Global Polyethylene Terephthalate Pet Foam Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

434.78 Million

USD

747.03 Million

2025

2033

USD

434.78 Million

USD

747.03 Million

2025

2033

| 2026 –2033 | |

| USD 434.78 Million | |

| USD 747.03 Million | |

| % | |

|

Global Polyethylene Terephthalate (PET) Foam Market Segmentation, By Raw Material (Virgin Polyethylene Terephthalate (PET) and Recycled Polyethylene Terephthalate (PET)), Target (Low Density Polyethylene Terephthalate (PET) Foam and High- Polyethylene Terephthalate (PET) Foam Density), End Use Industry (Wind Energy, Automotive, Aerospace and Defense, Marine, Building and Construction, Packaging, and Others) - Industry Trends and Forecast to 2033

Polyethylene Terephthalate (PET) Foam Market Size

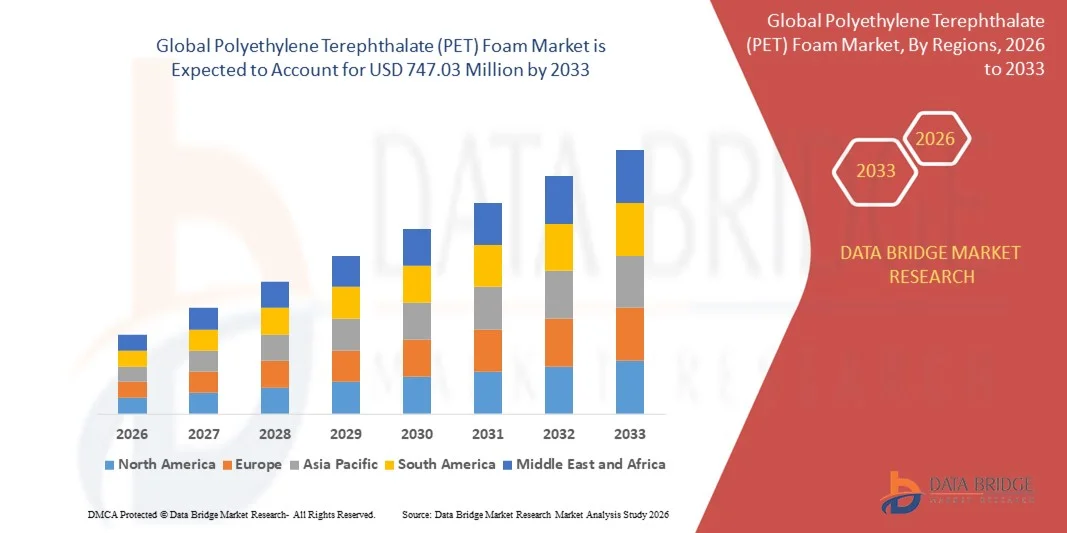

- The global Polyethylene Terephthalate (PET) foam market size was valued at USD 434.78 million in 2025 and is expected to reach USD 747.03 million by 2033, at a CAGR of 7.00% during the forecast period

- The market growth is largely driven by the rising adoption of lightweight and high-performance core materials across wind energy, automotive, marine, and construction applications, where PET foam offers an optimal balance of strength, durability, and recyclability

- Furthermore, increasing focus on sustainability, weight reduction, and cost-efficient composite solutions is positioning PET foam as a preferred alternative to traditional core materials, accelerating its penetration across structural and insulation applications and significantly supporting overall market growth

Polyethylene Terephthalate (PET) Foam Market Analysis

- Polyethylene Terephthalate (PET) foam, used as a structural core material in sandwich composites, has become a critical component in modern wind turbine blades, automotive structures, marine vessels, and building materials due to its high strength-to-weight ratio, fatigue resistance, and moisture stability

- The growing demand for Polyethylene Terephthalate (PET) foam foam is primarily fueled by the rapid expansion of renewable energy projects, increasing emphasis on lightweight materials for fuel efficiency and emission reduction, and the rising adoption of recyclable and environmentally compliant materials across industrial applications

- Asia-Pacific dominated the Polyethylene Terephthalate (PET) foam market with a share of around 35% in 2025, due to rapid expansion of wind energy installations, growing automotive manufacturing, and increasing adoption of lightweight composite materials

- North America is expected to be the fastest growing region in the Polyethylene Terephthalate (PET) foam market during the forecast period due to rising wind energy capacity additions, increasing use of lightweight materials in automotive and aerospace sectors, and strong emphasis on recyclable composites

- Virgin Polyethylene Terephthalate (PET) segment dominated the market with a market share of 62.5% in 2025, due to its superior mechanical strength, consistent quality, and reliable performance across high-load structural applications. Manufacturers prefer virgin Polyethylene Terephthalate (PET) foam for wind energy, aerospace, and marine uses due to its predictable behavior under stress and long-term durability. Its higher purity ensures better bonding with resins and composites, which is critical for safety-sensitive applications. The availability of standardized grades further supports its dominance in large-scale industrial projects

Report Scope and Polyethylene Terephthalate (PET) Foam Market Segmentation

|

Attributes |

Polyethylene Terephthalate (PET) Foam Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Polyethylene Terephthalate (PET) Foam Market Trends

Increasing use of Recyclable and Sustainable PET Foam Core Materials

- A significant trend in the Polyethylene Terephthalate (PET) foam market is the increasing adoption of recyclable and sustainable core materials across composite-intensive industries, driven by growing environmental regulations and corporate sustainability targets. PET foam is gaining preference over traditional core materials due to its recyclability, lower environmental impact, and ability to meet structural performance requirements in demanding applications

- For instance, Gurit Holding AG has expanded its recyclable PET foam product portfolio for wind energy and marine applications, supporting circular economy objectives while maintaining mechanical strength and durability. Such initiatives are reinforcing PET foam’s position as a sustainable alternative in large-scale composite structures

- The wind energy sector is increasingly integrating PET foam cores in turbine blades as manufacturers seek materials that support lifecycle sustainability without compromising fatigue resistance. This trend is strengthening PET foam adoption in both onshore and offshore wind projects

- Automotive manufacturers are also incorporating recyclable PET foam into lightweight vehicle components to support emission reduction and end-of-life recyclability goals. This is contributing to broader acceptance of PET foam within transportation applications

- Building and construction activities are witnessing rising use of PET foam for insulation and structural panels, where sustainability certifications and energy efficiency standards are becoming decisive purchasing factors. This is expanding PET foam usage in green building projects

- Overall, the growing emphasis on sustainability and recyclability across industries is reinforcing PET foam’s role as a future-ready core material, supporting long-term market expansion

Polyethylene Terephthalate (PET) Foam Market Dynamics

Driver

Rising Demand for Lightweight and High-Strength Composite Structures

- The increasing demand for lightweight yet high-strength composite materials across wind energy, automotive, aerospace, and marine sectors is a primary driver for the PET foam market. PET foam offers an optimal balance of mechanical strength, weight reduction, and durability, making it suitable for load-bearing sandwich structures

- For instance, Toray Industries, Inc. utilizes advanced PET foam solutions in composite applications where weight reduction and structural performance are critical, particularly in aerospace and transportation-related uses. Such adoption highlights the growing reliance on PET foam in performance-driven environments

- In the automotive sector, manufacturers are adopting PET foam to achieve lightweighting objectives that improve fuel efficiency and electric vehicle range. PET foam’s compatibility with composite manufacturing processes enhances its appeal for structural and semi-structural components

- Marine and aerospace industries are also driving demand as PET foam provides resistance to moisture, fatigue, and harsh operating conditions. These performance advantages are strengthening its adoption in high-value applications

- The continued shift toward lightweight composite engineering across industries is reinforcing this driver, positioning PET foam as a critical material supporting modern structural design requirements

Restraint/Challenge

High Processing and Initial Manufacturing Costs

- The PET foam market faces challenges related to high initial processing and manufacturing costs, particularly when compared with conventional core materials. Advanced processing requirements and specialized composite integration increase overall production expenses for manufacturers and end users

- For instance, BASF SE highlights that producing high-performance PET foam grades requires controlled processing conditions and precise material formulation, which adds to capital and operational costs. These cost factors can limit adoption in price-sensitive applications

- Manufacturing PET foam for structural uses involves energy-intensive processes and strict quality control standards to ensure consistent density and mechanical performance. These requirements raise production complexity and cost structures

- Small and mid-sized manufacturers may face difficulties scaling PET foam production due to the need for specialized equipment and skilled labor. This can constrain supply and affect market penetration in emerging regions

- As a result, high initial costs remain a key challenge, requiring manufacturers to focus on process optimization, economies of scale, and technological advancements to improve cost competitiveness while maintaining product performance

Polyethylene Terephthalate (PET) Foam Market Scope

The market is segmented on the basis of raw material, target density, and end use industry.

- By Raw Material

On the basis of raw material, the Polyethylene Terephthalate (PET) foam market is segmented into virgin Polyethylene Terephthalate (PET) and recycled Polyethylene Terephthalate (PET). The virgin Polyethylene Terephthalate (PET) segment dominated the market with the largest revenue share of 62.5% in 2025, driven by its superior mechanical strength, consistent quality, and reliable performance across high-load structural applications. Manufacturers prefer virgin Polyethylene Terephthalate (PET) foam for wind energy, aerospace, and marine uses due to its predictable behavior under stress and long-term durability. Its higher purity ensures better bonding with resins and composites, which is critical for safety-sensitive applications. The availability of standardized grades further supports its dominance in large-scale industrial projects.

The recycled Polyethylene Terephthalate (PET) segment is expected to register the fastest growth from 2026 to 2033, supported by increasing sustainability mandates and circular economy initiatives across manufacturing industries. Growing emphasis on reducing carbon footprints is encouraging end users to adopt recycled Polyethylene Terephthalate (PET) foam without compromising structural integrity. Advancements in recycling technologies are improving material consistency, making recycled Polyethylene Terephthalate (PET) suitable for automotive, construction, and packaging applications. Cost advantages over virgin material and strong regulatory support are accelerating adoption across emerging and developed markets.

- By Target

On the basis of target density, the Polyethylene Terephthalate (PET) foam market is segmented into low-density Polyethylene Terephthalate (PET) foam and high-density Polyethylene Terephthalate (PET) foam. The high-density Polyethylene Terephthalate (PET) foam segment accounted for the dominant revenue share in 2025, driven by its high compressive strength, excellent fatigue resistance, and suitability for load-bearing structures. This segment is widely used in wind turbine blades, marine hulls, and aerospace components where structural stability and long service life are essential. Its resistance to moisture and chemicals further enhances performance in harsh operating environments. Strong demand from renewable energy and defense sectors continues to reinforce its market leadership.

The low-density Polyethylene Terephthalate (PET) foam segment is projected to witness the fastest growth during the forecast period, fueled by rising demand for lightweight materials in automotive interiors, building insulation, and packaging. Low-density Polyethylene Terephthalate (PET) foam offers weight reduction benefits while maintaining adequate thermal and acoustic insulation properties. Its ease of processing and cost efficiency make it attractive for high-volume applications. Increasing focus on energy-efficient buildings and lightweight vehicle design is supporting rapid expansion of this segment.

- By End Use Industry

On the basis of end use industry, the Polyethylene Terephthalate (PET) foam market is segmented into wind energy, automotive, aerospace and defense, marine, building and construction, packaging, and others. The wind energy segment dominated the market in 2025, driven by the extensive use of Polyethylene Terephthalate (PET) foam as a core material in wind turbine blades. Polyethylene Terephthalate (PET) foam provides high strength-to-weight ratio, fatigue resistance, and recyclability, which are essential for large and durable turbine structures. Rising investments in onshore and offshore wind projects globally are sustaining strong demand. Its compatibility with automated manufacturing processes further supports widespread adoption in this segment.

The automotive segment is anticipated to grow at the fastest rate from 2026 to 2033, supported by increasing demand for lightweight, fuel-efficient, and electric vehicles. Polyethylene Terephthalate (PET) foam is gaining traction in automotive structural components, interiors, and battery enclosures due to its impact resistance and thermal stability. Automakers are increasingly using Polyethylene Terephthalate (PET) foam to meet emission reduction targets and improve vehicle range. Continuous innovation in foam processing and design flexibility is accelerating its penetration in the automotive industry.

Polyethylene Terephthalate (PET) Foam Market Regional Analysis

- Asia-Pacific dominated the Polyethylene Terephthalate (PET) foam market with the largest revenue share of around 35% in 2025, driven by rapid expansion of wind energy installations, growing automotive manufacturing, and increasing adoption of lightweight composite materials

- The region’s strong manufacturing base, availability of cost-efficient raw materials, and rising investments in renewable energy and infrastructure projects are accelerating PET foam demand

- Supportive government policies, expanding composite manufacturing capacity, and rapid industrialization across developing economies are boosting consumption of PET foam in structural and insulation applications

China Polyethylene Terephthalate (PET) Foam Market Insight

China held the largest share in the Asia-Pacific Polyethylene Terephthalate (PET) foam market in 2025, supported by its dominance in wind turbine manufacturing, large-scale construction activity, and extensive composite material production capabilities. The country’s strong focus on renewable energy expansion and lightweight materials for transportation is driving sustained demand. In addition, well-developed supply chains and domestic production capacity are reinforcing China’s leadership position.

India Polyethylene Terephthalate (PET) Foam Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, fueled by rapid growth in wind energy projects, rising automotive production, and increasing use of lightweight materials in construction. Government initiatives supporting renewable energy capacity expansion and infrastructure development are strengthening Polyethylene Terephthalate (PET) foam adoption. Growing investments in domestic composite manufacturing are further contributing to strong market momentum.

Europe Polyethylene Terephthalate (PET) Foam Market Insight

The Europe Polyethylene Terephthalate (PET) foam market is growing steadily, driven by strict sustainability regulations, high adoption of recyclable core materials, and strong demand from wind energy and automotive sectors. The region emphasizes lightweight, high-performance, and environmentally compliant materials in structural applications. Increasing investments in offshore wind projects and electric vehicles are supporting long-term market growth.

Germany Polyethylene Terephthalate (PET) Foam Market Insight

Germany’s Polyethylene Terephthalate (PET) foam market is supported by its advanced automotive industry, strong wind energy infrastructure, and leadership in composite engineering. The country’s focus on lightweight vehicle design, energy efficiency, and recyclable materials is driving Polyethylene Terephthalate (PET) foam usage. Strong R&D capabilities and industrial collaboration further enhance adoption across multiple end-use industries.

U.K. Polyethylene Terephthalate (PET) Foam Market Insight

The U.K. market benefits from growing offshore wind energy projects, rising demand for sustainable construction materials, and increasing adoption of advanced composites. Focus on renewable energy targets and lightweight structural materials is strengthening Polyethylene Terephthalate (PET) foam demand. Investments in marine and wind energy applications continue to support market expansion.

North America Polyethylene Terephthalate (PET) Foam Market Insight

North America is projected to grow at the fastest CAGR from 2026 to 2033, driven by rising wind energy capacity additions, increasing use of lightweight materials in automotive and aerospace sectors, and strong emphasis on recyclable composites. Growing investments in renewable energy infrastructure and advanced manufacturing technologies are key growth drivers.

U.S. Polyethylene Terephthalate (PET) Foam Market Insight

The U.S. accounted for the largest share in the North America Polyethylene Terephthalate (PET) foam market in 2025, supported by significant wind energy installations, strong aerospace and automotive industries, and high demand for structural core materials. Focus on sustainability, lightweighting, and domestic composite manufacturing is accelerating Polyethylene Terephthalate (PET) foam adoption. Presence of established manufacturers and advanced production capabilities further strengthen the U.S.’s leading position.

Polyethylene Terephthalate (PET) Foam Market Share

The Polyethylene Terephthalate (PET) foam industry is primarily led by well-established companies, including:

- JSP Corporation (Japan)

- Armacell International S.A. (Luxembourg)

- Dow Inc. (U.S.)

- Zotefoams Plc (U.K.)

- Sealed Air Corporation (U.S.)

- Carbon-Core Corp. (U.S.)

- BASF SE (Germany)

- INOAC Corporation (Japan)

- Wisconsin Foam Products (U.S.)

- Huntsman International LLC (U.S.)

- Palziv Ltd. (Israel)

- Trecolan GmbH (Germany)

- Pregis LLC (U.S.)

- Mitsui Chemicals America, Inc. (U.S.)

- Kaneka Corporation (Japan)

- Toray Industries, Inc. (Japan)

- Gurit Holding AG (Switzerland)

Latest Developments in Global Polyethylene Terephthalate (PET) Foam Market

- In October 2025, 3M Company initiated a collaborative development program with leading automotive manufacturers to engineer advanced PET foam solutions aimed at improving vehicle performance and fuel efficiency. This collaboration is strengthening innovation pipelines in the PET foam market by accelerating the adoption of lightweight core materials in next-generation vehicles. The partnership enhances 3M’s market position by aligning its material expertise with OEM requirements, while also expanding the application scope of PET foam within the automotive sector

- In September 2025, SABIC introduced a new portfolio of sustainable PET foam products tailored for environmentally conscious industries. This development reflects the growing market shift toward recyclable and low-carbon materials, reinforcing PET foam’s role as a sustainable alternative to traditional core materials. By addressing sustainability-driven demand, SABIC is enhancing its competitive differentiation and supporting wider adoption of PET foam across construction, transportation, and industrial applications

- In August 2025, Toray Industries Inc announced a major investment in a new PET foam production facility to expand its manufacturing capacity. This move directly supports rising global demand, particularly from aerospace applications where lightweight and high-strength materials are critical. The expansion improves supply chain resilience and positions Toray to capture a larger share of high-value PET foam applications

- In June 2025, Armacell expanded its PET foam product range with high-performance grades designed for wind energy and marine applications. This development strengthens the market by addressing the need for durable, fatigue-resistant core materials in large composite structures. The expanded portfolio enables Armacell to deepen its presence in renewable energy projects and high-growth marine segments

- In April 2025, Gurit Holding AG enhanced its PET foam manufacturing capabilities by upgrading production lines to improve efficiency and product consistency. This strategic initiative supports increasing demand from wind energy and transportation sectors while reducing production costs. The upgrade reinforces Gurit’s ability to deliver high-quality PET foam at scale, contributing to stronger competitiveness in a rapidly expanding market

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.