Global Tank Insulation Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

3.84 Billion

USD

10.30 Billion

2024

2032

USD

3.84 Billion

USD

10.30 Billion

2024

2032

| 2025 –2032 | |

| USD 3.84 Billion | |

| USD 10.30 Billion | |

| % | |

|

세계 탱크 절연제 시장 세그먼트, 유형 (저장과 수송)에 의하여, 물자 유형 (Expanded Polystyrene (EPS), Rockwool, 셀룰러 유리, 섬유유리, 탄성 거품, 폴리우레탄 (PU), 및 다른 사람), 온도 유형 (뜨거운 절연제 및 찬 절연제), 탱크 유형 (전형 탱크, 수평한 탱크, 조정 탱크 및 거치된 탱크), 탱크 끝 (Parabolic 접시 및 평평한), 끝 사용자 (오일 & 가스, 에너지 절약 및 물 정화, 2032를 위해)

Tank Insulation Market Size

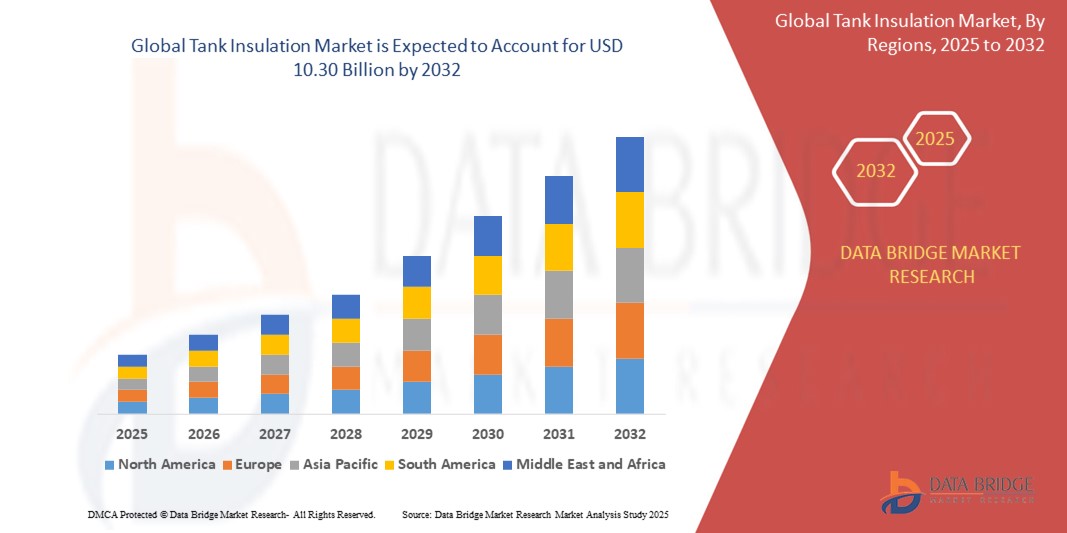

- The global tank insulation market size was valued atUSD 3.84 billion in 2024and is expected to reachUSD 10.30 billion by 2032, at aCAGR of 5.25%during the forecast period

- This growth is driven by factors such as the increasing demand for energy-efficient insulation solutions in industries such as oil & gas, energy, and chemicals

Tank Insulation Market Analysis

- Tank insulation is defined as the process in which different chemicals and materials are applied to the inside of tank and also to the surface, to maintain the temperature throughout its usage period

- Tank insulation is done to preserve the temperature inside the tank in order to minimize the heat loss

- North America is expected to dominate the tank insulations market due to its advanced infrastructure and continuous focus on technological innovations in insulation materials

- Asia-Pacific is expected to be the fastest growing region in the tank insulation market during the forecast period due to rapid industrialization and urbanization, which is driving significant demand for tank insulation solutions

- Rockwool and polyurethane (PU) segment is expected to dominate the market with a market share of 31.5% due to their high thermal insulation properties and versatility. These materials are widely used in industries such as oil and gas, chemicals, and energy due to their excellent ability to maintain the required temperature levels while ensuring energy efficiency

Report Scope and Tank Insulation Market Segmentation

|

Attributes |

Tank Insulation Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Tank Insulation Market Trends

“Advancements in Sustainable Insulation Materials”

- In recent years, there has been a significant trend towards the use of sustainable and eco-friendly insulation materials in tank insulation. Industries are increasingly focused on minimizing their environmental footprint and improving energy efficiency. Manufacturers are developing insulation solutions that are not only thermally efficient but also made from renewable or recyclable materials

- For Instance, Rockwool International A/S, which has been at the forefront of developing insulation products made from sustainable materials. Their mineral wool insulation solutions are designed to be highly energy-efficient while being recyclable, aligning with growing global sustainability goals

- The transition to a circular economy is influencing the tank insulation market. Companies are investing in materials that can be reused or recycled, reducing waste and fostering sustainability in the supply chain

- Many governments around the world are implementing stricter regulations related to energy efficiency in industrial sectors. This is pushing companies to adopt more advanced and sustainable insulation solutions that reduce energy consumption and improve temperature control for storage tanks

- Manufacturers of tank insulation are increasingly obtaining environmental certifications for their products, ensuring compliance with international standards such as LEED (Leadership in Energy and Environmental Design) and BREEAM (Building Research Establishment Environmental Assessment Method)

Tank Insulation Market Dynamics

Driver

“Increasing Energy Efficiency Demands”

- The primary driver of growth in the global tank insulation market is the increasing demand for energy efficiency. Insulated tanks help reduce energy loss during the storage and transportation of liquids, gases, and chemicals by maintaining temperature control. This is especially critical in sectors such as oil and gas, chemicals, and food processing, where temperature-sensitive materials are involved

- As the global energy crisis intensifies, industries are under pressure to optimize their energy consumption. Tank insulation solutions help minimize energy waste by maintaining the desired temperature, leading to significant energy savings

- Governments are implementing stricter regulations regarding energy use, particularly in high-consumption industries.

- For instance, the European Union's Energy Efficiency Directive mandates the reduction of energy use across industries, pushing companies to adopt solutions such as tank insulation to comply with these regulations

- Tank insulation reduces the need for additional energy resources by preventing heat loss or gain. This directly results in lower energy bills for companies that adopt these solutions, making it a cost-effective measure

- The oil and gas industry is one of the largest consumers of insulated tanks. With the growing focus on reducing operational costs, the demand for advanced insulation solutions is surging to ensure that thermal energy is not wasted during storage and transportation processes

Opportunity

“Growth in Emerging Markets”

- Emerging markets, particularly in regions such as Asia-Pacific, Latin America, and the Middle East, offer significant growth opportunities for the global tank insulation market. As these regions industrialize at a rapid pace, there is an increasing demand for tank insulation solutions across various sectors, including chemicals, oil and gas, and pharmaceuticals

- Countries in the Middle East and Asia are investing heavily in infrastructure development, including energy production and petrochemical plants. This creates opportunities for the tank insulation market, as these facilities require highly efficient thermal insulation for storage tanks to optimize energy use

- Governments in emerging markets are encouraging foreign investments and providing incentives for companies to adopt energy-efficient technologies. These incentives are a key opportunity for manufacturers of tank insulation solutions to expand their reach in these regions

- As renewable energy projects such as wind, solar, and bioenergy grow in emerging markets, there is an increasing need for efficient storage solutions. Insulated tanks are crucial in ensuring that energy storage systems function optimally, which presents an opportunity for insulation companies to cater to the renewable energy sector

- The growing food processing and pharmaceutical industries in emerging markets create new opportunities for tank insulation providers, as these industries require insulated storage tanks for temperature-sensitive materials

Restraint/Challenge

“High Initial Investment Costs”

- The installation of advanced tank insulation systems, particularly those made from high-performance materials, involves significant upfront capital investment. For many small and medium-sized enterprises (SMEs), this high initial cost can be a major barrier to adopting tank insulation solutions

- The return on investment (ROI) for insulated tanks, although positive in terms of energy savings, can take several years to materialize. This long payback period discourages many companies from making the initial investment, especially in industries with tighter profit margins

- Retrofitting existing tanks with new insulation systems can be complex and costly. Many companies face challenges when integrating insulation into their pre-existing infrastructure, leading to higher operational costs during the installation process

- The prices of raw materials used in insulation, such as fiberglass, mineral wool, and polyurethane, can fluctuate significantly. This price volatility can increase the overall cost of insulation systems and create uncertainty in the market

- In some developing regions, the awareness of the benefits of tank insulation is still low. Companies may not fully realize the long-term energy savings and operational efficiency gains that can be achieved through proper insulation, which limits market growth in these areas

Tank Insulation Market Scope

The market is segmented on the basis type, material type, temperature type, tank type, tank ends, and end-user.

|

Segmentation |

Sub-Segmentation |

|

By Type |

|

|

By Material Type |

|

|

By Temperature Type |

|

|

By Tank Type |

|

|

By Tank Ends |

|

|

By End-User |

|

In 2025, the rockwool and polyurethane (PU) is projected to dominate the market with a largest share in material type segment

The rockwool and polyurethane (PU) segment is expected to dominate the tank insulation market with the largest share of 31.5% in 2025 due to their high thermal insulation properties and versatility. These materials are widely used in industries such as oil and gas, chemicals, and energy due to their excellent ability to maintain the required temperature levels while ensuring energy efficiency.

The hot insulation is expected to account for the largest share during the forecast period in temperature market

In 2025, the got insulation segment is expected to dominate the market with the largest market share of 51.31% due to preventing heat loss and protecting equipment, ensuring that industrial processes remain within safe temperature limits. Hot insulation solutions help companies save on heating costs and reduce energy consumption, making this a highly demanded segment across various industries.

Tank Insulation Market Regional Analysis

“North America Holds the Largest Share in the Tank Insulation Market”

- North America remains a dominant player in the global tank insulation market due to its advanced infrastructure and continuous focus on technological innovations in insulation materials. The region is home to a highly developed chemical, oil & gas, and energy sector, all of which rely heavily on insulated tanks for storage and transportation of liquids and gases

- Stringent regulations related to energy efficiency and safety standards have prompted companies in North America to adopt tank insulation solutions. These regulations not only ensure operational safety but also contribute to energy conservation and reduction of carbon footprints

- The oil & gas sector, especially in the U.S. and Canada, is a major consumer of tank insulation, where insulated tanks are essential to maintaining temperature control for both storage and transportation. The sector's growth, driven by the need for storage tanks for crude oil and natural gas, further bolsters market demand

- North America has well-established manufacturing capabilities for tank insulation materials such as polyurethane, polystyrene, and fiberglass, enabling a strong supply chain to meet local and international demand

- Increasing investments in energy efficiency across various industries, especially in power generation and industrial manufacturing, have further driven the demand for insulated tanks in this region, making North America a market leader

“Asia-Pacific is Projected to Register the Highest CAGR in the Tank Insulation Market”

- The Asia-Pacific region, particularly countries such as China, India, and South Korea, is experiencing rapid industrialization and urbanization, which is driving significant demand for tank insulation solutions. Industries such as chemicals, oil & gas, and food processing are growing rapidly, creating a high need for insulated tanks

- Several governments in APAC are focusing on enhancing industrial infrastructure, which includes the construction of storage facilities and refineries that require tank insulation solutions. Government incentives for energy-efficient solutions and compliance with environmental regulations are contributing to the region's growth in this market

- As energy consumption in the region rises, particularly in emerging economies such as India and China, there is a growing need to store and transport energy-efficient materials, requiring the installation of insulated tanks to maintain temperature stability and minimize energy losses

- APAC is seeing significant growth in its petrochemical industry, with major projects coming online, particularly in countries such as China and India. These industries are among the biggest consumers of tank insulation systems to store chemicals at safe temperatures

- The adoption of more affordable and locally manufactured insulation materials, such as fiberglass and mineral wool, is driving market growth in the APAC region. The lower costs of production and raw materials have made insulated tank solutions more accessible to a larger number of companies in this region

Tank Insulation Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Commercial Thermal Solutions, Inc. (U.S.)

- Dow(U.S.)

- GILSULATE INTERNATIONAL, INC. (U.S.)

- ITW INSULATION SYSTEMS(U.S.)

- J.H. Ziegler GmbH(Germany)

- Knauf Insulation (U.S.)

- PolarClad Tank Insulation (U.S.)

- ARMACELL LLC (U.S.)

- Kingspan Group (Ireland)

- Synavax (U.S.)

- Johns Manville (U.S.)

- Mayes Coatings & Insulation, Inc. (U.S.)

- Thermacon (U.S.)

- Gulf Cool Therm Factory LTD (UAE)

- ROCKWOOL International A/S (Denmark)

- Cabot Corporation (U.S.)

- SPX Transformer Solutions Inc. (U.S.)

- DUNMORE (U.S.)

- T.F. Warren Group (U.S.)

- Saint-Gobain (France)

- Huntsman International LLC (U.S.)

- Corrosion Resistant Technologies, Inc. (U.S.)

- Röchling (Germany)

Latest Developments in Global Tank Insulation Market

- In May 2025, Rockwool International A/S Expands Product Line, the new products are designed with improved fire resistance and better thermal performance, catering to industries with stringent regulatory requirements

- In March 2025, Dow Launches New Polyurethane-Based Insulation, designed to enhance the performance and energy efficiency of tank insulation systems. The new product features improved thermal resistance properties and lower environmental impact due to the use of renewable materials

- In January 2025, Knauf Insulation Partners with Large Industrial Clients, to supply tank insulation materials for large-scale oil and gas refineries and chemical plants. The collaboration aims to enhance the energy efficiency of storage and transportation tanks used in these industries

- In December 2024, ITW Insulation Systems Launches Advanced Insulation Solutions for High-Temperature Applications, designed for hot tanks in the petrochemical industry. The products feature enhanced resistance to thermal stress and are designed to improve energy conservation in high-demand environments

- In September 2024, Johns Manville Introduces Recyclable Insulation Products, made from sustainable materials. These products are aimed at companies looking to reduce their environmental impact while maintaining high insulation performance

- In June 2024, Armacell LLC Expands Operations in Asia-Pacific, expanded its operations in the Asia-Pacific region by opening a new production facility in India. This facility will cater to the growing demand for tank insulation in industries such as oil & gas and chemicals

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

목차

TABLE OF CONTENTS GLOBAL TANK 소개

1 소개

1.1 글로벌 TANK 통합 시장 1.4 CURRENCY 및 1.5 LIMITATIONS 1.6 시장 COVERED

2 시장 세그먼트

MARKETS는 2.2 GEOGRAPHICAL SCOPE 2.3 년 STUDY 2.4 CURRENCY 및 PRICING 2.5 DBMR TRIPOD DATA VALIDATION 모델 2.6 기술 LIFE LINE CURVE 2.7 MULTIVARIATE MODELLING 2.8 주요 OPINION LEADERS와 PRIMARY INTERVIEWS 2.9 DBMR MARKET POSITION GRID 2.10 MARKET 적용 2.11 MARKET 2.11 MARKET 적용 2.11 MARKET 2.12 MARKET MARKET 2.12 MARKET MARKET MARKET MARKET MARKET MARKET MARKET 2.12 MARKET MARKET MARKET MARKET MARKET MARKET MARKET MARKET MARKET MARKET MARKET MARKET MARKET MARKET MARKET MARKET MARKET MARKET MARKET MARKET MARKET MARKET MARKET MARKET MARKET MARKET MARKET MARKET MARKET MARKET MARKET MARKET MARKET MARKET MARKET MARKET MARKET MARKET MARK

3 시장 전망

3.1 운전사

3.1.1 OIL & GAS 산업 3.1.2 GROWING DEMAND LNG 저장 및 운송 3.1.3 GROWING DEMAND 3.1.3 GROWING DEMAND OF TEMPERATURE CONTROLLED PACKAGING FOR PHARMACEUTICALS 3.1.4 GROWING DEMAND OF MICA SHEETS IN RMAL BARRIER

3.2 수익

3.2.1 가공 RAW 물자 가격 3.2.2 CHEMICAL STRUCTURE의 변화는 TANKS 3.2.4에 있는 MOLTEN 금속을 붙들기 위하여 물자의 3.2.3 UNAVAILABILITY OF PROFICIENT INSULATING 물자의 3.2.3 UNAVAILABILABILABILITY를 구멍을 뚫는 철과 강철 기업 3.2.4 FREQUENT에 있는 금속을 붙들기 위하여. 화학 공업에 있는 물자

3.3 기회

3.3.1 중국과 인도에 있는 석유 산업에 TANKS DUE를 위한 높은 DEMAND 3.3.2 GROWING DEMAND OF INSULATING MULTI-STORIES를 위한 물 TANKS에 있는 물자의 침투 3.3.3 증가하는 환경

3.4 도전

3.4.1 화재 및 폭발물은 TANK 3.4.2에 있는 격리 물자로 화학적 반응을 측정하기 위하여 매체의 위험합니다

4 독점 요약 5 프리미엄 INSIGHTS 6 산업 INSIGHTS 7 GLOBAL TANK INSULATION MARKET, 유형별

7.1 전망 7.2 저장 7.3 수송

8 물자 유형에 의하여 세계적인 탱크 절연제 시장,

8.1 OVERVIEW 8.2 우수한 성분 (EPS) 8.3 ROCKWOOL 8.4 셀룰러 글라스 8.5 FIBERGLASS 8.6 ELASTOMERIC FOAM 8.7 POLYURETHANE (PU) 8.8 기타

9 글로벌 탱크 기업 시장, TEMPERATURE

9.1 전망 9.2 뜨거운 절연제 9.3 찬 절연제

10 글로벌 TANK INSULATION MARKET, TANK TYPE에 의해

10.1 전망 10.2 VERTICAL 탱크 10.3 HORIZONTAL 탱크 10.4 FIXED 탱크 10.5 MOUNTED 탱크

11 글로벌 탱크 기업 시장, TANK ENDS

11.1 개요 11.2 PARABOLIC DISH 11.3 FLAT

12 글로벌 TANK INSULATION MARKET, END-USER에 의해

12.1 전망 12.2 기름과 가스

12.2.1 기름

12.2.1.1 CRUDE 오일 12.2.1.2 PETROCHEMICAL 12.2.1.3 기타 CRUDE 오일 DERIVATIVES

12.2.2 가스

12.2.2.1 NATURAL 가스 12.2.2.2 SYNTHETIC 가스

12.3 에너지 및 전력 12.4 화학 12.5 음식과 음료

12.5.1 음식 12.5.2 음료

12.5.2.1 ALCOHOLIC BEVERAGES 12.5.2.2 DAIRY 12.5.2.3 AERATED DRINKSRIN 12.5.2.4 JUICES 및 FLAVORED 워터 12.5.2.5 기타

12.6 물 정화

12.6.1 상업적인 건물 12.6.2 MUNICIPALITY 12.6.3 RESIDENTIAL 건물

12.7 WASTEWATER 보수

12.7.1 상업적인 건물 12.7.2 MUNICIPALITY 12.7.3 주거 건물

12.8 기타

13 GEOGRAPHY에 의한 GLOBAL TANK INSULATION MARKET

13.1 전망 13.2 북아메리카

13.2.1 미국 13.2.2 캐나다 13.2.3 멕시코

13.3 유로

13.3.1 독일 13.3.2 미국 13.3.3 이탈리아 13.3.4 프랑스 13.3.5 스페인 13.3.6 스위스 13.3.7 러시아 13.3.8 터키 13.3.9 벨기에 13.3.10 네덜란드 13.3.11 EUROPE의 등급

13.4 아시아 수출

13.4.1 중국 13.4.2 인도 13.4.3 SOUTH KOREA 13.4.4 일본 13.4.5 AUSTRALIA 13.4.6 SINGAPORE 13.4.7 태국 13.4.8 INDONESIA 13.4.9 MALAYSIA 13.4.10 필리핀 13.4.11 ASIA-PACIFIC의 시험

13.5 SOUTH 아메리카

13.5.1 BRAZIL 13.5.2 ARGENTINA 13.5.3 SOUTH AMERICA의 상승

13.6 중동 및 아프리카

13.6.1 UAE 13.6.2 SAUDI ARABIA 13.6.3 ISRAEL 13.6.4 SOUTH AFRICA 13.6.5 EGYPT 13.6.6 MIDDLE EAST 및 AFRICA의 등급

14 GLOBAL TANK 기업 시장, 기업 LANDSCAPE

14.1 COMPANY SHARE ANALYSIS: GLOBAL 14.2 COMPANY SHARE ANALYSIS: NORTH AMERICA 14.3 COMPANY SHARE ANALYSIS: EUROPE 14.4 COMPANY SHARE ANALYSIS: ASIA- PACIFIC 14.5 MERGERS & ACQUISITION 14.6 신제품 개발 및 APPROVALS 14.7 EXPANSIONS 14.8 PARTNERSHIP AND OTHER STRATEGIC DEVELOPMENTS

15 회사소개

15.1 BASF 세트

15.1.1 COMPANY SNAPSHOT 15.1.2 SWOT ANALYSIS 15.1.3 REVENUE ANALYSIS 15.1.4 COMPANY SHARE ANALYSIS 15.1.5 GEOGRAPHICAL PRESENCE 15.1.6 PRODUCT PORTFOLIO 15.1.7 RECENT DEVELOPMENTS 15.1.8 DATA BRIDGE MARKET ANALYSIS

15.2 DOW 화학 회사

15.2.1 COMPANY SNAPSHOT 15.2.2 SWOT ANALYSIS 15.2.3 REVENUE ANALYSIS 15.2.4 COMPANY ANALYSIS 15.2.5 GEOGRAPHICAL PRESENCE 15.2.6 제품 PORTFOLIO 15.2.7 RECENT DEVELOPMENTS 15.2.8 DATA BRIDGE MARKET RESEARCH ANALYSIS

15.3 포인트

15.3.1 COMPANY SNAPSHOT 15.3.2 SWOT ANALYSIS 15.3.3 REVENUE ANALYSIS 15.3.4 COMPANY SHARE ANALYSIS 15.3.5 GEOGRAPHICAL PRESENCE 15.3.6 PRODUCT PORTFOLIO 15.3.7 RECENT DEVELOPMENTS 15.3.8 DATA BRIDGE MARKET ANALYSIS

15.4 HUNTSMAN 국제 LLC

15.4.1 COMPANY SNAPSHOT 15.4.2 SWOT ANALYSIS 15.4.3 REVENUE ANALYSIS 15.4.4 COMPANY SHARE ANALYSIS 15.4.5 GEOGRAPHICAL PRESENCE 15.4.6 제품 PORTFOLIO 15.4.7 RECENT DEVELOPMENTS 15.4.8 DATA BRIDGE MARKET 수지 분석

15.5 KINGSPAN 그룹

15.5.1 COMPANY SNAPSHOT 15.5.2 SWOT ANALYSIS 15.5.3 REVENUE ANALYSIS 15.5.4 COMPANY SHARE ANALYSIS 15.5.5 GEOGRAPHICAL PRESENCE 15.5.6 PRODUCT PORTFOLIO 15.5.7 RECENT DEVELOPMENTS 15.5.8 DATA BRIDGE MARKET RESEARCH ANALYSIS

15.6 ARMACELL 소프트웨어

15.6.1 COMPANY SNAPSHOT 15.6.2 REVENUE ANALYSIS 15.6.3 GEOGRAPHICAL PRESENCE 15.6.4 제품 PORTFOLIO 15.6.5 유지 보수

15.7 CABOT 기업

15.7.1 COMPANY SNAPSHOT 15.7.2 REVENUE ANALYSIS 15.7.3 GEOGRAPHICAL PRESENCE 15.7.4 제품 PORTFOLIO 15.7.5 유지 보수

15.8 상업적인 TheRMAL 해결책, INC.

15.8.1 COMPANY SNAPSHOT 15.8.2 제품 PORTFOLIO 15.8.3 보유 개발

15.9 부식 저항 기술, INC.

15.9.1 COMPANY SNAPSHOT 15.9.2 제품포트폴리오 15.9.3 RECENT DEVELOPMENT

15.10 시간

15.10.1 COMPANY SNAPSHOT 15.10.2 GEOGRAPHICAL PRESENCE 15.10.3 제품 PORTFOLIO 15.10.4 수익률

15.11 GILSULATE 국제, INC.

15.11.1 회사 SNAPSHOT 15.11.2 제품 PORTFOLIO 15.11.3 유지 보수

15.12 GULF 냉각 THERM 공장 LTD

15.12.1 회사 SNAPSHOT 15.12.2 제품 PORTFOLIO 15.12.3 유지 보수

15.13 ITW 통합 시스템

15.13.1 회사 SNAPSHOT 15.13.2 GEOGRAPHICAL PRESENCE 15.13.3 제품 PORTFOLIO 15.13.4 유지 보수

15.14 JOHNS 매뉴얼

15.14.1 COMPANY SNAPSHOT 15.14.2 GEOGRAPHICAL PRESENCE 15.14.3 제품 PORTFOLIO 15.14.4 RECENT DEVELOPMENTS

15.15 J.H. 지글러 GMBH

15.15.15.1 COMPANY SNAPSHOT 15.15.2 GEOGRAPHICAL PRESENCE 15.15.3 제품포트폴리오 15.15.4 RECENT DEVELOPMENT

15.16 KNAUF 절연

15.16.1 회사 SNAPSHOT 15.16.2 GEOGRAPHICAL PRESENCE 15.16.3 제품 PORTFOLIO 15.16.4 저장소

15.17 MAYES 코팅 및 절연, INC.

15.17.1 회사 SNAPSHOT 15.17.2 제품 PORTFOLIO 15.17.3 저장소

15.18 OWENS 공동작업

15.18.1 COMPANY SNAPSHOT 15.18.2 REVENUE ANALYSIS 15.18.3 GEOGRAPHICAL PRESENCE 15.18.4 제품 PORTFOLIO 15.18.5 저장소

15.19 POLARCLAD 탱크 절연

15.19.1 회사 SNAPSHOT 15.19.2 제품 PORTFOLIO 15.19.3 RECENT 개발

15.20 RÖCHLING 그룹

15.20.1 회사 SNAPSHOT 15.20.2 GEOGRAPHICAL PRESENCE 15.20.3 제품 PORTFOLIO 15.20.4 유지 보수

15.21 ROCKWOOL 국제 A / S

15.21.1 회사 SNAPSHOT 15.21.2 REVENUE ANALYSIS 15.21.3 GEOGRAPHICAL PRESENCE 15.21.4 제품 PORTFOLIO 15.21.5 유지 보수

15.22 SPX 트랜스포머 솔루션 INC.

15.22.1 회사 SNAPSHOT 15.22.2 제품 PORTFOLIO 15.22.3 RECENT 개발

15.23 SYNAVAX의 특징

15.23.1 기업 SNAPSHOT 15.23.2 해결책 PORTFOLIO 15.23.3 책임 차원

15.24 더마콘

15.24.1 COMPANY SNAPSHOT 15.24.2 제품 PORTFOLIO 15.24.3 RECENT 개발

15.25 T.F.WARREN 그룹

15.25.1 COMPANY SNAPSHOT 15.25.2 GEOGRAPHICAL PRESENCE 15.25.3 제품 PORTFOLIO 15.25.4 RECENT 개발

16 질문 17 계약 18 관련 자료

표 목록

TABLES GLOBAL TANK 소개

RESERVOIRS, TANKS, VAT 및 SIMILAR CONTAINERS, IRON 또는 강철의 1 IMPORT DATA, 어떤 재료 "OTHER THAN COMPRESSED 또는 LIQUEFIED GAS"의 용량 > 300 L, MECHANICAL OR THERMAL EQUIPMENT, WHETHER 또는 LINED 또는 HEAT-INSULATED (EXCLUDING CONTAINERS SPECIFICALLY CONSTRUCTED 또는 TRANSPORT의 하나 이상의 유형에 대 한 공급); HS CODE 7309 (USD MILLION) TABLE 2 RESERVOIRS, TANKS, VAT AND SIMILAR AND S AND SOILAR, ORFIAL AND AND AND SENSOR AND SENSOR AND SENSOR AND SENS AND SENSOR AND AND SENSOR AND SENS AND SENS AND SENSOR AND AND AND AND AND AND SENS AND SENS AND SENSOR AND SENS AND SENS AND SENS AND SENS AND SENS AND SENS AND SENS AND SENS AND SENS AND SENS AND SENS AND SENS AND SENS AND SENS AND SENS AND SENS AND SENS AND SENS AND SENS AND SENS AND SENS AND SENS AND SENS AND SENS AND SENS AND SENS AND SENS AND SENS AND SENS AND SENS AND SENS AND SENS AND SENS AND SENS AND S NKION, NKION, NKION, NKION, NKION, NKION, NKION, NKION, NKION, NKION, NKION, NKION, NKION, NKION, NKION, NKION, NKION, NKION, NKION, NKION, NKION, NKION, NKION, NKION, NKION, NKION, NKION, NKION, NKION, NKION, NKION, NKION, NKION, NKION, NKION, NKION

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.