyclable and lightweight packaging. Germany’s focus on precision engineering and quality assurance continues to position it as a key player in the European market

High Barrier Packaging Films Market Share

The high barrier packaging films industry is primarily led by well-established companies, including:

- Advanced Converting Works (U.S.)

- Constantia Flexibles (Austria)

- HPM GLOBAL INC. (U.S.)

- FLAIR Flexible Packaging Corporation (U.S.)

- ClearBags (U.S.)

- Perlen Packaging (Switzerland)

- OLIVER (U.S.)

- Celplast Metallized Products (Canada)

- Toray Plastics (America), Inc. (U.S.)

- ISOFlex Packaging (U.S.)

- KREHALON (Netherlands)

- MULTIVAC (Germany)

- BERNHARDT Packaging & Process (U.S.)

- Sonoco Products Company (U.S.)

- Sealed Air (U.S.)

- WINPAL LTD. (Taiwan)

- Schur Flexibles Holding GesmbH (Austria)

- Amcor Ltd. (Australia)

Latest Developments in Global High Barrier Packaging Films Market

- In April 2024, UFlex launched a series of new high barrier packaging films, designed to provide superior product protection and extended shelf life while enhancing sustainability. These advanced packaging solutions cater to the growing demand for high-performance, eco-friendly materials in the flexible packaging industry

- In April 2024, Inteplast BOPP Films partnered with VerdaFresh to create flexible high barrier films that will enhance food shelf life while minimizing package waste. Inteplast's high-moisture barrier biaxially oriented polypropylene (BOPP) films will be blended with oxygen protective coating technology from VerdaFresh

- In March 2024, Toppan announced the launch of a new high barrier packaging film that combines recyclability with superior barrier performance, enhancing sustainability in the packaging industry

- In December 2023, Amcor introduced a new recyclable high barrier packaging film, designed to deliver exceptional product protection while supporting sustainability efforts

- In October 2022, Toppan expanded its GL Barrier range with a mono-material PE barrier designed to package liquid products in a durable, sterile, and easy-to-recycle material. Aiming to meet "growing demand" in the European and North American markets, the company claims that vapor deposition has previously posed a challenge with PE packaging and that its new barrier supersedes existing designs of its kind

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.