Global Missile And Air Defense Radar System Market

Tamanho do mercado em biliões de dólares

CAGR :

%

USD

13.67 Billion

USD

31.97 Billion

2025

2033

USD

13.67 Billion

USD

31.97 Billion

2025

2033

| 2026 –2033 | |

| USD 13.67 Billion | |

| USD 31.97 Billion | |

| % | |

|

Global Missile and Air Defense Radar System Market Segmentation, By Type (Missile Defense System, Anti-Aircraft System, Counter Rocket, Artillery, and Mortar (C-RAM) System), Platform (Airborne, Land, and Naval), Range (Short Range Air Defense (ShoRAD) System, Medium Range Air Defense (MRAD) System, and Long Range Air Defense (LRAD) System), Component (Weapon System, Fire Control System, Fire Control Radar, Surveillance Radar, Command and Control System, and Others) - Industry Trends and Forecast to 2033

Missile and Air Defense Radar System Market Size

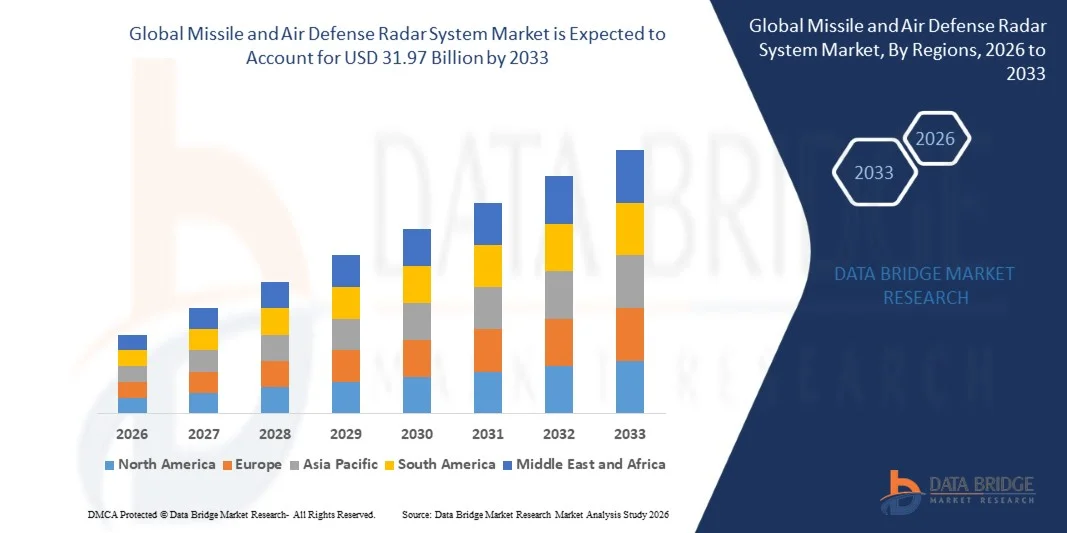

- The global missile and air defense radar system market size was valued at USD 13.67 billion in 2025 and is expected to reach USD 31.97 billion by 2033, at a CAGR of 11.20% during the forecast period

- The market growth is largely fueled by rising geopolitical tensions and increasing investments by governments in strengthening national air defense and missile detection capabilities

- Furthermore, the growing deployment of integrated air and missile defense networks, along with advancements in radar technologies such as active electronically scanned array (AESA) and digital radar architecture, is significantly enhancing threat detection and tracking capabilities. These factors are accelerating the adoption of advanced radar systems, thereby contributing to the expansion of the missile and air defense radar system market

Missile and Air Defense Radar System Market Analysis

- Missile and air defense radar systems, designed to detect, track, and guide interception of aerial threats such as ballistic missiles, aircraft, and unmanned aerial vehicles, have become critical components of modern defense infrastructure across land, naval, and airborne platforms due to their role in early warning and situational awareness

- The increasing demand for these systems is primarily driven by growing defense modernization programs, rising cross-border security threats, and the need for advanced surveillance technologies capable of monitoring large airspaces and supporting integrated missile defense operations

- North America dominated the missile and air defense radar system market with a share of 32.59% in 2025, due to substantial defense spending, continuous modernization of military infrastructure, and strong investments in advanced radar technologies for missile detection and tracking

- Asia-Pacific is expected to be the fastest growing region in the missile and air defense radar system market during the forecast period due to rising defense expenditures and increasing security concerns across the region

- Missile defense system segment dominated the market with a market share of 46.8% in 2025, due to the rising global emphasis on protection against ballistic and cruise missile threats. Governments across major defense economies are prioritizing missile interception capabilities as part of integrated air and missile defense architectures. These systems rely heavily on advanced radar technologies for early warning, tracking, and guidance of interceptors

Report Scope and Missile and Air Defense Radar System Market Segmentation

|

Attributes |

Missile and Air Defense Radar System Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Missile and Air Defense Radar System Market Trends

“Growing Adoption of AESA Radar Technology”

- A major trend in the missile and air defense radar system market is the growing adoption of active electronically scanned array (AESA) radar technologies, driven by the need for higher detection accuracy, faster target tracking, and improved resistance to electronic warfare environments. AESA radars enable simultaneous tracking of multiple aerial threats and provide enhanced situational awareness for modern air defense networks

- For instance, Raytheon Technologies developed the Lower Tier Air and Missile Defense Sensor (LTAMDS) for the United States Army, featuring a 360-degree active electronically scanned array design that significantly improves threat detection and tracking capabilities against advanced missile threats

- The integration of AESA radar systems into modern air defense platforms is expanding as defense forces require improved tracking of low-observable targets such as stealth aircraft, drones, and cruise missiles. These radars provide enhanced beam steering, higher resolution tracking, and rapid target discrimination during complex combat scenarios

- Naval defense platforms are also incorporating AESA radar technologies to strengthen maritime surveillance and missile interception capabilities. Warships equipped with advanced phased-array radar systems can monitor extensive airspace and respond quickly to emerging aerial threats in strategic maritime regions

- Airborne surveillance systems are increasingly deploying AESA radars to support early warning and control operations. These radars enable extended detection range and improved monitoring of high-speed aerial targets across wide operational zones

- The rising reliance on multi-mission radar systems capable of handling surveillance, tracking, and fire control tasks is reinforcing the demand for AESA technology. This transition toward electronically scanned radar architectures is strengthening overall detection efficiency and advancing the modernization of global missile and air defense infrastructures

Missile and Air Defense Radar System Market Dynamics

Driver

“Rising Defense Spending and Air Defense Modernization”

- Increasing defense budgets and large-scale military modernization programs across several countries are significantly driving the demand for advanced missile and air defense radar systems. Governments are prioritizing investments in surveillance and early warning technologies to strengthen national security and counter evolving aerial threats

- For instance, Lockheed Martin delivered the TPY-4 radar to the United States Air Force, a next-generation radar system designed to enhance long-range air surveillance and threat detection capabilities in complex operational environments

- Many defense agencies are deploying advanced radar networks capable of monitoring large airspaces and detecting ballistic missiles, aircraft, and unmanned aerial systems. These technologies play a critical role in early warning and interception strategies that protect national borders and strategic assets

- The modernization of integrated air and missile defense architectures is encouraging the procurement of sophisticated radar platforms across land, naval, and airborne systems. Governments are prioritizing radar upgrades to strengthen multi-layered defense frameworks that support rapid response against incoming threats

- Continuous technological advancements in digital radar processing, sensor fusion, and long-range detection capabilities are further supporting defense modernization initiatives. These developments are driving sustained demand for advanced radar systems across global military infrastructures

Restraint/Challenge

“High Cost of Advanced Radar Systems”

- The missile and air defense radar system market faces challenges due to the high cost associated with the development, deployment, and maintenance of advanced radar platforms. These systems require sophisticated electronic components, high-power transmitters, and complex software architectures that significantly increase production and operational costs

- For instance, Thales Group produces advanced radar platforms such as the Ground Master 200 radar, which incorporate advanced phased-array technology and high-performance sensors that demand significant investment in engineering and manufacturing

- Developing high-precision radar systems involves extensive research and development efforts, specialized testing environments, and complex integration with missile defense networks. These processes require advanced expertise and prolonged development cycles, which elevate overall project costs

- The deployment of radar systems across large geographic areas also involves infrastructure investments, maintenance facilities, and skilled technical personnel to ensure operational reliability. These additional requirements can create financial constraints for countries with limited defense budgets

- The need to maintain high performance and reliability under challenging battlefield conditions further adds to operational expenses. These cost pressures can limit widespread adoption of advanced radar systems in certain regions, posing a challenge to market expansion while maintaining technological advancement

Missile and Air Defense Radar System Market Scope

The market is segmented on the basis of type, platform, range, and component.

• By Type

On the basis of type, the Missile and Air Defense Radar System market is segmented into missile defense system, anti-aircraft system, and counter rocket, artillery, and mortar (C-RAM) system. The missile defense system segment dominated the market with the largest revenue share of 46.8% in 2025, driven by the rising global emphasis on protection against ballistic and cruise missile threats. Governments across major defense economies are prioritizing missile interception capabilities as part of integrated air and missile defense architectures. These systems rely heavily on advanced radar technologies for early warning, tracking, and guidance of interceptors. Increasing investments in layered missile defense networks and modernization of national defense infrastructures continue to strengthen demand for missile defense radar systems. The growing deployment of multi-layered defense shields to safeguard strategic assets, military bases, and urban centers further reinforces the leadership of this segment.

The counter rocket, artillery, and mortar (C-RAM) system segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing asymmetric warfare and cross-border security threats. Military forces are increasingly deploying C-RAM solutions to detect and intercept short-range projectiles and rocket attacks in real time. These systems depend on highly responsive radar platforms capable of rapidly identifying incoming threats and directing countermeasures. Rising conflicts in urban and border regions are accelerating the adoption of such systems to protect forward operating bases and civilian infrastructure. In addition, continuous advancements in radar tracking accuracy and automated response capabilities are enhancing the operational effectiveness of C-RAM systems, supporting strong segment growth.

• By Platform

On the basis of platform, the Missile and Air Defense Radar System market is segmented into airborne, land, and naval. The land segment dominated the market with the largest market revenue share in 2025, supported by the widespread deployment of ground-based radar systems for national air defense networks. Land-based radar installations play a critical role in early warning, threat detection, and missile tracking across national borders. Governments are investing heavily in fixed and mobile radar units to strengthen homeland security and battlefield awareness. These systems provide long-range surveillance capabilities and support integrated command and control networks. Increasing modernization of ground-based missile defense infrastructure and deployment of mobile radar units in strategic locations continue to sustain the dominance of this segment.

The airborne segment is expected to witness the fastest growth rate from 2026 to 2033 due to the growing demand for airborne early warning and control (AEW&C) platforms. Airborne radar systems provide extended detection range and enhanced situational awareness by operating at higher altitudes. Defense forces increasingly rely on airborne platforms to detect stealth aircraft, missiles, and drones beyond ground radar coverage. Integration of advanced phased-array radars and sensor fusion technologies is further improving the performance of airborne surveillance systems. Rising investments in next-generation surveillance aircraft and unmanned aerial platforms are expected to significantly accelerate the growth of this segment.

• By Range

On the basis of range, the Missile and Air Defense Radar System market is segmented into short range air defense (ShoRAD) system, medium range air defense (MRAD) system, and long range air defense (LRAD) system. The long range air defense (LRAD) system segment dominated the market with the largest revenue share in 2025, driven by the increasing need to detect and intercept high-altitude and long-distance threats. LRAD radar systems provide early detection of ballistic missiles, aircraft, and long-range projectiles, enabling defense forces to initiate timely interception strategies. These systems are often integrated with advanced missile defense frameworks to create multi-layered protection for national territories. Governments are prioritizing long-range radar installations to monitor vast airspaces and strategic defense zones. Continuous technological advancements in long-range radar tracking and target discrimination further support the segment’s dominance.

The short range air defense (ShoRAD) system segment is projected to witness the fastest growth rate from 2026 to 2033, driven by increasing threats from low-flying drones, helicopters, and tactical missiles. Modern battlefields require rapid response systems capable of detecting and neutralizing threats within short distances. ShoRAD radar systems offer quick detection and tracking capabilities that support mobile defense units and frontline operations. Increasing deployment of mobile air defense platforms and tactical radar systems is boosting the demand for short-range solutions. In addition, the growing use of unmanned aerial vehicles in warfare is encouraging defense forces to strengthen short-range detection capabilities.

• By Component

On the basis of component, the Missile and Air Defense Radar System market is segmented into weapon system, fire control system, fire control radar, surveillance radar, command and control system, and others. The surveillance radar segment dominated the market with the largest revenue share in 2025 due to its critical role in continuous monitoring and early detection of aerial threats. Surveillance radars enable defense forces to track aircraft, missiles, and unmanned aerial systems across large geographical areas. These systems form the backbone of integrated air defense networks by providing real-time situational awareness to command centers. Increasing deployment of advanced 3D and phased-array radar technologies is enhancing the detection range and accuracy of surveillance radars. Growing emphasis on strengthening national airspace monitoring capabilities further reinforces the dominance of this segment.

The fire control radar segment is anticipated to witness the fastest growth rate from 2026 to 2033 as modern defense systems require highly precise targeting and interception capabilities. Fire control radars are responsible for guiding missiles and weapon systems toward identified threats with high accuracy. The increasing development of advanced interceptor missiles and automated targeting systems is driving demand for sophisticated fire control radars. These systems enable faster engagement of multiple threats simultaneously in complex combat environments. Continuous innovations in radar tracking algorithms, electronic warfare resistance, and real-time targeting capabilities are expected to accelerate the growth of this segment.

Missile and Air Defense Radar System Market Regional Analysis

- North America dominated the missile and air defense radar system market with the largest revenue share of 32.59% in 2025, driven by substantial defense spending, continuous modernization of military infrastructure, and strong investments in advanced radar technologies for missile detection and tracking

- Defense agencies in the region prioritize the deployment of integrated air and missile defense networks capable of detecting ballistic missiles, cruise missiles, and advanced aerial threats. The presence of major defense contractors and extensive research and development activities further strengthens the regional market

- Growing focus on national security, expansion of next-generation radar systems, and increasing deployment of layered missile defense architectures across military bases and strategic locations continue to reinforce North America's leadership in the global market

U.S. Missile and Air Defense Radar System Market Insight

The U.S. missile and air defense radar system market captured the largest revenue share in 2025 within North America, fueled by extensive investments in national missile defense programs and advanced surveillance technologies. The country is continuously upgrading its radar infrastructure to strengthen early warning and threat detection capabilities. The presence of leading defense technology companies and ongoing development of next-generation radar platforms further accelerates market growth. In addition, the integration of radar systems with advanced interceptor missiles and command networks plays a critical role in expanding the missile and air defense ecosystem across the country.

Europe Missile and Air Defense Radar System Market Insight

The Europe missile and air defense radar system market is projected to expand at a considerable CAGR during the forecast period, primarily driven by increasing geopolitical tensions and the rising need for advanced air defense capabilities. Several European nations are strengthening their defense frameworks through modernization programs and investments in radar surveillance infrastructure. The region is witnessing increased adoption of integrated radar systems for monitoring airspace and protecting critical infrastructure. Growing collaborations among defense organizations and technology providers are further supporting the expansion of radar-based air defense solutions across Europe.

U.K. Missile and Air Defense Radar System Market Insight

The U.K. missile and air defense radar system market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising investments in defense modernization and advanced surveillance technologies. The country is focusing on strengthening its airspace monitoring capabilities and improving response mechanisms against emerging aerial threats. Continuous upgrades in radar installations and integration with missile defense systems are supporting the adoption of advanced radar platforms. The U.K.’s strong defense research ecosystem and strategic partnerships with global defense companies are expected to further stimulate market growth.

Germany Missile and Air Defense Radar System Market Insight

The Germany missile and air defense radar system market is expected to expand at a significant CAGR during the forecast period, supported by increasing defense budgets and modernization of military surveillance infrastructure. Germany is focusing on strengthening integrated air defense capabilities to monitor and respond to evolving aerial threats. The adoption of advanced radar technologies is growing across military installations and defense networks. The country’s emphasis on technological innovation and collaboration with European defense initiatives is further accelerating the development and deployment of modern radar systems.

Asia-Pacific Missile and Air Defense Radar System Market Insight

The Asia-Pacific missile and air defense radar system market is expected to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by rising defense expenditures and increasing security concerns across the region. Countries are rapidly modernizing their military infrastructure to strengthen early warning and threat detection capabilities. The expansion of missile defense programs and the development of indigenous radar technologies are contributing significantly to market growth. In addition, the increasing focus on protecting national airspace and strategic assets is encouraging the deployment of advanced radar surveillance systems across the region.

Japan Missile and Air Defense Radar System Market Insight

The Japan missile and air defense radar system market is gaining strong momentum due to the country’s growing emphasis on strengthening national defense and missile interception capabilities. Japan continues to invest in advanced radar technologies to improve detection of ballistic missile threats and enhance situational awareness. The deployment of modern radar platforms across air defense networks is increasing as the country strengthens its security infrastructure. Integration of radar systems with missile defense frameworks and advanced surveillance platforms is playing a crucial role in supporting market expansion.

China Missile and Air Defense Radar System Market Insight

The China missile and air defense radar system market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to significant investments in defense modernization and indigenous radar technology development. China is expanding its radar surveillance networks to strengthen air defense capabilities and monitor large airspace regions. The country’s focus on developing advanced phased-array radar systems and integrated missile defense platforms is accelerating the adoption of radar technologies. Continuous advancements in military electronics and growing investments in next-generation defense systems are further propelling the market in China.

Missile and Air Defense Radar System Market Share

The missile and air defense radar system industry is primarily led by well-established companies, including:

- BAE Systems plc (U.K.)

- Leonardo S.p.A. (Italy)

- Saab AB (Sweden)

- Israel Aerospace Industries Ltd. (Israel)

- Lockheed Martin Corporation (U.S.)

- Rheinmetall AG (Germany)

- Thales Group (France)

- Raytheon Technologies Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- ASELSAN A.S. (Turkey)

- Reutech Radar Systems (South Africa)

Latest Developments in Global Missile and Air Defense Radar System Market

- In September 2025, Northrop Grumman entered into a strategic collaboration with several Taiwanese industry partners to support the supply and deployment of the AN/TPS-78 Advanced Capabilities Radar in Taiwan. Through memoranda of understanding with local firms, the company aimed to facilitate system delivery, integration, and long-term maintenance while strengthening Taiwan’s domestic defense industry participation. The radar operates in the S-band frequency and is designed to detect both high- and low-altitude targets in complex environments, making it suitable for modern air surveillance operations. This collaboration reflects the growing demand for mobile long-range radar platforms and highlights the importance of international defense partnerships in expanding radar system deployment across strategic regions

- In April 2025, Lockheed Martin delivered the first TPY‑4 radar to the United States Air Force, marking a major milestone in the modernization of next-generation air surveillance capabilities. The software-defined radar completed initial phase testing before its official handover and demonstrated the ability to detect smaller and more challenging targets in contested radio-frequency environments. Designed for both fixed and mobile deployment, the system incorporates a fully digital architecture that enhances flexibility and operational performance. This advancement strengthens early warning infrastructure and signals a broader shift toward advanced digital radar technologies within modern air defense networks

- In November 2024, Raytheon successfully conducted a live-fire test of its Lower Tier Air and Missile Defense Sensor (LTAMDS) at the White Sands Missile Range. During the exercise, the radar detected and tracked a tactical ballistic missile surrogate and guided a PAC‑3 Missile Segment Enhancement interceptor to intercept the target successfully. The demonstration validated the radar’s capability to operate within the Integrated Battle Command System, highlighting its role in addressing complex and high-speed missile threats. This milestone accelerated the program’s progress toward operational deployment and reinforced industry momentum toward integrated radar and missile defense solutions

- In April 2024, Thales Group secured a follow-on contract to supply seven Ground Master 200 Multi‑Mission Compact radar units to the Royal Netherlands Army through the Dutch procurement agency COMMIT. The agreement also included an option for two additional systems and expanded an existing defense partnership established through earlier radar acquisitions. Equipped with advanced 4D Active Electronically Scanned Array technology, the system can detect and track drones, aircraft, and missile threats simultaneously. This development strengthened Europe’s air surveillance infrastructure and highlighted the increasing adoption of highly mobile radar platforms capable of rapid deployment and multi-threat detection

- In February 2024, Saab AB announced the delivery of additional Giraffe 4A radar systems to several international defense customers to enhance short- and medium-range air defense capabilities. The radar employs active electronically scanned array technology and offers advanced target detection and tracking against drones, missiles, and aircraft within complex operational environments. Its modular architecture enables integration with multiple missile defense platforms and command systems. This development reflects the increasing global demand for versatile radar solutions capable of supporting multi-layered air defense strategies and addressing emerging aerial threats

SKU-

Obtenha acesso online ao relatório sobre a primeira nuvem de inteligência de mercado do mundo

- Painel interativo de análise de dados

- Painel de análise da empresa para oportunidades de elevado potencial de crescimento

- Acesso de analista de pesquisa para personalização e customização. consultas

- Análise da concorrência com painel interativo

- Últimas notícias, atualizações e atualizações Análise de tendências

- Aproveite o poder da análise de benchmark para um rastreio abrangente da concorrência

Metodologia de Investigação

A recolha de dados e a análise do ano base são feitas através de módulos de recolha de dados com amostras grandes. A etapa inclui a obtenção de informações de mercado ou dados relacionados através de diversas fontes e estratégias. Inclui examinar e planear antecipadamente todos os dados adquiridos no passado. Da mesma forma, envolve o exame de inconsistências de informação observadas em diferentes fontes de informação. Os dados de mercado são analisados e estimados utilizando modelos estatísticos e coerentes de mercado. Além disso, a análise da quota de mercado e a análise das principais tendências são os principais fatores de sucesso no relatório de mercado. Para saber mais, solicite uma chamada de analista ou abra a sua consulta.

A principal metodologia de investigação utilizada pela equipa de investigação do DBMR é a triangulação de dados que envolve a mineração de dados, a análise do impacto das variáveis de dados no mercado e a validação primária (especialista do setor). Os modelos de dados incluem grelha de posicionamento de fornecedores, análise da linha de tempo do mercado, visão geral e guia de mercado, grelha de posicionamento da empresa, análise de patentes, análise de preços, análise da quota de mercado da empresa, normas de medição, análise global versus regional e de participação dos fornecedores. Para saber mais sobre a metodologia de investigação, faça uma consulta para falar com os nossos especialistas do setor.

Personalização disponível

A Data Bridge Market Research é líder em investigação formativa avançada. Orgulhamo-nos de servir os nossos clientes novos e existentes com dados e análises que correspondem e atendem aos seus objetivos. O relatório pode ser personalizado para incluir análise de tendências de preços de marcas-alvo, compreensão do mercado para países adicionais (solicite a lista de países), dados de resultados de ensaios clínicos, revisão de literatura, mercado remodelado e análise de base de produtos . A análise de mercado dos concorrentes-alvo pode ser analisada desde análises baseadas em tecnologia até estratégias de carteira de mercado. Podemos adicionar quantos concorrentes necessitar de dados no formato e estilo de dados que procura. A nossa equipa de analistas também pode fornecer dados em tabelas dinâmicas de ficheiros Excel em bruto (livro de factos) ou pode ajudá-lo a criar apresentações a partir dos conjuntos de dados disponíveis no relatório.