Global Drug Eluting Stents Des Market

Tamanho do mercado em biliões de dólares

CAGR :

%

USD

8.49 Billion

USD

16.54 Billion

2025

2033

USD

8.49 Billion

USD

16.54 Billion

2025

2033

| 2026 –2033 | |

| USD 8.49 Billion | |

| USD 16.54 Billion | |

| % | |

|

Global Drug Eluting Stents (DES) Market Segmentation, By Coating (Polymer Based Coating, Biodegradable, Non-biodegradable, Polymer Free Coating, Microporous Surface, Microstructured Surface, Slotted Tubular Surface, and Nanoporous Surface), End-Users (Hospitals, Cardiology Centers, and Ambulatory Surgical Centers), Application (Coronary Artery Disease and Peripheral Artery Disease), Drug (Sirolimus, Pactitaxel, Zotarolimus, Everolimus, Biolimus, and Others), Generation (1st Generation, 2nd Generation, 3RD Generation, and 4TH Generation) - Industry Trends and Forecast to 2033

Drug Eluting Stents (DES) Market Size

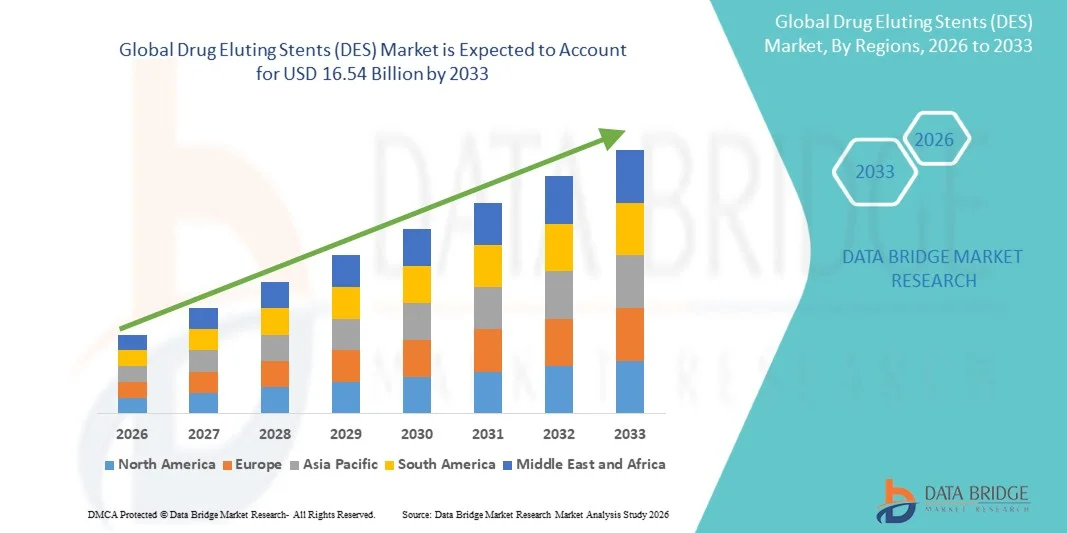

- The global drug eluting stents (DES) market size was valued at USD 8.49 billion in 2025 and is expected to reach USD 16.54 billion by 2033, at a CAGR of 8.70% during the forecast period

- The market growth is largely fueled by the increasing prevalence of cardiovascular diseases, rising adoption of minimally invasive procedures, and technological advancements in stent design and drug delivery systems

- Furthermore, growing patient awareness about advanced treatment options, expanding healthcare infrastructure, and rising demand for outpatient and interventional cardiology procedures are accelerating the uptake of Drug Eluting Stents (DES) solutions, thereby significantly boosting the industry's growth

Drug Eluting Stents (DES) Market Analysis

- Drug Eluting Stents (DES), offering advanced cardiovascular intervention solutions, are increasingly vital components of modern cardiac care in both hospitals and specialty cardiology centers due to their proven efficacy in reducing restenosis, improving patient outcomes, and supporting minimally invasive procedure

- The escalating demand for Drug Eluting Stents is primarily fueled by the rising prevalence of cardiovascular diseases, increasing geriatric populations, growing adoption of percutaneous coronary interventions, and technological advancements in stent coatings and drug-eluting materials

- North America dominated the drug eluting stents (DES) market with the largest revenue share of approximately 44.5% in 2025, supported by advanced healthcare infrastructure, high prevalence of cardiovascular diseases, and strong adoption of minimally invasive procedures. The U.S. is experiencing substantial growth in DES usage across hospitals, cardiac catheterization labs, and specialty cardiology centers, driven by increasing demand for innovative stent designs, drug-eluting technologies, and rising awareness among patients and healthcare providers

- Asia-Pacific is expected to be the fastest-growing region in the drug eluting stents (DES) market during the forecast period, registering a CAGR of approximately 9.3%, fueled by rising incidences of cardiovascular disorders, expanding healthcare infrastructure, growing geriatric populations, and increasing awareness of advanced interventional cardiology procedures in emerging economies such as China and India

- The CAD segment dominated the largest revenue share of 63.5% in 2025, driven by the high prevalence of coronary artery disease globally and central role of DES in PCI

Report Scope and Drug Eluting Stents (DES) Market Segmentation

|

Attributes |

Drug Eluting Stents (DES) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Abbott (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Drug Eluting Stents (DES) Market Trends

“Enhanced Clinical Outcomes Through Advanced Stent Technologies”

- A significant and accelerating trend in the global drug eluting stents (DES) market is the development and adoption of next-generation DES with biodegradable polymers, ultrathin struts, and improved drug-elution profiles, aimed at reducing restenosis and thrombosis risks while enhancing patient safety

- For instance, Boston Scientific’s SYNERGY DES, with its bioabsorbable polymer coating, has been increasingly adopted in hospitals across North America and Europe, showing improved vessel healing and long-term outcomes. Similarly, Abbott’s XIENCE Sierra DES has gained attention for its enhanced deliverability and safety profile

- There is also a growing trend of expanding DES use in high-risk and complex patient populations, including diabetic patients, multi-vessel disease, and chronic total occlusions, in line with updated clinical guidelines

- Manufacturers are focusing on stent platform innovations, including improved radial strength, flexibility, and thinner strut designs, to optimize procedural success and reduce complications

- These technological advancements are reshaping cardiologists’ expectations for interventional procedures and driving demand for more effective and safer DES options

- The global demand for DES that offer improved clinical outcomes is increasing rapidly across both developed and emerging markets, as healthcare providers prioritize patient safety, procedural efficiency, and long-term cardiovascular health

Drug Eluting Stents (DES) Market Dynamics

Driver

“Growing Adoption of Minimally Invasive Cardiac Interventions”

- The increasing prevalence of cardiovascular diseases, coupled with rising awareness of minimally invasive interventions, is a significant driver for DES adoption

- For instance, in 2025, Medtronic reported a substantial rise in DES procedures in European cardiac centers, reflecting a shift from bare-metal stents to DES due to better long-term clinical outcomes and reduced restenosis rates

- Advancements in stent technology and physician training programs are encouraging wider adoption across hospitals and specialized cardiac care centers

- Rising government initiatives promoting cardiovascular health, preventive interventions, and insurance coverage for advanced cardiac procedures further support DES market growth

- The convenience of reduced hospital stays, lower repeat intervention rates, and better patient prognosis are key factors propelling the adoption of DES globally

Restraint/Challenge

“High Cost and Procedural Complexity”

- The high cost of next-generation Drug Eluting Stents (DES), compared to traditional bare-metal stents, continues to be a significant barrier for adoption, particularly in developing countries and smaller healthcare facilities. These costs not only include the stents themselves but also the specialized equipment, hospital infrastructure, and extended procedural time required for optimal outcomes

- For instance, in 2025, several mid-sized hospitals in Southeast Asia reported limited DES adoption due to budgetary constraints, even though clinical evidence demonstrated improved patient outcomes. Similarly, smaller cardiac centers in India and Africa often rely on older stent technologies due to limited reimbursement and resource availability

- Procedural complexity also poses challenges, as the placement of DES requires skilled interventional cardiologists, precise imaging techniques, and post-procedure patient management to minimize risks of thrombosis or restenosis. This requirement for specialized expertise can slow market penetration in regions with a shortage of trained healthcare professionals

- Furthermore, the long-term dual antiplatelet therapy (DAPT) required after DES implantation can limit patient access in areas with lower healthcare literacy or limited follow-up capabilities, raising concerns about adherence and safety

- Despite growing clinical evidence supporting DES efficacy, healthcare providers often weigh the cost, required expertise, and post-procedure care requirements against the perceived benefits, which can delay adoption

- Overcoming these challenges will require strategies such as cost optimization, wider insurance coverage, training programs for cardiologists, and robust patient follow-up initiatives, ensuring that the advantages of DES reach a broader patient population globally

Drug Eluting Stents (DES) Market Scope

The market is segmented on the basis of coating, end-user, application, drug, and generation.

• By Coating

On the basis of coating, the market is segmented into Polymer-Based Coating, Biodegradable, Non-Biodegradable, Polymer-Free Coating, Microporous Surface, Microstructured Surface, Slotted Tubular Surface, and Nanoporous Surface. The Polymer-Based Coating segment dominated the largest market revenue share of 46.1% in 2025, driven by excellent drug-elution performance, biocompatibility, and proven efficacy in reducing restenosis. Hospitals and cardiology centers prefer polymer-based DES for predictable drug release, lower thrombosis risk, and compatibility with complex interventional procedures. Technological improvements in polymer chemistry, including durable and biodegradable polymers, enhance stent performance. Widespread clinical validation and guideline endorsements reinforce adoption. Surgeons favor polymer coatings for high-risk patients. Long-term outcome data, regulatory approvals, and repeat procedural reliability support dominance. Growing awareness about better patient outcomes and post-procedure recovery boosts adoption. The segment benefits from extensive training programs and integration in modern PCI procedures. Market expansion is also aided by increasing cardiovascular disease prevalence and higher interventional volumes.

The Biodegradable coating segment is expected to witness the fastest CAGR of 10.8% from 2026 to 2033, fueled by increasing demand for stents that minimize long-term complications and promote vessel healing. Biodegradable DES gradually resorb after drug delivery, reducing late thrombosis and inflammation. Younger patients and high-risk coronary profiles increasingly adopt biodegradable DES. Technological advances in bioresorbable polymers and controlled drug release improve safety and efficacy. Adoption is driven by clinical guideline support, insurance reimbursement, and positive trial outcomes. Cardiologists prefer biodegradable options for elective and complex interventions. Market growth is further accelerated by rising cardiovascular disease prevalence. Expanding healthcare infrastructure and awareness programs promote uptake. Patient preference for minimally invasive solutions contributes to growth. Collaboration with manufacturers and specialized training programs strengthen market penetration. Continuous innovation in resorption rates and stent flexibility sustains demand.

• By End-User

On the basis of end-user, the DES market is segmented into Hospitals, Cardiology Centers, and Ambulatory Surgical Centers (ASCs). The Hospitals segment dominated the largest revenue share of 55.2% in 2025, driven by high procedural volumes, availability of skilled interventional cardiologists, and comprehensive post-operative care. Hospitals manage complex cases, including multi-vessel interventions and high-risk patients, requiring advanced DES technologies. Infrastructure support, recurring procedure volumes, and long-term follow-up capability reinforce adoption. Hospitals integrate next-generation DES through ongoing trials and standard care protocols. Regulatory approvals and clinical guideline recommendations favor hospital utilization. Repeat interventions and patient outcomes drive stable revenue streams. Hospitals often conduct training and workshops, promoting stent adoption. Wide product availability and strong supplier networks support dominance. Hospitals also invest in cutting-edge interventional equipment. The segment benefits from robust reimbursement systems. Strong brand loyalty and clinical familiarity further reinforce usage.

The Cardiology Centers segment is expected to witness the fastest CAGR of 11.3% from 2026 to 2033, driven by rising numbers of specialized cardiac centers offering focused interventional procedures. Targeted DES implantation for elective coronary and peripheral interventions fuels growth. Patients increasingly prefer specialized cardiac care for quicker procedures and better outcomes. Adoption of biodegradable, polymer-free, and next-generation DES is higher in cardiology centers. Lower operational overheads and flexible infrastructure encourage rapid uptake. Collaboration with DES manufacturers supports technology adoption. Training programs and focused clinical trials strengthen acceptance. Faster procedure turnover enhances revenue potential. Centers often implement digital patient tracking and follow-up systems. Growing awareness among cardiologists accelerates market penetration. Centers focus on advanced stent technologies for complex lesions. Strategic partnerships with hospitals and manufacturers expand market share.

• By Application

On the basis of application, the market is segmented into Coronary Artery Disease (CAD) and Peripheral Artery Disease (PAD). The CAD segment dominated the largest revenue share of 63.5% in 2025, driven by the high prevalence of coronary artery disease globally and central role of DES in PCI. DES reduce restenosis, improve vessel patency, and lower repeat interventions. Hospitals and cardiology centers prioritize CAD treatments due to procedural volumes. Guideline recommendations and reimbursement support reinforce adoption. Technological advances, including polymer-based and biodegradable coatings, improve outcomes. Clinical validation, training programs, and long-term efficacy studies drive usage. Surgeons prefer DES for high-risk and complex patients. Repeat procedure reliability and improved post-operative recovery contribute to dominance. Awareness campaigns and public health initiatives increase CAD patient coverage. Broad availability of stent sizes and types enhances adoption. Market stability is strengthened by recurring interventions. CAD-focused DES dominate procedural volumes in developed and emerging markets.

The PAD segment is expected to witness the fastest CAGR of 9.7% from 2026 to 2033, fueled by rising prevalence of peripheral vascular diseases and expanding DES adoption in limb salvage procedures. Technological improvements, including microstructured and nanoporous surfaces, enhance outcomes. Awareness among vascular specialists drives growth. Insurance reimbursement and clinical guideline adoption accelerate uptake. Advanced stents improve procedural success and reduce restenosis. Patients increasingly prefer minimally invasive solutions. Expansion in emerging markets boosts demand. Centers focus on innovative DES designs for complex PAD lesions. Collaboration with manufacturers promotes trial adoption. Rapid urbanization and lifestyle changes increase PAD incidence. Educational programs for vascular surgeons support technology penetration. Biodegradable and polymer-free options encourage early adoption.

• By Drug

On the basis of drug, DES are segmented into Sirolimus, Paclitaxel, Zotarolimus, Everolimus, Biolimus, and Others. The Everolimus segment dominated with a revenue share of 38.6% in 2025, driven by superior clinical outcomes, lower thrombosis risk, and extensive coronary adoption. Everolimus DES offer predictable drug release, high vessel patency, and reduced restenosis. Regulatory approvals and guideline endorsements enhance usage. Hospitals and cardiology centers widely adopt Everolimus DES. Strong clinical trial evidence supports preference. Surgeons prefer Everolimus for high-risk and multi-vessel lesions. Integration with second- and third-generation DES designs improves patient outcomes. Repeat procedural reliability ensures stable revenue streams. Availability across major markets enhances adoption. Reimbursement support drives hospital and cardiology center uptake. Awareness programs strengthen acceptance. High-quality manufacturing standards ensure consistency. Long-term follow-up data reinforces trust.

The Biolimus segment is expected to witness the fastest CAGR of 10.2% from 2026 to 2033, driven by enhanced anti-proliferative properties and adoption in newer-generation DES for complex lesions. Biolimus DES are favored for high-risk coronary and peripheral interventions. Technological innovation in drug-eluting polymer coatings improves efficacy. Surgeons adopt Biolimus DES to reduce restenosis and thrombosis. Positive clinical trial results encourage hospital and cardiology center uptake. Insurance coverage and guideline endorsements accelerate adoption. Emerging markets show increased acceptance. Integration with biodegradable stents enhances appeal. Reimbursement policies support broader adoption. Rapid growth in interventional procedures drives volume. Training programs for cardiologists promote Biolimus DES usage. Focus on patient outcomes fuels preference.

• By Generation

On the basis of generation, the market is segmented into 1st, 2nd, 3rd, and 4th Generation DES. The 2nd Generation DES dominated the largest revenue share of 41.7% in 2025, attributed to improved polymer coatings, better stent flexibility, and lower restenosis rates compared to 1st generation DES. Hospitals and cardiology centers prefer 2nd generation stents for routine and high-risk interventions. Widespread clinical validation and long-term follow-up data reinforce adoption. Repeat procedural reliability drives recurring revenue. Surgeons favor improved flexibility and deliverability. Regulatory approvals and guideline support enhance confidence. Strong supplier networks ensure consistent availability. Patient outcomes and recovery rates are superior to 1st generation stents. Broad adoption in developed and emerging markets supports dominance. Integration into complex interventional procedures is common. Ongoing clinical trials maintain adoption. High awareness among cardiologists ensures preference.

The 4th Generation DES segment is expected to witness the fastest CAGR of 11.5% from 2026 to 2033, driven by innovations in biodegradable polymers, nanostructured surfaces, and enhanced drug delivery mechanisms. These stents improve patient outcomes and procedural safety. Adoption is fueled by regulatory approvals and guideline endorsements. Hospitals and specialized cardiology centers rapidly integrate 4th generation DES. Technological advancements reduce restenosis and thrombosis risk. Surgeons prefer stents with superior flexibility and precise drug delivery. Emerging markets show increasing adoption due to improved awareness. Integration into minimally invasive procedures boosts uptake. Insurance coverage and reimbursement policies support rapid penetration. Positive clinical outcomes accelerate adoption in high-risk patients. Training programs for interventional cardiologists enhance market growth. Focus on next-generation stent safety and efficacy drives expansion.

Drug Eluting Stents (DES) Market Regional Analysis

- North America dominated the drug eluting stents (DES) market in 2025, capturing the largest revenue share of approximately 44.5%

- This growth is primarily driven by the region’s advanced healthcare infrastructure, high prevalence of cardiovascular diseases, and widespread adoption of minimally invasive procedures

- The presence of leading medical technology companies and strong research and development initiatives further reinforce market leadership in the region

U.S. Drug Eluting Stents (DES) Market Insight

The U.S. drug eluting stents (DES) market accounted for the majority of North America’s DES market, capturing a revenue share of approximately 81% in 2025. Substantial growth has been observed in hospitals, cardiac catheterization laboratories, and specialty cardiology centers, fueled by increasing demand for innovative stent designs and advanced drug-eluting technologies. For instance, top-tier hospitals such as the Mayo Clinic and Cleveland Clinic reported significant increases in DES implantations in 2025, particularly for patients with complex coronary artery disease. The rising awareness among healthcare providers and patients regarding the long-term benefits of DES, including reduced restenosis rates and improved clinical outcomes, continues to drive adoption.

Europe Drug Eluting Stents (DES) Market Insight

The European drug eluting stents (DES) market is projected to expand at a notable CAGR throughout the forecast period, supported by the region’s aging population, growing incidence of cardiovascular disorders, and well-established hospital infrastructure. Countries such as Germany and France are witnessing higher adoption of DES in specialized cardiology centers, as hospitals increasingly prefer drug-eluting stents over bare-metal stents to minimize complications and improve long-term outcomes. Strong regulatory frameworks and emphasis on healthcare innovation further promote the integration of advanced DES technologies into routine interventional cardiology procedures.

United Kingdom Drug Eluting Stents (DES) Market Insight

The U.K. drug eluting stents (DES) market is expected to grow at a noteworthy pace during the forecast period, driven by government initiatives to improve cardiovascular health, expansion of hospital capacities, and increasing awareness of minimally invasive cardiac procedures. For example, NHS cardiac programs in 2025 reported significant expansions in DES implantations among high-risk patient groups, reflecting a clear preference for next-generation stent technologies. This growing adoption contributes to higher procedural volumes in hospitals and specialized cardiac care centers across the country.

Germany Drug Eluting Stents (DES) Market Insight

Germany’s drug eluting stents (DES) market is anticipated to witness considerable growth due to robust healthcare infrastructure, increasing patient awareness, and strong adoption of advanced interventional cardiology practices. Leading German university hospitals have incorporated second-generation DES with enhanced biocompatible coatings for complex coronary interventions, resulting in improved patient outcomes and reduced restenosis rates. Continuous innovation and clinical excellence support sustained market development in the region.

Asia-Pacific Drug Eluting Stents (DES) Market Insight

Asia-Pacific drug eluting stents (DES) market is expected to be the fastest-growing DES market during the forecast period, registering a CAGR of approximately 9.3%. This growth is fueled by rising incidences of cardiovascular disorders, expanding healthcare infrastructure, growing geriatric populations, and increasing awareness of interventional cardiology procedures. Countries such as China and India are witnessing substantial increases in DES procedures within major urban hospitals, driven by government initiatives, expansion of specialized cardiology services, and heightened patient awareness. Rapid modernization of hospital facilities and the growing number of cardiac centers enable the adoption of innovative stent technologies across the region.

Japan Drug Eluting Stents (DES) Market Insight

The Japanese drug eluting stents (DES) market is gaining traction due to the country’s high-tech medical environment, increasing prevalence of coronary artery disease, and demand for minimally invasive cardiac procedures. Cardiology centers in Japan are progressively adopting second-generation DES with advanced biocompatible coatings to enhance patient outcomes and reduce complications. Additionally, the aging population is creating a demand for safer and more effective interventional solutions, supporting sustained market growth.

China Drug Eluting Stents (DES) Market Insight

China drug eluting stents (DES) market accounted for the largest share of the Asia-Pacific DES market in 2025, driven by rapid urbanization, rising middle-class populations, increasing cardiovascular disease prevalence, and expanding hospital infrastructure. Leading hospitals in Beijing and Shanghai reported higher adoption rates of DES in interventional cardiology programs, supported by greater patient awareness, improved insurance coverage, and availability of advanced stent technologies. Government initiatives promoting healthcare modernization and specialized cardiac care programs further bolster market expansion.

Drug Eluting Stents (DES) Market Share

The Drug Eluting Stents (DES) industry is primarily led by well-established companies, including:

• Abbott (U.S.)

• Boston Scientific (U.S.)

• Medtronic (Ireland)

• Terumo Corporation (Japan)

• B. Braun SE (Germany)

• Biotronik SE & Co. KG (Germany)

• C.R. Bard (U.S.)

• Cook Medical (U.S.)

• MicroPort Scientific Corporation (China)

• Lepu Medical Technology (China)

• OrbusNeich Medical (Hong Kong)

• Shandong Weigao Group Medical Polymer Company (China)

• Volcano Corporation (U.S.)

• QualiMed (France)

• Sinomed (China)

• Hangzhou MicroPort Medical (China)

• InspireMD (Israel)

• Balton (Poland)

• Biosensors International Group (Singapore)

• Terumo Interventional Systems (Japan)

Latest Developments in Global Drug Eluting Stents (DES) Market

- In October 2023, Medinol Ltd. announced that its EluNIR‑PERL™ drug‑eluting coronary stent system received approval from the U.S. Food and Drug Administration (FDA) for the treatment of coronary artery disease. The EluNIR‑PERL DES builds upon Medinol’s existing EluNIR platform and features enhanced radiopaque markers and an improved hybrid polymer‑metal catheter tip for more precise navigation and placement during percutaneous coronary interventions. This approval marked a significant expansion of advanced DES options available to interventional cardiologists in the U.S.

- In May 2024, Abbott announced the launch of its XIENCE Sierra Everolimus Eluting Coronary Stent System in India, introducing the latest generation in the XIENCE family of DES products. This launch expanded access to a high‑performance stent platform that aims to improve patient outcomes in coronary artery disease treatment, reflecting ongoing global commercialization efforts by major DES manufacturers

- In June 2024, the U.S. FDA granted Breakthrough Device Designation to Elixir Medical’s DynamX Sirolimus‑Eluting Coronary Bioadaptor System, a next‑generation bioadaptive DES designed to enhance coronary lumen diameter and reduce plaque progression. This designation accelerated regulatory review for a bioadaptive implant that could provide a new therapeutic option in interventional cardiology

- In June 2025, Teleflex plc completed a €760 million acquisition of BIOTRONIK’s Vascular Intervention business, which includes DES products such as the Freesolve drug‑eluting resorbable stent (CE marked in 2024) and the Orsiro Mission Drug Eluting Stent. This strategic acquisition broadened Teleflex’s portfolio across coronary and peripheral DES technologies and positioned the company for expanded global commercialization efforts

- In September 2025, Abbott received Health Canada approval for its Esprit BTK Everolimus Eluting Resorbable Scaffold System, a new‑generation dissolvable DES designed for use below the knee in peripheral arterial disease treatment. The approval marked a key regulatory milestone enabling broader availability of advanced DES solutions for complex vascular conditions in North America

SKU-

Obtenha acesso online ao relatório sobre a primeira nuvem de inteligência de mercado do mundo

- Painel interativo de análise de dados

- Painel de análise da empresa para oportunidades de elevado potencial de crescimento

- Acesso de analista de pesquisa para personalização e customização. consultas

- Análise da concorrência com painel interativo

- Últimas notícias, atualizações e atualizações Análise de tendências

- Aproveite o poder da análise de benchmark para um rastreio abrangente da concorrência

Metodologia de Investigação

A recolha de dados e a análise do ano base são feitas através de módulos de recolha de dados com amostras grandes. A etapa inclui a obtenção de informações de mercado ou dados relacionados através de diversas fontes e estratégias. Inclui examinar e planear antecipadamente todos os dados adquiridos no passado. Da mesma forma, envolve o exame de inconsistências de informação observadas em diferentes fontes de informação. Os dados de mercado são analisados e estimados utilizando modelos estatísticos e coerentes de mercado. Além disso, a análise da quota de mercado e a análise das principais tendências são os principais fatores de sucesso no relatório de mercado. Para saber mais, solicite uma chamada de analista ou abra a sua consulta.

A principal metodologia de investigação utilizada pela equipa de investigação do DBMR é a triangulação de dados que envolve a mineração de dados, a análise do impacto das variáveis de dados no mercado e a validação primária (especialista do setor). Os modelos de dados incluem grelha de posicionamento de fornecedores, análise da linha de tempo do mercado, visão geral e guia de mercado, grelha de posicionamento da empresa, análise de patentes, análise de preços, análise da quota de mercado da empresa, normas de medição, análise global versus regional e de participação dos fornecedores. Para saber mais sobre a metodologia de investigação, faça uma consulta para falar com os nossos especialistas do setor.

Personalização disponível

A Data Bridge Market Research é líder em investigação formativa avançada. Orgulhamo-nos de servir os nossos clientes novos e existentes com dados e análises que correspondem e atendem aos seus objetivos. O relatório pode ser personalizado para incluir análise de tendências de preços de marcas-alvo, compreensão do mercado para países adicionais (solicite a lista de países), dados de resultados de ensaios clínicos, revisão de literatura, mercado remodelado e análise de base de produtos . A análise de mercado dos concorrentes-alvo pode ser analisada desde análises baseadas em tecnologia até estratégias de carteira de mercado. Podemos adicionar quantos concorrentes necessitar de dados no formato e estilo de dados que procura. A nossa equipa de analistas também pode fornecer dados em tabelas dinâmicas de ficheiros Excel em bruto (livro de factos) ou pode ajudá-lo a criar apresentações a partir dos conjuntos de dados disponíveis no relatório.