Global Dc Fast Charging Market

Tamanho do mercado em biliões de dólares

CAGR :

%

USD

9.53 Billion

USD

51.60 Billion

2025

2033

USD

9.53 Billion

USD

51.60 Billion

2025

2033

| 2026 –2033 | |

| USD 9.53 Billion | |

| USD 51.60 Billion | |

| % | |

|

Segmentação do Mercado de Carregamento Rápido da DC Global, por Conector (CHAdeMO, CCS, e outros), Infraestrutura de Carregamento (Standalone e Integrated), Classificação de Energia (≤50 kW, 50–150 kW, 150–350 kW e acima de 350 kW), Aplicação (Comercial e Residencial) - Tendências e Previsão da Indústria para 2033

Carregamento Rápido DCTamanho do Mercado

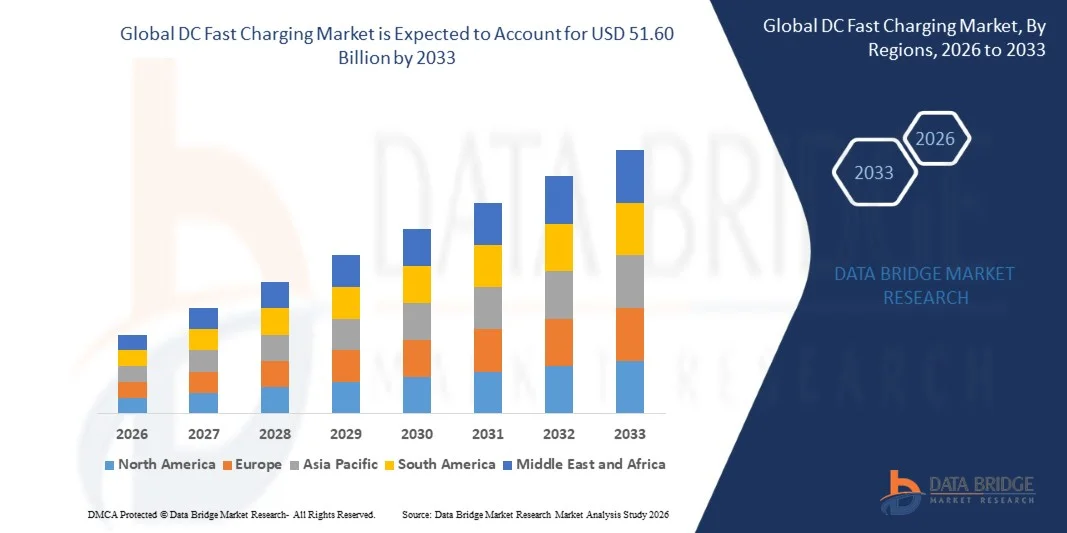

- A dimensão global do mercado de carregamento rápido da DC foi avaliada em9,53 mil milhões de dólares em 2025e espera-se alcançar51,60 mil milhões de USD até 2033, em umaCAGR de 23,51%durante o período de previsão

- O crescimento do mercado é amplamente impulsionado pela rápida expansão da adoção de veículos elétricos e fortes iniciativas governamentais de apoio à transição de mobilidade limpa, levando à implantação acelerada de infraestrutura de carregamento rápido de DC em redes urbanas e rodoviárias

- Além disso, avanços contínuos em tecnologias de carregamento ultra-rápido, sistemas de integração de redes e soluções inteligentes de gerenciamento de energia estão melhorando a eficiência de carregamento e reduzindo o tempo de inatividade, tornando o carregamento rápido de DC mais viável para adoção em larga escala

Carregamento Rápido DCAnálise de mercado

- Os sistemas de carregamento rápido DC, permitindo o reabastecimento em alta velocidade de baterias de veículos elétricos em minutos ao invés de horas, estão se tornando um componente crítico da moderna infraestrutura EV devido à sua capacidade de suportar viagens de longa distância e frotas comerciais de alta utilização

- A crescente demanda por carregamento rápido de DC é impulsionada principalmente pelo aumento da penetração de veículos elétricos, expansão de redes públicas de carregamento e crescente necessidade de soluções de carregamento confiáveis e eficientes em tempo em aplicações residenciais, comerciais e de frota

- Ásia-Pacífico domina o mercado de carregamento rápido DC com uma parte de49,48% em 2025, devido à rápida adoção da EV, forte apoio do governo à eletrificação e implantação em larga escala de infraestrutura de cobrança pública

- Espera-se que a América do Norte seja a região de crescimento mais rápido no mercado de carregamento rápido de DC durante o período de previsão devido ao aumento das vendas de EV, financiamento federal para cobrança de infraestrutura e crescente demanda por mobilidade elétrica de longa distância

- O segmento CCS dominou o mercado com uma quota de mercado de 42,48% em 2025, devido à sua ampla adoção em toda a Europa, América do Norte, e à sua crescente compatibilidade com uma ampla gama de modelos de veículos elétricos. CCS oferece velocidades de carregamento mais rápidas e suporta carregamento AC e DC através de uma única interface, tornando-a altamente eficiente para implantação moderna de infraestrutura EV

Âmbito do relatório eCarregamento Rápido DCSegmentação do mercado

|

Atributos |

Carregamento Rápido DCChavePerspectivas de mercado |

|

Segmentos Cobertos |

|

|

Países abrangidos |

América do Norte

Europa

Ásia- Pacífico

Médio Oriente e África

América do Sul

|

|

Jogadores do mercado chave |

|

|

Oportunidades de Mercado |

|

|

Informações sobre o Valor Adicionado |

Além dos insights de mercado, como valor de mercado, taxa de crescimento, segmentos de mercado, cobertura geográfica, atores de mercado e cenário de mercado, o relatório de mercado curado pela equipe de Pesquisa do Mercado da Ponte de Dados inclui análise de especialistas em profundidade, análise de importação/exportação, análise de preços, análise de consumo de produção e análise de pilão. |

Carregamento Rápido DCTendências do mercado

“Aumentar a implantação de redes de carregamento ultra-rápido”

- Uma tendência fundamental no mercado de carregamento rápido da DC é a rápida expansão de redes de carregamento ultra-rápido com o objetivo de reduzir o tempo de carregamento e melhorar a usabilidade da EV em corredores de viagens de longa distância e urbanas. Esta expansão está sendo impulsionada pela necessidade de suportar maiores capacidades de bateria em veículos elétricos modernos e garantir uma acessibilidade de carregamento sem descontinuidades entre rodovias e centros metropolitanos

- Por exemplo, Tesla continua a expandir sua rede de Supercarregadores globalmente, implementando carregadores rápidos de alta potência DC capazes de reduzir significativamente o tempo de carregamento para EVs compatíveis. Este desenvolvimento de infraestrutura reforça a viabilidade de viagens EV de longa distância e aumenta a conveniência do usuário nas principais rotas de transporte

- Outro grande desenvolvimento é a escala de corredores de carregamento multi-operadores liderados por consórcios como Ionity, que é apoiado conjuntamente pela BMW, Mercedes-Benz, Ford e Hyundai. Estas estações ultra-rápidas estão estrategicamente posicionadas através das rodovias europeias para permitir a interoperabilidade de carga de alta velocidade para várias marcas EV

- Operadores de rede de carregamento, como a Electrify America, também estão acelerando a implantação de estações de carregamento rápidas de alta capacidade DC nos EUA, com foco em centros urbanos e rodovias interestaduais. Esta expansão está melhorando a acessibilidade de cobrança e apoiando a transição para adoção de EV de alto volume

- A integração de sistemas de tarifação de alta potência por parte de empresas como a ABB e a Shell Recharge está a aumentar ainda mais a eficiência de tarifação nas redes de infraestruturas comerciais e públicas. Essas implantações estão melhorando as taxas de transferência de energia e reduzindo o tempo de parada do veículo, tornando a adoção da EV mais prática para operadores de frota e usuários privados

- O mercado também está testemunhando crescente investimento em infraestrutura de carregamento escalável projetada para apoiar futuros padrões de carregamento ultra-rápido, com empresas como BP Pulse expandindo sua pegada de rede em várias regiões. Esta implantação contínua de sistemas de carregamento de alta velocidade está reforçando a mudança para um ecossistema EV mais conectado e eficiente em tempo

Dinâmica do Mercado de Carregamento Rápido DC

Controlador

“Aumentar o apoio à adoção de EV e infraestrutura governamental”

- Um dos principais motores no mercado de carregamento rápido de DC é o rápido aumento da adoção de veículos elétricos, apoiado por fortes iniciativas governamentais destinadas a expandir a infraestrutura de carregamento e reduzir as emissões de carbono. O crescente tamanho da frota EV está criando demanda sustentada por redes de carregamento rápidas e confiáveis em setores público e privado

- Por exemplo, o programa US National Electric Vehicle Infrastructure (NEVI) sob a administração de Biden está financiando o desenvolvimento de corredores de carga rápida DC nacional para apoiar viagens EV de longa distância. Esta iniciativa está acelerando a implantação de infra-estruturas e melhorando a acessibilidade da tarifação nas rodovias interestaduais

- Iniciativas lideradas pelo governo, como o esquema FAME II da Índia, sob o Ministério das Indústrias Pesadas, estão apoiando a instalação de estações de carregamento rápido em regiões urbanas e semi-urbanas. Este apoio político está a incentivar a participação do sector privado e a reforçar o ecossistema nacional de tarifação de EV

- O Regulamento relativo à Infraestrutura Alternativa de Combustíveis (AFIR) da União Europeia está a obrigar a expansão das estações de carregamento de alta potência ao longo das principais rotas de transporte a garantir uma disponibilidade uniforme de carregamento. Este quadro regulamentar está a impulsionar o crescimento coordenado das infra-estruturas entre os Estados-Membros

- A colaboração contínua entre montadoras, fornecedores de energia e governos está reforçando os investimentos em larga escala em infraestrutura de cobrança, com empresas como a ABB e a EVgo desempenhando um papel fundamental na implantação. Este impulso combinado está a reforçar a trajectória global de crescimento do mercado de tarifação rápida da DC

Restrição/Desafio

“Alto custo de instalação e restrições de capacidade da grade”

- Um desafio significativo no mercado de carregamento rápido da DC é o alto custo associado à instalação e implantação de estações de carregamento de alta potência, que exigem infraestrutura elétrica avançada e investimento substancial em capital. Estas pressões de custos limitam a velocidade de expansão da rede, em especial nas regiões em desenvolvimento e semi-urbanas

- Por exemplo, operadores como a Electrify America enfrentam altos requisitos de gasto de capital na construção de estações de carregamento ultra-rápido equipadas com transformadores de alta capacidade e eletrônicos avançados. Esses custos de infraestrutura impactam significativamente a escalabilidade do projeto e o retorno dos prazos de investimento

- As limitações de capacidade da grade também representam uma grande restrição, pois as redes elétricas existentes lutam para suportar a alta demanda de energia de carregadores rápidos DC sem atualizações. Em regiões como a Califórnia, utilitários como o California Independent System Operator (CAISO) gerenciam o estresse da grade causado pelo aumento das cargas de carregamento EV

- Os fornecedores de energia como a National Grid no Reino Unido são obrigados a investir fortemente em reforço de grade e upgrades de subestação para apoiar a expansão da infraestrutura de carregamento rápido. Essas atualizações aumentam a linha do tempo de implantação e adicionam complexidade à implantação da infraestrutura

- A combinação de elevados custos de infraestrutura e requisitos de modernização da rede continua a restringir o rápido escalonamento das redes de carregamento rápido de DC, colocando pressão sobre as partes interessadas para otimizar estratégias de investimento e melhorar a eficiência de gestão de energia em todos os ecossistemas de carregamento

DC Fast Charging Market Scope

O mercado é segmentado com base em conectores, infraestrutura de carregamento, classificação de potência e aplicação.

• Por Conector

Com base no conector, o mercado DC Fast Charging é segmentado em CHAdeMO, CCS e Outros. O segmento CCS dominou o mercado com a maior parcela de receita de 42,48% em 2025, impulsionada por sua adoção generalizada em toda a Europa, América do Norte, e expandindo a compatibilidade com uma ampla gama de modelos de veículos elétricos. CCS oferece velocidades de carregamento mais rápidas e suporta carregamento AC e DC através de uma única interface, tornando-o altamente eficiente para implantação moderna de infraestrutura EV. Automakers preferem cada vez mais CCS devido aos seus esforços de padronização e forte apoio de alianças automotivas globais. A sua crescente integração com as estações de carregamento de alta potência reforça ainda mais o seu domínio nas redes de carregamento públicas e rodoviárias.

O segmento CHAdeMO é esperado para testemunhar a adoção constante, mas está gradualmente perdendo participação em implantações mais recentes devido à compatibilidade global limitada e transição mais lenta para os padrões EV da próxima geração. No entanto, continua a manter relevância nos mercados de EV legados, particularmente no Japão, onde permanece amplamente apoiado e integrado nas redes de infraestrutura existentes.

• Ao carregar a infra-estrutura

Com base na infraestrutura de tarifação, o mercado DC Fast Charging é segmentado em sistemas autônomos e integrados. O segmento Integrado dominou o mercado com a maior participação de receita em 2025, impulsionado pela sua capacidade de combinar múltiplos pontos de carregamento com sistemas de gestão de energia, soluções de pagamento e conectividade de rede em um único ecossistema. A infraestrutura integrada suporta carregamento inteligente, balanceamento de carga e monitoramento em tempo real, tornando-o altamente adequado para hubs urbanos e redes de carregamento EV em larga escala. A crescente concentração na integração de redes inteligentes e na compatibilidade das energias renováveis aumenta ainda mais a procura de soluções integradas. Além disso, sua escalabilidade e eficiência na gestão de múltiplas estações de carregamento aumentam a conveniência operacional para os prestadores de serviços.

Espera-se que o segmento Standalone testemunhe crescimento constante devido à sua menor complexidade de instalação e adequação para configurações de carregamento em pequena escala ou descentralizadas. Estes sistemas são amplamente utilizados em locais comerciais residenciais ou de baixo tráfego, onde a capacidade básica de carregamento rápido é suficiente sem integração avançada de rede.

• Por Classificação de Potência

Com base na notação de potência, o mercado DC Fast Charging é segmentado em ≤50 kW, 50–150 kW, 150–350 kW e acima de 350 kW. O segmento de 50–150 kW dominou o mercado com a maior quota de receita em 2025, impulsionada pelo seu equilíbrio ideal entre velocidade de carregamento, custo de infraestrutura e compatibilidade com a maioria dos veículos elétricos de médio alcance e premium. Esta gama de energia é amplamente implantada em estações de recarga urbana, centros comerciais e áreas de estacionamento de varejo devido à sua capacidade de fornecer carregamento eficiente sem tensão excessiva da rede. A crescente expansão da infraestrutura de cobrança pública e o aumento da adoção de EV nas cidades apoiam ainda mais a liderança deste segmento. Sua relação custo-efetividade em relação aos sistemas de ultra-alta potência também incentiva a instalação generalizada.

Prevê-se que o segmento acima de 350 kW testemunhe a taxa de crescimento mais rápida de 2026 a 2033, alimentada pela crescente procura de soluções de carregamento ultra-rápido para veículos elétricos de longo alcance e aplicações pesadas. Aumentar os investimentos em corredores de carregamento de rodovias e plataformas EV de última geração estão impulsionando a adoção de sistemas de carregamento de ultra-alta potência.

• Por Aplicação

Com base na aplicação, o mercado DC Fast Charging é segmentado em Comercial e Residencial. O segmento comercial dominou o mercado com a maior participação de receita em 2025, impulsionado pela implantação em larga escala de estações de carregamento rápido em áreas públicas, como centros comerciais, complexos de escritórios, rodovias e depósitos de frota. A infraestrutura de tarifação comercial beneficia de altas taxas de utilização e forte suporte governamental para o desenvolvimento do ecossistema EV. O número crescente de frotas de veículos elétricos e de serviços de transporte acelera ainda mais a demanda neste segmento. A integração de sistemas de pagamento, monitoramento inteligente e recursos de carregamento de múltiplos veículos aumentam sua atratividade para os operadores.

Espera-se que o segmento Residencial testemunhe um crescimento constante devido ao aumento da adoção de soluções de carregamento de EV em casa. Aumentar a preferência do consumidor pela conveniência de cobrança overnight e políticas de apoio à promoção de instalações de carregador doméstico são fatores fundamentais para a expansão deste segmento.

DC Fast Charging Market Análise Regional

- A Ásia-Pacífico dominou o mercado de carregamento rápido da DC com a maior parcela de receita de 49,48% em 2025, impulsionada pela rápida adoção da EV, forte apoio do governo à eletrificação e implantação em larga escala de infraestrutura pública de carregamento

- A região beneficia com a expansão da fabricação de veículos elétricos, aumento da demanda de mobilidade urbana e investimentos agressivos em redes de carregamento de rodovias e cidades

- Uma forte integração dos sistemas de energias renováveis e o desenvolvimento de redes inteligentes está a acelerar ainda mais a implantação das infra-estruturas nas principais economias

China DC Fast Charging Market Insight

A China teve a maior participação no mercado de carregamento rápido Ásia-Pacífico DC em 2025, apoiado pela sua enorme frota EV, extensa expansão da rede de carregamento e forte apoio político do governo para novos veículos energéticos. O país tem um ecossistema de infraestrutura de carregamento rápido bem estabelecido liderado por serviços públicos apoiados pelo Estado e operadores privados de cobrança. Alta adoção de tecnologias de carregamento ultra-rápido e forte fabricação doméstica de EV estão reforçando ainda mais a liderança do mercado. Além disso, o investimento contínuo em corredores de carregamento de rodovias está fortalecendo o domínio da China na implantação regional.

Índia DC Fast Charging Market Insight

A Índia está presenciando o crescimento mais rápido na região Ásia-Pacífico, impulsionado pelo aumento da adoção de EV, expansão das necessidades de mobilidade urbana e iniciativas governamentais de apoio, como a cobrança de subsídios à infraestrutura. O aumento da penetração de duas rodas elétricas, ônibus e frotas comerciais está aumentando a demanda por estações de carregamento rápido. O desenvolvimento de cidades inteligentes e parcerias público-privadas está acelerando a implantação de infraestrutura em grandes centros urbanos. Além disso, os investimentos crescentes em redes de tarifação renováveis apoiam a expansão do mercado a longo prazo.

Europe DC Fast Charging Market Insight

O mercado de tarifação rápida da Europa DC está se expandindo de forma constante, apoiado por regulamentos rigorosos de emissões, fortes taxas de adoção de EV e infraestrutura de tarifação pública bem desenvolvida. A região está fortemente focada na redução das emissões de carbono, impulsionando a implantação generalizada de estações de carregamento de alta potência nos corredores urbanos e rodoviários. Um forte apoio político à mobilidade e às normas de interoperabilidade em matéria de emissões nulas aumenta ainda mais a eficiência das infra-estruturas. Além disso, o aumento dos investimentos em redes de tarifação ultra-rápida está a reforçar a dinâmica de crescimento regional.

Alemanha DC Fast Charging Market Insight

A Alemanha representou a maior parte do mercado de carregamento rápido da Europa DC em 2025, impulsionada pela sua forte indústria automotiva e rápida mudança para a mobilidade elétrica. O país tem uma extensa rede de carregamento de rodovias apoiada por montadoras líderes e fornecedores de energia. A alta adoção de veículos elétricos premium e o investimento contínuo em estações de carregamento ultra-rápido estão reforçando a demanda de infraestrutura. Além disso, fortes capacidades de engenharia e incentivos governamentais estão reforçando a liderança da Alemanha na expansão da carga EV.

U.K. DC Fast Charging Market Insight

O mercado do Reino Unido é apoiado pelo aumento da adoção de EV, fortes compromissos do governo para eliminar progressivamente os veículos de combustão interna e rápida expansão dos pontos de carregamento públicos. Os crescentes investimentos em centros de carregamento rápido urbano e soluções de carregamento residencial estão impulsionando o desenvolvimento de infraestrutura. O foco do país na mobilidade verde e na neutralidade do carbono está impulsionando a implantação de estações de carregamento de alta velocidade. Além disso, a participação do sector privado em redes de tarifação está a acelerar ainda mais o crescimento do mercado.

América do Norte DC Fast Charging Market Insight

Estima-se que a América do Norte cresça no CAGR mais rápido de 2026 para 2033, impulsionado pelo aumento das vendas de EV, financiamento federal para cobrança de infraestrutura e crescente demanda por mobilidade elétrica de longa distância. Fortes investimentos em corredores de carregamento rápido de rodovias e expansão de frotas EV estão apoiando o crescimento do mercado. Os avanços tecnológicos contínuos em sistemas de carregamento ultra-rápido estão aumentando ainda mais a adoção. Além disso, a crescente colaboração entre montadoras e empresas de energia está acelerando a implantação de infraestrutura em toda a região.

U.S. DC Fast Charging Market Insight

Os EUA representaram a maior participação no mercado de carregamento rápido da DC da América do Norte em 2025, apoiado pela forte adoção de EV, extensos programas de financiamento federal e rápida expansão de redes de carregamento interestaduais. O país beneficia de um ecossistema automotivo e energético altamente desenvolvido que apoia a implantação de infraestrutura em larga escala. A crescente penetração de SUVs elétricos e frotas comerciais EV está aumentando a demanda por estações de carregamento de alta potência. Além disso, o investimento contínuo em tecnologia de carregamento ultra-rápido está reforçando a posição de liderança dos EUA no mercado regional.

DC Fast Charging Market Share

A indústria de carregamento rápido DC é liderada principalmente por empresas bem estabelecidas, incluindo:

- Pulso da PA (UK)

- Siemens AG (Alemanha)

- EVgo (EUA)

- Potência Tata (Índia)

- ABB (Suíça)

- Eletrificar a América (EUA)

- ChargeZone (Índia)

- Schneider Electric (França)

- Soluções de recarga de Shell (Países Baixos)

- Tesla (EUA)

- Alpitronic GmbH (Alemanha)

- Blink Charging Co. (EUA)

- Delta Electronics (Taiwan)

- Bolt. Terra (Índia)

- EVBox (Países Baixos)

- CharIN e.V. (Alemanha)

Últimos desenvolvimentos no mercado global de carregamento rápido de DC

- Em janeiro de 2026, a Schneider Electric lançou o StarCharge Fast 720, uma solução de carregamento rápido de alta potência DC projetada para apoiar a eletrificação em aplicações comerciais, industriais e de uso público. O sistema oferece capacidade de carga de até 720 kW, permitindo carregamento simultâneo de vários veículos elétricos, incluindo caminhões, ônibus e carros de passageiros. Sua arquitetura descentralizada com gerenciamento dinâmico de carga aumenta a eficiência da rede e flexibilidade operacional em locais de carregamento. Espera-se que esse desenvolvimento fortaleça a implantação de cargas ultra-rápidas, reduza significativamente o tempo de carregamento e suporte à expansão escalável da infraestrutura para segmentos EV pesados

- Em setembro de 2025, a ChargeZone, uma das principais operadoras de rede de carregamento EV da Índia, adquiriu a facilidade de carregamento Wadala da Zerovolt em Mumbai através de uma transação em dinheiro, marcando um movimento de consolidação chave no ecossistema de carregamento EV. A instalação adquirida está estrategicamente posicionada ao longo de um grande corredor de transporte e logística e atende principalmente ônibus elétricos e veículos da frota comercial. Essa integração amplia a pegada operacional da ChargeZone e fortalece sua capacidade de atender segmentos de frota de alta utilização. Espera-se que o desenvolvimento acelere a densificação da rede e melhore a confiabilidade do acesso rápido para operadores comerciais de EV na Índia

- Em julho de 2025, Tesla expandiu sua rede Supercharger em toda a Europa, abrindo novas estações de carga rápida DC de alta capacidade em principais rodovias e locais urbanos. A expansão centra-se na melhoria da mobilidade transfronteiriça da EV e na redução do congestionamento da tarifação em corredores de alta procura. Estas novas estações estão equipadas com Supercarregadores V4 de próxima geração, permitindo velocidades de carregamento mais rápidas e melhor compatibilidade com várias marcas EV. Prevê-se que este desenvolvimento aumente a eficiência das viagens de longa distância no domínio da EV e reforce a acessibilidade ultra-rápida ao carregamento em todo o mercado europeu

- Em maio de 2025, a BP Pulse anunciou o lançamento de novos hubs de carregamento rápido de DC de alta potência nos EUA, visando operadores de frota e usuários comerciais de EV. A iniciativa inclui a instalação de estações de carregamento multi-portas capazes de suportar carregamento rápido para vans de entrega, veículos de transporte e caminhões elétricos. Esses hubs são integrados com sistemas de gerenciamento de energia para otimizar a distribuição de energia e reduzir os custos operacionais. Espera-se que esse desenvolvimento aumente a eletrificação da frota, melhore a escalabilidade da infraestrutura de carregamento e reforce a posição da BP no rápido crescimento do mercado norte-americano de carregamento de EV

- Em março de 2025, a ABB E-mobility introduziu uma versão atualizada do seu carregador rápido Terra 360 DC, aumentando a eficiência de carregamento e capacidades de suporte multiveículo. O sistema atualizado permite o carregamento simultâneo de vários EVs com melhor distribuição de energia e tempo de inatividade reduzido entre as sessões. É projetado para implantação em centros comerciais, estações rodoviárias e redes de carregamento urbano. Este desenvolvimento deve acelerar a adoção de infraestrutura de carregamento de alto desempenho e melhorar a eficiência global de utilização em ambientes de carregamento EV densamente implantados

SKU-

Obtenha acesso online ao relatório sobre a primeira nuvem de inteligência de mercado do mundo

- Painel interativo de análise de dados

- Painel de análise da empresa para oportunidades de elevado potencial de crescimento

- Acesso de analista de pesquisa para personalização e customização. consultas

- Análise da concorrência com painel interativo

- Últimas notícias, atualizações e atualizações Análise de tendências

- Aproveite o poder da análise de benchmark para um rastreio abrangente da concorrência

Metodologia de Investigação

A recolha de dados e a análise do ano base são feitas através de módulos de recolha de dados com amostras grandes. A etapa inclui a obtenção de informações de mercado ou dados relacionados através de diversas fontes e estratégias. Inclui examinar e planear antecipadamente todos os dados adquiridos no passado. Da mesma forma, envolve o exame de inconsistências de informação observadas em diferentes fontes de informação. Os dados de mercado são analisados e estimados utilizando modelos estatísticos e coerentes de mercado. Além disso, a análise da quota de mercado e a análise das principais tendências são os principais fatores de sucesso no relatório de mercado. Para saber mais, solicite uma chamada de analista ou abra a sua consulta.

A principal metodologia de investigação utilizada pela equipa de investigação do DBMR é a triangulação de dados que envolve a mineração de dados, a análise do impacto das variáveis de dados no mercado e a validação primária (especialista do setor). Os modelos de dados incluem grelha de posicionamento de fornecedores, análise da linha de tempo do mercado, visão geral e guia de mercado, grelha de posicionamento da empresa, análise de patentes, análise de preços, análise da quota de mercado da empresa, normas de medição, análise global versus regional e de participação dos fornecedores. Para saber mais sobre a metodologia de investigação, faça uma consulta para falar com os nossos especialistas do setor.

Personalização disponível

A Data Bridge Market Research é líder em investigação formativa avançada. Orgulhamo-nos de servir os nossos clientes novos e existentes com dados e análises que correspondem e atendem aos seus objetivos. O relatório pode ser personalizado para incluir análise de tendências de preços de marcas-alvo, compreensão do mercado para países adicionais (solicite a lista de países), dados de resultados de ensaios clínicos, revisão de literatura, mercado remodelado e análise de base de produtos . A análise de mercado dos concorrentes-alvo pode ser analisada desde análises baseadas em tecnologia até estratégias de carteira de mercado. Podemos adicionar quantos concorrentes necessitar de dados no formato e estilo de dados que procura. A nossa equipa de analistas também pode fornecer dados em tabelas dinâmicas de ficheiros Excel em bruto (livro de factos) ou pode ajudá-lo a criar apresentações a partir dos conjuntos de dados disponíveis no relatório.