Global Fcrn Inhibitor Drug Market

Tamanho do mercado em biliões de dólares

CAGR :

%

USD

2.04 Billion

USD

7.21 Billion

2025

2033

USD

2.04 Billion

USD

7.21 Billion

2025

2033

| 2026 –2033 | |

| USD 2.04 Billion | |

| USD 7.21 Billion | |

| % | |

|

Segmentação Global de Inibidores do Mercado de Medicamentos FcRn, Por Tipo de Medicamentos (Inibidores com Fragmento Fc, Anticorpos Monoclonais Anti-FcRn, e Outros), Por Indicação (Miastenia Generalizada Gravis, Polineuropatia Inflamada Crônica Desmielinizante, Trombocitopenia Imunológica Primária, Pênfigus Vulgaris, Anemia Hemolítica Autoimune Quente, Doença Ocular Tiróide, e Outros), Por Rota de Administração (Intravenosa, subcutânea, e Outros), Por Usuário Final (Hospitales, Neurologia Especializada e Clínicas Imunológicas, Institutos Acadêmicos e de Pesquisa e Outros), Por Canal de Distribuição ( Farmácia Hospital, Farmácia Especial e Farmácia Online) - Tendências e Previsão para 2033

Inibidor de FcRnTamanho do Mercado

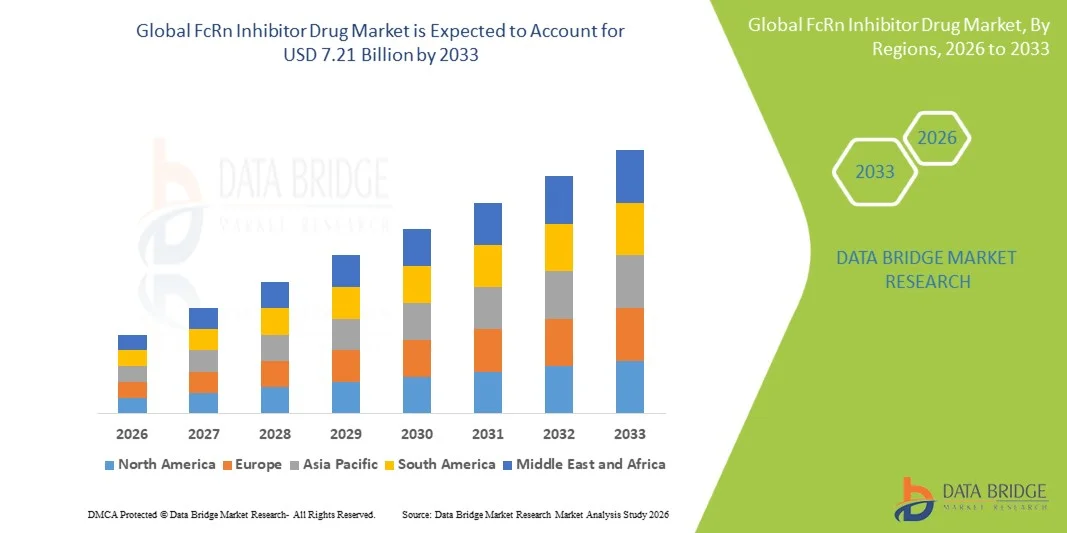

- A dimensão global do mercado de medicamentos inibidores da FcRn foi avaliada emUSD 2,04 mil milhões em 2025e espera-se alcançar7,21 mil milhões de USD até 2033, emCAGR de 17,10%durante o período de previsão

- O crescimento do mercado é amplamente alimentado pelo sucesso comercial sem precedentes de efgartigimod (Vyvgart) gerando USD 2,2 bilhões em vendas líquidas globais em 2024, o portfólio em expansão de indicações de inibidores de FcRn aprovados, incluindo miastenia gravis generalizada, polineuropatia desmielinizante inflamatória crônica e trombocitopenia imune primária, e o oleoduto clínico ampliando visando mais de 20 condições autoimunes e neurológicas

- Além disso, a aprovação pela FDA de abril de 2025 do nipocalimab (Imaavy) como o primeiro antagonista da FcRn demonstrando controle sustentado da doença na população de pacientes com GMG mais ampla, o crescente reconhecimento do bloqueio da FcRn como uma alternativa superior à imunossupressão ampla, e o oleoduto inibidor da FcRn em rápida expansão de empresas, incluindo Immunovant e Viridian Therapeutics, estão estabelecendo a inibição da FcRn como a plataforma terapêutica transformadora do manejo moderno da doença autoimune. Esses fatores convergentes estão acelerando a captação de soluções inibidoras de FcRn, aumentando significativamente o crescimento da indústria

Inibidor de FcRnAnálise de mercado

- As drogas inibidoras da FcRn, funcionando pelo bloqueio competitivo do receptor de Fc neonatal para interromper o mecanismo de reciclagem de IgG e acelerar a degradação lisossômica dos anticorpos circulantes da imunoglobulina G, são cada vez mais reconhecidas como terapias de imunologia de precisão transformadora para doenças mediadas por autoanticorpos devido à sua capacidade de reduzir seletivamente a IgG patogênica sem suprimir amplamente o sistema imunológico

- A crescente demanda por inibidores da FcRn é principalmente alimentada pela substancial diferenciação clínica sobre os imunossupressores convencionais, incluindo corticosteroides e inibidores da calcineurina, pela expansão do roster de condições autoimunes com autoanticorpos patogênicos IgG que conduzem a doença que são passíveis de bloqueio da FcRn, e pela crescente tração comercial de agentes aprovados através da miastenia gravis generalizada e outras indicações autoimunes neuromusculares e hematológicas.

- A América do Norte dominou o mercado de drogas inibidoras de FcRn com a maior participação de receita de 30.00% em 2025, caracterizada pelos EUA representando o maior contribuinte de receita de um país com a adoção comercial precoce de Vyvgart, Rystiggo e Imaavy, caminhos regulatórios robustos da FDA que suportam aprovações aceleradas através de múltiplas indicações de inibidores de FcRn, e a presença de desenvolvedores pioneiros de inibidores de FcRn argenx, UCB, Johnson e Johnson, e Immunovant

- Asia-Pacific é esperado para ser a região de crescimento mais rápido no mercado de drogas inibidor FcRn durante o período de previsão devido à rápida expansão da consciência da doença autoimune, aumento da infraestrutura de neurologia e imunologia especialistas, e crescente aprovação regulatória do inibidor FcRn no Japão e China

- O segmento intravenoso teve a maior parcela de receita de mercado de 61,2% em 2025, impulsionada pelo seu uso generalizado na administração hospitalar e ação terapêutica rápida em condições autoimunes graves.

Âmbito do relatório eSegmentação do Mercado de Medicamentos Inibidores da FcRn

|

Atributos |

Chave do Inibidor de Drogas FcRnPerspectivas de mercado |

|

Segmentos Cobertos |

|

|

Países abrangidos |

América do Norte · U.S. · Canadá · México Europa · Alemanha · França · U.K. · Países Baixos · Suíça · Bélgica · Rússia · Itália · Espanha · Turquia · Resto da Europa Ásia- Pacífico · China · Japão · Índia · Coreia do Sul · Singapura · Malásia · Austrália · Tailândia · Indonésia · Filipinas · Resto da Ásia-Pacífico Médio Oriente e África · Arábia Saudita · U.A.E. · África do Sul · Egito · Israel · Resto do Oriente Médio e África América do Sul · Brasil · Argentina · Resto da América do Sul |

|

Jogadores do mercado chave |

·Johnson e Johnson(EUA) ·Immunovant Inc.(EUA) ·Terapêutica Viridian(EUA) ·Pfizer Inc.. (EUA) ·Roche(Suíça) · AstraZeneca (U.K.) · Biogen Inc. (EUA) · Novartis AG (Suíça) · Sanofi (França) · AbbVie (EUA) · GSK plc (U.K.) · Indústrias Farmacêuticas Teva (Israel) · Grupo Zydus (Índia) · Ciências Roivant (EUA) · Momenta Pharmaceuticals/Johnson and Johnson (EUA) · UCB Biosciences (EUA) · Tecnologias Alpha Cancer (Canadá) · HanAll Biopharma (Coreia do Sul) |

|

Oportunidades de Mercado |

· Expansão em mais de 20 indicações auto-imunes mediadas por IgG · Desenvolvimento da plataforma de auto-administração subcutânea crescente |

|

Informações sobre o Valor Adicionado |

Além dos insights sobre cenários de mercado, como valor de mercado, taxa de crescimento, segmentação, cobertura geográfica e grandes atores, os relatórios de mercado curados pela Data Bridge Market Research também incluem análise de especialistas em profundidade, epidemiologia de pacientes, análise de pipelines, análise de preços e marco regulatório. |

Tendências do Mercado de Drogas Inibidores da FcRn

“Plataformas de Auto-Administração subcutânea e Indicação Expansão Conduzindo Crescimento Comercial“

- Uma tendência significativa e acelerada no mercado global de medicamentos inibidores de FcRn é o desenvolvimento estratégico de formulações de autoadministração subcutânea e formatos de entrega centrados no paciente, incluindo seringas pré-cheias e autoinjetores que estão melhorando substancialmente a conveniência do tratamento, ampliando a independência do paciente e estendendo a penetração do mercado de inibidores de FcRn para além das configurações de hospital e centro de infusão para administração domiciliar.

- Por exemplo, o argenx obteve a aprovação do FDA para a formulação subcutânea de efgartigimod VYVGART Hytrulo em junho de 2023, oferecendo uma dose fixa de 1.008 mg administrável através de uma única injeção de 30 a 90 segundos em ciclos semanais. Em Maio de 2024, mais de 10 000 doentes globalmente tinham sido tratados com ambas as formulações de Vyvgart e o argenx recebeu subsequentemente a aprovação da FDA para um formato de administração pré-cheia de seringas que permitia a auto-injeção para as indicações de gMG e CIDP, aumentando significativamente a autonomia dos doentes na gestão dos seus esquemas de tratamento.

- A tendência para o parto subcutâneo está permitindo o acesso ao inibidor de FcRn em uma ampla gama de ambientes de saúde além dos centros de infusão hospitalares. Além disso, espera-se que o desenvolvimento de plataformas autoinjectoras para o efgartigimod previsto até 2027 e a investigação de regimes posológicos ainda menos frequentes para o nipocalimab diferenciem ainda mais os inibidores da FcRn das alternativas dependentes da perfusão, incluindo a IVIG e a plasmaferese, reforçando a sua proposta de valor comercial para pagadores e doentes

- A integração perfeita da administração subcutânea do inibidor de FcRn com programas de suporte domiciliar liderados por enfermeiros, plataformas de adesão digital e serviços de entrega de farmácia especializada está facilitando o gerenciamento centralizado do paciente através de múltiplas indicações de uma única plataforma de tratamento. Através de mecanismos unificados de bloqueio FcRn, a mesma classe molecular pode ser alavancada através de neurologia, reumatologia, hematologia e especialidades dermatológicas com adaptações de dosagem específicas para indicação

- Essa tendência para plataformas inibidoras de FcRn mais convenientes, empowering do paciente e multi-indication está fundamentalmente reformulando a dinâmica competitiva do mercado biológico autoimune. Consequentemente, empresas como o Immunovant avançam simultaneamente com o IMVT-1402 em 10 indicações, e o Viridian Therapeutics está a desenvolver o VRDN-006 e o VRDN-008 como inibidores da FcRn de última geração com potencial melhor diferenciação de classe.

- A demanda por inibidores subcutâneos de FcRn com capacidade de autoadministração e ampla cobertura multiindicação está crescendo rapidamente em ambas as especialidades de neurologia e reumatologia-imunologia, pois clínicos e pacientes priorizam cada vez mais a conveniência do tratamento e reduzem a utilização de recursos de saúde como elementos-chave do manejo da doença autoimune.

Dinâmicas do Mercado de Drogas Inibidores da FcRn

Controlador

“Expansão comercial rápida através de múltiplas indicações aprovadas impulsionando o crescimento do mercado”

- O extraordinário sucesso comercial de efgartigimod atingir o status de sucesso dentro de dois anos após sua aprovação da FDA em dezembro de 2021, combinado com a rápida expansão regulatória dos inibidores de FcRn em múltiplas indicações autoimunes de alta prevalência, é o principal impulsionador do crescimento excepcional do mercado no espaço global de medicamentos inibidores de FcRn

- Por exemplo, em junho de 2024, efgartigimod recebeu aprovação do FDA para polineuropatia desmielinizante inflamatória crônica, tornando-se o primeiro e único bloqueador FcRn indicado para essa população de pacientes, com o estudo ADHERE representando o maior ensaio controlado randomizado de qualquer tratamento com CIDP até o momento. Espera-se que tais expansões rápidas das empresas-chave conduzam substancialmente ao crescimento do mercado dos inibidores da FcRn ao longo do período previsto

- Como a evidência clínica para o bloqueio da FcRn continua a acumular-se através de uma lista crescente de doenças patogênicas mediadas por IgG, incluindo pênfigo vulgar, anemia hemolítica autoimune morna, doença ocular tireoidiana e vasculite associada à ANCA, a confiança do médico em prescrever inibidores da FcRn para além de sua base inicial da GMG está se expandindo rapidamente, criando múltiplas novas ondas comerciais de crescimento de mercado específico de indicação.

- Além disso, a aprovação pela FDA de abril de 2025 do nipocalimab (Imaavy) acrescentando um segundo anticorpo monoclonal FcRn comercialmente disponível para gMG está intensificando a concorrência no mercado, validando simultaneamente a viabilidade comercial da classe inibidora FcRn e ampliando a familiaridade do médico com o bloqueio FcRn como uma modalidade de tratamento, que deve ampliar a adoção global do mercado.

- O crescente reconhecimento por parte dos pagadores de inibidores de FcRn como alternativas custo-efetivas à IVIG crônica e à plasmaferese para o manejo de doenças autoimunes de longo prazo, combinado com resultados favoráveis de avaliação de tecnologias de saúde que apoiam amplo reembolso em grandes mercados, está removendo barreiras de acesso e impulsionando a penetração sustentada do mercado em populações de pacientes adultos e pediátricos.

Restrição/Desafio

“Altos Custos com Drogas, Competição Biosimilar Horizon e Considerações de Segurança do Colesterol LDL“

- O preço premium das terapias inibidoras de FcRn, que frequentemente requerem ciclos de tratamento contínuos com agentes biológicos a preços de vários milhares de dólares por ciclo, representa um desafio significativo para a ampla penetração no mercado, particularmente em mercados com infraestrutura de reembolso de imunologia especializada limitada, sistemas de saúde sensíveis aos preços e rigorosos critérios de avaliação de tecnologias de saúde que podem restringir o acesso de fórmulas a subpopulações específicas de pacientes

- Por exemplo, alguns candidatos a inibidores da FcRn no desenvolvimento, incluindo o batoclimabe de Immunovant, foram associados a elevações do colesterol LDL em ensaios clínicos, criando preocupações de diferenciação de segurança que podem influenciar a escolha do prescritor entre inibidores concorrentes da FcRn e requerem monitorização adicional da segurança cardiovascular em doentes em risco. A priorização estratégica da Imunovant da IMVT-1402 sobre o batoclimabe foi impulsionada, em parte, pela necessidade de desenvolver um composto sem a responsabilidade pelo colesterol LDL observada com doses mais elevadas de batoclimabe

- A aproximação de clichês de exclusividade de patentes para inibidores de FcRn de primeira geração, incluindo efgartigimod, combinada com a entrada antecipada de inibidores de FcRn biossimilares após expiração de patente no início de 2030, cria incerteza comercial de longo prazo que está influenciando decisões de investimento de pipeline e estratégias de posicionamento competitivo entre desenvolvedores de inibidores de FcRn.

- Empresas como a argenx estão enfrentando desafios de preços e acesso por meio de discussões de contratação baseadas em resultados com pagadores, enquanto o desenvolvimento da Immunovant de IMVT-1402 com um perfil de segurança diferenciado e o desenvolvimento da Viridian Therapeutics de VRDN-006 visam fornecer opções clinicamente superiores que justifiquem o posicionamento premium em uma paisagem cada vez mais competitiva do inibidor FcRn

- Superar esses desafios através de modelos de preços baseados em resultados, desenvolver inibidores FcRn de próxima geração com melhores perfis de segurança e conveniência, e expandir a educação do pagador sobre a economia de custos a longo prazo do gerenciamento de doenças baseado em FcRn sobre a imunossupressão convencional será vital para o crescimento sustentado do mercado global de medicamentos inibidores FcRn

Âmbito do Inibidor do Mercado de Drogas FcRn

O mercado é segmentado com base no tipo de droga, indicação, via de administração, usuário final e canal de distribuição.

- Por tipo de droga

Com base no tipo de fármaco, o Mercado de Inibidores de FcRn é segmentado em inibidores baseados em fragmentos de Fc, anticorpos monoclonais anti-FcRn e outros. O segmento monoclonal de anticorpos anti-FcRn dominou a maior parcela de receita de mercado de 54,6% em 2025, impulsionada por forte eficácia clínica, redução da imunoglobulina G (IgG) direcionada e crescente adoção no manejo da doença autoimune. Essas terapias demonstram melhores perfis de segurança e efeitos imunomoduladores sustentados, tornando-os altamente preferidos em condições crônicas. Aumentando as aprovações de biologics e expandindo pipelines clínicos mais dominância do segmento de apoio. O aumento da prevalência de doenças autoimunes mediadas por anticorpos contribui significativamente para a demanda. As empresas farmacêuticas estão investindo fortemente em anticorpos monoclonais de próxima geração com meia-vida e seletividade melhoradas. Aumentar a preferência do médico por biológicos direcionados em relação aos imunossupressores convencionais fortalece a adoção. A expansão dos gasodutos de I&D nas principais empresas de biotecnologia impulsiona ainda mais o crescimento.

Espera-se que o segmento de inibidores baseados em fragmentos de Fc testemunhe o CAGR mais rápido de 18,7% de 2026 a 2033, impulsionado pelo aumento da pesquisa clínica e desenvolvimento de construtos de Fc projetados com inibição de ligação ao receptor aprimorado. Estas moléculas oferecem uma melhor farmacocinética e uma menor frequência de administração em comparação com as terapêuticas convencionais. A crescente procura de regimes de tratamento compatíveis com o doente apoia a adopção. O crescente investimento no receptor de Fc neonatal (FcRn) visando a pesquisa acelera a inovação. Expandir aplicações em várias doenças autoimunes impulsiona ainda mais o crescimento. Aumentar o foco na medicina personalizada aumenta o potencial do segmento. Ensaios clínicos iniciais estão mostrando resultados promissores de eficácia. Colaborações biotecnológicas também estão alimentando a expansão do gasoduto.

- Por Indicação

Com base na indicação, o mercado é segmentado em miastenia gravis generalizada, polineuropatia desmielinizante inflamatória crônica, trombocitopenia imune primária, pênfigo vulgar, anemia hemolítica autoimune quente, doença ocular tireoidiana, entre outros. O segmento de miastenia gravis generalizada representou a maior parcela de receita de mercado de 32,8% em 2025, impulsionada pela alta prevalência da doença e forte sucesso clínico dos inibidores da FcRn na redução dos anticorpos patogênicos IgG. Aumentar as taxas de diagnóstico e o conhecimento das doenças neuromusculares autoimunes suportam ainda mais a dominância do segmento. A disponibilidade de biológicos direcionados melhorou significativamente os resultados do tratamento. A adoção crescente de terapias poupadoras de esteróides contribui para o crescimento. Expandir as diretrizes clínicas recomendando inibidores de FcRn fortalece o uso. Aumentar a preferência do paciente por terapias não esteroides de longo prazo suporta ainda mais a demanda. As aprovações farmacêuticas para tratamentos de miastenia gravis impulsionam a expansão do mercado.

Espera-se que o segmento primário de trombocitopenia imune testemunhe o CAGR mais rápido de 19,3% de 2026 a 2033, impulsionado pelo uso crescente de inibidores de FcRn como terapia de segunda linha para casos refratários. A incidência crescente de distúrbios plaquetários e condições autoimunes suporta a demanda. Resultados melhorados de ensaios clínicos que demonstram rápida recuperação da contagem de plaquetas aceleram a adoção. A preferência crescente por biológicos específicos sobre imunossupressores aumenta o crescimento. A expansão do acesso ao tratamento nas economias emergentes apoia ainda mais a adopção. Aumentar o conhecimento médico e inclusão de diretrizes aumentar as taxas de prescrição. Expansões contínuas de gasodutos em empresas de biotecnologia também contribuem para o crescimento.

- Por Via de Administração

Com base na via de administração, o mercado é segmentado para intravenosa, subcutânea e outras. O segmento intravenoso teve a maior parcela de receita de mercado de 61,2% em 2025, impulsionada pelo seu uso generalizado na administração hospitalar e ação terapêutica rápida em condições autoimunes graves. A perfusão intravenosa garante uma dosagem precisa e biodisponibilidade imediata, tornando-a preferível em situações de cuidados agudos. A alta adoção inicial de inibidores biológicos da FcRn está concentrada em ambientes hospitalares. O uso crescente em enfermarias de neurologia e imunologia suporta a dominância. A familiaridade do médico com os biológicos IV reforça ainda mais a captação. As estruturas de reembolso hospitalar também favorecem terapias intravenosas. A elevação das taxas de internação por condições autoimunes contribui para a demanda.

Espera-se que o segmento subcutâneo testemunhe o CAGR mais rápido de 20,1% de 2026 a 2033, impulsionado pela preferência do paciente pela autoadministração e pela redução das consultas hospitalares. As formulações subcutâneas melhoram a conveniência, a adesão e o manejo da doença em longo prazo. Os avanços na tecnologia de formulação de medicamentos permitem maiores intervalos de dosagem. A crescente mudança para o cuidado domiciliar apoia a adoção. O aumento do desenvolvimento de seringas pré-cheias e auto-injetores acelera a usabilidade. Os sistemas de saúde favorecem modelos de tratamento ambulatorial custo-efetivo. A ampliação das aprovações regulatórias para os biológicos subcutâneos aumenta ainda mais o crescimento.

- Por Usuário Final

Com base no usuário final, o mercado é segmentado em hospitais, clínicas especiais de neurologia e imunologia, institutos acadêmicos e de pesquisa, entre outros. O segmento hospitalar dominou o maior percentual de receita de mercado de 57,9% em 2025, impulsionado pelo alto fluxo de pacientes, disponibilidade de infraestrutura de infusão e manejo de condições autoimunes graves que requerem terapia biológica. Os hospitais permanecem centros primários para administração de inibidores de FcRn. Fortes sistemas de reembolso e disponibilidade especializada apoiam ainda mais o domínio. O aumento das taxas de internação por doenças autoimunes contribui para a demanda. Os hospitais também lideram na adoção clínica de biológicos recém-aprovados. Capacidades diagnósticas avançadas aumentam as taxas de iniciação do tratamento. A expansão global da infraestrutura de saúde fortalece ainda mais esse segmento.

Espera-se que o segmento especializado de clínicas de neurologia e imunologia testemunhe o CAGR mais rápido de 18,4% de 2026 a 2033, impulsionado pelo aumento da descentralização do manejo da doença autoimune. Essas clínicas oferecem atendimento especializado com diagnóstico mais rápido e início do tratamento. A preferência crescente pela terapia biológica ambulatorial suporta o crescimento. A ampliação do número de centros especializados em mercados desenvolvidos e emergentes impulsiona o acesso. Melhor experiência médica em doenças autoimunes acelera a adoção. Aumentar a preferência do paciente por ambientes de cuidado focados impulsiona ainda mais a demanda. O uso crescente de biológicos direcionados em ambientes ambulatoriais suporta expansão.

- Por Canal de Distribuição

Com base no canal de distribuição, o mercado é segmentado em farmácia hospitalar, farmácia especializada e farmácia online. O segmento de farmácia hospitalar detinha a maior parcela de receita de mercado de 66,5% em 2025, impulsionada pela administração direta de inibidores de FcRn em ambientes hospitalares e sistemas de aquisição fortes. Farmácias hospitalares garantem armazenamento controlado, dispensação e monitoramento de biológicos. A alta dependência do tratamento hospitalar suporta a dominância. Os requisitos de conformidade regulamentar reforçam ainda mais este canal. O aumento das terapias biológicas hospitalares contribui para o crescimento. Fortes acordos institucionais de compra aumentam a disponibilidade. A elevação das taxas de hospitalização autoimune suporta a demanda continuada.

Espera-se que o segmento de farmácia especializada testemunhe o CAGR mais rápido de 21,5% de 2026 a 2033, impulsionado pelo aumento do deslocamento para o manejo ambulatorial da terapia biológica. As farmácias especializadas fornecem suporte ao paciente, programas de adesão e serviços de entrega domiciliar. O uso crescente de terapias subcutâneas autoadministradas aumenta a demanda. A ampliação da cobertura de seguros para medicamentos especializados apoia o crescimento. O aumento da carga de doenças crônicas impulsiona a distribuição do tratamento a longo prazo. A adoção crescente de biológicos fora do ambiente hospitalar acelera a expansão. A melhoria da logística de cadeia fria dá suporte à acessibilidade.

Análise Regional do Mercado de Drogas Inibidor da FcRn

- A América do Norte dominou o mercado de drogas inibidoras de FcRn com a maior participação de receita de 30.00% em 2025, impulsionado pelos EUA, representando o maior mercado de inibidores de FcRn comercial do mundo com a primeira e mais rápida adoção de efgartigimod, rozanolixizumab e nipocalimab após suas aprovações da FDA, apoiados por reembolso favorável de doenças raras, alta conscientização neurologista, e as fortes infraestruturas comerciais de argenx, UCB, Johnson e Johnson

- Os consumidores da região se beneficiam das vias regulatórias mais avançadas de doenças raras em todo o mundo, com o FDA concedendo múltiplas terapias inovadoras, designações de medicamentos rápidos e órfãos para candidatos a inibidores de FcRn, e a crescente lista de indicações aprovadas através de gMG, CIDP e ITP criando uma ampla base comercial para terapias de bloqueio de FcRn

- Esta adoção generalizada é ainda apoiada por altas rendas disponíveis no sistema de saúde dos EUA, robusta infraestrutura de cuidados especializados em neurologia e imunologia, e pelo crescente reconhecimento entre neurologistas e hematologistas de que a inibição da FcRn oferece uma alternativa direcionada, rapidamente eficaz e bem tolerada à imunossupressão ampla convencional para doenças autoimunes mediadas por IgG

Inibidor do Mercado de Drogas dos EUA

O mercado de drogas inibidor FcRn dos EUA capturou a maior participação de receita na América do Norte em 2025, alimentada pela efgartigimod gerando USD 2,2 bilhões em vendas líquidas globais em 2024 com os EUA representando o maior contribuinte de receita de um país único, a aprovação de junho de 2023 da VYVGART Hytrulo para gMG proporcionando conveniência subcutânea que acelera o início de novo paciente, e a aprovação de junho de 2024 do efgartigimod CIDP acrescentando uma nova indicação de alta prevalência com substancial oportunidade comercial. A aprovação da FDA em abril de 2025 do nipocalimab (Imaavy), oferecendo controle sustentado da doença na população mais ampla do gMG, está expandindo ainda mais a adoção do inibidor de FcRn e gerando uma dinâmica competitiva esperada para aumentar a consciência geral do mercado.

Inibidor do Mercado de Drogas da Europa

Projeta-se que o mercado europeu de medicamentos inibidores de FcRn se expanda em um CAGR substancial ao longo do período de previsão, impulsionado principalmente pela ampliação das aprovações EMA para efgartigimod no gMG e CIDP, a submissão de setembro de 2024 do pedido de Autorização de Introdução no Mercado por Janssen-Cilag para nipocalimab no gMG, e a crescente rede de centros especializados de doenças neuromusculares e transtornos autoimunes em toda a Alemanha, França, Reino Unido e Holanda adotando protocolos de terapia inibidora de FcRn. O crescimento do mercado de inibidores europeus de FcRn é ainda apoiado por programas nacionais de doenças raras, resultados favoráveis da avaliação de tecnologias de saúde para efgartigimod em mercados-chave, e a robusta infraestrutura de pesquisa clínica facilitando ensaios de inibidores de FcRn Fase 3 em centros especializados europeus.

Inibidor do Mercado de Drogas do Reino Unido FcRn

O mercado de medicamentos inibidores de FcRn do Reino Unido é esperado para crescer em um CAGR notável durante o período de previsão, impulsionado por avaliações de tecnologia NICE avaliando efgartigimod para gMG e CIDP, crescendo redes de centros de doenças neuromusculares especialistas da NHS Inglaterra, e o alinhamento regulatório progressivo da MHRA com as aprovações da FDA permitindo o acesso oportuno do paciente aos inibidores recém aprovados de FcRn. A forte comunidade de pesquisa neurológica acadêmica do Reino Unido em instituições, incluindo University College London e King's College London, está contribuindo para a geração de evidências do mundo real.

Alemanha FcRn Inibidor do Mercado de Drogas

Espera-se que o mercado de medicamentos inibidores da FcRn da Alemanha se expanda em um considerável CAGR durante o período de previsão, alimentado pelo início do lançamento comercial de efgartigimod na Alemanha após a aprovação da EMA, a cobertura legal de seguro de saúde bem desenvolvida do país para doenças autoimunes raras biológicas, e os principais centros acadêmicos de doenças neuromusculares em Munique, Berlim e Heidelberg adotando ativamente protocolos inibidores da FcRn para o gerenciamento de gMG e CIDP. A ênfase da Alemanha no tratamento personalizado de doenças autoimunes e forte ecossistema de defesa de doenças raras apoia a adoção de inibidores FcRn.

Inibidor do Mercado de Drogas da Ásia-Pacífico

O mercado de drogas inibidoras de FcRn Ásia-Pacífico está pronto para crescer no CAGR mais rápido durante o período de previsão de 2026 a 2033, impulsionado pela aprovação de março de 2024 do efgartigimod IV pelo MHLW do Japão para a trombocitopenia imune primária, acrescentando às suas aprovações existentes de GMG e CIDP no Japão, e o crescente impulso regulatório e comercial para inibidores de FcRn em toda a Coreia do Sul, Austrália e China. Por exemplo, Vyvgart é aprovado na China continental para gMG, refletindo o progresso regulatório da região no acesso a novos biológicos autoimunes. Além disso, HanAll Biopharma da Coreia do Sul está avançando seu próprio candidato inibidor FcRn, refletindo a crescente atividade de inovação regional nesta classe terapêutica.

Japão FcRn Inibidor do Mercado de Drogas

O mercado de medicamentos inibidores de FcRn no Japão está ganhando ímpeto devido à alta prevalência de doenças neuromusculares autoimunes do país, à infraestrutura de cuidados de neurologia bem desenvolvida e às progressivas aprovações regulatórias da MHLW para efgartigimod nas indicações de gMG, CIDP e PTI. Quadros nacionais de apoio às doenças raras no Japão e centros dedicados de doenças neuromusculares estão impulsionando a adoção crescente de inibidores de FcRn, com rozanolixizumabe também recebendo aprovação no Japão para gMG em pacientes positivos para MuSK.

China FcRn Inibidor do Mercado de Drogas

O mercado de drogas inibidora da FcRn da China representou a maior participação de receita de mercado na Ásia-Pacífico em 2025, atribuída à aprovação do país pela Vyvgart para a gMG, criando o maior mercado de inibidores da FcRn na região, a rápida expansão da infraestrutura especializada em neurologia e imunologia em grandes centros médicos acadêmicos chineses, e o crescente investimento do governo chinês no acesso a drogas raras através do processo de expansão da National Reembolsment Drug List.

FcRn Inibidor do Mercado de Drogas

A indústria dos inibidores de FcRn Drugs é liderada principalmente por empresas bem estabelecidas, incluindo:

- Johnson e Johnson (EUA)

- Immunovant Inc. (EUA)

- Viridian Therapeutics (EUA)

- Pfizer Inc. (EUA)

- Roche (Suíça)

- AstraZeneca (U.K.)

- Biogen Inc. (EUA)

- Novartis AG (Suíça)

- Sanofi (França)

- AbbVie (EUA)

- GSK plc (UK)

- Indústrias Farmacêuticas Teva (Israel)

- Grupo Zydus (Índia)

- Ciências Roivant (EUA)

- Momenta Pharmaceuticals/Johnson and Johnson (EUA)

- UCB Biosciences (EUA)

- Tecnologias Alpha Cancer (Canadá)

- HanAll Biopharma (Coreia do Sul)

Mais recentes desenvolvimentos no mercado global de inibidores de drogas FcRn

- Em março de 2022, argenx anunciou dados positivos de Fase 3 do estudo ADVANCE avaliando efgartigimod em adultos com trombocitopenia imune primária, demonstrando respostas estatisticamente significativas à contagem de plaquetas e estabelecendo a primeira evidência clínica de eficácia do inibidor de FcRn na PTI. Este resultado de estudo de referência ampliou substancialmente a população de pacientes com abordagem percebida para inibição da FcRn além da indicação inicial da gMG e marcou o início da estratégia de expansão da classe multiindicação.

- Em junho de 2023, o argenx obteve a aprovação do FDA para o VYVGART Hytrulo, a primeira formulação de inibidor de FcRn subcutâneo co-formulada com a tecnologia de liberação de fármacos ENHANZE de Halozyme, oferecendo uma dose fixa de 1.008 mg administrable através de uma única injeção subcutânea durante 30 a 90 segundos em ciclos semanais. Essa aprovação representou um marco comercial importante para a classe inibidora de FcRn, permitindo que a terapia domiciliar administrada pelo paciente melhorasse drasticamente a conveniência do tratamento e contribuísse para o rápido escalonamento das vendas de Vyvgart para US$ 1,2 bilhão em 2023 e US$ 2,2 bilhões em 2024

- Em junho de 2024, efgartigimod recebeu aprovação do FDA para polineuropatia desmielinizante inflamatória crônica, tornando-se o primeiro e único bloqueador FcRn aprovado para essa indicação. O estudo ADHERE, que foi o maior ensaio clínico randomizado e controlado já realizado em CIDP, demonstrou que efgartigimod reduziu significativamente as taxas de recidiva e melhorou os resultados funcionais, estabelecendo a inibição da FcRn como um novo padrão de tratamento para esta neuropatia autoimune crônica e abrindo uma nova via comercial substancial para a classe inibidora da FcRn.

- Em setembro de 2024, o Immunovant anunciou resultados positivos de seu ensaio de Fase IIa de batoclimab na Doença de Graves e recebeu a liberação do FDA IND para ensaios fundamentais de IMVT-1402, seu inibidor de FcRn de próxima geração, na Doença de Graves. Em Outubro de 2024, Johnson e Johnson anunciaram resultados positivos de Fase II/III para o nipocalimab em adolescentes com gMG e Janssen- Cilag submeteram o pedido de Autorização de Introdução no Mercado para o nipocalimab à EMA para o tratamento de gMG.

- Em abril de 2025, Johnson e Johnson receberam a aprovação do FDA para IMAAVY (nipocalimab-aahu), o primeiro anticorpo monoclonal anti-FcRn totalmente humano, para o tratamento de miastenia generalizada positiva para anticorpos em adultos e adolescentes com 12 anos de idade ou mais, que são AChR-positivos ou muSK-positivos. O estudo de Fase 3 de Vivacidade-MG3 demonstrou melhorias estatisticamente significativas nos escores de MG-ADL, estabelecendo o nipocalimab como o primeiro antagonista da FcRn que oferece controle sustentado da doença na população de gMG mais ampla e marca uma nova era competitiva para a classe inibidora da FcRn

- Em Março de 2026, o FDA aprovou uma nova via de administração da seringa pré-cheia para o efgartigimod (Vyvgart Hytrulo), permitindo que os doentes com gMG e CIDP realizassem auto-injecção após treino adequado com uma injecção subcutânea de 20 a 30 segundos. Esta aprovação aumentou ainda mais a independência do paciente no gerenciamento da terapia inibidora de FcRn e posicionou argenx competitivamente antes do lançamento do autoinjetor planejado em 2027, demonstrando o compromisso da empresa com a inovação contínua centrada no paciente em plataformas de entrega inibidor de FcRn

SKU-

Obtenha acesso online ao relatório sobre a primeira nuvem de inteligência de mercado do mundo

- Painel interativo de análise de dados

- Painel de análise da empresa para oportunidades de elevado potencial de crescimento

- Acesso de analista de pesquisa para personalização e customização. consultas

- Análise da concorrência com painel interativo

- Últimas notícias, atualizações e atualizações Análise de tendências

- Aproveite o poder da análise de benchmark para um rastreio abrangente da concorrência

Metodologia de Investigação

A recolha de dados e a análise do ano base são feitas através de módulos de recolha de dados com amostras grandes. A etapa inclui a obtenção de informações de mercado ou dados relacionados através de diversas fontes e estratégias. Inclui examinar e planear antecipadamente todos os dados adquiridos no passado. Da mesma forma, envolve o exame de inconsistências de informação observadas em diferentes fontes de informação. Os dados de mercado são analisados e estimados utilizando modelos estatísticos e coerentes de mercado. Além disso, a análise da quota de mercado e a análise das principais tendências são os principais fatores de sucesso no relatório de mercado. Para saber mais, solicite uma chamada de analista ou abra a sua consulta.

A principal metodologia de investigação utilizada pela equipa de investigação do DBMR é a triangulação de dados que envolve a mineração de dados, a análise do impacto das variáveis de dados no mercado e a validação primária (especialista do setor). Os modelos de dados incluem grelha de posicionamento de fornecedores, análise da linha de tempo do mercado, visão geral e guia de mercado, grelha de posicionamento da empresa, análise de patentes, análise de preços, análise da quota de mercado da empresa, normas de medição, análise global versus regional e de participação dos fornecedores. Para saber mais sobre a metodologia de investigação, faça uma consulta para falar com os nossos especialistas do setor.

Personalização disponível

A Data Bridge Market Research é líder em investigação formativa avançada. Orgulhamo-nos de servir os nossos clientes novos e existentes com dados e análises que correspondem e atendem aos seus objetivos. O relatório pode ser personalizado para incluir análise de tendências de preços de marcas-alvo, compreensão do mercado para países adicionais (solicite a lista de países), dados de resultados de ensaios clínicos, revisão de literatura, mercado remodelado e análise de base de produtos . A análise de mercado dos concorrentes-alvo pode ser analisada desde análises baseadas em tecnologia até estratégias de carteira de mercado. Podemos adicionar quantos concorrentes necessitar de dados no formato e estilo de dados que procura. A nossa equipa de analistas também pode fornecer dados em tabelas dinâmicas de ficheiros Excel em bruto (livro de factos) ou pode ajudá-lo a criar apresentações a partir dos conjuntos de dados disponíveis no relatório.