Middle East And Africa Lipid Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

496.85 Million

USD

878.32 Million

2022

2030

USD

496.85 Million

USD

878.32 Million

2022

2030

| 2023 –2030 | |

| USD 496.85 Million | |

| USD 878.32 Million | |

| % | |

Middle East and Africa Lipids Market, By Type (Natural Lipids and Synthetic Lipids), Lipid System (Neutral Lipids, Bacterial Lipids, Fluorescent Lipids, Bioactive Lipids, Polymerizable Lipids, Headgroup Modified Lipids, and Others), Delivery System (Liposomes, Solid Lipid Nanoparticles, Nanostructures Lipid Carrier, Niosomes, Transferosomes, and Others), Source (Egg Yolk, Soyabean, Non-GMO Soyabean, Purified Oils, Purified Fatty Acids, and Others), End User (Pharmaceutical Industries, Biotechnology Industries, Academic and Research Institutes, Cosmetic Industries and Others), Distribution Channel (Direct Tender, Retail Sales and Others) - Industry Trends and Forecast to 2030.

Middle East and Africa Lipids Market Analysis and Insights

The growing prevalence of chronic diseases globally has enhanced the demand of the market. The rising healthcare expenditure for better health services are also attributing in the growth of the market. The major market players are highly focusing on various product launches and drug approvals during this crucial period. In addition, the increasing demand for lipids in various other industries such as food and beverage, cosmetic industries and among others also contributing in the rising demand for lipids market.

The increasing healthcare expenditure, strategic initiatives by market players and are giving opportunities to the market. However, different manufacturing challenges for lipid nanoparticles production and lack of healthcare facilities in emerging economies are key challenges for the market growth.

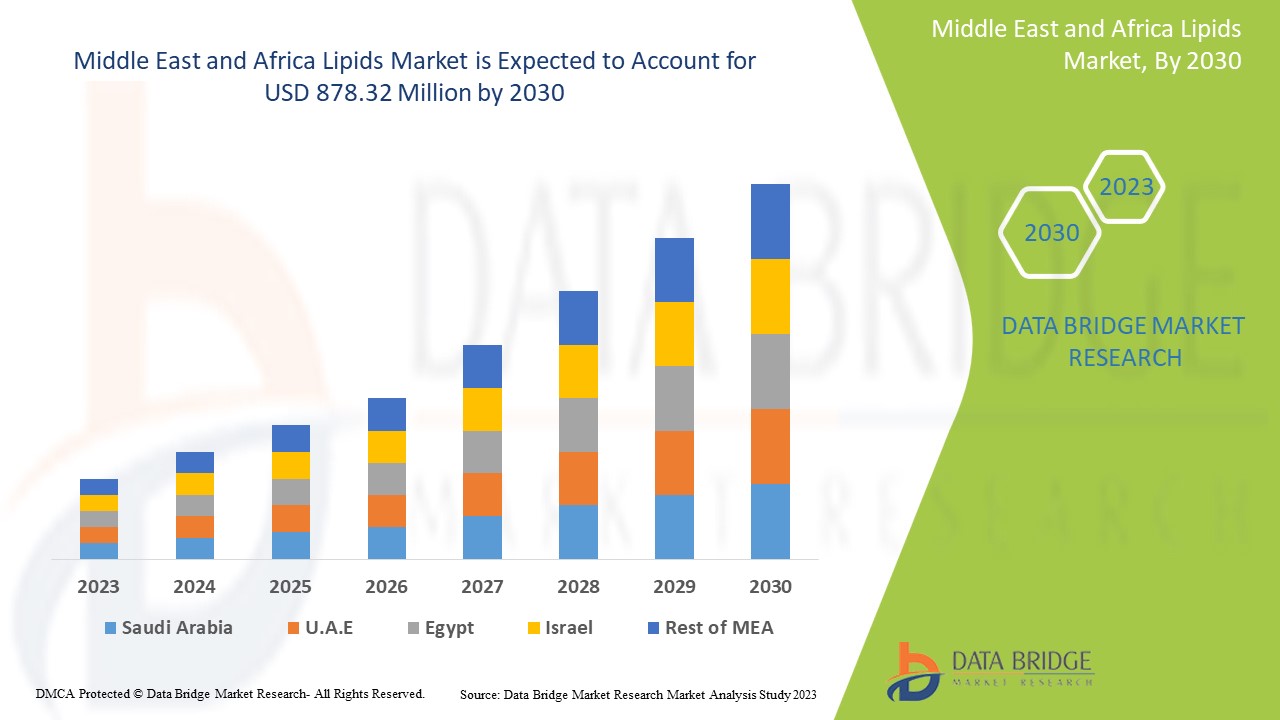

Middle East and Africa lipids market is expected to gain market growth in the forecast period of 2023 to 2030. Data Bridge Market Research analyses that the market is growing with a CAGR of 7.4% in the forecast period of 2023 to 2030 and is expected to reach USD 878.32 million by 2030 from USD 496.85 million in 2022.

|

Report Metric |

Details |

|

Forecast Period |

2023 to 2030 |

|

Base Year |

2022 |

|

Historic Years |

2021 (Customisable to 2020-2015) |

|

Quantitative Units |

Revenue in USD Million |

|

Segments Covered |

By Type (Natural Lipids and Synthetic Lipids), Lipid System (Neutral Lipids, Bacterial Lipids, Fluorescent Lipids, Bioactive Lipids, Polymerizable Lipids, Headgroup Modified Lipids, and Others), Delivery System (Liposomes, Solid Lipid Nanoparticles, Nanostructures Lipid Carrier, Niosomes, Transferosomes, and Others), Source (Egg Yolk, Soyabean, Non-GMO Soyabean, Purified Oils, Purified Fatty Acids, and Others), End User (Pharmaceutical Industries, Biotechnology Industries, Academic and Research Institutes, Cosmetic Industries and Others), Distribution Channel (Direct Tender, Retail Sales and Others) |

|

Countries Covered |

South Africa, Saudi Arabia, U.A.E, Egypt, Israel, and Rest of Middle East and Africa |

|

Market Players Covered |

Alnylam Pharmaceutical, Inc., Croda International Plc., Moderna Inc., BioNTech SE., Pfizer Inc., Evonik Industries AG, Lipoid GmbH, Matreya LLC, VAV Life Sciences Pvt Ltd., Curia Middle East and Africa Inc., Cargill, Incorporated, Gattefossé, CD Bioparticles, Merck KGaA, NOF EUROPE GmbH, ABITEC, Cayman Chemical, CordenPharma International, CHEMI S.p.A., DSM, BASF SE, Tokyo Chemical Industry Co., Ltd., ADMSIO, Stepan Company, and Kerry |

Market Definition

Lipids can be defined as a group of organic compounds found in animals, plants, and micro- organisms. They include sterols, waxes, fats, and fat soluble vitamins. Lipids hold an ability to execute various activities. At the same time, they are known for having low toxicity levels. These qualities of lipids help in effective drug delivery. As a result, they are increasingly used as excipients in the drug production. This factor is fueling the growth of the Middle East and Africa pharmaceutical lipids market.

In recent period, the worldwide healthcare sector is going through remarkable changes. Development in drug delivery technology along with the incorporation of drug formularies is working as a driver for the growth of the pharmaceutical lipids market. Growth in quick chronic health issues and quick resulting drug delivery to the patient is one of the key factors pushing the growth of the Middle East and Africa pharmaceutical lipids market.

Lipids Market Dynamics

Drivers

-

Increase in the prevalence of chronic diseases

The encumbrance of chronic disease is briskly increasing across the globe. According to the WHO (World Health Organization), in 2021, the contribution of chronic disease was about 60%, which accounted for the number of deaths. In most Western countries, the major reason behind the increasing number of chronic diseases is the continuous increase in the aged population. The rise in the number of chronic diseases such as cardiovascular diseases, neurological disorders, and various other chronic diseases has led to an increase in the demand for various medicinal drugs that will drive the growth of the Middle East and Africa lipids market in the coming years.

-

Rising demand for lipids in food and beverage as well as the cosmetic industry

The demand for lipids in pharmaceuticals is very high as it is used in developing various drugs in the market. Also, the demand for lipids has increased in various other industries, such as in food & beverage and cosmetic products.

Lipids are an essential ingredient in the formulation of dietary supplements owing to their high content of energy and fat-soluble vitamins. Increasing health concern among people in light of COVID-19 has propelled the Middle East and Africa demand for dietary supplements. Furthermore, the availability of dietary supplements in multiple forms and flavours has made them more socially acceptable to all age groups. Growing dietary supplement consumption is expected to boost the demand for lipids over the projected years.

-

Rise in drug development

In the pharmaceutical industry, lipids and polymers are considered pillar excipients for formulating various drugs. They are used as stabilizers, solubilizes, permeation enhancers, and transfection agents. Increasing adoption of a wide range of natural, synthetic, semi-synthetic or completely artificial lipids and polymers in the formulation of various dosage forms is expected to boost the market over the forecast period.

Opportunities

-

Rise in healthcare expenditure

Healthcare expenditure has increased worldwide as people's disposable income in various countries increases. Moreover, to accomplish the population requirements, government bodies and healthcare organizations are taking the initiative to accelerate healthcare expenditure. The rise in healthcare expenditure simultaneously helps healthcare settings to improve their treatment facilities for various diseases is highly prevalent in recent years.

-

Strategic initiatives by major players

Increasing rates of various types of disease and their severity are widely seen among people globally. The dramatic rise in research quality and increasing research opportunities is because of various strategic initiatives the market players take. They are taking initiatives such as product launch, collaborations, mergers, acquisitions, and many more over the years and is expected to lead and create more opportunities in the market. Evonik invested in the short-term growth of its specialty lipids production at its Hanau and Dossenheim locations in Germany, which supplied two of the four lipids for the Pfizer/BioNTech vaccine. According to Spencer, the first batches were delivered to BioNTech in April 2021, months ahead of schedule.

Restraints/Challenges

High cost of lipid synthesis and increasing cost of raw materials

Lipid based drugs require a huge cost for the development process. As the concept needs to be locked down, the materials need to be sourced, and it is important to consider lead times. Additionally, the process is time consuming as the drug needs sufficient time to fulfil all the clinical trials before bringing in the market for use.

Furthermore, any changes that must be re-verified will impact time. The growing advancements in biosensor assay formats and other complementary technologies demanded an effective investment for successful operations and a project risk management plan. The establishment of R&D for conducting research entails high costs, leading to expensive drugs. Thus, this factor is a major restraint for the Middle East and Africa lipids market.

- Different manufacturing challenges for lipid nanoparticle production

Lipid nanoparticles have made a major impact on the pharmaceutical industry. At their core, lipid nanoparticles (LNPs) are delivery carriers that safeguard nucleic acids. As an integral part of recent mRNA vaccines, they are injected and transported to the intended site in the cell. Despite the many advantages of lipid nanoparticles as delivery systems, the pharmaceutical industry must address significant manufacturing challenges.

These challenges include:

- Precisely controlled particle size/size distributions

- Sterilization issues

- Process repeatability and scalability

- Regulatory requirements (such as cGMP regulations)

Post COVID-19 Impact on Lipids Market

The COVID-19 has positively affected the market. As the demand for COVID-19 vaccine was on the great demand and the positive point here is the lipid is majorly used in the vaccine production. Thus COVID-19 affected lipids market positively.

Recent Developments

- In November 2022, BioNTech SE announced its Singapore affiliate BioNTech Pharmaceuticals Asia Pacific Pte. Ltd. had entered into an agreement with Novartis Singapore Pharmaceutical Manufacturing Pte. Ltd. to acquire one of its GMP-certified manufacturing facilities. The acquisition is part of BioNTech’s expansion strategy to strengthen its Middle East and Africa footprint in Asia.

- In September 2021, U.S. ingredients supplier ABITEC Corporation signed an amended agreement with DKSH to distribute its specialty lipids into new markets and regions across Europe. This has helped the company to expand its business in various regions.

Middle East and Africa Lipids Market Scope

Middle East and Africa lipids market is segmented into, type, lipid systems, delivery systems, source, end user and distribution channel. The growth amongst these segments will help you analyse meagre growth segments in the industries and provide the users with a valuable market overview and market insights to make strategic decisions to identify core market applications.

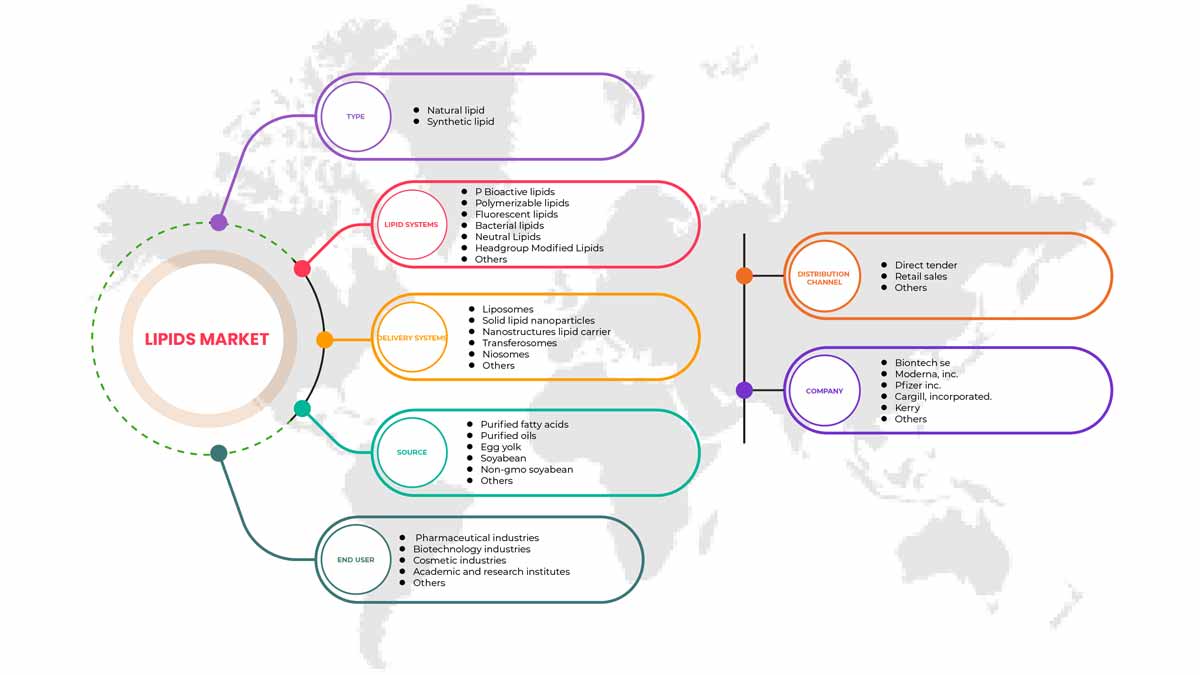

Type

- Natural Lipid

- Synthetic Lipids

On the basis of type, the Middle East and Africa lipids market is segmented into natural lipid and synthetic lipid.

Lipid Systems

- Bioactive Lipids

- Polymerizable Lipids

- Fluorescent Lipids

- Bacterial Lipids

- Neutral Lipids

- Headgroup Modified Lipids

- Others

Based on lipid systems, the Middle East and Africa lipids market is segmented into neutral lipids, bacterial lipids, fluorescent lipids, bioactive lipids, polymerizable lipids, headgroup modified lipids and others.

Delivery Systems

- Liposomes

- Solid Lipid Nanoparticles

- Nanostructures Lipid Carrier

- Transferosomes

- Niosomes

- Others

Based on delivery systems, the Middle East and Africa lipids market is segmented into liposomes, solid lipid nanoparticles, nanostructures lipid carrier, niosomes, transferosomes and others.

Source

- Purified Fatty Acids

- Purified Oils

- Egg Yolk

- Soyabean

- Non-GMO Soyabean

- Others

Based on source, the Middle East and Africa lipids market is segmented into egg yolk, soyabean, non-GMO soyabean, purified oils, purified fatty acids and others.

End User

- Pharmaceutical Industries

- Biotechnology Industries

- Cosmetic Industry

- Academic and Research Institutes

- Others

Based on end user, the Middle East and Africa lipids market is segmented into pharmaceutical industries, biotechnology industries, academic and research institutes, cosmetic industries and others.

Distribution Channel

- Direct Tender

- Retail Sales

- Others

Based on distribution channel, the Middle East and Africa lipids market is segmented into direct tender, retail sales and others.

Lipids market Regional Analysis/Insights

The lipids market is analysed and market size insights and trends are provided by country, type, lipid systems, delivery systems, source, end user and distribution channel.

Countries covered in lipids market are South Africa, Saudi Arabia, U.A.E, Egypt, Israel, and Rest of Middle East and Africa.

South Africa is expected to grow due to a rise in chronic diseases owing to high demand for pharmaceutical drugs and rising demand for lipids in different industries are expected to drive the regional market in the forecasted period.

The country section of the report also provides individual market-impacting factors and changes in market regulation that impact the current and future trends of the market. Data points like downstream and upstream value chain analysis, technical trends, porter's five forces analysis, and case studies are some of the pointers used to forecast the market scenario for individual countries. Also, the presence and availability of Asia-Pacific brands and their challenges faced due to large or scarce competition from local and domestic brands, the impact of domestic tariffs, and trade routes are considered while providing forecast analysis of the country data.

Competitive Landscape and Lipids Market Share Analysis

The lipids market competitive landscape provides details by the competitors. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, Middle East and Africa presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, and application dominance. The above data points provided are only related to the companies' focus on lipids market.

Some of the major players operating in the lipids market are Alnylam Pharmaceutical, Inc., Croda International Plc., Moderna Inc., BioNTech SE., Pfizer Inc., Evonik Industries AG, Lipoid GmbH, Matreya LLC, VAV Life Sciences Pvt Ltd., Curia Middle East and Africa Inc., Cargill, Incorporated, Gattefossé, CD Bioparticles, Merck KGaA, NOF EUROPE GmbH, ABITEC, Cayman Chemical, CordenPharma International, CHEMI S.p.A., DSM, BASF SE, Tokyo Chemical Industry Co., Ltd., ADMSIO, Stepan Company, and Kerry among others.

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

목차

1 서론

1.1 연구 목적

1.2 시장 정의

1.3 중동 및 아프리카 지질 시장 개요

1.4 제한 사항

1.5 대상 시장

2 시장 세분화

2.1 대상 시장

2.2 지리적 범위

연구에 2.3년이 고려됨

2.4 통화 및 가격

2.5 DBMR TRIPOD 데이터 검증 모델

2.6 다변량 모델링

2.7 유형 라이프라인 곡선

2.8 주요 여론 선도자와의 1차 인터뷰

2.9 DBMR 시장 위치 그리드

2.1 시장 최종 사용자 범위 그리드

2.11 공급업체 점유율 분석

2.12 2차 소스

2.13 가정

3 요약

4가지 프리미엄 인사이트

4.1 PESTEL 분석

4.2 포터의 5가지 힘

4.3 합병 및 인수, 중동 및 아프리카 지질 시장

4.4 특허 분석, 중동 및 아프리카 지질 시장

4.5 성숙 시장별 약물 치료율

4.6 인구 통계적 추세: 모든 발생률에 미치는 영향

4.7 주요 가격 책정 전략

4.8 주요 환자 등록 전략

4.9 가격 분석, 중동 및 아프리카 지질 시장

4.1 중동 및 아프리카 지질 시장, 임상 시험

4.11 중동 및 아프리카 지질 시장, 단계별 제품 분포

4.12 중동 및 아프리카 지질 시장, 파이프라인 분석

4.13 1단계 후보자

4.14 1/2단계 후보자

4.15 2단계 후보자

4.16 3단계 후보자

5 중동 및 아프리카 지질 시장, 규제 프레임워크

5.1 미국 내 규제:

5.2 유럽의 규제:

6 시장 개요

6.1 드라이버

6.1.1 만성질환 유병률 증가

6.1.2 식품 및 음료와 화장품 산업에서 지질에 대한 수요 증가

6.1.3 약물 개발 증가

6.2 제약

6.2.1 지질 합성의 높은 비용과 원자재 비용의 증가

6.2.2 엄격한 정부 규정

6.3 기회

6.3.1 의료비 지출 증가

6.3.2 시장 참여자의 전략적 이니셔티브

6.4 과제

6.4.1 지질 나노입자 생산을 위한 다양한 제조 과제

6.4.2 신흥 경제권의 의료 시설 부족

7 중동 및 아프리카 지질 시장, 유형별

7.1 개요

7.2 천연지질

7.2.1 불포화 인지질

7.2.2 수소화 인지질

7.2.3 스핑고미엘린

7.2.4 글리세롤포스포콜린

7.3 합성지질

7.3.1 페길화 인지질

7.3.2 포스파티딜세린

7.3.3 인지질글리세롤

7.3.4 포스파티딜에탄올아민

7.3.5 포스파티딜콜린

7.3.6 인산지질산

8 중동 및 아프리카 지질 시장, 지질 시스템

8.1 개요

8.2 생물학적 활성 지질

8.2.1 식물지질

8.2.2 지질 활성제

8.2.3 지질 억제제

8.2.4 작용제

8.2.5 생물학적 활성 세라마이드

8.2.6 아실 카르니틴 지질

8.2.7 엔도칸나비노이드

8.2.8 리포뉴클레오타이드

8.2.9 리실포스파티딜글리세롤

8.2.10 디아실글리세롤 피로인산(DGPP)

8.3 중합성 지질

8.3.1 기능성 PEG 지질

8.3.2 MPEG 스테롤

8.3.3 MPEG 세라마이드

8.3.4 MPEG 인지질

8.3.5 MPEG 글리세리드

8.4 형광지질

8.4.1 형광 스핑고지질

8.4.2 형광 글리세롤지질

8.4.3 형광 PEG 지질

8.4.4 형광성 인산지질

8.4.5 형광 스테롤

8.4.6 기타

8.5 세균성 지질

8.5.1 미콜산지질

8.5.2 N-아실호모세린 지질

8.5.3 분지형 지질

8.5.4 시클로프로필 지질

8.6 중성지질

8.6.1 프레놀

8.6.2 매우 긴 사슬 지방산

8.6.3 글리세리드

8.6.4 에이코사노이드

8.6.5 산소화된 지방산

8.6.6 글리코실화 디아실 글리세롤

8.6.7 프로스타글란딘

8.7 헤드그룹 변형지질

8.7.1 기능성 지질

8.7.2 항원성 지질

8.7.3 당화지질

8.7.4 킬레이트제

8.7.5 접착성 지질

8.7.6 스냅태그 반응성 지질

8.7.7 알킬 인산염

8.8 기타

9 중동 및 아프리카 지질 시장, 배송 시스템별

9.1 개요

9.2 리포좀

9.2.1 DNA/RNA용 리포좀

9.2.1.1 DNA/RNA 전달을 위한 DOTAP 리포좀

9.2.1.2 DNA/RNA 전달을 위한 DDAB 리포좀

9.2.1.3 DNA/RNA 전달을 위한 GL-67 리포좀

9.2.1.4 DNA/RNA 전달을 위한 DC-콜레스테롤 리포좀

9.2.1.5 DNA/RNA 전달을 위한 DOTMA 리포좀

9.2.1.6 DNA/RNA 전달을 위한 DODAP 리포좀

9.2.2 반응성 리포좀

9.2.2.1 석시닐 리포좀

9.2.2.2 DBCO 리포좀

9.2.2.3 바이오틴화 리포좀

9.2.2.4 카르복실산 리포좀

9.2.2.5 아민 리포좀

9.2.2.6 CYANUR 리포좀

9.2.2.7 아지드 리포좀

9.2.2.8 엽산 리포좀

9.2.2.9 도데카닐 리포좀

9.2.2.10 NI 반응성 리포좀

9.2.2.11 PDP 리포좀

9.2.2.12 글루타릴 리포좀

9.2.2.13 기타

9.2.3 약물이 적재된 리포좀

9.2.4 일반 리포좀

9.2.4.1 카디오리핀 지질 리포좀

9.2.4.2 DOTAP 리포좀

9.2.4.3 포스파티딜세린 리포좀

9.2.4.4 포스파티딜콜린 리포좀

9.2.4.5 포스파티딜글리세롤 리포좀

9.2.4.6 기타

9.3 고체 지질 나노입자

9.4 나노구조 지질 운반체

9.5 전이소체

9.6 니오솜

9.7 기타

10 중동 및 아프리카 지질 시장, 출처별

10.1 개요

10.2 정제지방산

10.3 정제 오일

10.4 달걀 노른자

10.5 콩

10.6 비GMO 대두

10.7 기타

11 중동 및 아프리카 지질 시장, 최종 사용자별

11.1 개요

11.2 제약 산업

11.3 생명공학 산업

11.4 화장품 산업

11.5 학술 및 연구 기관

11.6 기타

12 중동 및 아프리카 지질 시장, 유통 채널별

12.1 개요

12.2 직접 입찰

12.3 소매 판매

12.4 기타

13 중동 및 아프리카 지질 시장, 지역별

13.1 중동 및 아프리카

13.1.1 남아프리카 공화국

13.1.2 사우디 아라비아

13.1.3 아랍에미리트

13.1.4 이집트

13.1.5 이스라엘

13.1.6 중동 및 아프리카의 나머지 지역

14 중동 및 아프리카 지질 시장: 회사 환경

14.1 회사 점유율 분석: 중동 및 아프리카

15 SWOT 분석

16 회사 프로필

16.1 바이오텍 SE.

16.1.1 회사 스냅샷

16.1.2 수익 분석

16.1.3 회사 점유율 분석

16.1.4 제품 포트폴리오

16.1.5 최근 개발

16.2 모더나 주식회사

16.2.1 회사 스냅샷

16.2.2 수익 분석

16.2.3 회사 점유율 분석

16.2.4 제품 포트폴리오

16.2.5 최근 개발 사항

16.3 파이저 주식회사

16.3.1 회사 스냅샷

16.3.2 수익 분석

16.3.3 회사 점유율 분석

16.3.4 제품 포트폴리오

16.3.5 최근 개발 사항

16.4 카길 주식회사.

16.4.1 회사 스냅샷

16.4.2 회사 점유율 분석

16.4.3 제품 포트폴리오

16.4.4 최근 개발 사항

16.5 케리.

16.5.1 회사 스냅샷

16.5.2 회사 점유율 분석

16.5.3 제품 포트폴리오

16.5.4 최근 개발 사항

16.6 아비텍

16.6.1 회사 스냅샷

16.6.2 제품 포트폴리오

16.6.3 최근 개발 사항

16.7 ADMSIO

16.7.1 회사 스냅샷

16.7.2 제품 포트폴리오

16.7.3 최근 개발 사항

16.8 알나일람제약 주식회사

16.8.1 회사 스냅샷

16.8.2 수익 분석

16.8.3 제품 포트폴리오

16.8.4 최근 개발

16.9 바스프 SE

16.9.1 회사 스냅샷

16.9.2 수익 분석

16.9.3 제품 포트폴리오

16.9.4 최근 개발 사항

16.1 케이맨 케미컬

16.10.1 회사 스냅샷

16.10.2 제품 포트폴리오

16.10.3 최근 개발 사항

16.11 CD 생물입자.

16.11.1 회사 스냅샷

16.11.2 제품 포트폴리오

16.11.3 최근 개발 사항

16.12 케미 스파

16.12.1 회사 스냅샷

16.12.2 제품 포트폴리오

16.12.3 최근 개발 사항

16.13 코덴파마 인터내셔널

16.13.1 회사 스냅샷

16.13.2 제품 포트폴리오

16.13.3 최근 개발 사항

16.14 크로다 인터내셔널 PLC.

16.14.1 회사 스냅샷

16.14.2 제품 포트폴리오

16.14.3 최근 개발 사항

16.15 쿠리아 중동 및 아프리카 주식회사

16.15.1 회사 스냅샷

16.15.2 제품 포트폴리오

16.15.3 최근 개발

16.16 DSM

16.16.1 회사 스냅샷

16.16.2 제품 포트폴리오

16.16.3 최근 개발 사항

16.17 에보닉 인더스트리스 AG

16.17.1 회사 스냅샷

16.17.2 제품 포트폴리오

16.17.3 최근 개발 사항

16.18 가테포세

16.18.1 회사 스냅샷

16.18.2 제품 포트폴리오

16.18.3 최근 개발 사항

16.19 리포이드 GMBH

16.19.1 회사 스냅샷

16.19.2 제품 포트폴리오

16.19.3 최근 개발

16.2 마트레이아, 유한회사

16.20.1 회사 스냅샷

16.20.2 제품 포트폴리오

16.20.3 최근 개발 사항

16.21 머크 KGAA

16.21.1 회사 스냅샷

16.21.2 제품 포트폴리오

16.21.3 최근 개발 사항

16.22 NOF 유럽 GMBH

16.22.1 회사 스냅샷

16.22.2 제품 포트폴리오

16.22.3 최근 개발 사항

16.23 스테판 회사

16.23.1 회사 스냅샷

16.23.2 제품 포트폴리오

16.23.3 최근 개발 사항

16.24 도쿄화학공업 주식회사

16.24.1 회사 스냅샷

16.24.2 제품 포트폴리오

16.24.3 최근 개발 사항

16.25 VAV 생명과학 PVT LTD

16.25.1 회사 스냅샷

16.25.2 제품 포트폴리오

16.25.3 최근 개발 사항

17 설문지

18 관련 보고서

표 목록

표 1 지질 시장의 주요 약물에 대한 ASP(USD 가격)

표 2 COVID-19 백신을 위한 지질 기반 나노 입자

표 3 암 백신을 위한 지질 기반 나노 입자

표 4 RNA 캡슐화된 지질 나노입자

표 5 리포좀 제형

표 6 COVID 백신을 위한 지질 기반 나노 입자

표 7 리포좀 제형

표 8 암 백신을 위한 지질 기반 나노 입자

표 9 RNA 캡슐화된 지질 나노입자

표 10 리포좀 제형

표 11 COVID 백신을 위한 지질 기반 나노 입자

표 12 암 백신을 위한 지질 기반 나노 입자

표 13 리포좀 제형

표 14 중동 및 아프리카 지질 시장, 유형별, 2021-2030(백만 달러)

표 15 중동 및 아프리카 천연 지질 시장, 지역별, 2021-2030 (백만 달러)

표 16 중동 및 아프리카 천연 지질 시장, 유형별, 2021-2030(백만 달러)

표 17 중동 및 아프리카 합성 지질 시장, 지역별 지질 시장, 2021-2030 (백만 달러)

표 18 중동 및 아프리카 합성 지질 시장, 유형별, 2021-2030(백만 달러)

표 19 중동 및 아프리카 지질 시장, 지질 시스템별, 2021-2030년(백만 달러)

표 20 중동 및 아프리카 지역별 지질 시장의 생물 활성 지질, 2021-2030년(백만 달러)

표 21 지질 시스템별 지질 시장의 중동 및 아프리카 생물 활성 지질, 2021-2030년(백만 달러)

표 22 중동 및 아프리카 지역별 지질 시장의 중합성 지질, 2021-2030년(백만 달러)

표 23 지질 시스템별 지질 시장의 중동 및 아프리카 중합성 지질, 2021-2030년(백만 달러)

표 24 중동 및 아프리카 형광지질 시장, 지역별, 2021-2030 (백만 달러)

표 25 지질 시스템별 지질 시장의 중동 및 아프리카 형광 지질, 2021-2030년(백만 달러)

표 26 중동 및 아프리카 박테리아 지질 시장, 지역별, 2021-2030(백만 달러)

표 27 지질 시스템별 지질 시장의 중동 및 아프리카 박테리아 지질, 2021-2030년(백만 달러)

표 28 중동 및 아프리카 중성 지질 시장, 지역별, 2021-2030 (백만 달러)

표 29 지질 시스템별 지질 시장의 중동 및 아프리카 중성 지질, 2021-2030년(백만 달러)

표 30 중동 및 아프리카 헤드그룹 지질 시장의 변형 지질, 지역별, 2021-2030 (백만 달러)

표 31 중동 및 아프리카 헤드그룹 지질 시장의 변형 지질, 지질 시스템별, 2021-2030(백만 달러)

표 32 중동 및 아프리카 기타 지역별 지질 시장, 2021-2030년(백만 달러)

표 33 중동 및 아프리카 지질 시장, 배달 시스템별, 2021-2030년(백만 달러)

표 34 중동 및 아프리카 리포좀 지질 시장, 지역별, 2021-2030 (백만 달러)

표 35 중동 및 아프리카 지질 시장의 리포좀, 전달 시스템별, 2021-2030년(백만 달러)

표 36 중동 및 아프리카 지질 시장에서 DNA/RNA용 리포좀, 전달 시스템별, 2021-2030년(백만 달러)

표 37 중동 및 아프리카 지질 시장에서의 반응성 리포좀, 전달 시스템별, 2021-2030년(백만 달러)

표 38 중동 및 아프리카 지질 시장에서의 플레인 리포좀, 전달 시스템별, 2021-2030년(백만 달러)

표 39 중동 및 아프리카 고체 지질 나노입자 지질 시장, 지역별, 2021-2030 (백만 달러)

표 40 중동 및 아프리카 나노구조 지질 운반체 지질 시장, 지역별, 2021-2030 (백만 달러)

표 41 중동 및 아프리카 지질 시장의 전이소체, 지역별, 2021-2030년(백만 달러)

표 42 중동 및 아프리카 지질 시장의 니오솜, 지역별, 2021-2030년(백만 달러)

표 43 중동 및 아프리카 기타 지역별 지질 시장, 2021-2030년(백만 달러)

표 44 중동 및 아프리카 지질 시장, 출처별, 2021-2030년(백만 달러)

표 45 중동 및 아프리카 정제 지방산 지질 시장, 지역별, 2021-2030 (백만 달러)

표 46 중동 및 아프리카 정제 오일 지질 시장, 지역별, 2021-2030 (백만 달러)

표 47 중동 및 아프리카 계란 노른자 지질 시장, 지역별, 2021-2030 (백만 달러)

표 48 중동 및 아프리카 대두 지질 시장, 지역별, 2021-2030 (백만 달러)

표 49 중동 및 아프리카 비GMO 대두 지질 시장, 지역별, 2021-2030 (백만 달러)

표 50 중동 및 아프리카 기타 지역별 지질 시장, 2021-2030년(백만 달러)

표 51 중동 및 아프리카 지질 시장, 최종 사용자별, 2021-2030년(백만 달러)

표 52 중동 및 아프리카 제약 산업의 지질 시장, 지역별, 2021-2030 (백만 달러)

표 53 중동 및 아프리카 생명공학 산업의 지질 시장, 지역별, 2021-2030 (백만 달러)

표 54 중동 및 아프리카 화장품 산업의 지질 시장, 지역별, 2021-2030 (백만 달러)

표 55 중동 및 아프리카 학술 및 연구 기관 지질 시장, 지역별, 2021-2030 (백만 달러)

표 56 중동 및 아프리카 기타 지역별 지질 시장, 2021-2030년(백만 달러)

표 57 중동 및 아프리카 지질 시장, 유통 채널별, 2021-2030년(백만 달러)

표 58 중동 및 아프리카 지질 시장 직접 입찰, 지역별, 2021-2030 (백만 달러)

표 59 중동 및 아프리카 지역별 리피드 시장의 소매 판매, 2021-2030년 (백만 달러)

표 60 중동 및 아프리카 기타 지역별 지질 시장, 2021-2030년(백만 달러)

표 61 중동 및 아프리카 지질 시장, 국가별, 2021-2030년(백만 달러)

표 62 중동 및 아프리카 지질 시장, 유형별, 2021-2030(백만 달러)

표 63 중동 및 아프리카 천연 지질 시장, 유형별, 2021-2030(백만 달러)

표 64 중동 및 아프리카 합성 지질 시장, 유형별, 2021-2030(백만 달러)

표 65 중동 및 아프리카 지질 시장, 지질 시스템별, 2021-2030년(백만 달러)

표 66 지질 시스템별 지질 시장의 중동 및 아프리카 중성 지질, 2021-2030년(백만 달러)

표 67 지질 시스템의 지질 시장에서 중동 및 아프리카 박테리아 지질, 2021-2030년(백만 달러)

표 68 지질 시스템별 지질 시장의 중동 및 아프리카 형광 지질, 2021-2030년(백만 달러)

표 69 지질 시스템별 지질 시장의 중동 및 아프리카 생물 활성 지질, 2021-2030년(백만 달러)

표 70 중동 및 아프리카 지질 시장의 중합성 지질, 지질 시스템별, 2021-2030(백만 달러)

표 71 중동 및 아프리카 헤드그룹 지질 시장의 변형 지질, 지질 시스템별, 2021-2030(백만 달러)

표 72 중동 및 아프리카 지질 시장, 배달 시스템별, 2021-2030년(백만 달러)

표 73 중동 및 아프리카 지질 시장의 리포좀, 전달 시스템별, 2021-2030년(백만 달러)

표 74 중동 및 아프리카 지질 시장에서 DNA/RNA용 리포좀, 전달 시스템별, 2021-2030년(백만 달러)

표 75 중동 및 아프리카 지질 시장의 반응성 리포좀, 전달 시스템별, 2021-2030년(백만 달러)

표 76 중동 및 아프리카 지질 시장에서의 플레인 리포좀, 전달 시스템별, 2021-2030년(백만 달러)

표 77 중동 및 아프리카 지질 시장, 출처별, 2021-2030(백만 달러)

표 78 중동 및 아프리카 지질 시장, 최종 사용자별, 2021-2030년(백만 달러)

표 79 중동 및 아프리카 지질 시장, 유통 채널별, 2021-2030년(백만 달러)

표 80 남아프리카 지방 시장, 유형별, 2021-2030 (백만 달러)

표 81 남아프리카 공화국 천연 지질 시장, 유형별, 2021-2030(백만 달러)

표 82 남아프리카 공화국 합성 지질의 지질 시장, 유형별, 2021-2030(백만 달러)

표 83 지질 시스템별 남아프리카 지질 시장, 2021-2030년(백만 달러)

표 84 지질 시스템별 지질 시장의 남아프리카 중성 지질, 2021-2030년(백만 달러)

표 85 지질 시스템의 지질 시장에서 남아프리카 박테리아 지질, 2021-2030년(백만 달러)

표 86 지질 시스템별 지질 시장의 남아프리카 형광 지질, 2021-2030년(백만 달러)

표 87 지질 시스템별 지질 시장의 남아프리카 생물 활성 지질, 2021-2030년(백만 달러)

표 88 지질 시스템별 지질 시장의 남아프리카 중합성 지질, 2021-2030년(백만 달러)

표 89 남아프리카 헤드그룹 지질 시장의 변형 지질, 지질 시스템별, 2021-2030(백만 달러)

표 90 남아프리카 공화국 지질 시장, 배달 시스템별, 2021-2030년(백만 달러)

표 91 남아프리카 공화국 지질 시장의 리포좀, 전달 시스템별, 2021-2030년(백만 달러)

표 92 지질 시장에서 DNA/RNA를 위한 남아프리카 리포좀, 전달 시스템별, 2021-2030년(백만 달러)

표 93 남아프리카 공화국 지질 시장의 반응성 리포좀, 전달 시스템별, 2021-2030년(백만 달러)

표 94 남아프리카 공화국 플레인 리포좀 지질 시장, 전달 시스템별, 2021-2030년(백만 달러)

표 95 남아프리카 지질 시장, 출처별, 2021-2030(백만 달러)

표 96 남아프리카 지질 시장, 최종 사용자별, 2021-2030년(백만 달러)

표 97 남아프리카 공화국 지질 시장, 유통 채널별, 2021-2030년(백만 달러)

표 98 사우디 아라비아 지질 시장, 유형별, 2021-2030 (백만 달러)

표 99 사우디 아라비아 천연 지질 시장, 유형별, 2021-2030(백만 달러)

표 100 사우디 아라비아 합성 지질 시장, 유형별, 2021-2030(백만 달러)

표 101 사우디 아라비아 지질 시장, 지질 시스템별, 2021-2030년(백만 달러)

표 102 사우디 아라비아 지질 시스템의 지질 시장에서 중성 지질, 2021-2030년 (백만 달러)

표 103 지질 시스템의 지질 시장에서 사우디 아라비아 박테리아 지질, 2021-2030년(백만 달러)

표 104 사우디 아라비아 형광 지질, 지질 시스템별 지질 시장, 2021-2030(백만 달러)

표 105 사우디 아라비아 지질 시스템의 지질 시장에서의 생물학적 지질, 2021-2030년 (백만 달러)

표 106 사우디 아라비아의 지질 시스템에서의 중합성 지질, 2021-2030년 (백만 달러)

표 107 사우디 아라비아 헤드그룹 지질 시장의 변형 지질, 지질 시스템별, 2021-2030(백만 달러)

표 108 사우디 아라비아 지질 시장, 배달 시스템별, 2021-2030년(백만 달러)

표 109 사우디 아라비아 지질 시장에서의 리포좀, 전달 시스템별, 2021-2030년(백만 달러)

표 110 사우디 아라비아 지질 시장에서 DNA/RNA용 리포좀, 전달 시스템별, 2021-2030년(백만 달러)

표 111 사우디 아라비아 지질 시장에서의 반응성 리포좀, 전달 시스템별, 2021-2030년(백만 달러)

표 112 사우디 아라비아 플레인 리포좀 지질 시장, 전달 시스템별, 2021-2030년(백만 달러)

표 113 사우디 아라비아 지질 시장, 출처별, 2021-2030 (백만 달러)

표 114 사우디 아라비아 지질 시장, 최종 사용자별, 2021-2030(백만 달러)

표 115 사우디 아라비아 지질 시장, 유통 채널별, 2021-2030년(백만 달러)

표 116 UAE 지질 시장, 유형별, 2021-2030 (백만 달러)

표 117 지질 시장의 UAE 천연 지질, 유형별, 2021-2030(백만 달러)

표 118 지질 시장에서의 UAE 합성 지질, 유형별, 2021-2030 (백만 달러)

표 119 UAE LIPIDS 시장, LIPIDS 시스템별, 2021-2030(백만 달러)

표 120 지질 시스템별 지질 시장의 UAE 중성 지질, 2021-2030년(백만 달러)

표 121 지질 시스템의 지질 시장에서의 UAE 박테리아 지질, 2021-2030년(백만 달러)

표 122 지질 시스템별 지질 시장의 UAE 형광 지질, 2021-2030(백만 달러)

표 123 지질 시스템의 지질 시장에서의 UAE 생물학적 활성 지질, 2021-2030년(백만 달러)

표 124 지질 시스템별 지질 시장의 UAE 중합성 지질, 2021-2030년(백만 달러)

표 125 지질 시스템별 지질 시장의 UAE HEADGROUP 변형 지질, 2021-2030(백만 달러)

표 126 UAE 지질 시장, 배달 시스템별, 2021-2030년(백만 달러)

표 127 2021-2030년 전달 시스템별 지질 시장의 UAE 리포좀(백만 달러)

표 128 2021-2030년 전달 시스템별 지질 시장에서 DNA/RNA용 UAE 리포좀(백만 달러)

표 129 UAE 지질 시장의 반응성 리포좀, 전달 시스템별, 2021-2030년(백만 달러)

표 130 2021-2030년 전달 시스템별 지질 시장에서의 UAE 일반 리포좀(백만 달러)

표 131 출처별 UAE 지질 시장, 2021-2030년(백만 달러)

표 132 최종 사용자별 UAE 지질 시장, 2021-2030년(백만 달러)

표 133 유통 채널별 UAE 지질 시장, 2021-2030년(백만 달러)

표 134 이집트 지질 시장, 유형별, 2021-2030 (백만 달러)

표 135 지질 시장에서 이집트 천연 지질, 유형별, 2021-2030(백만 달러)

표 136 지질 시장에서 이집트 합성 지질, 유형별, 2021-2030(백만 달러)

표 137 이집트 지질 시장, 지질 시스템별, 2021-2030년(백만 달러)

표 138 지질 시스템에서의 이집트 중성 지질, 지질 시장, 2021-2030 (백만 달러)

표 139 지질 시스템의 지질 시장에서 이집트 박테리아 지질, 2021-2030 (백만 달러)

표 140 지질 시스템에서의 이집트 형광 지질, 지질 시장, 2021-2030 (백만 달러)

표 141 지질 시스템에서의 이집트 생물 활성 지질, 2021-2030 (백만 달러)

표 142 지질 시스템에서의 이집트 중합성 지질, 지질 시장, 2021-2030 (백만 달러)

표 143 지질 시스템에서 지질 시장의 이집트 헤드그룹 변형 지질, 2021-2030년(백만 달러)

표 144 이집트 지질 시장, 배달 시스템별, 2021-2030년(백만 달러)

표 145 이집트 리포좀의 지질 시장, 전달 시스템별, 2021-2030 (백만 달러)

표 146 지질 시장에서 DNA/RNA를 위한 이집트 리포좀, 전달 시스템별, 2021-2030년(백만 달러)

표 147 이집트 지질 시장의 반응성 리포좀, 전달 시스템별, 2021-2030년(백만 달러)

표 148 이집트 일반 리포좀 지질 시장, 전달 시스템별, 2021-2030 (백만 달러)

표 149 이집트 지질 시장, 출처별, 2021-2030 (백만 달러)

표 150 이집트 지질 시장, 최종 사용자별, 2021-2030(백만 달러)

표 151 이집트 지질 시장, 유통 채널별, 2021-2030년(백만 달러)

표 152 이스라엘 지질 시장, 유형별, 2021-2030 (백만 달러)

표 153 지질 시장에서 이스라엘 천연 지질, 유형별, 2021-2030(백만 달러)

표 154 이스라엘 합성 지질의 지질 시장, 유형별, 2021-2030(백만 달러)

표 155 이스라엘 지질 시장, 지질 시스템별, 2021-2030년(백만 달러)

표 156 지질 시스템별 지질 시장의 이스라엘 중성 지질, 2021-2030년(백만 달러)

표 157 지질 시스템의 지질 시장에서 이스라엘 박테리아 지질, 2021-2030 (백만 달러)

표 158 지질 시스템별 지질 시장의 이스라엘 형광 지질, 2021-2030년(백만 달러)

표 159 지질 시스템별 지질 시장의 이스라엘 생물학적 지질, 2021-2030(백만 달러)

표 160 지질 시스템별 지질 시장의 이스라엘 중합성 지질, 2021-2030년(백만 달러)

표 161 이스라엘 헤드그룹 지질 시장의 변형 지질, 지질 시스템별, 2021-2030(백만 달러)

표 162 이스라엘 지질 시장, 배달 시스템별, 2021-2030년(백만 달러)

표 163 이스라엘 지질 시장의 리포좀, 전달 시스템별, 2021-2030년(백만 달러)

표 164 이스라엘 지질 시장에서 DNA/RNA용 리포좀, 전달 시스템별, 2021-2030년(백만 달러)

표 165 이스라엘 지질 시장의 반응성 리포좀, 전달 시스템별, 2021-2030년(백만 달러)

표 166 이스라엘 플레인 리포좀 지질 시장, 전달 시스템별, 2021-2030 (백만 달러)

표 167 이스라엘 지질 시장, 출처별, 2021-2030 (백만 달러)

표 168 이스라엘 지질 시장, 최종 사용자별, 2021-2030년(백만 달러)

표 169 이스라엘 지질 시장, 유통 채널별, 2021-2030년(백만 달러)

표 170 중동 및 아프리카 나머지 지역 지질 시장, 유형별, 2021-2030년(백만 달러)

그림 목록

그림 1 중동 및 아프리카 지질 시장: 세분화

그림 2 중동 및 아프리카 지질 시장: 데이터 삼각 측량

그림 3 중동 및 아프리카 지질 시장: DROC 분석

그림 4 중동 및 아프리카 지질 시장: 중동 및 아프리카 대 지역 시장 분석

그림 5 중동 및 아프리카 지질 시장: 회사 연구 분석

그림 6 중동 및 아프리카 지질 시장: 인터뷰 인구 통계

그림 7 중동 및 아프리카 지질 시장: DBMR 시장 위치 그리드

그림 8 중동 및 아프리카 지질 시장: 시장 최종 사용자 범위 그리드

그림 9 중동 및 아프리카 지질 시장: 공급업체 점유율 분석

그림 10 중동 및 아프리카 지질 시장: 세분화

그림 11 만성 질환의 증가하는 유행과 다양한 산업에서 지질에 대한 수요 증가는 2023년에서 2030년 예측 기간 동안 중동 및 아프리카 지질 시장을 주도할 것으로 예상됩니다.

그림 12 테스트 서비스 부문은 2023년 및 2030년에 중동 및 아프리카 지질 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다.

그림 13 중동 및 아프리카 지질 시장의 동인, 제약, 기회 및 과제

그림 14 중동 및 아프리카 지질 시장: 유형별, 2022

그림 15 중동 및 아프리카 지질 시장: 유형별, 2023-2030(백만 달러)

그림 16 중동 및 아프리카 지질 시장: 유형별, CAGR(2023-2030)

그림 17 중동 및 아프리카 지질 시장: 유형별, 수명선 곡선

그림 18 중동 및 아프리카 지질 시장: 지질 시스템별, 2022

그림 19 중동 및 아프리카 지질 시장: 지질 시스템별, 2023-2030년(백만 달러)

그림 20 중동 및 아프리카 지질 시장: 지질 시스템별, CAGR(2023-2030)

그림 21 중동 및 아프리카 지질 시장: 지질 시스템별, 수명선 곡선

그림 22 중동 및 아프리카 지질 시장: 배달 시스템별, 2022

그림 23 중동 및 아프리카 지질 시장: 배달 시스템별, 2023-2030년(백만 달러)

그림 24 중동 및 아프리카 지질 시장: 배달 시스템별, CAGR(2023-2030)

그림 25 중동 및 아프리카 지질 시장: 배달 시스템별, 수명선 곡선

그림 26 중동 및 아프리카 지질 시장: 출처별, 2022년

그림 27 중동 및 아프리카 지질 시장: 출처별, 2023-2030년(백만 달러)

그림 28 중동 및 아프리카 지질 시장: 출처별, CAGR(2023-2030)

그림 29 중동 및 아프리카 지질 시장: 출처별, 수명선 곡선

그림 30 중동 및 아프리카 지질 시장: 최종 사용자별, 2022

그림 31 중동 및 아프리카 지질 시장: 최종 사용자별, 2023-2030년(백만 달러)

그림 32 중동 및 아프리카 지질 시장: 최종 사용자별, CAGR(2023-2030)

그림 33 중동 및 아프리카 지질 시장: 최종 사용자별, 수명선 곡선

그림 34 중동 및 아프리카 지질 시장: 유통 채널별, 2022

그림 35 중동 및 아프리카 지질 시장: 유통 채널별, 2023-2030년(백만 달러)

그림 36 중동 및 아프리카 지질 시장: 유통 채널별, CAGR(2023-2030)

그림 37 중동 및 아프리카 지질 시장: 유통 채널별, 수명선 곡선

그림 38 중동 및 아프리카 지질 시장: 스냅샷(2022)

그림 39 중동 및 아프리카 지질 시장: 국가별(2022년)

그림 40 중동 및 아프리카 지질 시장: 국가별(2023년 및 2030년)

그림 41 중동 및 아프리카 지질 시장: 국가별(2022년 및 2030년)

그림 42 중동 및 아프리카 지질 시장: 유형별(2023년 및 2030년)

그림 43 중동 및 아프리카 지질 시장: 회사 점유율 2022(%)

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.