Global Bio Based Polymer Additives Market

Tamanho do mercado em biliões de dólares

CAGR :

%

USD

4.90 Billion

USD

9.14 Billion

2025

2033

USD

4.90 Billion

USD

9.14 Billion

2025

2033

| 2026 –2033 | |

| USD 4.90 Billion | |

| USD 9.14 Billion | |

| % | |

|

Segmentação de Mercado de Aditivos de Polímeros Biobaseados Globais, por Produto (Plasticizadores, Estabilizadores, Lubrificantes, Retardadores de Chamas, Enchimentos e Reforços, Aditivos Antimicrobiais, Outros), Fonte (Plant-based, Biofermentation, Waste-derived), Tipo de Polímero (PE, PP, PLA, PHA, PET, Outros), Aplicação (Pacote, Automotivo, Bens de Consumo, Saúde, Agricultura, Outros) – Tendências e Previsão da Indústria a 2033Global Bio-based Polymer Additives Market Segmentation, By Product (Plasticizers, Stabilizers, Lubricants, Flame Retardants, Fillers & Reforcements, PET, Antimicrobial Additives, Outros), Fonte (Plackaging, Automotive, Biofermentation, Waste-derived), Tipo de Polímeros (PE, PP, PP, PLA, PHA, PHA,

Aditivos de Polímero Bio-basedTamanho do Mercado

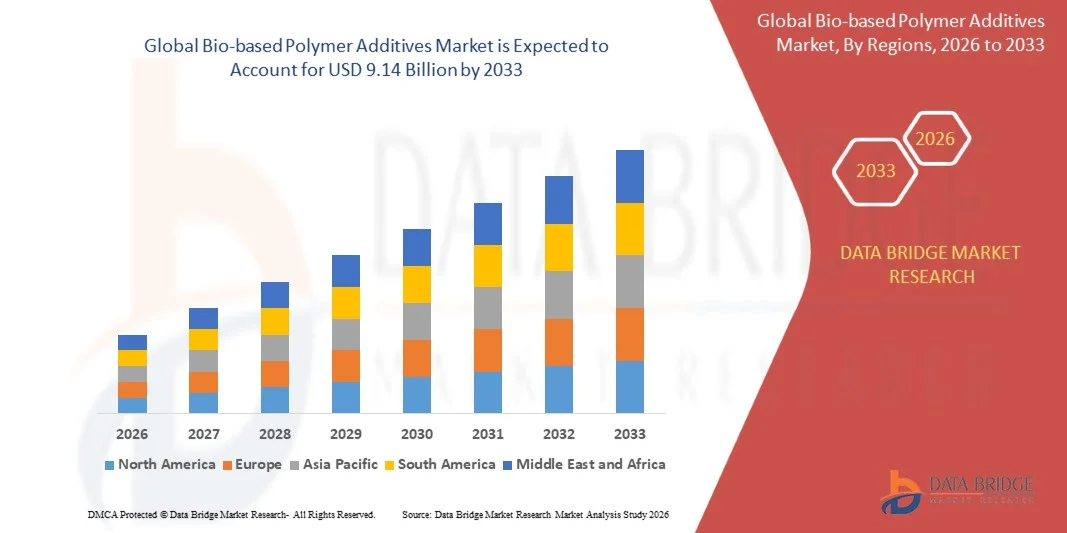

- O tamanho global do mercado de aditivos de polímeros bio-baseados foi avaliado emUSD 4,90 mil milhões em 2025e espera-se alcançar9,14 mil milhões de USD até 2033, emCAGR de 8,1%durante o período de previsão

- O crescimento do mercado é impulsionado principalmente pela crescente demanda por materiais sustentáveis e ecológicos entre as indústrias de embalagens, automóveis e bens de consumo, juntamente com regulamentos ambientais rigorosos que limitam o uso de aditivos convencionais à base de petróleo e a ênfase crescente na redução da pegada de carbono em economias desenvolvidas e emergentes

- Além disso, a adoção crescente de polímeros biodegradáveis e bio-baseados, avanços em tecnologias de química verde e investimentos crescentes em iniciativas de economia circular estão posicionando aditivos de polímeros bio-baseados como componentes críticos em soluções de materiais de próxima geração, acelerando significativamente o crescimento global do mercado

Aditivos de Polímero Bio-basedAnálise de mercado

- Os aditivos de polímeros bio-baseados, que melhoram as propriedades do material, como flexibilidade, durabilidade, estabilidade térmica e biodegradabilidade, estão se tornando componentes essenciais na fabricação de plástico sustentável nas indústrias de embalagens, automóveis, construção e bens de consumo, devido à sua natureza eco-friendly e conformidade com as regulamentações ambientais

- A crescente demanda por aditivos polímeros de base biológica é impulsionada principalmente pelo aumento das restrições regulatórias aos aditivos à base de petróleo, aumento da preferência do consumidor por produtos sustentáveis e adoção crescente de polímeros biodegradáveis e recicláveis, juntamente com compromissos corporativos em relação à neutralidade de carbono e práticas econômicas circulares

- A Europa dominou o mercado dos aditivos de polímeros à base de bio-base com a maior quota de receitas de 38,42% em 2025, apoiada por regulamentos ambientais rigorosos, forte apoio político aos materiais à base de bio-base e adoção precoce de soluções de embalagem sustentáveis, com países como Alemanha e França liderando a inovação e o consumo

- A Ásia-Pacífico deverá ser a região de crescimento mais rápido no mercado de aditivos de polímeros bio-baseados durante o período de previsão devido à rápida industrialização, aumento do consumo de plástico, aumento da conscientização ambiental e expansão de iniciativas governamentais que promovam materiais de base biológica em economias emergentes, como China e Índia

- O segmento de plastificantes dominou o mercado de aditivos de polímeros bio-baseados com uma quota de mercado de 30,35% em 2025, impulsionado pela alta demanda por flexibilidade e aprimoramento de desempenho em filmes de embalagem, componentes automotivos e produtos de consumo, juntamente com a crescente mudança para alternativas de plastificantes não tóxicos e bio-baseados.

Âmbito do relatório eAditivos de Polímero Bio-basedSegmentação do mercado

|

Atributos |

Aditivos de Polímero Bio-basedChavePerspectivas de mercado |

|

Segmentos Cobertos |

|

|

Países abrangidos |

América do Norte · U.S. · Canadá · México Europa · Alemanha · França · U.K. · Países Baixos · Suíça · Bélgica · Rússia · Itália · Espanha · Turquia · Resto da Europa Ásia- Pacífico · China · Japão · Índia · Coreia do Sul · Singapura · Malásia · Austrália · Tailândia · Indonésia · Filipinas · Resto da Ásia-Pacífico Médio Oriente e África · Arábia Saudita · U.A.E. · África do Sul · Egito · Israel · Resto do Oriente Médio e África América do Sul · Brasil · Argentina · Resto da América do Sul |

|

Jogadores do mercado chave |

· BASF SE (Alemanha) · Dow Inc. (EUA) · Evonik Industries AG (Alemanha) · Arkema S.A. (França) · Clariant AG (Suíça) · LANXESS AG (Alemanha) · Solvay S.A. (Bélgica) · LyondellBasell Industries N.V. (Países Baixos) · Avient Corporation (EUA) · Croda International Plc (U.K.) · ADEKA Corporation (Japão) · Songwon Industrial Co. Ltd. (Coreia do Sul) · Nouryon (Países Baixos) · Emery Oleochemicals (Malásia) · Cargill Incorporated (EUA) · Corbion N.V. (Países Baixos) · NatureWorks LLC (EUA) · Braskem S.A. (Brasil) · Novamont S.p.A. (Itália) · Palsgaard A/S (Dinamarca) |

|

Oportunidades de Mercado |

· Aumento da procura de plásticos sustentáveis e biodegradáveis nas indústrias de embalagens, automóveis e bens de consumo · Aumento dos investimentos em inovação de materiais bio-baseados e desenvolvimento de tecnologias avançadas de aditivos eco-friendly |

|

Informações sobre o Valor Adicionado |

Além dos insights sobre cenários de mercado, como valor de mercado, taxa de crescimento, segmentação, cobertura geográfica e principais atores, os relatórios de mercado curados pela Data Bridge Market Research também incluem análise de importação, visão geral da capacidade de produção, análise do consumo de produção, análise de tendências de preços, cenário de mudança climática, análise da cadeia de suprimentos, análise da cadeia de valor, visão geral da matéria-prima/consumíveis, critérios de seleção de fornecedores, Análise de PESTLE, Análise de Porter e quadro regulatório. |

Tendências do mercado de aditivos de polímeros baseados em bio-base

“Shift Toward Sustainable, High-Performance, and Circular Material Solutions”

- Uma tendência significativa e acelerada no mercado global de aditivos de polímeros bio-baseados é a crescente mudança para soluções sustentáveis, de alto desempenho e de materiais amigos do meio ambiente que melhoram a funcionalidade do polímero, reduzindo o impacto ambiental em várias indústrias de uso final.

- Por exemplo, empresas como a BASF SE e a Evonik Industries AG estão cada vez mais desenvolvendo plastificantes e estabilizadores bio-baseados derivados de matérias-primas renováveis para substituir aditivos convencionais à base de petróleo em embalagens e aplicações automotivas.

- Avanços tecnológicos em química verde estão permitindo o desenvolvimento de aditivos bio-baseados com maior estabilidade térmica, durabilidade e compatibilidade com uma ampla gama de polímeros, ajudando os fabricantes a manter o desempenho ao atingir metas de sustentabilidade.

- A adoção crescente de plásticos biodegradáveis e compostáveis, incluindo PLA e PHA, está apoiando a demanda de aditivos bio-base compatíveis que melhorem a eficiência de processamento e o desempenho do produto final.

- Essa tendência para aditivos ecológicos e de alta eficiência está reformulando as expectativas da indústria em relação à conformidade regulatória, desempenho do produto e sustentabilidade do ciclo de vida nos setores de embalagens, construção e bens de consumo.

- A demanda por aditivos avançados à base de bio-base, com maior funcionalidade e redução da pegada de carbono, está crescendo rapidamente em economias desenvolvidas e emergentes, impulsionadas por compromissos de sustentabilidade corporativa e mandatos regulatórios.

- A adoção crescente de soluções de materiais recicláveis e circulares está ganhando força devido à pressão crescente para minimizar o desperdício de plástico e melhorar a eficiência de recursos em cadeias de valor globais.

Dinâmica de Mercado de Aditivos de Polímeros Biobaseados

Controlador

“Demanda crescente para materiais sustentáveis e impulso regulatório para alternativas verdes”

- A crescente procura de materiais sustentáveis e respeitadores do ambiente, juntamente com regulamentos rigorosos que limitem o uso de aditivos plásticos convencionais, é um importante motor para o crescimento do mercado mundial de aditivos de polímeros bio-baseados

- Por exemplo, os quadros regulamentares em regiões como a União Europeia estão a promover a adopção de aditivos bio-baseados e não tóxicos para reduzir o impacto ambiental e melhorar a reciclagem de produtos plásticos

- À medida que as indústrias se concentram mais na redução das emissões de carbono e na consecução de metas de sustentabilidade, os aditivos de polímero bio-baseados oferecem fontes renováveis, menor toxicidade e melhor desempenho ambiental em comparação com os aditivos tradicionais

- Além disso, a crescente mudança para embalagens sustentáveis e design de produtos eco-friendly, apoiada pela conscientização dos consumidores e iniciativas de ESG corporativas, está aumentando a adoção de aditivos de base biológica entre as indústrias

- A compatibilidade destes aditivos com as técnicas de processamento de polímeros existentes e a sua capacidade de melhorar o desempenho dos materiais são factores fundamentais para a adopção generalizada nos sectores de fabrico

- A expansão da industrialização e a crescente procura de materiais sustentáveis nas economias emergentes estão a apoiar ainda mais a expansão do mercado

- Incentivos governamentais e políticas favoráveis de promoção de indústrias de base biológica estão acelerando investimentos e comercialização de soluções avançadas de aditivos

Restrição/Desafio

“Limitações de alto custo e desempenho em comparação com aditivos convencionais”

- Os desafios relacionados com o custo mais elevado dos aditivos bio-baseados e as limitações de desempenho em determinadas aplicações colocam obstáculos significativos à adopção em larga escala, nomeadamente em mercados sensíveis aos preços.

- Por exemplo, os aditivos à base de bio-base envolvem frequentemente processos de produção complexos e dependência de matérias-primas agrícolas, conduzindo a custos de produção mais elevados do que os aditivos convencionais à base de petroquímica.

- Enfrentar esses desafios através de avanços tecnológicos, otimização de processos e economias de escala é fundamental para melhorar a competitividade dos custos e a penetração no mercado. Embora a procura de materiais sustentáveis esteja a aumentar, o desempenho inconsistente em aplicações de alta temperatura ou de alta tensão pode limitar a sua utilização em certos sectores industriais.

- Superar esses desafios através de inovação contínua, técnicas de formulação melhoradas e propriedades de materiais aprimorados será essencial para o crescimento do mercado a longo prazo. A disponibilidade limitada e a volatilidade dos preços das matérias-primas biobaseadas podem ter impacto na estabilidade da cadeia de abastecimento e no planeamento da produção

- Normas regulatórias rigorosas e requisitos de certificação para alegações de conteúdo e sustentabilidade bio-baseados podem aumentar os custos de conformidade e atrasar a comercialização de produtos

Âmbito de mercado dos aditivos de polímeros bio-baseados

O mercado é segmentado com base em produto, fonte, tipo de polímero e aplicação.

- Por Produto

Com base no produto, o mercado global de aditivos de polímeros bio-baseados é segmentado em plastificantes, estabilizadores, lubrificantes, retardantes de chama, cargas e agentes de reforço, aditivos antimicrobianos, entre outros. O segmento de plastificantes dominou o mercado com a maior parcela de receita de 30,35% em 2025, impulsionada pelo seu amplo uso no aumento da flexibilidade, durabilidade e eficiência de processamento de polímeros entre as indústrias de embalagens, automóveis e bens de consumo. Os plastificantes de base biológica estão a substituir cada vez mais as alternativas convencionais baseadas em ftalato, devido a regulamentações ambientais rigorosas e crescentes preocupações de saúde. Sua compatibilidade com polímeros amplamente utilizados, como polietileno e polipropileno, juntamente com um balanço favorável de custo-desempenho, suporta sua adoção generalizada. Avanços contínuos em formulações não tóxicas e de alto desempenho estão fortalecendo ainda mais a dominância do segmento.

Espera-se que o segmento estabilizador testemunhe o crescimento mais rápido durante o período de previsão, alimentado pela crescente demanda por maior estabilidade térmica, resistência UV e maior ciclo de vida do produto em aplicações plásticas sustentáveis. O uso crescente em materiais externos, filmes de embalagem e componentes automotivos está impulsionando a adoção. As inovações tecnológicas em antioxidantes e estabilizadores de luz derivados de fontes renováveis estão melhorando a eficiência e ampliando o escopo de aplicação, acelerando ainda mais o crescimento global dos segmentos.

- Por Fonte

Com base na fonte, o mercado é segmentado em matéria-prima vegetal, derivada de biofermentação e derivada de resíduos/reciclada. O segmento de base vegetal representou a maior parcela de receita de mercado de 55,8% em 2025, impulsionada pela disponibilidade abundante de matérias-primas renováveis, como óleos vegetais, amido e celulose. Essas matérias-primas são amplamente utilizadas devido à sua custo-efetividade, escalabilidade e cadeias de abastecimento estabelecidas. A crescente demanda por materiais sustentáveis nas indústrias de embalagens e bens de consumo, juntamente com políticas governamentais favoráveis que promovam recursos bio-baseados, está apoiando ainda mais o domínio do segmento.

Prevê-se que o segmento de biofermentação registe o crescimento mais rápido ao longo do período de previsão, devido aos avanços na biotecnologia e ao aumento da produção de produtos químicos bio-baseados de alto desempenho. Os aditivos à base de fermentação oferecem consistência, pureza e desempenho funcional superiores, tornando-os adequados para aplicações de alto valor. O aumento dos investimentos em biotecnologia industrial e a expansão das infra-estruturas de bio-refinaria apoiam ainda mais o rápido crescimento deste segmento.

- Por tipo de polímero

Com base no tipo de polímero, o mercado de aditivos de polímeros bio-baseados é segmentado em polietileno (PE), polipropileno (PP), ácido poliláctico (PLA), polihidroxialcanoatos (PHA), tereftalato de polietileno (PET) e outros. O segmento de polietileno (PE) dominou o mercado com uma parcela de 29,4% em 2025, impulsionada pela sua ampla utilização em embalagens flexíveis, filmes e recipientes. Os aditivos bio-baseados são amplamente utilizados em PE para aumentar a resistência, flexibilidade e desempenho ambiental, especialmente em soluções de embalagem sustentáveis. Altos volumes de consumo e ampla aplicabilidade industrial apoiam sua liderança no mercado.

Espera-se que o segmento PLA e PHA testemunhe o crescimento mais rápido durante o período de previsão, alimentado pelo aumento da adoção de polímeros biodegradáveis e compostáveis em embalagens e aplicações agrícolas. A crescente pressão regulamentar para reduzir os resíduos de plástico e aumentar a preferência dos consumidores por materiais ecológicos está a acelerar a procura destes polímeros bio-baseados. A inovação contínua no aprimoramento do desempenho e redução de custos está impulsionando o crescimento do segmento.

- Por Aplicação

Com base na aplicação, o mercado de aditivos de polímero bio-based é segmentado em embalagens, automotivos, bens de consumo, construção, saúde, agricultura, entre outros. O segmento de embalagens dominou o mercado em 2025 com uma participação de 34,2%, apoiada pela crescente demanda por materiais de embalagem biodegradáveis, recicláveis e sustentáveis em alimentos e bebidas, cuidados pessoais e comércio eletrônico. Os regulamentos ambientais rigorosos e o aumento da sensibilização dos consumidores para a redução dos resíduos de plástico são factores fundamentais para a dominância do segmento. Aditivos baseados em bio-base aumentam a funcionalidade do material, garantindo o cumprimento dos padrões de sustentabilidade, tornando-os amplamente adotados em aplicações de embalagem.

Espera-se que o segmento automotivo testemunhe o crescimento mais rápido durante o período de previsão, impulsionado pelo aumento da demanda por materiais leves e sustentáveis para melhorar a eficiência do combustível e reduzir as emissões. Os aditivos bio-baseados são cada vez mais utilizados em componentes interiores, revestimentos e plásticos de engenharia para melhorar a durabilidade e o desempenho ambiental. A crescente mudança em direção aos veículos elétricos e o foco regulatório na sustentabilidade estão acelerando ainda mais a adoção, enquanto inovações contínuas em bioaditivos de alto desempenho estão expandindo seu uso em aplicações automotivas avançadas.

Análise Regional do Mercado de Aditivos Polímeros Biobaseados

- A Europa dominou o mercado de aditivos de polímeros bio-baseados com a maior quota de receitas de 38,42% em 2025, apoiada por regulamentações ambientais rigorosas, quadros políticos fortes que promovem materiais bio-baseados e adoção precoce de plásticos sustentáveis nas indústrias de embalagens, automóveis e bens de consumo

- Fabricantes e indústrias de uso final na região dão ênfase significativa à sustentabilidade, práticas de economia circular e redução da pegada de carbono, levando à adoção generalizada de aditivos de polímeros bio-baseados em aplicações de produção e processamento de materiais

- Esta forte posição de mercado é ainda apoiada por altos investimentos em química verde, presença de principais fabricantes químicos, como BASF SE e Arkema S.A., e aumento da pressão regulatória para substituir aditivos convencionais, estabelecendo aditivos de polímeros bio-based como componentes essenciais em soluções de materiais sustentáveis de próxima geração entre as indústrias

Insight do mercado de aditivos de polímeros baseados em biocom base nos EUA

O mercado de aditivos de polímeros de base biológica dos EUA capturou a maior parte de receita de 80,82% em 2025 na América do Norte, impulsionada pela forte demanda por materiais sustentáveis nas indústrias de embalagens, automóveis e bens de consumo. Os fabricantes priorizam cada vez mais aditivos eco-friendly para atender as normas regulatórias e metas de sustentabilidade corporativa. A crescente adoção de plásticos biodegradáveis, apoiada por avanços na química verde e na inovação de materiais, continua impulsionando o crescimento do mercado. Além disso, a presença de empresas químicas líderes como a Dow Inc. e a Cargill Incorporated contribui significativamente para uma expansão sustentada do mercado.

Europe Bio-based Polymer Aditives Market Insight

Prevê-se que o mercado europeu de aditivos de polímeros bio-baseados se expanda num CAGR estável ao longo do período previsto, impulsionado principalmente por regulamentações ambientais rigorosas e por um forte apoio político aos materiais bio-baseados. O crescente enfoque nas práticas de economia circular e na redução de resíduos de plástico está acelerando a procura de aditivos sustentáveis. As indústrias europeias enfatizam o design e a reciclagem de produtos ecológicos, promovendo a adoção consistente entre os setores de embalagens, construção e automóveis. O crescimento é apoiado por iniciativas governamentais, quadros regulatórios e ampla disponibilidade de soluções avançadas de base biológica.

U.K. Bio-based Polymer Aditives Market Insight

Prevê-se que o mercado de aditivos de polímeros à base biológica do Reino Unido cresça em um notável CAGR durante o período de previsão, apoiado pelo crescente foco na redução sustentável de embalagens e resíduos plásticos. Aumentar a conscientização sobre o impacto ambiental e um forte impulso regulatório para materiais biodegradáveis estão impulsionando a demanda em todas as indústrias. Os setores de manufatura e varejo bem estabelecidos do país estão adotando aditivos ecológicos para atingir metas de sustentabilidade. Além disso, a expansão das iniciativas de economia circular e os investimentos em materiais verdes aumentam o crescimento do mercado em toda a cadeia de valor.

Alemanha Bio-based Polymer Aditives Market Insight

Espera-se que o mercado de aditivos de polímeros à base de bio-base da Alemanha se expanda em um considerável CAGR durante o período de previsão, impulsionado por forte base industrial e liderança em tecnologias de fabricação sustentáveis. Alta ênfase na conformidade ambiental e engenharia avançada de materiais apoia a adoção de aditivos bio-baseados em indústrias automotivas, de embalagem e de construção. O foco da Alemanha em inovação e materiais de alto desempenho promove o uso de soluções avançadas de aditivos. A integração de materiais bio-baseados se alinha ao compromisso do país com a eficiência energética e metas de redução de carbono.

Visão de mercado de aditivos de polímeros baseados em biomarcas Ásia-Pacífico

O mercado de aditivos de polímero à base de biopolímeros da Ásia-Pacífico está preparado para crescer no CAGR mais rápido durante o período de previsão de 2026 a 2033, impulsionado pela rápida industrialização, aumento do consumo de plástico e aumento da conscientização ambiental em países como China, Índia e Japão. A expansão dos setores de fabricação e a crescente demanda por materiais sustentáveis estão acelerando a adoção. As iniciativas governamentais que promovem as indústrias de base biológica e melhoram as práticas de gestão de resíduos apoiam ainda mais o crescimento do mercado. Além disso, a forte base de produção da região aumenta a acessibilidade e a disponibilidade de aditivos de base biológica.

Japão Bio-based Polymer Aditives Market Insight

O mercado japonês de aditivos de polímeros bio-baseados está ganhando impulso devido ao crescente foco em materiais sustentáveis e tecnologias avançadas de polímeros. Forte ênfase na alta qualidade de fabricação e responsabilidade ambiental está impulsionando a adoção em todas as indústrias de eletrônicos, automotivos e embalagens. O uso crescente de plásticos biodegradáveis e aditivos ecológicos suporta objetivos de sustentabilidade a longo prazo. A integração de soluções materiais inovadoras em processos industriais continua a alimentar o crescimento do mercado em vários setores.

Índia Bio-based Polymer Aditives Market Insight

O mercado indiano de aditivos de polímeros bio-baseados representou uma parte significativa da receita na Ásia-Pacífico em 2025, atribuída à urbanização rápida, ao aumento do consumo de plástico e à crescente conscientização da sustentabilidade ambiental. A expansão da população de classe média e a crescente demanda por mercadorias empacotadas estão impulsionando a adoção de materiais sustentáveis. Os aditivos bio-baseados são cada vez mais utilizados nas indústrias de embalagens, agricultura e bens de consumo devido à sua relação custo-eficácia e disponibilidade. Iniciativas governamentais como as regras de gestão de resíduos plásticos e promoção de indústrias de base biológica são fatores fundamentais para a expansão sustentada do mercado na Índia.

Aditivos de Polímero Biobaseados Market Share

A indústria de aditivos de polímeros bio-baseados é liderada principalmente por empresas bem estabelecidas, incluindo:

- BASF SE (Alemanha)

- Dow Inc. (EUA)

- Evonik Industries AG (Alemanha)

- Arkema S.A. (França)

- Clariant AG (Suíça)

- LANXESS AG (Alemanha)

- Solvay S.A. (Bélgica)

- LyondellBasell Industries N.V. (Países Baixos)

- Avient Corporation (EUA)

- Croda International Plc (U.K.)

- ADEKA Corporation (Japão)

- Songwon Industrial Co. Ltd (Coreia do Sul)

- Nouryon (Países Baixos)

- Emery Oleochemicals (Malásia)

- Cargill Incorporated (EUA)

- Corbion N.V. (Países Baixos)

- NatureWorks LLC (EUA)

- Braskem S.A. (Brasil)

- Novamont S.p.A. (Itália)

- Palsgaard A/S (Dinamarca)

Quais são os desenvolvimentos recentes no mercado global de aditivos de polímeros baseados em bio

- Em dezembro de 2025, a BASF SE expandiu seu portfólio de plastificantes bio-baseados, introduzindo novos aditivos derivados de matérias-primas renováveis, visando melhorar a flexibilidade e sustentabilidade em embalagens e aplicações automotivas, reduzindo a dependência de materiais fósseis

- Em outubro de 2025, a Evonik Industries AG anunciou avanços em estabilizadores e aditivos de base biológica, com foco em aumentar a estabilidade térmica e durabilidade dos polímeros usados em aplicações de alto desempenho e sustentáveis em várias indústrias

- Em agosto de 2025, a Arkema S.A. reforçou seu segmento de materiais bio-baseados através do desenvolvimento de aditivos avançados para polímeros biodegradáveis, apoiando iniciativas de economia circular e aumentando a adoção em soluções de embalagem sustentáveis

- Em junho de 2025, a Cargill Incorporated expandiu seu portfólio bioindustrial lançando novas soluções de aditivos vegetais derivados de óleos vegetais, visando aplicações em embalagens flexíveis, revestimentos e bens de consumo

- Em março de 2024, a Corbion N.V. introduziu aditivos bio-baseados de nova geração para melhorar o desempenho de polímeros à base de PLA, com foco em melhorar a resistência ao calor, a processabilidade e o desempenho global do material em aplicações de plástico compostavel

SKU-

Obtenha acesso online ao relatório sobre a primeira nuvem de inteligência de mercado do mundo

- Painel interativo de análise de dados

- Painel de análise da empresa para oportunidades de elevado potencial de crescimento

- Acesso de analista de pesquisa para personalização e customização. consultas

- Análise da concorrência com painel interativo

- Últimas notícias, atualizações e atualizações Análise de tendências

- Aproveite o poder da análise de benchmark para um rastreio abrangente da concorrência

Metodologia de Investigação

A recolha de dados e a análise do ano base são feitas através de módulos de recolha de dados com amostras grandes. A etapa inclui a obtenção de informações de mercado ou dados relacionados através de diversas fontes e estratégias. Inclui examinar e planear antecipadamente todos os dados adquiridos no passado. Da mesma forma, envolve o exame de inconsistências de informação observadas em diferentes fontes de informação. Os dados de mercado são analisados e estimados utilizando modelos estatísticos e coerentes de mercado. Além disso, a análise da quota de mercado e a análise das principais tendências são os principais fatores de sucesso no relatório de mercado. Para saber mais, solicite uma chamada de analista ou abra a sua consulta.

A principal metodologia de investigação utilizada pela equipa de investigação do DBMR é a triangulação de dados que envolve a mineração de dados, a análise do impacto das variáveis de dados no mercado e a validação primária (especialista do setor). Os modelos de dados incluem grelha de posicionamento de fornecedores, análise da linha de tempo do mercado, visão geral e guia de mercado, grelha de posicionamento da empresa, análise de patentes, análise de preços, análise da quota de mercado da empresa, normas de medição, análise global versus regional e de participação dos fornecedores. Para saber mais sobre a metodologia de investigação, faça uma consulta para falar com os nossos especialistas do setor.

Personalização disponível

A Data Bridge Market Research é líder em investigação formativa avançada. Orgulhamo-nos de servir os nossos clientes novos e existentes com dados e análises que correspondem e atendem aos seus objetivos. O relatório pode ser personalizado para incluir análise de tendências de preços de marcas-alvo, compreensão do mercado para países adicionais (solicite a lista de países), dados de resultados de ensaios clínicos, revisão de literatura, mercado remodelado e análise de base de produtos . A análise de mercado dos concorrentes-alvo pode ser analisada desde análises baseadas em tecnologia até estratégias de carteira de mercado. Podemos adicionar quantos concorrentes necessitar de dados no formato e estilo de dados que procura. A nossa equipa de analistas também pode fornecer dados em tabelas dinâmicas de ficheiros Excel em bruto (livro de factos) ou pode ajudá-lo a criar apresentações a partir dos conjuntos de dados disponíveis no relatório.