Global Graft Versus Host Disease Gvhd Treatment Market

Tamanho do mercado em biliões de dólares

CAGR :

%

USD

4.07 Billion

USD

5.81 Billion

2024

2032

USD

4.07 Billion

USD

5.81 Billion

2024

2032

| 2025 –2032 | |

| USD 4.07 Billion | |

| USD 5.81 Billion | |

| % | |

Global Graft-Versus-Host Disease (GvHD) Treatment Market, By Treatment (Medication and Therapy), Type (Chronic GvHD, Acute GvHD, and Prophylactic), Gender (Female and Male), Age (Adults and Pediatric), Method of Administration (Oral, Intravenous, Topical, and Others), End User (Hospitals, Transplant Centers, Institutes and Specialty Centers), Distribution Channel (Direct Tender, Retail Sales and Others - Industry Trends and Forecast to 2031.

Graft-Versus-Host Disease (GvHD) Treatment Market Analysis and Insights

According to an article published by National Institutes of Health in August 2023, as per the study conducted across 24 HCT centers in North America, Europe, and Asia investigated the natural progression of GvHD, the total incidence of acute GvHD requiring treatment was 40.9%, 35.2% for classic acute GvHD and 5.7% for late acute GvHD. Among patients with classic and late acute GvHD, 77.8% (1245 out of 1601) and 75.4% (193 out of 256), respectively, received systemic GvHD treatment. according to an article published by National Library of Medicine, acute graft-versus-host disease (GvHD) can develop in approximately half of patients undergoing hematopoietic stem cell transplantation (HCT) from a human leukocyte antigen (HLA)-matched sibling.

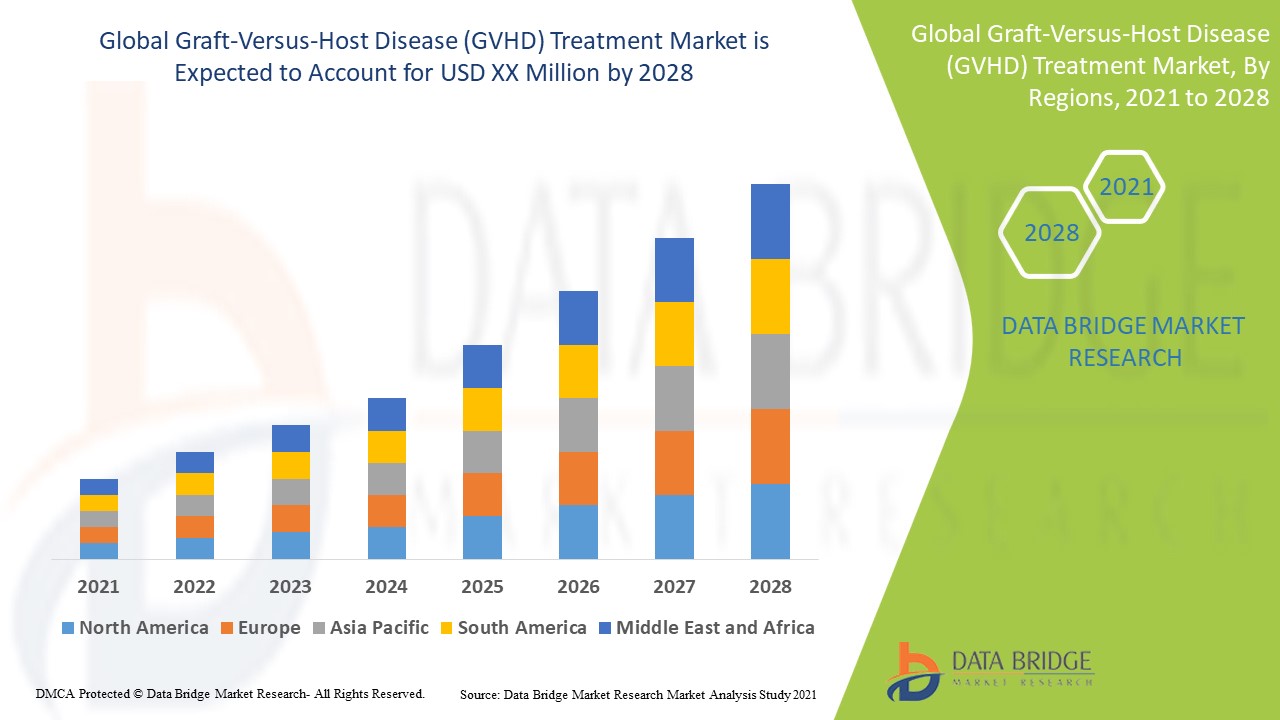

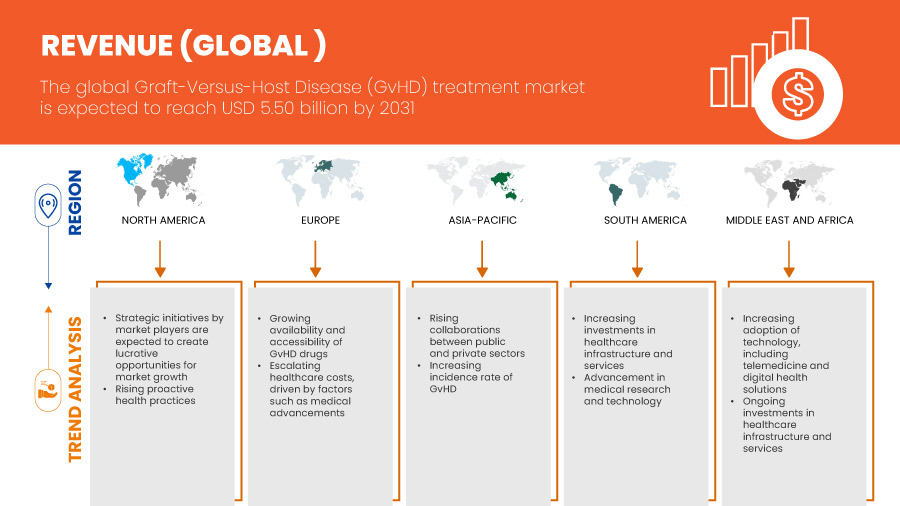

Data Bridge Market Research analyses that the global Graft-Versus-Host Disease (GvHD) treatment market is expected to reach USD 5.50 billion by 2031 from USD 3.94 billion in 2023, growing at a CAGR of 4.4% in in the forecast period of 2024 to 2031.

|

Report Metric |

Details |

|

Forecast Period |

2024 to 2031 |

|

Base Year |

2023 |

|

Historic Years |

2022 (Customizable to 2016–2021) |

|

Quantitative Units |

Revenue in USD Billion |

|

Segments Covered |

Treatment (Medication and Therapy), Type (Chronic GvHD, Acute GvHD, and Prophylactic), Gender (Female and Male), Age (Adults and Pediatric), Method of Administration (Oral, Intravenous, Topical, and Others), End User (Hospitals, Transplant Centers, Institutes and Specialty Centers), Distribution Channel (Direct Tender, Retail Sales and Others) |

|

Countries Covered |

U.S., Canada, Mexico, Germany, France, Italy, U.K., Spain, Belgium, Russia, Switzerland, Denmark, Rest of Europe, China, Japan, Australia, South Korea, India, Malaysia, Singapore, Philippines, Indonesia, Rest of Asia-Pacific, Brazil, Argentina, Rest of South America, South Africa, Saudi Arabia, U.A.E., Kuwait, Bahrain, and Rest of Middle East and Africa |

|

Market Players Covered |

Bristol-Myers Squibb Company, AbbVie Inc, Novartis AG, Janssen Global Services, LLC, MALLINCKRODT PLC, Incyte., Sanofi, Alkem Laboratories Ltd., and Astellas Pharma Inc., among others |

Market Definition

Graft-versus-host disease (GvHD) is a condition that can occur after a stem cell or bone marrow transplant in which the newly transplanted donor cells attack the transplant recipient's body. This immune response can cause a variety of symptoms and complications, ranging from mild to severe. GvHD is a significant concern in transplant medicine and requires careful management.

Graft-versus-host disease (GvHD) treatment refers to the various medical interventions used to manage and alleviate the symptoms of GvHD. These treatments aim to suppress the immune response of the donor cells against the recipient's tissues and organs. Common treatments for GvHD include immunosuppressive medications, such as corticosteroids, as well as other medications that target specific aspects of the immune response. In severe cases, more intensive therapies, such as photopheresis or other immune-modulating therapies, may be used. The choice of treatment depends on the severity of GvHD and other factors specific to the individual patient.

Global Graft-Versus-Host Disease (GvHD) Treatment Market Dynamics

This section deals with understanding the market drivers, opportunities, restraints, and challenges. All of this is discussed in detail below:

Driver

- Increasing Incidence of Hematopoietic Stem Cell Transplants (HSCT)

The increasing incidence of hematopoietic stem cell transplants (HSCT) is a significant driver for the demand for graft-versus-host disease (GvHD) treatment. This trend is primarily fueled by the growing prevalence of blood cancers, such as leukemia, lymphoma, and myeloma, which often require HSCT as a treatment option. Additionally, other hematological disorders, such as aplastic anemia and certain genetic disorders, also necessitate HSCT for disease management.

As the number of patients undergoing HSCT continues to rise, so does the demand for effective GvHD treatment. GvHD is a common complication of HSCT, occurring when the transplanted donor cells attack the recipient's tissues, leading to potentially severe and life-threatening symptoms. Therefore, the increasing incidence of HSCT directly translates to a higher need for GvHD treatment to manage and mitigate the effects of this complication.

Restraint

- High Cost of Medications and Supportive Care

The high cost of treating graft-versus-host disease (GvHD) presents a restraint that extends beyond the mere affordability of medications. It encompasses the expenses associated with comprehensive care, including medications, hospitalizations, outpatient visits, diagnostic tests, and supportive therapies. In developing regions with limited healthcare resources and financial constraints, these costs can be particularly burdensome, often leading to delayed or inadequate treatment.

Calcineurin inhibitors, such as tacrolimus and cyclosporine, are vital components of GvHD treatment, but their high prices can strain healthcare budgets. Antimetabolites like methotrexate and mycophenolate mofetil, immunosuppressive agents such as ruxolitinib, belumosudil, and ibrutinib, and corticosteroids including methylprednisolone and prednisolone are also essential but put excessive economic burden on patients.

Opportunity

- Market Expansion through Strategic Initiatives and Partnership

Market expansion through strategic collaboration can be a highly effective approach for companies operating in the GvHD (Graft-versus-Host Disease) treatment market. As the demand for innovative treatments and comprehensive care solutions for GvHD continues to rise, companies can capitalize on strategic partnerships and collaborations to expand their market presence and offer a diverse product portfolio tailored to meet evolving patient needs .By collaborating with research institutions, academic centers, and biotechnology companies, GvHD market players can access cutting-edge technologies, novel therapeutic approaches, and scientific expertise to advance their product development efforts. These collaborations enable companies to accelerate the discovery and development of promising GvHD therapies, including personalized cellular therapies, targeted biologic agents, and supportive care interventions. Moreover, strategic alliances with key opinion leaders and patient advocacy groups facilitate market access and enhance the adoption of new treatments by fostering trust, credibility, and patient engagement.

Furthermore, market expansion through strategic initiatives allows GvHD market players to diversify their product portfolio and capture a larger share of the GvHD market. By leveraging their expertise and resources to develop complementary products and services, companies can offer comprehensive care solutions that address the multifaceted needs of GvHD patients across different stages of the disease continuum.

Challenge

- Stringent Regulations in GvHD Therapies

Stringent regulation presents a significant challenge for the GvHD market in the future. As the field continues to advance with the development of novel therapies and treatment modalities, regulatory authorities impose rigorous standards for safety, efficacy, and quality control. Meeting these regulatory requirements demands substantial investment in preclinical and clinical development, as well as extensive documentation and data submission for regulatory approval. Additionally, the complexity of GvHD, its heterogeneous presentation, and the lack of standardized diagnostic criteria further complicate regulatory evaluation and approval processes. Regulatory agencies often require robust clinical trial data demonstrating not only the efficacy of novel therapies but also their comparative effectiveness against existing treatments. This necessitates large-scale, well-designed clinical trials with lengthy follow-up periods, leading to prolonged timelines and increased costs for product development.

Recent Developments

- In March 2024, Johnson & Johnson has announced the successful completion of its acquisition of Ambrx Biopharma, Inc. This clinical-stage biopharmaceutical company possesses a proprietary synthetic biology technology platform used for designing and developing next-generation antibody drug conjugates (ADCs). This acquisition offers Johnson & Johnson a unique opportunity to create, develop, and market targeted oncology therapies

- In February 2024, AbbVie Inc. and Tentarix Biotherapeutics have announced a partnership to collaboratively discover and develop conditionally-active, multi-specific biologics in the fields of oncology and immunology. This collaboration will leverage AbbVie's extensive experience in these areas alongside Tentarix's proprietary Tentacles™ platformIn April 2023, Medtronic and DaVita Inc. jointly launched Mozarc Medical, an independent company dedicated to transforming kidney health and advancing patient-centered technology solutions

- In February 2024, Novartis AG has agreed to acquire MorphoSys AG, a German biopharmaceutical company focused on innovative oncology medicines. This acquisition, subject to standard closing conditions and regulatory approvals, strengthens Novartis' oncology pipeline and expands its global presence in hematology

- In May 2022, Bristol-Myers Squibb Company announced the approval of Opdivo plus Yervoy as a first line treatment for adult patients for GvHD by Japan's Ministry of Health, Labour and Welfare. This may help the company to strengthen its product portfolio

- In January 2020, Astellas Pharma Inc. announced that it has entered into an agreement with Adaptimmune to develop stem cell derived allogenc CAR-T and TCR T-Cell Therapies to treat cancer. This will help the company to further acquire the market in coming years

Global Graft-Versus-Host Disease (GvHD) Treatment Market Scope

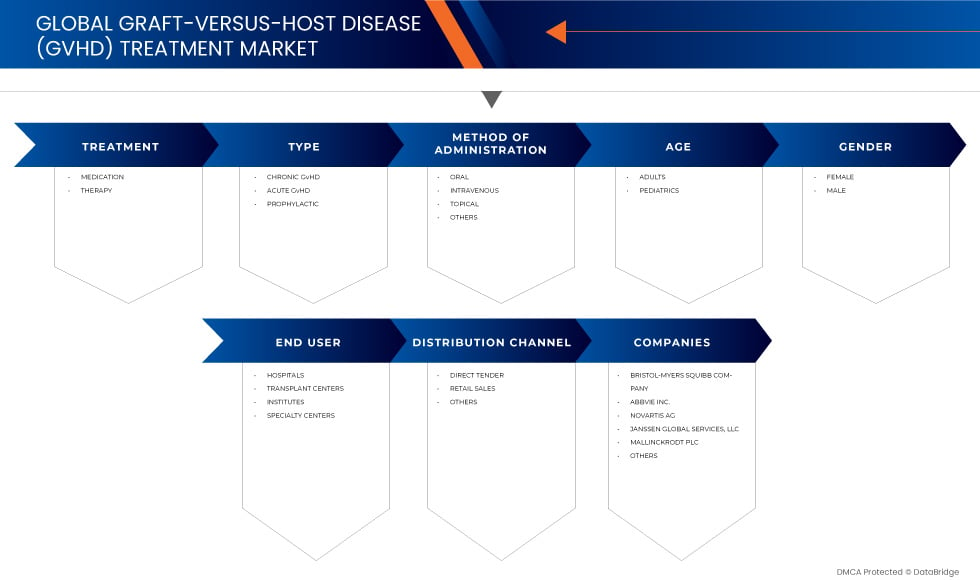

The global Graft-Versus-Host Disease (GvHD) treatment market is treatment market is segmented into seven notable segments based on treatment, type, gender, age, method of administration, end user, and distribution channel. The growth among segments helps you analyze niche pockets of growth and strategies to approach the market and determine your core application areas and the differences in your target markets.

Treatment

- Medication

- Therapy

On the basis of treatment, the market is segmented into medication and therapy.

Type

- Chronic GvHD

- Acute GvHD

- Prophylactic

On the basis of type, the market is segmented into chronic GvHD, acute GvHD, and prophylactic.

Gender

- Female

- Male

On the basis of gender, the market is segmented into female and male.

Age

- Adults

- Pediatric

On the basis of age, the market is segmented into adults and pediatric.

Method of Administration

- Oral

- Intravenous

- Topical

- Others

On the basis of method of administration, the market is segmented into oral, intravenous, topical, and others.

End User

- Hospitals

- Transplant Centers

- Institutes

- Specialty Centers

On the basis of end user, the market is segmented into hospitals, transplant centers, institutes, and specialty centers.

Distribution Channel

- Direct Tender

- Retail Sales

- Others

On the basis of distribution channel, the market is segmented into direct tender, retail sales and others.

Global Graft-Versus-Host Disease (GvHD) Treatment Market Regional Analysis/Insights

The global Graft-Versus-Host Disease (GvHD) treatment market is segmented into seven notable segments based on treatment, type, gender, age, method of administration, end user, and distribution channel.

The countries covered in this market report are U.S., Canada, Mexico, Germany, France, Italy, U.K., Spain, Belgium, Russia, Switzerland, Denmark, rest of Europe, China, Japan, Australia, South Korea, India, Malaysia, Singapore, Philippines, Indonesia, rest of Asia-Pacific, Brazil, Argentina, rest of South America, South Africa, Saudi Arabia, U.A.E., Kuwait, Bahrain, and rest of Middle East and Africa.

North America region is expected to dominate the market due to its advanced healthcare infrastructure, high rates of hematopoietic cell transplants, robust investment in research and development, supportive regulatory environment, significant healthcare spending, and greater disease awareness. These factors contribute to the region's leading position in the development and adoption of new GvHD treatments. U.S. is expected to dominate in North America due to Increasing incidence of hematopoietic stem cell transplants (HSCT). Japan is expected to dominate in the Asia-Pacific region advanced medical technology, significant investment in healthcare research and development, a high rate of hematopoietic cell transplants, strong governmental support and regulatory efficiency in approving new treatments, and increased public awareness and education about GvHD. Germany is expected to dominate in the Europe region due to its advanced technology adoption, robust healthcare infrastructure, and mature market.

The country section of the report also provides individual market-impacting factors and changes in regulation in the market domestically that impact the current and future trends of the market. Data points such as new sales, replacement sales, country demographics, regulatory acts, and import-export tariffs are some of the major pointers used to forecast the market scenario for individual countries. Also, the presence and availability of global brands and their challenges faced due to large or scarce competition from local and domestic brands and the impact of sales channels are considered while providing forecast analysis of the country data.

Competitive Landscape and Global Graft-Versus-Host Disease (GvHD) Treatment Market Share Analysis

The global Graft-Versus-Host Disease (GvHD) treatment market competitive landscape provides details of competitors. Details included are company overview, company financials, revenue generated, market potential, investment in R&D, new market initiatives, production sites and facilities, company strengths and weaknesses, product launch, product approvals, product width and breadth, application dominance, and product type lifeline curve. The above data points provided are only related to the company’s focus on the market.

Some of the major market players operating in the market are Bristol-Myers Squibb Company, AbbVie Inc, Novartis AG, Janssen Global Services, LLC, MALLINCKRODT PLC, Incyte., Sanofi, Alkem Laboratories Ltd., and Astellas Pharma Inc., among others.

SKU-

Obtenha acesso online ao relatório sobre a primeira nuvem de inteligência de mercado do mundo

- Painel interativo de análise de dados

- Painel de análise da empresa para oportunidades de elevado potencial de crescimento

- Acesso de analista de pesquisa para personalização e customização. consultas

- Análise da concorrência com painel interativo

- Últimas notícias, atualizações e atualizações Análise de tendências

- Aproveite o poder da análise de benchmark para um rastreio abrangente da concorrência

Metodologia de Investigação

A recolha de dados e a análise do ano base são feitas através de módulos de recolha de dados com amostras grandes. A etapa inclui a obtenção de informações de mercado ou dados relacionados através de diversas fontes e estratégias. Inclui examinar e planear antecipadamente todos os dados adquiridos no passado. Da mesma forma, envolve o exame de inconsistências de informação observadas em diferentes fontes de informação. Os dados de mercado são analisados e estimados utilizando modelos estatísticos e coerentes de mercado. Além disso, a análise da quota de mercado e a análise das principais tendências são os principais fatores de sucesso no relatório de mercado. Para saber mais, solicite uma chamada de analista ou abra a sua consulta.

A principal metodologia de investigação utilizada pela equipa de investigação do DBMR é a triangulação de dados que envolve a mineração de dados, a análise do impacto das variáveis de dados no mercado e a validação primária (especialista do setor). Os modelos de dados incluem grelha de posicionamento de fornecedores, análise da linha de tempo do mercado, visão geral e guia de mercado, grelha de posicionamento da empresa, análise de patentes, análise de preços, análise da quota de mercado da empresa, normas de medição, análise global versus regional e de participação dos fornecedores. Para saber mais sobre a metodologia de investigação, faça uma consulta para falar com os nossos especialistas do setor.

Personalização disponível

A Data Bridge Market Research é líder em investigação formativa avançada. Orgulhamo-nos de servir os nossos clientes novos e existentes com dados e análises que correspondem e atendem aos seus objetivos. O relatório pode ser personalizado para incluir análise de tendências de preços de marcas-alvo, compreensão do mercado para países adicionais (solicite a lista de países), dados de resultados de ensaios clínicos, revisão de literatura, mercado remodelado e análise de base de produtos . A análise de mercado dos concorrentes-alvo pode ser analisada desde análises baseadas em tecnologia até estratégias de carteira de mercado. Podemos adicionar quantos concorrentes necessitar de dados no formato e estilo de dados que procura. A nossa equipa de analistas também pode fornecer dados em tabelas dinâmicas de ficheiros Excel em bruto (livro de factos) ou pode ajudá-lo a criar apresentações a partir dos conjuntos de dados disponíveis no relatório.