Global Brachytherapy Afterloaders Market

Tamanho do mercado em biliões de dólares

CAGR :

%

USD

1.40 Billion

USD

2.80 Billion

2025

2033

USD

1.40 Billion

USD

2.80 Billion

2025

2033

| 2026 –2033 | |

| USD 1.40 Billion | |

| USD 2.80 Billion | |

| % | |

|

Global Brachytherapy Afterloaders Mercado Segmentação, Por Tipo (HDR Afterloaders, PDR Afterloaders, LDR Afterloaders), Aplicação (Câncer de Próstato, Câncer Ginecológico, Câncer de Mama, Câncer de Pele, Câncer de Cabeça e Pescoço, e Outros), Usuário Final (Hospitales, Centros Cirúrgicos Ambulatórios, Clínicas Especializadas de Câncer, Institutos de Pesquisa), Técnica (Braquiterapia Intracavitária, Braquiterapia Intersticial, Braquiterapia de Superfície/Mold, Braquiterapia Intraluminal) – Tendências da Indústria e Previsão para 2033

Braquiterapia Afterloaders Tamanho do Mercado

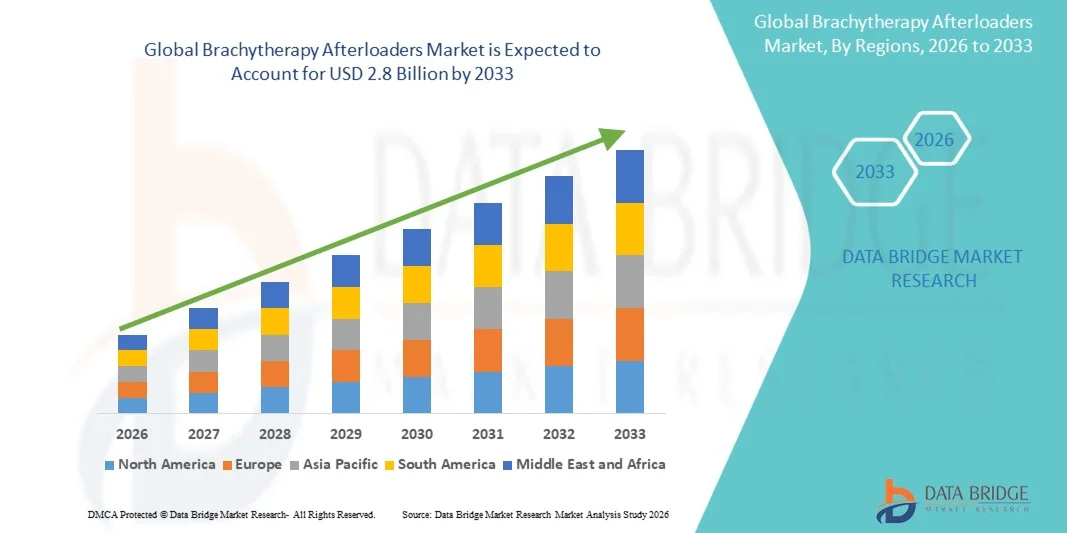

- O mercado global de pós-carregadores de Braquiterapia foi avaliado em1,4 mil milhões de USDem 2025 e espera-se alcançar2,8 mil milhões de USDaté 2033, num CAGR de5%durante o período de previsão de 2026 a 2033.

- O crescimento do mercado é impulsionado principalmente pela crescente incidência global de cânceres – particularmente próstata, ginecológico (cervical e endometrial) e câncer de mama – para o qual a braquiterapia é uma modalidade de tratamento clinicamente comprovada, poupando órgãos. A expansão do deslocamento para sistemas de pós-carregamento de HDR compatíveis com o ambulatório e a integração contínua com imagens avançadas e planejamento de tratamento assistido por IA estão acelerando ainda mais a adoção.

- Além disso, crescentes investimentos em infraestrutura de oncologia em economias emergentes, políticas de reembolso favoráveis em mercados desenvolvidos, aumento da preferência médica pela entrega de radiação localizada minimamente invasiva e o desenvolvimento de plataformas de pós-carregador compactas e integradas eletronicamente estão apoiando coletivamente uma forte expansão global do mercado.

Braquiterapia Afterloaders Análise de Mercado

- Os pós-carregadores de braquiterapia, utilizados em aplicações como tratamento intracavitário HDR, entrega de pulso PDR, suporte de implantação de sementes LDR e terapia intersticial guiada por imagem, permitem aos oncologistas entregar doses de radiação precisas e localizadas diretamente aos sítios tumorais, minimizando a exposição a tecidos saudáveis circundantes.

- A crescente demanda por pós-carregadores de braquiterapia é impulsionada pelo aumento da prevalência de câncer globalmente, aumento da preferência por técnicas de radioterapia minimamente invasivas e poupadoras de órgãos, adoção crescente de plataformas de braquiterapia guiada por imagens (IBGT) e ampliação do uso de sistemas de planejamento de tratamento integrados com IA que melhoram a precisão da dose e a eficiência clínica do fluxo de trabalho.

- A América do Norte dominou o mercado de pós-carregadores de braquiterapia em 2025, com uma participação de 39,92%, apoiada por uma infraestrutura de cuidados oncológicos bem estabelecida, altos volumes de procedimentos, quadros de reembolso favoráveis e uma grande base instalada de sistemas avançados de radioterapia nos Estados Unidos e Canadá.

- Espera-se que a Ásia-Pacífico seja a região de crescimento mais rápido, com um cagr de 8,20%, impulsionado pela rápida expansão das instalações de tratamento do câncer, aumento dos investimentos governamentais na modernização da saúde, aumento da incidência de câncer em países como China, Índia, Japão e Coreia do Sul e adoção crescente de tecnologias avançadas de radioterapia.

- O segmento de HDR Afterloaders dominou o mercado com uma participação de 71,79%, devido à sua eficiência clínica superior, sessões de tratamento ambulatorial curto, forte integração com as plataformas de planejamento de imagem e tratamento, e adoção generalizada em protocolos de tratamento de câncer de próstata e ginecologia.

Escopo de relatório e pós-carregadores de braquiterapia Segmentação de mercado

|

Atributos |

Brachytherapy Afterloaders Key Market Insights |

|

Segmentos Cobertos |

·Por Tipo: HDR (alta taxa de dose) Afterloaders, PDR (taxa de dose-pulso) Afterloaders, LDR (baixa taxa de dose) Afterloaders ·Por Aplicação: Câncer de próstata, câncer ginecológico (cervical, endometrial), câncer de mama, câncer de pele, câncer de cabeça e pescoço, e outros ·Por Usuário Final: Hospitais, Centros Cirúrgicos Ambulatórios (CSAP), Clínicas Especializadas de Câncer e Institutos de Pesquisa ·Por Técnica: Braquiterapia intracavitária, Braquiterapia Intersticial, Braquiterapia Superfície/Mold e Braquiterapia Intraluminal |

|

Países abrangidos |

América do Norte: · U.S. · Canadá · México Europa: · Alemanha · França · U.K. · Países Baixos · Suíça · Bélgica · Rússia · Itália · Espanha · Turquia · Resto da Europa Ásia- Pacífico: · China · Japão · Índia · Coreia do Sul · Singapura · Malásia · Austrália · Tailândia · Indonésia · Filipinas · Resto da Ásia-Pacífico Médio Oriente e África: · Arábia Saudita · U.A.E. · África do Sul · Egito · Israel · Resto de MEA América do Sul: · Brasil · Argentina · Resto da América do Sul |

|

Jogadores do mercado chave |

· Elekta AB (Suécia) · Varian Medical Systems / Siemens Healthineers (EUA) · Eckert & Ziegler BEBIG GmbH (Alemanha) · Isoray Inc. (EUA) · Becton Dickinson and Company (EUA) · IsoAid LLC (EUA) · Theragenics Corporation (EUA) · Radioterapia CIVCO (EUA) · Sun Nuclear Corporation (EUA) · Boston Scientific Corporation (EUA) · Mick Radio-Nuclear Instruments Inc. (EUA) · C.R. Bard / BD (EUA) |

|

Oportunidades de Mercado |

· Expansão da infraestrutura de cuidado ao câncer nas economias emergentes da Ásia-Pacífico, América Latina e MEA. · Adoção crescente do planejamento de tratamento de braquiterapia assistida por IA e guiada por imagem. · Aumentar a demanda por sistemas de pós-carregamento HDR compatíveis com o ambulatório com requisitos de blindagem reduzidos. |

|

Informações sobre o Valor Adicionado |

Além do valor de mercado, taxa de crescimento, segmentação, cobertura geográfica e principais atores, os relatórios de mercado incluem análise de importação/exportação, visão geral da capacidade de produção, análise da tendência de preços, análise da cadeia de suprimentos, análise da cadeia de valor, critérios de seleção de fornecedores, Análise de PESTLE, Análise de Porter e quadro regulatório. |

Tendências do mercado de pós-carregadores de braquiterapia

"A adoção crescente de sistemas de pós-carregamento HDR integrados e guiados por imagens de IA está transformando fluxos de trabalho oncológicos de precisão"

- A crescente integração de inteligência artificial e recursos avançados de imagem dentro das plataformas pós-carregador HDR está criando oportunidades de crescimento significativas no mercado global de pós-carregadores de braquiterapia.

- As ferramentas de planejamento de tratamento assistida por IA agora permitem a otimização automatizada da dose, reduzindo o tempo de preparação do tratamento em aproximadamente 25% e melhorando a consistência do plano entre operadores e centros clínicos.

- A integração de imagens por RM e TC em tempo real dentro dos sistemas pós-carregador permite que os clínicos alcancem a colocação precisa da fonte e a entrega precisa da dose, particularmente para casos de câncer cervical, próstata e endometrial.

- Aumentar a adoção de unidades eletrônicas de braquiterapia com requisitos de blindagem simplificados está permitindo a implantação em ambulatórios de oncologia que não possuem cofres de radiação dedicados, ampliando o alcance do mercado.

- Aumentar a implementação de plataformas de dosimetria habilitadas para nuvem e ferramentas de garantia de qualidade remota está simplificando as operações clínicas e reduzindo a carga de recursos para físicos médicos especializados.

- O uso crescente de sistemas de pós-carregamento assistidos por robótica está aumentando a precisão no posicionamento da fonte, minimizando a variabilidade do operador e melhorando a reprodutibilidade da entrega de dose em aplicações intersticiais complexas.

- Os fabricantes estão investindo em projetos de pós-carregador modular compactos que oferecem menor pegada e melhor portabilidade, apoiando a implantação em ambientes clínicos restritos aos recursos e limitados ao espaço globalmente.

- No geral, a convergência tecnológica de IA, robótica e imagem dentro de plataformas pós-carregador está redefinindo padrões processuais e apoiando uma maior trajetória de adoção clínica globalmente.

Braquiterapia Afterloaders Market Dynamics

Controlador

"O aumento da incidência global de câncer e a crescente preferência pela radioterapia localizada e de precisão estão conduzindo a adoção de pós-carregador de braquiterapia"

- O aumento da carga global de câncer, com o câncer permanece uma das principais causas de mortalidade em todo o mundo, é um motor primário do mercado de pós-carregadores de braquiterapia, dada a comprovada eficácia da modalidade na realização de radioterapia direcionada.

- Próstata, ginecológica (cervical e endometrial), e câncer de mama – as principais indicações para a braquiterapia – estão experimentando taxas de incidência crescentes globalmente devido ao envelhecimento das populações, mudanças de estilo de vida, e melhores capacidades diagnósticas.

- Os pós-carregadores de braquiterapia, particularmente os sistemas HDR, oferecem tempos de tratamento mais curtos, compatibilidade ambulatorial e alta precisão de dose, tornando-os cada vez mais preferidos em relação à radioterapia externa prolongada (EBRT) em protocolos clínicos selecionados.

- A crescente preferência do médico por opções de tratamento de câncer minimamente invasivas e poupadoras de órgãos está acelerando ainda mais a adoção de braquiterapia baseada em pós-carregadores em sistemas de saúde desenvolvidos e desenvolvidos.

- Dados de desfechos clínicos favoráveis, incluindo melhora das taxas de controle local e redução da recorrência em casos de câncer de próstata e colo do útero tratados com braquiterapia HDR, reforçam as decisões de investimento institucional.

- Aumentar a integração de programas de planejamento de tratamento, sistemas de imagem e plataformas eletrônicas de registro de saúde (EHR) com equipamentos pós-carregadores está aumentando a eficiência clínica do fluxo de trabalho e a reprodutibilidade do tratamento.

- A expansão da infraestrutura oncológica, o aumento dos gastos com saúde e a crescente conscientização das opções avançadas de radioterapia em mercados emergentes estão ampliando coletivamente o mercado global endereçável para pós-carregadores de braquiterapia.

Restrição/Desafio

"Requisitos de investimento de capital elevados e escassez de mão-de-obra especializada estão limitando a adoção mais ampla de pós-carregadores de braquiterapia"

- Os elevados custos de capital associados aos sistemas pós-carregador de braquiterapia – que variam de US$ 100.000 a mais de US$ 600 mil por unidade – criam barreiras significativas para aquisições de hospitais de nível médio, centros regionais de câncer e serviços de saúde em mercados de menor renda.

- A exigência de médicos especializados em oncologia por radiação, físicos médicos e equipe clínica treinada para operação pós-carregador apresenta um desafio crítico de disponibilidade de mão-de-obra, particularmente em economias emergentes, onde a escassez de pessoal treinado pode atingir aproximadamente 30%.

- Requisitos regulatórios complexos para manipulação de fontes radioativas, armazenamento, descarte e licenciamento de instalações adicionam custos operacionais e de conformidade, desencorajando as instituições de saúde menores do estabelecimento de programas de braquiterapia.

- Requisitos dedicados de infraestrutura de proteção contra radiações associados aos sistemas tradicionais de pós-carregamento HDR e PDR aumentam a construção de instalações e os custos de retromontagem, limitando a implantação em ambientes clínicos não-propósitos.

- A concorrência das tecnologias de radioterapia de feixe externo (EBRT), incluindo a radioterapia corporal estereotáxica (SBRT) e a terapia de prótons, que são cada vez mais comercializadas como alternativas para indicações selecionadas, representa um risco de substituição para certas aplicações de braquiterapia.

- Programas limitados de treinamento clínico e conhecimento insuficiente das vantagens clínicas da braquiterapia em algumas geografias resultam em subutilização e penetração subótima do mercado em regiões potencialmente de alto crescimento.

Braquiterapia Afterloaders Market Scope

O mercado é segmentado com base no tipo, aplicação, usuário final e técnica.

Por Tipo

Com base no Type, o mercado global de pós-carregadores de Braquiterapia é segmentado em HDR (Alta Taxa de Dose) Afterloaders, PDR (Pulse-Dose Rate) Afterloaders, e LDR (Baixa Taxa de Dose) Afterloaders.

O segmento HDR Afterloaders dominou o mercado com a maior participação de receita em 2025 com uma participação de 71,79%, representando aproximadamente 70% das instalações globais. Os sistemas HDR são preferidos pelos centros de oncologia em todo o mundo por sua capacidade de fornecer doses de radiação concentradas de alta precisão em curtas sessões de tratamento ambulatorial compatível. Sua forte integração com plataformas avançadas de imagem, software de planejamento de dose assistido por IA e mecanismos automatizados de posicionamento de fonte fazem deles o padrão clínico para a braquiterapia da próstata, ginecológica e de câncer de mama. A capacidade de personalizar os esquemas de fracionamento, reduzir as necessidades de internação do paciente e melhorar a produtividade do tratamento reforçam ainda mais a dominância da HDR.

Espera-se que o segmento de pós-carregadores PDR (Pulse-Dose Rate) testemunhe o crescimento mais rápido de 9,50% durante o período de previsão, impulsionado pelo crescente interesse clínico em protocolos de entrega de dose de pulso que combinam as vantagens biológicas da terapia contínua de baixa taxa de dose com a segurança e precisão do pós-carregamento remoto. Os sistemas PDR estão ganhando impulso particularmente em centros de oncologia europeus especializados e instituições que tratam cânceres ginecológicos complexos e de cabeça e pescoço, onde a deposição gradual de dose é clinicamente preferível. A adoção crescente de plataformas híbridas de pós-carregamento HDR/PDR e o aumento do financiamento para programas avançados de radioterapia estão apoiando ainda mais a expansão do segmento.

Por Aplicação

Com base na Aplicação, o mercado global de pós-carregadores de Braquiterapia é segmentado em Câncer de Próstata, Câncer Ginecológico (Cervical, Endometrial), Câncer de Mama, Câncer de Pele, Câncer de Cabeça e Pescoço, e Outros.

O segmento de Câncer de Próstata dominou o mercado com a maior participação de receita em 2025 com uma participação de 33,02%, representando aproximadamente 33-38% do total de uso de pós-carregador. O câncer de próstata representa a principal indicação para pós-carregadores de braquiterapia globalmente, apoiado pela sua alta incidência global, pela comprovada eficácia clínica da HDR e da braquiterapia LDR na entrega de altas doses tumorais com impacto mínimo em órgãos adjacentes, como bexiga e reto, e pela crescente preferência do médico pela braquiterapia como monoterapia ou potenciar o tratamento em combinação com EBRT. Fortes diretrizes clínicas suportam e ampliam o uso de sistemas de colocação de aplicadores guiados por imagens reforçam ainda mais a liderança do segmento.

Espera-se que o segmento de Câncer Ginecológico (Cervical e Endometrial) testemunhe o crescimento mais rápido de 7,60% durante o período de previsão, impulsionado pelo aumento da consciência global do câncer cervical – particularmente em países em desenvolvimento –, juntamente com a adoção crescente de braquiterapia intracavitária e intersticial HDR como um componente padrão de cuidados para o câncer cervical e endometrial localmente avançado. A crescente integração dos protocolos de braquiterapia adaptativa guiada por RM (IGABT), que demonstraram melhorias significativas no controle tumoral local e redução da toxicidade tardia, está aumentando substancialmente a demanda por sistemas avançados de pós-carregamento de HDR compatíveis com as orientações da RM.

Por Usuário Final

Com base no Usuário Final, o mercado global de pós-carregadores de Braquiterapia é segmentado em Hospitais, Centros Cirúrgicos Ambulatórios (ASCs), Clínicas Especiais de Câncer e Institutos de Pesquisa.

O segmento de Hospitais dominou o mercado com a maior parcela de receita em 2025 com uma participação de 60,00%, impulsionada pela concentração de casos complexos de oncologia, disponibilidade de equipes multidisciplinares de atenção ao câncer e aquisição institucional de equipamentos de pós-carregador intensivos em capital, apoiados por quadros de reembolso favoráveis na América do Norte e na Europa. Centros médicos acadêmicos e grandes hospitais oncológicos representam os compradores primários de plataformas avançadas de pós-carregadores HDR e PDR com planejamento integrado de tratamento e recursos de imagem.

Espera-se que o segmento Centros Cirúrgicos Ambulatórios (ASCs) testemunhe o crescimento mais rápido de 8,50% durante o período de previsão, alimentado pelo aumento da transferência de procedimentos de braquiterapia elegíveis para ambientes ambulatoriais impulsionados por pressões de otimização de custos, preferência do paciente pelo tratamento conveniente e o desenvolvimento de sistemas pós-carregamento compactos de HDR com requisitos simplificados de blindagem. A expansão das redes dedicadas de câncer ASC e o aumento do investimento privado em instalações ambulatoriais de radiação oncológica estão acelerando ainda mais a adoção desse segmento.

Por Técnica

Com base na Técnica, o mercado global de pós-carregadores de Braquiterapia é segmentado em Braquiterapia Intracavitária, Braquiterapia Intersticial, Braquiterapia Superfície/Mold e Braquiterapia Intraluminal.

O segmento de Braquiterapia Intracavitária dominou o mercado com a maior parcela de receita de 48,00% em 2025, uma vez que representa a técnica mais utilizada no tratamento ginecológico do câncer – particularmente câncer cervical e endometrial – onde sistemas aplicadores padronizados (ring-and-tandem, cilindros vaginais) possibilitam a entrega de dose consistente, reprodutível e sustentada por diretrizes. Sua compatibilidade com as principais plataformas de pós-carregador HDR de fabricantes líderes e forte base de evidências clínicas ao longo de décadas de uso reforçam a liderança do segmento.

Espera-se que o segmento de Braquiterapia Intersticial testemunhe o crescimento mais rápido de 9,00% durante o período de previsão, impulsionado pela expansão de aplicações em tumores ginecológicos localmente avançados, câncer de próstata recorrente, câncer de mama (radiação parcial acelerada da mama – APBI) e casos complexos de câncer de cabeça e pescoço. A adoção crescente de técnicas de implante intersticial guiado por imagem 3D, o desenvolvimento de sistemas de aplicação de agulha flexível pré-carregada e o aumento do uso em combinação com abordagens intracavitárias para o câncer de colo do útero avançado estão levando significativamente à adoção global de braquiterapia intersticial.

Pós-carregadores de Braquiterapia Análise Regional de Mercado

- A América do Norte dominou o mercado de pós-carregadores de Braquiterapia com a maior parcela de receita de aproximadamente 38,92% em 2025, apoiada pela forte demanda dos departamentos de oncologia de radiação hospitalar, altos volumes de procedimentos de câncer, reembolso favorável da Medicare e seguradoras privadas para procedimentos de braquiterapia HDR e uma grande base instalada de sistemas avançados de pós-carregamento. Os Estados Unidos lideram a demanda regional, com mais de 70% dos centros de oncologia utilizando plataformas automáticas de pós-carregador HDR. A presença de fabricantes globais chave, incluindo Varian Medical Systems (Siemens Healthineers), Isoray, IsoAid e Theragenics reforça ainda mais a posição de liderança da região.

- Participantes da indústria em toda a América do Norte enfatizam fortemente a integração clínica de fluxo de trabalho, dosimetria precisa, planejamento de tratamento aprimorado por IA e capacidades de tratamento ambulatorial de alto rendimento, impulsionando a demanda consistente por plataformas de pós-carregador de próxima geração e atualizações. O uso crescente da braquiterapia em combinação com a terapia de feixe externo, a adoção crescente de braquiterapia adaptativa guiada por imagem e a expansão de programas dedicados de braquiterapia em centros oncológicos abrangentes estão acelerando ainda mais o consumo de pós-carregadores de braquiterapia.

- Essa forte posição de mercado é reforçada pela robusta infraestrutura de pesquisa em oncologia, investimento contínuo na modernização da tecnologia de radioterapia, forte ecossistema de treinamento clínico que apoia o desenvolvimento especializado da força de trabalho de braquiterapia e um ambiente de reembolso progressivo que recompensa a qualidade processual e a prestação de cuidados baseados em resultados.

U.S. Brachytherapy Afterloaders Market Insight

O mercado de pós-carregadores de braquiterapia dos EUA ocupa uma posição dominante globalmente, impulsionado pela forte demanda de centros de câncer abrangentes, instituições médicas acadêmicas e programas de oncologia comunitária de alto volume. O uso generalizado de pós-carregadores HDR para o tratamento de próstata, colo do útero e câncer de mama está apoiando significativamente o crescimento do mercado. Além disso, a presença de uma infraestrutura de radiação oncológica bem estabelecida, a alta adoção de plataformas de planejamento de tratamento orientadas por IA e o aumento da implantação de programas de braquiterapia no sistema hospitalar Veteranos Affairs (VA) e redes hospitalares comunitárias estão fortalecendo ainda mais a expansão do mercado.

Europe Brachytherapy Afterloaders Market Insight

O mercado europeu de pós-carregadores de Braquiterapia está testemunhando crescimento constante, impulsionado pela forte demanda dos departamentos de oncologia por radiação hospitalar na Alemanha, França, Reino Unido e Holanda, onde a braquiterapia é um componente integral das diretrizes nacionais de tratamento do câncer. A região representa aproximadamente 27% da receita global de pós-carregadores, apoiada por uma rede bem desenvolvida de centros de radioterapia especializados, fortes marcos regulatórios para o manuseio de isótopos e a maior concentração de instalações de pós-carregadores de PDR em todo o mundo. O aumento da adoção de braquiterapia adaptativa guiada por RM (MR-IGBT) e a modernização contínua da infraestrutura de pós-carregador legado estão apoiando ainda mais o crescimento do mercado europeu.

Alemanha Braquiterapia Afterloaders Market Insight

O mercado alemão de pós-carregadores de braquiterapia está experimentando crescimento constante, impulsionado pela forte demanda do setor avançado de radiação oncológica hospitalar do país. A Alemanha é um dos mercados de braquiterapia mais avançados da Europa, apoiado pela infraestrutura de cuidados com o câncer, reembolso favorável através de seguro de saúde legal (GKV), e alta penetração tecnológica. Os sistemas HDR são amplamente utilizados no tratamento de câncer de próstata e ginecológico, enquanto as instalações de pós-carregador PDR mantêm presença significativa no mercado em centros especializados em oncologia. A substituição de plataformas de pós-carregador legado e a integração de atualizações de software de planejamento de tratamento continuam a sustentar a demanda de equipamentos de capital.

Asia-Pacific Brachytherapy Afterloaders Market Insight

Espera-se que o mercado de pós-carregadores de Braquiterapia Ásia-Pacífico registre o CAGR mais rápido durante o período de previsão de 2026-2033, impulsionado pela rápida expansão da infraestrutura de assistência ao câncer, aumento da incidência de câncer em toda a região, e aumento dos investimentos governamentais na modernização da saúde na China, Índia, Japão, Coreia do Sul e países do Sudeste Asiático. Aumentar a conscientização das opções avançadas de radioterapia, melhorar o acesso a profissionais treinados de oncologia de radiação e aumentar a adoção de plataformas pós-carregador HDR em centros de câncer recém-estabelecidos estão aumentando significativamente o crescimento do mercado. Atualmente, a região representa cerca de 15-27% do consumo global de pós-carregadores, com um potencial substancial e inexplorado nos mercados de países de renda baixa e média em todo o Sul e Sudeste Asiático.

Japão Brachytherapy Afterloaders Market Insight

O mercado de pós-carregadores de Braquiterapia do Japão está testemunhando crescimento constante, impulsionado pela forte demanda do ecossistema avançado de cuidados oncológicos do país. O envelhecimento da população japonesa e a alta incidência de câncer de próstata e ginecológico estão criando demanda sustentada por procedimentos de braquiterapia. O país beneficia de uma infraestrutura hospitalar bem estabelecida, de fortes marcos regulatórios para equipamentos radiológicos e de contínua inovação tecnológica em sistemas de liberação de radioterapia. Além disso, o uso crescente de pós-carregadores HDR em combinação com EBRT e a adoção crescente de protocolos de braquiterapia guiados por imagens estão apoiando a expansão consistente do mercado.

India Brachytherapy Afterloaders Market Insight

O mercado India Brachytherapy Afterloaders está experimentando forte impulso de crescimento, impulsionado pela rápida expansão da infraestrutura de cuidados de câncer, aumento dos gastos com saúde e aumento da carga de câncer – particularmente do câncer cervical e de mama – em todo o país. Iniciativas governamentais como o National Cancer Control Programme (NCCP) e Ayushman Bharat estão apoiando a expansão de instalações de tratamento de câncer hospitalares. O crescente estabelecimento de hospitais dedicados ao câncer e centros de radioterapia, o aumento das importações de equipamentos avançados de pós-carregador e o aumento da conscientização da braquiterapia como opção de tratamento local econômica estão fortalecendo coletivamente a expansão do mercado em todo o país.

Braquiterapia Afterloaders Market Share

A indústria de pós-carregadores de Braquiterapia é liderada principalmente por empresas bem estabelecidas, incluindo:

- Elekta AB (Suécia)

- Varian Medical Systems / Siemens Healthineers (EUA)

- Eckert & Ziegler BEBIG GmbH (Alemanha)

- Isoray Inc. (EUA)

- Becton, Dickinson and Company (EUA)

- IsoAid LLC (EUA)

- Theragenics Corporation (EUA)

- Radioterapia CIVCO (EUA)

- Sun Nuclear Corporation (EUA)

- Boston Scientific Corporation (EUA)

- Mick Radio-Nuclear Instruments Inc. (EUA)

- R. Bard / BD Medical (EUA)

Desenvolvimentos recentes no mercado global de pós-carregadores de braquiterapia

- Em novembro de 2024, a Varian Medical Systems (uma empresa Siemens Healthineers) melhorou suas ofertas de braquiterapia, incorporando inteligência artificial em seu software de planejamento de tratamento BrachyVision. As ferramentas de otimização de dose orientadas por IA são projetadas para automatizar e padronizar a geração de planos de tratamento para a braquiterapia de câncer de próstata e colo do útero HDR, reduzindo o tempo de preparação do plano e melhorando a consistência entre os centros clínicos.

- Em janeiro de 2025, a Isoray Inc. formou uma parceria estratégica para impulsionar a produção de seu isótopo Césio-131, apoiando a expansão da disponibilidade de tratamento de braquiterapia prostática LDR em todos os Estados Unidos, abordando restrições de oferta para uma das tecnologias de sementes isotópicas de baixa dose de ação mais rápida no tratamento do câncer de próstata.

- Em 2024, um fabricante líder revelou um sistema de pós-carregador HDR fonte recarregável projetado para estender o ciclo de vida do sistema em aproximadamente 15%, reduzindo interrupções de manutenção e reduzindo o custo total de propriedade para centros de oncologia, particularmente beneficiando hospitais de nível médio em mercados sensíveis aos custos.

- Em 2024, um sistema de pós-carregador PDR compacto foi introduzido com uma redução de aproximadamente 18% em relação aos sistemas padrão, projetados especificamente para clínicas especializadas restritas ao espaço e facilitando a implantação regional mais ampla em mercados emergentes com espaço de instalação limitado.

- Em 2023, as plataformas de dosimetria equipadas com nuvem integradas com sistemas pós-carregador permitiram o monitoramento remoto da garantia de qualidade, reduzindo a necessidade de visitas físicas médicas no local em aproximadamente 50% e melhorando o cumprimento dos padrões de dosimetria em locais de tratamento de câncer distribuídos.

SKU-

Obtenha acesso online ao relatório sobre a primeira nuvem de inteligência de mercado do mundo

- Painel interativo de análise de dados

- Painel de análise da empresa para oportunidades de elevado potencial de crescimento

- Acesso de analista de pesquisa para personalização e customização. consultas

- Análise da concorrência com painel interativo

- Últimas notícias, atualizações e atualizações Análise de tendências

- Aproveite o poder da análise de benchmark para um rastreio abrangente da concorrência

Metodologia de Investigação

A recolha de dados e a análise do ano base são feitas através de módulos de recolha de dados com amostras grandes. A etapa inclui a obtenção de informações de mercado ou dados relacionados através de diversas fontes e estratégias. Inclui examinar e planear antecipadamente todos os dados adquiridos no passado. Da mesma forma, envolve o exame de inconsistências de informação observadas em diferentes fontes de informação. Os dados de mercado são analisados e estimados utilizando modelos estatísticos e coerentes de mercado. Além disso, a análise da quota de mercado e a análise das principais tendências são os principais fatores de sucesso no relatório de mercado. Para saber mais, solicite uma chamada de analista ou abra a sua consulta.

A principal metodologia de investigação utilizada pela equipa de investigação do DBMR é a triangulação de dados que envolve a mineração de dados, a análise do impacto das variáveis de dados no mercado e a validação primária (especialista do setor). Os modelos de dados incluem grelha de posicionamento de fornecedores, análise da linha de tempo do mercado, visão geral e guia de mercado, grelha de posicionamento da empresa, análise de patentes, análise de preços, análise da quota de mercado da empresa, normas de medição, análise global versus regional e de participação dos fornecedores. Para saber mais sobre a metodologia de investigação, faça uma consulta para falar com os nossos especialistas do setor.

Personalização disponível

A Data Bridge Market Research é líder em investigação formativa avançada. Orgulhamo-nos de servir os nossos clientes novos e existentes com dados e análises que correspondem e atendem aos seus objetivos. O relatório pode ser personalizado para incluir análise de tendências de preços de marcas-alvo, compreensão do mercado para países adicionais (solicite a lista de países), dados de resultados de ensaios clínicos, revisão de literatura, mercado remodelado e análise de base de produtos . A análise de mercado dos concorrentes-alvo pode ser analisada desde análises baseadas em tecnologia até estratégias de carteira de mercado. Podemos adicionar quantos concorrentes necessitar de dados no formato e estilo de dados que procura. A nossa equipa de analistas também pode fornecer dados em tabelas dinâmicas de ficheiros Excel em bruto (livro de factos) ou pode ajudá-lo a criar apresentações a partir dos conjuntos de dados disponíveis no relatório.