North America Additive Manufacturing Market, By Material Type (Metal, Plastic, Alloys, and Ceramics), Technology (Stereolithography (SLA), Fused Disposition Modelling (FDM), Laser Sintering (LS), Binder Jetting Printing, Polyjet Printing, Electron Beam Melting (EBM), Laminated Object Manufacturing (LOM), and Others), Application (Automotive, Healthcare, Aerospace, Consumer Goods, Industrial, Defence, Architecture, and Others) Market Trends and Forecast to 2030.

North America Additive Manufacturing Market Analysis and Size

The additive manufacturing market is concerned with the design, production and distribution of yarn, cloth, clothing and garments. The raw material may be metal, plastics, alloys and ceramic. The additive manufacturing industries contribute significantly towards the national economy of many countries. Growing demand for lightweight components from the automotive and aerospace categories and advancement in 3D metal printing technologies has highly increased the demand in the North America additive manufacturing market.

The North America additive manufacturing market report provides details of market share, new developments, and the impact of domestic and localized market players, analyses opportunities in terms of emerging revenue pockets, changes in market regulations, products approvals, strategic decisions, product launches, geographic expansions, and technological innovations in the market. To understand the analysis and the market scenario, contact us for an Analyst Brief. Our team will help you create a revenue-impact solution to achieve your desired goal.

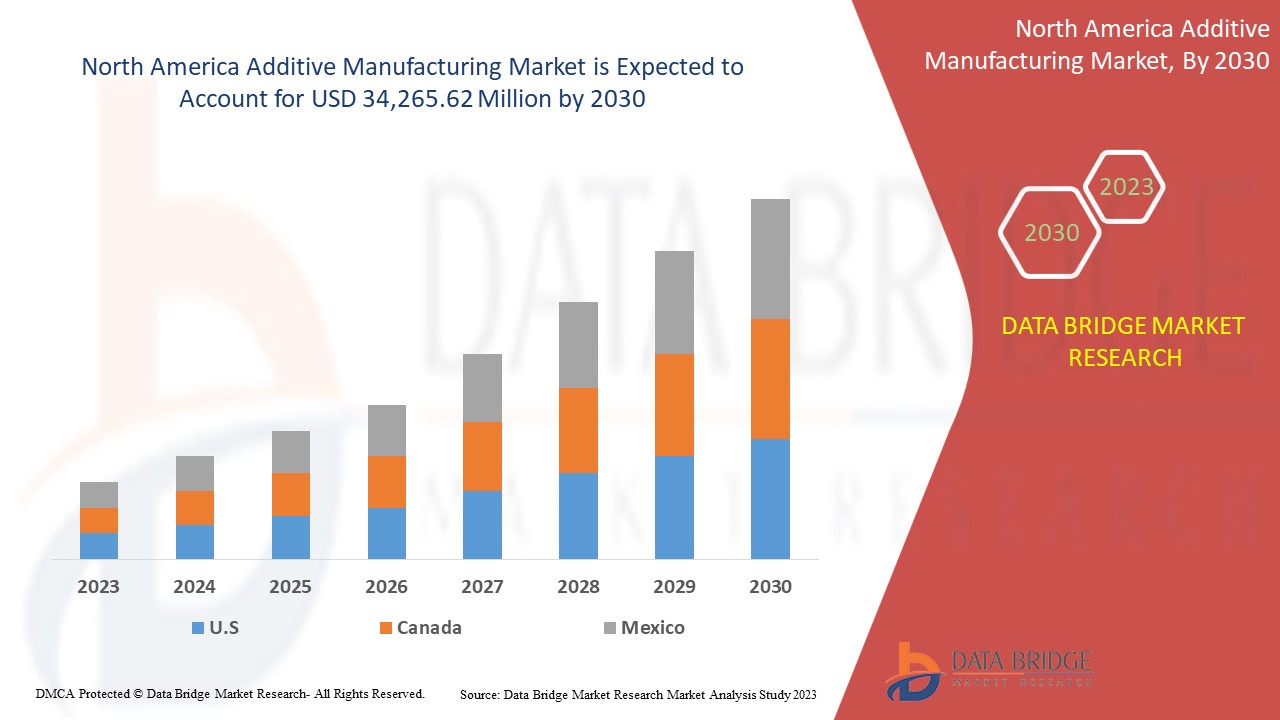

The North America additive manufacturing market is expected to gain significant growth in the forecast period of 2023 to 2030. Data Bridge Market Research analyses that the market is growing with a CAGR of 20.8% in the forecast period of 2023 to 2030 and is expected to reach USD 34,265.62 million by 2030. The major factor driving the growth of the additive manufacturing market is the increasing demand for lightweight components from the automotive and aerospace industries.

|

Report Metric |

Details |

|

Forecast Period |

2023 to 2030 |

|

Base Year |

2022 |

|

Historic Years |

2021 (Customizable to 2020 - 2015) |

|

Quantitative Units |

Revenue in USD Million |

|

Segments Covered |

By Material Type (Metal, Plastic, Alloys, and Ceramics), Technology (Stereolithography (SLA), Fused Disposition Modelling (FDM), Laser Sintering (LS), Binder Jetting Printing, Polyjet Printing, Electron Beam Melting (EBM), Laminated Object Manufacturing (LOM), and Others), Application (Automotive, Healthcare, Aerospace, Consumer Goods, Industrial, Defence, Architecture, and Others). |

|

Countries Covered |

U.S., Canada, and Mexico. |

|

Market Players Covered |

ANSYS, Inc, Höganäs AB, EOS, ARBURG GmbH + Co KG, Stratasys, Renishaw plc., YAMAZAKI MAZAK CORPORATION, Materialise, Markforged, Titomic Limited., SLM Solutions, Proto Labs, ENVISIONTEC US LLC, Ultimaker BV, American Additive Manufacturing LLC, Optomec, Inc., 3D system Inc., and ExOne. (A Subsidiary of Desktop Metal, Inc.), among others. |

Market Definition

Additive manufacturing (AM) is different from the subtractive method of production, which envisages grinding out unnecessary material from a block of material. The use of additive manufacturing in industrial applications usually refers to 3D printing. Additive manufacturing involves a layer-by-layer addition of material to form an object while referring to a three-dimensional file with the help of a 3D printer and 3D printer software. A suitable additive manufacturing technology is selected from the available set of technologies depending upon the application.

North America Additive Manufacturing Market Dynamics

Drivers

- Increasing demand for lightweight components from the automotive and aerospace industries

The automotive and aerospace sector requires numerous interacting technical and economic objectives of functional performance, lead time reduction, lightweight, cost management and delivery of safety-critical components. To meet the demand and to compensate for the fuel consumption and cost management to enhance the technical performance and allowable to make a lighter structure which directly related to enhancing economic and technical performance and which will help the airlines industry to carry more payload, which will directly improve their revenue. Additive manufacturing technologies, unlike conventional traditional manufacturing, use layer-by-layer manufacturing based on typical powder or wire and materials like plastic polymer, which is of lighter weight

- Advantages offered by additive manufacturing in various end-user industries

Industries like aerospace some of the industries that use the additive manufacturing product for their performance, and aeroplane parts are used by additive manufacturing products that are lightweight and can withstand harsh environmental conditions due to less material required, and the process of forming materials layers by layers aerospace industries utilize it as the advantage for weight reduction and waste reduction which are very important for the manufacturing of aerospace parts for major companies.

In rapidly innovating medical industries, the utilization of additive manufacturing products is of great advantage for doctors, patients and research institutions. Through functional prototype design provided by additive manufacturing technologies, it has been of great advantage to create a flexible design of various design lifesaving tools needed for surgical and study purposes, tools used in the dental procedure, pre-surgery models for CT scans, custom saw and drill guides, enclosure and specialized instrumentation.

- Easy customization and bulk production using additive manufacturing

Additive manufacturing customization, unlike traditional manufacturing, doesn’t add additional cost for customization and doesn’t require any certain mold or tools for the design it just needs a prototype 3D design and can be created by the customer itself because of the easy customization and fast production there is high demand, and we can mass produce any unique design without hampering the cost and time when making use of the 3D printers. Not only does it provide mass customized production, but it also gives the consumer a unique buyer and consumer experience where it gives them the feeling of belongingness and consumer satisfaction as compared to the counterpart who doesn’t provide personalized design. It also allows the consumer to buy the design of their choice. For example, NIKE, a shoe manufacturer, sells its shoes on their website with a 3D design where the consumer can add their colour choice on their own without much hesitation. This will add an advantage to market competition since, through this system, it lets the manufacturer know their client

- Rise in industrialization and advancement in 3D metal printing technology

With the rise in industrialization, there is a huge demand for 3D metal printing products in industries like aerospace, automotive, health care and others industries. With the demand from various fields for parts in aerospace for their jets engine and other structural parts to customize parts in automotive industries to customize the design of shoes and other electronic gadgets there is a demand for the rigorous development of 3D printing technologies which will perform more efficiently and can produce the product at a much faster rate with more precision. So the demand for the advancement and convenience of additive manufacturing technologies lead to an increase in the demand for 3D metal printing technologies.

Opportunities

- Advancement in the healthcare sector

In the medical field, every patient is unique, and therefore additive manufacturing has a high potential to be utilized for personalized and customized medical applications. The most common medical clinical used are personalized implants and medical model saws guides. In dental fields, additive manufacturing products are used in splints, orthodontic appliances, dental models and drill guides. However, additive manufacturing products are also used to make artificial tissues and organs, which can be used for study purposes in a research institute or in between doctor and patients consultation. The development of digitalizing medical imaging that digitalization allows for the reconstruction of 3D models from patients' anatomy. The typical workflow of the personalized medical device starts with imaging or capturing the patient’s geometry of the anatomy using computed 3D scanning methods. Such data can be utilized to print 3D models of a patient’s anatomy or can be used to create personalized devices or implants.

- Increasing government funding to promote additive manufacturing

Additive manufacturing has immense potential to revolutionize the manufacturing and industrial production landscape through digital processes, communication and imaging. Additive manufacturing is a trending business that has high demand from various industries like aerospace, automotive, medical sector, electronics, fashion etc. seeing the potential possibility of this sector's contribution to the nation's economy, governments of different countries are coming up with a different strategy to support and promote this industry.

Restraints/Challenges

- High costs of the equipment, machinery and lack of skilled professional

The benefits that additive manufacturing provides have opened wide horizons for creating absolutely any 3D shapes and components. But not every business does not have the capacity to affordably integrate this type of activity into their business processes. Some of the most common causes that hinder the future of additive manufacturing are the high cost of equipment and the lack of professionals in this industry.

The average price for additive manufacturing equipment is between USD 300,000 to USD 1.5 million. The industrial consumables cost varies from USD 100 to USD 150 per piece. Although, the final price depends on the chosen material, such as plastic, which is considered the most budget-friendly option among all other materials available. The time required is also quite high as it takes more than an hour to print a 40cm object.

- Lack of software efficiency

Additive manufacturing using the laser powder-bed fusion (PBF) process has the ability to build complex and intricate shapes along with organic structures which were previously too expensive or complex to make using traditional manufacturing operations. For example, the design freedoms achieved by laser PBF could be exploited to lightweight components to build the most intricate lattice structures for more efficient material usage. But, laser PBF has its disadvantages. It includes thin-walled/high-aspect-ratio parts that might fail during a build, difficult-to-remove support structures, layering effects on surface roughness and different process parameter settings such as laser settings for up-skin versus down-skin surfaces.

Recent Development

- In February, SLM Solutions launched the SLM.Quality. It is a quality assurance software solution that enables customers to perform build job evaluations and process qualifications and part certifications more efficiently. Whether it's for single part or series production, the SLM. Quality solutions can support industrial customers during the qualification process, improving the traceability and documentation of key process data. This development will help the company to attract more customers.

- In February, SLM Solutions and Assembrix jointly announced the successful integration of the Assembrix VMS software with SLM Solutions machines across the globe. This new partnership will meet the growing demand by OEMs for secure distributed additive manufacturing and enable the creation of a reliable, international additive manufacturing ecosystem.

North America Additive Manufacturing Market Scope

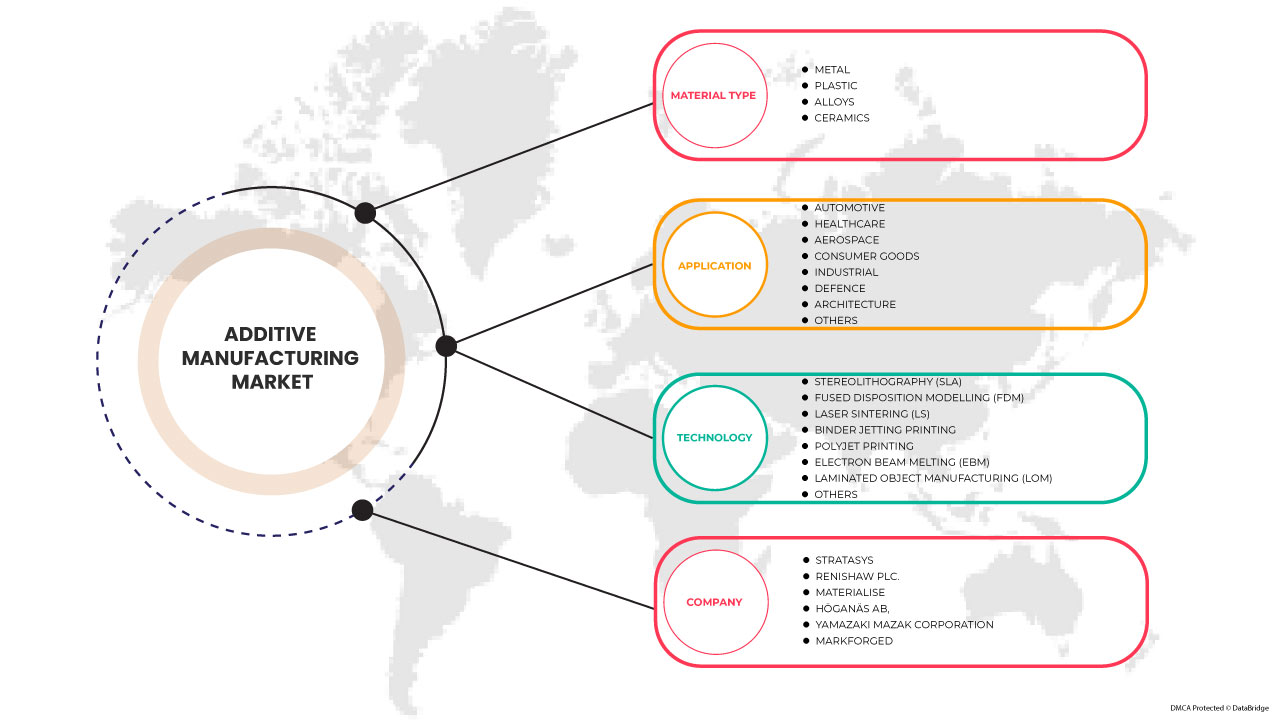

The North America additive manufacturing market is categorized based on material type, technology, and application. The growth amongst these segments will help you analyze major growth segments in the industries and provide the users with a valuable market overview and market insights to make strategic decisions to identify core market applications.

Material Type

- Metals

- Plastics

- Alloys

- Ceramics

On the basis of material type, the North America additive manufacturing market is classified into five segments metals, plastics, alloys, and ceramics,.

Technologies

- Stereolithography (SLA)

- Fused Disposition Modelling (FDM)

- Laser Sintering (LS)

- Binder Jetting Printing

- Polyjet Printing

- Electron Beam Melting (EBM)

- Laminated Object Manufacturing (LOM)

- Others

On the basis of technology, the North America additive manufacturing market is classified into eight Segments Stereolithography (SLA), Fused Disposition Modelling (FDM), Laser Sintering (LS), Binder Jetting printing, Polyjet printing, Electron Beam Melting (EBM), Laminated Object Manufacturing (LOM), and others.

Application

- Automotive

- Healthcare

- Aerospace

- Consumer Goods

- Industrial

- Defence

- Architecture

- Others

On the basis of application, the North America additive manufacturing market is classified into eight segments healthcare, aerospace, consumer goods, industrial, defence, architecture, and others.

North America Additive Manufacturing Market Regional Analysis/Insights

The North America Additive manufacturing market is segmented on the basis of material type technology and applications.

The countries in the North America additive manufacturing market are the U.S., Canada, and Mexico, where the USA is the leading market in the region.

The country section of the report also provides individual market-impacting factors and changes in market regulation that impact the current and future trends of the market. Data point downstream and upstream value chain analysis, technical trends, porter's five forces analysis, and case studies are some of the pointers used to forecast the market scenario for individual countries. Also, the presence and availability of North America brands and their challenges faced due to large or scarce competition from local and domestic brands, the impact of domestic tariffs, and trade routes are considered while providing forecast analysis of the country data.

Competitive Landscape and North America Additive Manufacturing Market Share Analysis

North America additive manufacturing market competitive landscape provides details by competitors. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, production sites and facilities, company strengths and weaknesses, product launch, product trials pipelines, product approvals, patents, product width and breadth, application dominance, technology lifeline curve. The above data points provided are only related to the companies’ focus related to the North America Additive manufacturing market.

Some of the prominent participants operating in the North America additive manufacturing market are SLM Solutions, Proto Labs, Stratasys, Renishaw plc., Materialise, Titomic Limited., Höganäs AB, YAMAZAKI MAZAK CORPORATION, Markforged, Ultimaker BV, Optomec, Inc., ExOne. (A Subsidiary of Desktop Metal, Inc.), American Additive Manufacturing LLC, ANSYS, Inc., ARBURG GmbH + Co KG, ENVISIONTEC US LLC, EOS, and 3D Systems, Inc., among others.

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

목차

1 서론

1.1 연구 목적

1.2 시장 정의

1.3 북미 적층 제조 시장 개요

1.4 제한 사항

1.5 대상 시장

2 시장 세분화

2.1 대상 시장

2.2 지리적 범위

연구에 2.3년이 고려됨

2.4 통화 및 가격

2.5 DBMR TRIPOD 데이터 검증 모델

2.6 유형 라이프라인 곡선

2.7 다변량 모델링

2.8 주요 여론 선도자와의 1차 인터뷰

2.9 DBMR 시장 위치 그리드

2.1 시장 적용 범위 그리드

2.11 DBMR 시장 도전 매트릭스

2.12 DBMR 공급업체 점유율 분석

2.13 2차 소스

2.14 가정

3 요약

4가지 프리미엄 인사이트

4.1 포터의 5가지 힘:

4.1.1 신규 진입자의 위협:

4.1.2 대체품 위협:

4.1.3 고객 협상력:

4.1.4 공급업체 협상력:

4.1.5 내부 경쟁(경쟁):

4.2 생산 소비 분석

4.3 제조업체의 기술적 진보

4.4 공급망 분석

5 규제 프레임워크

6 시장 개요

6.1 드라이버

6.1.1 자동차 및 항공우주 산업에서 경량 부품에 대한 수요 증가

6.1.2 다양한 최종 사용자 산업에서 적층 제조가 제공하는 이점

6.1.3 적층 제조를 사용한 쉬운 사용자 정의 및 대량 생산

6.1.4 산업화의 증가와 3D 금속 인쇄 기술의 발전

6.2 제약

6.2.1 장비, 기계의 높은 비용 및 숙련된 전문가의 부족

6.2.2 소프트웨어 효율성 부족

6.3 기회

6.3.1 의료 분야의 발전

6.3.2 적층 제조 촉진을 위한 정부 자금 지원 증가

6.4 과제

6.4.1 자재 가용성, 개발, 검증 및 표준화와 관련된 문제

6.4.2 소규모 및 중규모 제조업체의 프로토타입 제작 프로세스에 대한 오해

7 북미 적층 제조 시장, 재료 유형별

7.1 개요

7.2 금속

7.2.1 재료 유형별 금속

7.2.1.1 강철

7.2.1.2 알루미늄(알루미드)

7.2.1.3 티타늄

7.2.1.4 실버

7.2.1.5 골드

7.2.1.6 기타

7.3 플라스틱

7.3.1 재료 유형별 플라스틱

7.3.1.1 아크릴로니트릴 부타디엔 스티렌

7.3.1.2 폴리락틱산(PLA)

7.3.1.3 나일론

7.3.1.4 광중합체

7.3.1.5 기타

7.3.2 기타, 재료 유형별

7.3.2.1 폴리프로필렌

7.3.2.2 고밀도 폴리에틸렌

7.3.2.3 폴리카보네이트

7.3.2.4 폴리비닐알코올

7.4 합금

7.4.1 재료 유형별 합금

7.4.1.1 공구강 및 마르게이징강

7.4.1.2 상업적으로 순수한 티타늄 및 합금

7.4.1.3 알루미늄 합금

7.4.1.4 니켈 기반 합금

7.4.1.5 코발트-크롬 합금

7.4.1.6 구리 기반 합금

7.5 세라믹

7.5.1 재료 유형별 세라믹

7.5.1.1 유리

7.5.1.2 실리카

7.5.1.3 석영

7.5.1.4 기타

8 북미 적층 제조 시장, 기술별

8.1 개요

8.2 입체석판술(SLA)

8.3 융합 처리 모델링(FDM)

8.4 레이저 소결(LS)

8.4.1 기술에 따른 레이저 소결(LS)

8.4.1.1 선택적 레이저 용융(SLM)

8.4.1.2 선택적 레이저 소결(SLS)

8.4.1.3 직접 금속 레이저 소결

8.5 바인더 제트 인쇄

8.6 폴리젯 인쇄

8.7 전자빔 용융(EBM)

8.8 적층 물체 제조(LOM)

8.9 기타

9 북미 적층 제조 시장, 응용 분야별

9.1 개요

9.2 자동차

9.3 건강관리

9.4 항공우주

9.5 소비재

9.6 산업

9.7 방어

9.8 아키텍처

9.9 기타

10 북미 적층 제조 시장, 지역별

10.1 북미

10.1.1 미국

10.1.2 캐나다

10.1.3 멕시코

11 북미 적층 제조 시장: 회사 환경

11.1 회사 점유율 분석: 북미

11.2 인증

11.3 성과

11.4 출시

11.5 합병

12 SWOT 분석

13 회사 프로필

13.1 앤시스 주식회사

13.1.1 회사 스냅샷

13.1.2 수익 분석

13.1.3 회사 점유율 분석

13.1.4 제품 포트폴리오

13.1.5 최근 업데이트

13.2 호가네스 아브

13.2.1 회사 스냅샷

13.2.2 회사 점유율 분석

13.2.3 제품 포트폴리오

13.2.4 최근 업데이트

13.3 이오스

13.3.1 회사 스냅샷

13.3.2 회사 점유율 분석

13.3.3 제품 포트폴리오

13.3.4 최근 업데이트

13.4 아르부르크 GMBH + CO KG

13.4.1 회사 스냅샷

13.4.2 회사 점유율 분석

13.4.3 제품 포트폴리오

13.4.4 최근 업데이트

13.5 스트라타시스

13.5.1 회사 스냅샷

13.5.2 수익 분석

13.5.3 회사 점유율 분석

13.5.4 제품 포트폴리오

13.5.5 최근 업데이트

13.6 미국 첨가 제조 유한회사

13.6.1 회사 스냅샷

13.6.2 제품 포트폴리오

13.6.3 최근 업데이트

13.7 엔비전텍 US 유한회사

13.7.1 회사 스냅샷

13.7.2 제품 포트폴리오

13.7.3 최근 업데이트

13.8 EXONE. (DESKTOP METAL, INC.의 자회사)

13.8.1 회사 스냅샷

13.8.2 수익 분석

13.8.3 제품 포트폴리오

13.8.4 최근 업데이트

13.9 물질화

13.9.1 회사 스냅샷

13.9.2 수익 분석

13.9.3 제품 포트폴리오

13.9.4 최근 업데이트

13.1 마크포지드

13.10.1 회사 스냅샷

13.10.2 수익 분석

13.10.3 제품 포트폴리오

13.10.4 최근 업데이트

13.11 옵토멕 주식회사

13.11.1 회사 스냅샷

13.11.2 제품 포트폴리오

13.11.3 최근 업데이트

13.12 프로토랩스

13.12.1 회사 스냅샷

13.12.2 수익 분석

13.12.3 제품 포트폴리오

13.12.4 연례 보고서 및 SEC 제출최근 업데이트

13.13 레니쇼 PLC.

13.13.1 회사 스냅샷

13.13.2 수익 분석

13.13.3 제품 포트폴리오

13.13.4 최근 업데이트

13.14 SLM 솔루션

13.14.1 회사 스냅샷

13.14.2 수익 분석

13.14.3 제품 포트폴리오

13.14.4 최근 업데이트

13.15 티토믹 리미티드.

13.15.1 회사 스냅샷

13.15.2 수익 분석

13.15.3 제품 포트폴리오

13.15.4 최근 업데이트

13.16 얼티메이커 BV

13.16.1 회사 스냅샷

13.16.2 제품 포트폴리오

13.16.3 최근 업데이트

13.17 야마자키 마작 주식회사

13.17.1 회사 스냅샷

13.17.2 제품 포트폴리오

13.17.3 최근 업데이트

13.18 3D시스템 주식회사

13.18.1 회사 스냅샷

13.18.2 수익 분석

13.18.3 제품 포트폴리오

13.18.4 최근 업데이트

14 설문지

15 관련 보고서

표 목록

표 1 규제 프레임워크

표 2 북미 적층 제조 시장, 재료 유형별, 2021-2030년(백만 달러)

표 3 지역별 적층 제조 시장의 북미 금속, 2021-2030년(백만 달러)

표 4 재료 유형별 적층 제조 시장에서 북미 금속, 2021-2030년(백만 달러)

표 5 북미 플라스틱 적층 제조 시장, 지역별, 2021-2030 (백만 달러)

표 6 재료 유형별 적층 제조 시장에서 북미 플라스틱, 2021-2030년(백만 달러)

표 7 재료 유형별 적층 제조 시장의 북미 기타 국가, 2021-2030년(백만 달러)

표 8 지역별 적층 제조 시장에서의 북미 합금, 2021-2030년(백만 달러)

표 9 재료 유형별 적층 제조 시장에서의 북미 합금, 2021-2030년(백만 달러)

표 10 지역별 적층 제조 시장에서의 북미 세라믹스, 2021-2030년(백만 달러)

표 11 재료 유형별 적층 제조 시장에서의 북미 세라믹, 2021-2030년(백만 달러)

표 12 기술별 북미 적층 제조 시장, 2021-2030년(백만 달러)

표 13 지역별 적층 제조 시장에서의 북미 스테레오리소그래피(SLA), 2021-2030년(백만 달러)

표 14 지역별 적층 제조 시장에서의 북미 융합 처분 모델링(FDM), 2021-2030년(백만 달러)

표 15 지역별 적층 제조 시장에서의 북미 레이저 소결(LS), 2021-2030(백만 달러)

표 16 기술별 적층 제조 시장에서의 북미 레이저 소결(LS), 2021-2030년(백만 달러)

표 17 2021-2030년 지역별 적층 제조 시장에서의 북미 바인더 제트 인쇄(백만 달러)

표 18 지역별 적층 제조 시장에서의 북미 폴리젯 인쇄, 2021-2030년(백만 달러)

표 19 2021-2030년 지역별 적층 제조 시장에서의 북미 전자빔 용융(EBM) (백만 달러)

표 20 지역별 적층 제조 시장에서의 북미 적층 물체 제조(LOM), 2021-2030년(백만 달러)

표 21 북미 기타 지역별 적층 제조 시장, 2021-2030년(백만 달러)

표 22 북미 적층 제조 시장, 응용 분야별, 2021-2030년(백만 달러)

표 23 지역별 북미 자동차 적층 제조 시장, 2021-2030년(백만 달러)

표 24 지역별 적층 제조 시장의 북미 헬스케어, 2021-2030년(백만 달러)

표 25 지역별 적층 제조 시장에서의 북미 항공우주 산업, 2021-2030년(백만 달러)

표 26 지역별 적층 제조 시장의 북미 소비재, 2021-2030년(백만 달러)

표 27 지역별 북미 산업용 적층 제조 시장, 2021-2030년(백만 달러)

표 28 지역별 적층 제조 시장에서의 북미 방위, 2021-2030년(백만 달러)

표 29 지역별 적층 제조 시장의 북미 아키텍처, 2021-2030년(백만 달러)

표 30 북미 기타 지역별 적층 제조 시장, 2021-2030년(백만 달러)

표 31 북미 적층 제조 시장, 국가별, 2021-2030년(백만 달러)

표 32 북미 적층 제조 시장, 재료 유형별, 2021-2030년(백만 달러)

표 33 재료 유형별 적층 제조 시장에서 북미 금속, 2021-2030년(백만 달러)

표 34 재료 유형별 적층 제조 시장에서의 북미 플라스틱, 2021-2030년(백만 달러)

표 35 재료 유형별 적층 제조 시장의 북미 기타, 2021-2030년(백만 달러)

표 36 재료 유형별 적층 제조 시장의 북미 합금, 2021-2030년(백만 달러)

표 37 재료 유형별 적층 제조 시장에서의 북미 세라믹, 2021-2030년(백만 달러)

표 38 기술별 북미 적층 제조 시장, 2021-2030년(백만 달러)

표 39 기술별 적층 제조 시장에서의 북미 레이저 소결(LS), 2021-2030년(백만 달러)

표 40 북미 적층 제조 시장, 응용 분야별, 2021-2030년(백만 달러)

표 41 미국 적층 제조 시장, 재료 유형별, 2021-2030년(백만 달러)

표 42 재료 유형별 적층 제조 시장의 미국 금속, 2021-2030년(백만 달러)

표 43 미국 플라스틱 적층 제조 시장, 재료 유형별, 2021-2030 (백만 달러)

표 44 재료 유형별 적층 제조 시장의 미국 기타 기업, 2021-2030년(백만 달러)

표 45 재료 유형별 적층 제조 시장의 미국 합금, 2021-2030년(백만 달러)

표 46 재료 유형별 적층 제조 시장에서의 미국 세라믹, 2021-2030년(백만 달러)

표 47 기술별 미국 적층 제조 시장, 2021-2030년(백만 달러)

표 48 기술별 적층 제조 시장에서의 미국 레이저 소결(LS), 2021-2030년(백만 달러)

표 49 미국 적층 제조 시장, 응용 분야별, 2021-2030년(백만 달러)

표 50 캐나다 적층 제조 시장, 재료 유형별, 2021-2030 (백만 달러)

표 51 재료 유형별 적층 제조 시장에서의 캐나다 금속, 2021-2030년(백만 달러)

표 52 재료 유형별 적층 제조 시장에서의 캐나다 플라스틱, 2021-2030년(백만 달러)

표 53 재료 유형별 적층 제조 시장의 캐나다 기타 국가, 2021-2030년(백만 달러)

표 54 재료 유형별 적층 제조 시장에서의 캐나다 합금, 2021-2030년(백만 달러)

표 55 재료 유형별 적층 제조 시장에서의 캐나다 세라믹, 2021-2030년(백만 달러)

표 56 캐나다 적층 제조 시장, 기술별, 2021-2030 (백만 달러)

표 57 기술별 적층 제조 시장에서의 캐나다 레이저 소결(LS), 2021-2030(백만 달러)

표 58 캐나다 적층 제조 시장, 응용 분야별, 2021-2030년(백만 달러)

표 59 멕시코 적층 제조 시장, 재료 유형별, 2021-2030년(백만 달러)

표 60 멕시코 금속 적층 제조 시장, 재료 유형별, 2021-2030 (백만 달러)

표 61 멕시코 플라스틱 적층 제조 시장, 재료 유형별, 2021-2030 (백만 달러)

표 62 멕시코 기타 재료 유형별 적층 제조 시장, 2021-2030년(백만 달러)

표 63 멕시코 합금, 재료 유형별 적층 제조 시장, 2021-2030 (백만 달러)

표 64 멕시코 세라믹스 적층 제조 시장, 재료 유형별, 2021-2030(백만 달러)

표 65 멕시코 적층 제조 시장, 기술별, 2021-2030 (백만 달러)

표 66 멕시코 레이저 소결(LS) 적층 제조 시장, 기술별, 2021-2030(백만 달러)

표 67 멕시코 적층 제조 시장, 응용 분야별, 2021-2030년(백만 달러)

그림 목록

그림 1 북미 적층 제조 시장

그림 2 북미 적층 제조 시장: 데이터 삼각 측량

그림 3 북미 적층 제조 시장: DROC 분석

그림 4 북미 적층 제조 시장: 북미 대 지역 시장 분석

그림 5 북미 적층 제조 시장: 회사 연구 분석

그림 6 북미 적층 제조 시장: 유형 수명선 곡선

그림 7 북미 적층 제조 시장: 다변량 모델링

그림 8 북미 적층 제조 시장: 인터뷰 인구 통계

그림 9 북미 적층 제조 시장: DBMR 시장 위치 그리드

그림 10 북미 적층 제조 시장: 시장 최종 사용자 적용 범위 그리드

그림 11 북미 적층 제조 시장: 시장 과제 매트릭스

그림 12 북미 적층 제조 시장: 공급업체 점유율 분석

그림 13 북미 적층 제조 시장: 세분화

그림 14 자동차 및 항공우주 산업의 경량 구성품에 대한 수요 증가가 예측 기간 동안 북미 적층 제조 시장을 주도할 것으로 예상됩니다.

그림 15 금속 세그먼트는 2022년 및 2029년에 북미 적층 제조 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다.

그림 16 북미 적층 제조 시장의 동인, 제약, 기회 및 과제

그림 17 북미 적층 제조 시장: 재료 유형별, 2022년

그림 18 북미 적층 제조 시장: 기술별, 2022년

그림 19 북미 적층 제조 시장: 응용 분야별, 2022년

그림 20 북미 적층 제조 시장: 스냅샷(2022)

그림 21 북미 적층 제조 시장: 국가별(2022년)

그림 22 북미 적층 제조 시장: 국가별(2023년 및 2030년)

그림 23 북미 적층 제조 시장: 국가별(2022년 및 2030년)

그림 24 북미 적층 제조 시장: 재료 유형별(2023-2030)

그림 25 북미 적층 제조 시장: 회사 점유율 2022(%)

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.