Middle East And Africa Cardiopulmonary Bypass Accessory Equipment Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

5.23 Billion

USD

6.72 Billion

2025

2033

USD

5.23 Billion

USD

6.72 Billion

2025

2033

| 2026 –2033 | |

| USD 5.23 Billion | |

| USD 6.72 Billion | |

| % | |

|

Middle East and Africa Cardiopulmonary Bypass Accessory Equipment Market Segmentation, By Product (Oxygenator, ECMO Machine, Pumps, Cannula, Temperature Monitors, Heat Exchanger, Filters, Tubing Clamps, Hemoconcentrators, System Panel, Sensor and Accessories, Cardioplegia Control, Reservoir, Bubble Detector, Electronic Gas Blender, Electrical Venous Occluder, Venous Line Clamp and Accessories), Operation (Manually Operated, Electrically Operated and Battery Operated), Application (Cardiac Surgery, Cardiac Surgery Oxygenators, Acute Respiratory Failure Treatment, Lung Cancer, Transplant Operation and Others), Age (Adult, Geriatric and Pediatric), End User (Hospitals, Cardiac Centers, Research and Academic Institutions, Ambulatory Surgical Centers and Others), Distribution Channel (Direct Tender, Third Party Distributor and Retail Sales)- Industry Trends and Forecast to 2033

Middle East and Africa Cardiopulmonary Bypass Accessory Equipment Market Size

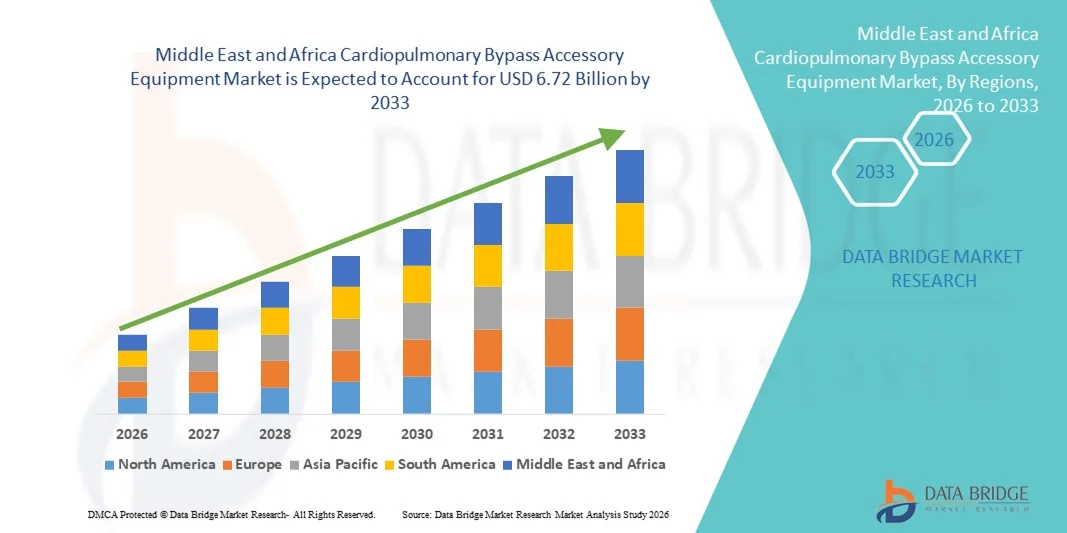

- The Middle East and Africa cardiopulmonary bypass accessory equipment market size was valued at USD 5.23 billion in 2025 and is expected to reach USD 6.72 billion by 2033, at a CAGR of 3.2% during the forecast period

- The market growth is largely fueled by the rising prevalence of cardiovascular diseases, expanding surgical infrastructure across GCC and African nations, and increasing utilization of advanced cardiopulmonary bypass systems in both public and private healthcare facilities

- Furthermore, growing demand for efficient and reliable surgical support equipment, heightened awareness of cardiac care, and investments in modernizing healthcare delivery systems are positioning cardiopulmonary bypass accessory products as essential tools in cardiac surgery settings across the Middle East & Africa. These converging factors are accelerating the uptake of such solutions, thereby significantly boosting the industry’s growth trajectory

Middle East and Africa Cardiopulmonary Bypass Accessory Equipment Market Analysis

- Cardiopulmonary bypass accessory equipment, including oxygenators, pumps, filters, and monitoring systems, are becoming increasingly essential in modern cardiac surgery, supporting both adult and pediatric procedures across hospitals and specialized cardiac centers in the Middle East and Africa due to their role in improving surgical efficiency, patient safety, and clinical outcomes

- The growing demand for these devices is primarily driven by the rising prevalence of cardiovascular diseases, expanding cardiac surgery infrastructure, and increasing awareness of advanced cardiac care solutions among healthcare providers in the region

- Saudi Arabia dominated the Middle East cardiopulmonary bypass accessory equipment market with the largest revenue share of 42.5% in 2025, characterized by well-established healthcare infrastructure, high healthcare expenditure, and the presence of advanced cardiac centers

- Africa is expected to be the fastest-growing region in the market during the forecast period driven by ongoing healthcare development initiatives, increasing investment in cardiac surgery facilities, and rising adoption of modern surgical support equipment in both public and private hospitals

- Oxygenator segment dominated the cardiopulmonary bypass accessory equipment market with a market share of 39.2% in 2025, driven by its critical role in ensuring effective gas exchange and patient safety during cardiopulmonary bypass procedures

Report Scope and Middle East and Africa Cardiopulmonary Bypass Accessory Equipment Market Segmentation

|

Attributes |

Middle East and Africa Cardiopulmonary Bypass Accessory Equipment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Middle East and Africa Cardiopulmonary Bypass Accessory Equipment Market Trends

Advancing Surgical Precision Through Integrated Monitoring and Automation

- A significant and accelerating trend in the Middle East and Africa cardiopulmonary bypass accessory equipment market is the deeper integration of advanced monitoring technologies and semi-automated control systems into perfusion workflows, which is substantially improving surgical precision and real-time decision-making during cardiac procedures

- For instance, modern heart-lung machine accessories are increasingly designed to integrate with digital monitoring platforms that track oxygenation levels, blood flow rates, and temperature parameters, allowing clinical teams to respond quickly to intraoperative changes while maintaining procedural stability

- Technology integration in bypass accessories enables features such as continuous data capture, predictive safety alerts, and improved perfusion management based on patient parameters. For instance, some oxygenator and sensor systems are designed to enhance gas exchange efficiency and trigger alerts when performance thresholds shift. Furthermore, automated control support offers perfusionists greater operational consistency and reduced manual adjustment burden

- The seamless integration of bypass accessories with hospital information systems and surgical monitoring platforms facilitates centralized oversight of cardiac procedures. Through unified interfaces, surgical teams can coordinate perfusion data alongside anesthesia and vital monitoring systems, creating a more synchronized and controlled operating room environment

- This trend toward more precise, responsive, and interconnected perfusion systems is reshaping clinical expectations for cardiac surgery support. Consequently, manufacturers are developing next-generation accessories with features such as integrated sensors, real-time analytics, and compatibility with digital surgical platforms used in advanced cardiac centers

- The demand for cardiopulmonary bypass accessories that offer high reliability and integrated monitoring support is rising steadily across major hospitals, as healthcare providers increasingly prioritize surgical safety, efficiency, and improved patient outcome

Middle East and Africa Cardiopulmonary Bypass Accessory Equipment Market Dynamics

Driver

Growing Need Due to Rising Cardiovascular Disease Burden and Surgical Capacity Expansion

- The increasing burden of cardiovascular diseases across the Middle East and Africa, combined with the gradual expansion of specialized cardiac care centers, is a major driver behind the growing demand for cardiopulmonary bypass accessory equipment

- For instance, several tertiary hospitals in the region are expanding their cardiac surgery departments and incorporating advanced perfusion accessories to support higher procedural volumes and more complex interventions, which is contributing to market growth momentum

- As healthcare systems strengthen their cardiac care capabilities, bypass accessories provide essential support functions such as blood oxygenation, circulation management, and filtration, making them indispensable in open-heart and corrective cardiac surgeries

- Furthermore, government investments in healthcare modernization and the establishment of specialized heart institutes are encouraging hospitals to adopt modern surgical support technologies that align with international treatment standards

- The growing aging population in several Middle Eastern countries is contributing to higher incidence of cardiac conditions, thereby increasing the procedural demand for cardiopulmonary bypass supported surgeries

- Medical tourism growth in parts of the Middle East is encouraging private hospitals to equip advanced cardiac surgery units with reliable bypass accessory systems to attract international patients

- The need for dependable surgical support, improved survival rates, and better postoperative outcomes is propelling adoption of advanced bypass accessories in both public and private healthcare facilities, while training programs for perfusionists further support utilization growth

Restraint/Challenge

High Equipment Costs and Technical Complexity Barriers

- Concerns surrounding the high cost and technical complexity of cardiopulmonary bypass accessory equipment present a notable challenge to wider market penetration, particularly in resource-constrained healthcare settings within parts of the region

- For instance, smaller hospitals may hesitate to invest in premium perfusion accessories and monitoring add-ons due to budget limitations and competing infrastructure priorities, which can slow adoption rates

- Addressing these barriers requires cost-effective product offerings, reliable technical support, and specialized training to ensure safe and efficient equipment usage. Manufacturers are increasingly focusing on durability, user training, and service agreements to support clinical teams

- In addition, the need for skilled perfusionists and ongoing maintenance increases the total ownership burden for healthcare providers, making procurement decisions more complex for some institutions

- Limited reimbursement frameworks for advanced cardiac procedures in certain countries can reduce hospital willingness to invest in premium bypass accessories and frequent upgrades

- Supply chain constraints and dependency on imported medical devices may create procurement delays and cost fluctuations for healthcare providers in some African and Middle Eastern markets

- Overcoming these challenges through affordability strategies, clinical training expansion, and long-term service support will be important for sustaining market growth across diverse healthcare systems in the region

Middle East and Africa Cardiopulmonary Bypass Accessory Equipment Market Scope

The market is segmented on the basis of product, operation, application, age, end user, and distribution channel.

- By Product

On the basis of product, the cardiopulmonary bypass accessory equipment market is segmented into oxygenator, ECMO machine, pumps, cannula, temperature monitors, heat exchanger, filters, tubing clamps, hemoconcentrators, system panel, sensor and accessories, cardioplegia control, reservoir, bubble detector, electronic gas blender, electrical venous occluder, venous line clamp and accessories. The oxygenator segment dominated the market with the largest market revenue share of 39.2% in 2025, driven by its indispensable role in gas exchange during cardiopulmonary bypass procedures. Oxygenators are required in nearly all open-heart surgeries, making them a standard component in cardiac operating rooms. Hospitals consistently procure advanced oxygenators to maintain patient oxygenation and procedural safety. Continuous improvements in membrane biocompatibility and efficiency support their strong adoption. The growing volume of cardiac surgeries across MEA further strengthens demand. The market also sees sustained preference for oxygenators due to their compatibility with modern heart-lung machines and monitoring systems.

The ECMO machine segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing demand for prolonged cardiopulmonary support in critical care. ECMO is increasingly used in cases of severe cardiac and respiratory failure. Expansion of ICU capacity in Gulf countries is supporting utilization. Training initiatives are improving clinician familiarity and confidence. The rising burden of respiratory diseases is also contributing to demand. The segment benefits from growing investments in life-support infrastructure across tertiary hospitals.

- By Operation

On the basis of operation, the market is segmented into manually operated, electrically operated, and battery operated. The electrically operated segment held the largest market revenue share in 2025 driven by its precision and automation advantages. These systems provide consistent flow control and stable performance. Hospitals prefer them for complex and long-duration surgeries. Automated functions reduce manual intervention and error risk. Integration with digital monitoring platforms improves workflow efficiency. The market also observes strong adoption due to their reliability in high-volume surgical centers.

The battery operated segment is expected to witness the fastest CAGR from 2026 to 2033, driven by its portability and backup power capability. These systems are valuable in emergency and transport scenarios. Facilities in regions with unstable electricity benefit significantly. Compact and mobile designs increase usability. Adoption is rising in developing healthcare setups. The market also sees demand growth as battery technology improves durability and runtime. Compact and portable designs increase usability. Their role in improving operational continuity supports growth.

- By Application

On the basis of application, the market is segmented into cardiac surgery, cardiac surgery oxygenators, acute respiratory failure treatment, lung cancer, transplant operation, and others. The cardiac surgery segment dominated the market with the largest revenue share in 2025, driven by the high number of bypass-dependent procedures. Coronary artery disease prevalence continues to support surgical volumes. Most open-heart surgeries require cardiopulmonary bypass. Specialized heart centers are expanding capacity. Government investments in cardiac care further support demand. The market also sees strong reliance on bypass accessories for complex surgical interventions.

The transplant operation segment is anticipated to witness the fastest growth from 2026 to 2033, fueled by the gradual expansion of organ transplant programs. Heart and lung transplants require advanced perfusion support. Specialized transplant centers are emerging in major cities. Success rates are improving with better technology. Cross-border collaborations are supporting program development. The market also benefits from rising awareness of transplant treatment options. Clinical success rates are gradually improving. This increases confidence in transplant surgeries.

- By Age

On the basis of age, the market is segmented into adult, geriatric, and pediatric. The adult segment held the largest market revenue share in 2025 driven by the higher incidence of cardiovascular disease among adults. Lifestyle-related risk factors increase surgical need. Most bypass surgeries are performed on adults. Hospitals are primarily structured for adult cardiac care. Screening programs help early diagnosis. The market also sees consistent adult procedure volumes sustaining equipment demand.

The geriatric segment is expected to witness the fastest growth rate from 2026 to 2033 due to the rising elderly population. Older adults face greater cardiac risk. Improvements in surgical safety enable more elderly operations. Healthcare access for seniors is expanding. Postoperative care quality is improving outcomes. The market also sees rising willingness to operate on elderly patients. Improved surgical safety enables operations in older patients. Healthcare access for seniors is expanding. This supports segment growth.

- By End User

On the basis of end user, the market is segmented into hospitals, cardiac centers, research and academic institutions, ambulatory surgical centers, and others. The hospitals segment dominated the market with the largest revenue share in 2025 as hospitals perform the majority of bypass surgeries. They possess complete surgical infrastructure. ICU availability supports complex cases. Skilled perfusionists are hospital-based. Hospitals receive larger procurement budgets. The market also sees hospitals maintaining long-term supplier agreements.

The cardiac centers segment is anticipated to witness the fastest growth from 2026 to 2033 driven by increasing specialization in heart care. These centers handle large patient volumes. Investments in dedicated cardiac units are rising. They adopt advanced technologies rapidly. Focus on clinical outcomes builds trust. The market also benefits from their specialized treatment capabilities. These centers adopt advanced technologies quickly. They emphasize quality outcomes. Their specialization drives growth.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, third-party distributor, and retail sales. The direct tender segment held the largest market revenue share in 2025 driven by bulk procurement by hospitals and governments. Tender systems ensure cost efficiency. They support transparent purchasing. Service contracts are often bundled. Authentic sourcing is ensured. The market also sees preference for tenders among large healthcare institutions.

The third-party distributor segment is expected to witness the fastest CAGR from 2026 to 2033 fueled by expanding access to smaller facilities. Distributors improve regional availability. They enable faster product delivery. Local technical support encourages adoption. They connect manufacturers with local buyers. The market also benefits from their ability to reach remote healthcare providers. They bridge global manufacturers and local buyers. This expands market penetration.

Middle East and Africa Cardiopulmonary Bypass Accessory Equipment Market Regional Analysis

- Saudi Arabia dominated the Middle East cardiopulmonary bypass accessory equipment market with the largest revenue share of 42.5% in 2025, characterized by well-established healthcare infrastructure, high healthcare expenditure, and the presence of advanced cardiac centers

- Healthcare providers in the country highly prioritize advanced cardiopulmonary bypass accessories to support a rising number of open-heart surgeries and complex cardiac procedures performed in leading hospitals and heart institutes

- This widespread adoption is further supported by high healthcare spending, ongoing healthcare modernization under national development programs, and the growing preference for technologically advanced surgical solutions, establishing cardiopulmonary bypass accessories as essential tools in cardiac care across major medical centers

The Saudi Arabia Cardiopulmonary Bypass Accessory Equipment Market Insight

The Saudi Arabia cardiopulmonary bypass accessory equipment market captured the largest revenue share in the Middle East and Africa in 2025, fueled by strong government investments in advanced healthcare infrastructure and the expansion of specialized cardiac centers. Healthcare providers are increasingly prioritizing high-quality perfusion accessories to support complex open-heart surgeries. The growing burden of cardiovascular diseases is pushing procedural volumes higher. National healthcare transformation programs are also strengthening procurement of advanced surgical technologies. Moreover, the concentration of well-equipped tertiary hospitals is significantly contributing to market expansion.

UAE Cardiopulmonary Bypass Accessory Equipment Market Insight

The UAE cardiopulmonary bypass accessory equipment market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rapid healthcare modernization and a strong focus on specialized cardiac care. Hospitals are adopting technologically advanced bypass accessories to enhance surgical precision. The country’s growing medical tourism sector supports higher volumes of cardiac procedures. Increased awareness of advanced treatment options is also encouraging adoption. In addition, partnerships with international medical device manufacturers are stimulating technology availability.

South Africa Cardiopulmonary Bypass Accessory Equipment Market Insight

The South Africa cardiopulmonary bypass accessory equipment market is expected to expand at a considerable CAGR during the forecast period, fueled by improving healthcare infrastructure and rising investment in cardiac care units. The country serves as a major healthcare hub in Sub-Saharan Africa. Increasing diagnosis of cardiovascular conditions is driving surgical demand. Public and private hospitals are gradually upgrading surgical capabilities. Adoption of modern perfusion technologies is rising in leading hospitals. Furthermore, physician training programs are supporting technology utilization.

Africa Cardiopulmonary Bypass Accessory Equipment Market Insight

The Africa cardiopulmonary bypass accessory equipment market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by healthcare development initiatives and increasing investment in specialized surgical care. Urbanization and improving access to tertiary care are supporting growth. Governments and NGOs are strengthening cardiac care programs. The region is witnessing gradual expansion of heart surgery facilities. International collaborations are improving equipment availability. As awareness of advanced cardiac treatments rises, adoption of bypass accessories is expanding.

Middle East and Africa Cardiopulmonary Bypass Accessory Equipment Market Share

The Middle East and Africa Cardiopulmonary Bypass Accessory Equipment industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- LivaNova PLC (U.K.)

- Braile Biomédica (Brazil)

- Teleflex Incorporated (U.S.)

- Getinge AB (Sweden)

- Terumo Corporation (Japan)

- Surge Cardiovascular (U.S.)

- Abbott (U.S.)

- Edwards Lifesciences Corporation (U.S.)

- SCHNELL MEDICAL Corp. (Switzerland)

- NIPRO Corporation (Japan)

- XENIOS AG (Germany)

- Advin Health Care (India)

- Boston Scientific Corporation (U.S.)

- APC Cardiovascular Ltd (U.K.)

- MicroPort Scientific Corporation (China)

- Alung Technologies, Inc. (U.S.)

- Berlin Heart (Germany)

- Jarvik Heart, Inc. (U.S.)

- Narang Medical Limited (India)

- Technowood International Pte. Ltd. (Singapore)

What are the Recent Developments in Middle East and Africa Cardiopulmonary Bypass Accessory Equipment Market?

- In September 2025, the Saudi humanitarian aid agency KSrelief reported the successful execution of nine open-heart surgeries and multiple catheterization procedures in Yemen as part of a medical project, demonstrating surgical outreach and capacity building in cardiac care across the region. These operations inherently depend on cardiopulmonary bypass support infrastructure for complex surgeries

- In February 2025, King Fahad Cardiac Center in Saudi Arabia advanced its ECMO project by establishing a dedicated ECMO service team aimed at improving clinical support and patient outcomes, aligning with Saudi Vision 2030’s focus on healthcare excellence and workforce development in critical care disciplines. This reflects institutional development in extracorporeal support systems and clinical expertise

- In February 2025, the 2025 SWAAC ELSO ECMO Conference concluded in Abu Dhabi, bringing together more than 1,100 clinicians and experts to explore the latest advancements in extracorporeal membrane oxygenation (ECMO) therapy and related life support technologies used in cardiac and critical care. The three-day event featured in-depth presentations, discussions on clinical best practices, emerging technologies, and integration of ECMO care into multidisciplinary healthcare teams

- In February 2022, Saudi Arabia’s Ministry of Health announced that the Kingdom would host the Extracorporeal Life Support Organization’s (ELSO) 8th regional conference to discuss the latest developments in ECMO and extracorporeal support, underscoring the region’s growing engagement with advanced cardiopulmonary life-support practices. This initiative aimed to foster knowledge sharing and scientific collaboration around ECMO and related technologies

- In March 2021, King Abdullah Medical City in Makkah reported that the use of ECMO technology helped increase recovery rates among severe COVID-19 patients, highlighting the clinical value of extracorporeal circulation machines in acute cardiopulmonary care. The ECMO system enabled critical support for patients who had not responded to conventional treatments, underlining expanded use of advanced perfusion-related life support technology in Saudi Arabia

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.