Asia Pacific Heat Shrink Tubing For Automotive Market

市场规模(十亿美元)

CAGR :

%

USD

221.52 Million

USD

383.47 Million

2025

2033

USD

221.52 Million

USD

383.47 Million

2025

2033

| 2026 –2033 | |

| USD 221.52 Million | |

| USD 383.47 Million | |

| % | |

|

Asia-Pacific Heat Shrink Tubing for Automotive Market Segmentation, By Application (Hoses, Connectors, Ring Terminals, In-Line Splices, Brake Pipes, Diesel Injection Clusters, Under Bonnet Cable Protection, Gas Pipes, and Miniature Splices), Material (Polyolefin, Polyvinyl Chloride, Polytetrafluoroethylene, Fluorinated Ethylene Propylene, Perfluoroalkoxy Alkane, Ethylene Tetrafluoroethylene, and Others), Color (Red, Yellow, and Others), Type (Single Wall Shrink Tubing and Dual Wall Shrink Tubing), Voltage (Low, Medium, and High), Fuel Type (Petrol, Diesel/CNG, and Electric), Sales Channel (OEM and Aftermarket), Vehicle Type (Passenger Cars, LCV, HCV, and Electric Vehicles) - Industry Trends and Forecast to 2033

Asia-Pacific Heat Shrink Tubing for Automotive Market Size

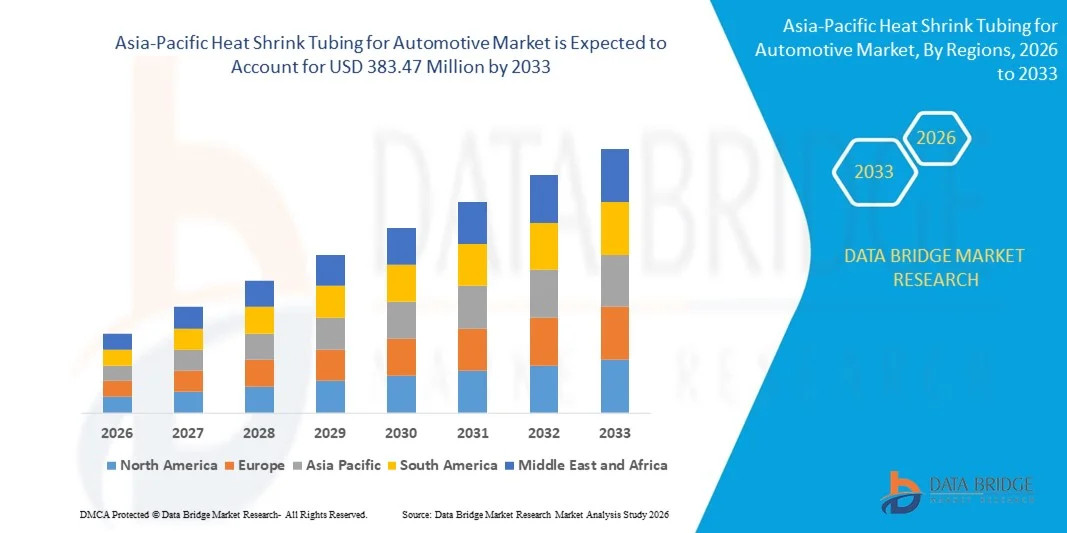

- The Asia-Pacific heat shrink tubing for automotive market size was valued at USD 221.52 million in 2025 and is expected to reach USD 383.47 million by 2033, at a CAGR of 7.1% during the forecast period

- The market growth is largely fueled by the rising integration of advanced electrical and electronic systems in modern vehicles, which significantly increases the need for reliable insulation and protection solutions for wiring harnesses and connectors

- Furthermore, the rapid expansion of electric vehicles and the growing complexity of automotive electrical architectures are increasing the demand for durable heat shrink tubing that can provide thermal resistance, electrical insulation, and environmental protection. These factors are strengthening the adoption of advanced cable protection materials across the automotive industry, thereby supporting market expansion

Asia-Pacific Heat Shrink Tubing for Automotive Market Analysis

- Heat shrink tubing used in automotive applications serves as an essential insulation and protection solution for electrical wiring, connectors, and cable assemblies, helping safeguard components from heat, vibration, chemicals, and moisture commonly present in vehicle operating environments

- The increasing demand for heat shrink tubing is primarily driven by the growth of automotive electronics, rising production of electric and hybrid vehicles, and the need for reliable protection of high-voltage wiring systems and sensitive electronic components in modern vehicles

- China dominated the heat shrink tubing for automotive market in 2025, due to its extensive automotive manufacturing ecosystem, large-scale production of wiring harnesses, and strong presence of electronics component suppliers serving both domestic and export markets

- India is expected to be the fastest growing country in the heat shrink tubing for automotive market during the forecast period due to expanding automobile production and rapid growth of the domestic automotive component industry

- Polyolefin segment dominated the market with a market share of 35.3% in 2025, due to its excellent balance of flexibility, durability, and electrical insulation properties. Polyolefin heat shrink tubing is widely preferred in automotive applications due to its resistance to moisture, chemicals, and mechanical stress, which helps maintain stable performance in demanding environments. The material also provides effective insulation for wiring harnesses and electrical connections while maintaining ease of installation

Report Scope and Heat Shrink Tubing for Automotive Market Segmentation

|

Attributes |

Heat Shrink Tubing for Automotive Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Asia-Pacific Heat Shrink Tubing for Automotive Market Trends

Growing Adoption of High-Performance and Heat-Resistant Tubing Materials

- A significant trend in the heat shrink tubing for automotive market is the growing adoption of high-performance and heat-resistant tubing materials that provide reliable insulation and protection for electrical wiring systems. These advanced materials help automotive manufacturers maintain safety, durability, and performance in increasingly complex vehicle electrical architectures

- For instance, TE Connectivity manufactures automotive heat shrink tubing products designed to withstand high temperatures and harsh operating environments in vehicle wiring systems. These tubing solutions improve electrical insulation, protect components from mechanical stress, and enhance the durability of critical automotive circuits

- Automotive manufacturers are increasingly integrating advanced heat shrink tubing materials that offer superior resistance to chemicals, moisture, vibration, and extreme temperatures. These characteristics are essential for ensuring the long-term performance of wiring systems installed in demanding automotive environments

- The expansion of electric vehicles and hybrid powertrains is further accelerating the demand for high-performance heat shrink tubing capable of protecting high-voltage cables and battery connections. These applications require tubing materials that maintain insulation integrity under high thermal and electrical loads

- Automotive suppliers are focusing on developing lightweight yet durable tubing materials that support vehicle weight reduction initiatives while maintaining strong insulation performance. This trend is strengthening the development of advanced polymer and fluoropolymer-based heat shrink tubing solutions for next-generation vehicles

- The growing complexity of automotive electronics and electrical connectivity systems is reinforcing the need for durable and high-temperature-resistant tubing materials. This expanding reliance on reliable insulation technologies is strengthening the adoption of advanced heat shrink tubing solutions across global automotive manufacturing

Asia-Pacific Heat Shrink Tubing for Automotive Market Dynamics

Driver

Rising Integration of Advanced Electrical Systems in Vehicles

- The increasing integration of advanced electrical systems in modern vehicles is a major driver for the heat shrink tubing for automotive market as vehicles incorporate a growing number of electronic modules and wiring networks. These systems require durable insulation and protection to ensure safe operation under varying mechanical and thermal conditions

- For instance, Sumitomo Electric Industries supplies automotive wiring harness components and insulation solutions that support complex vehicle electrical systems. Heat shrink tubing used in these harnesses protects wires from abrasion, environmental exposure, and electrical interference within vehicle architectures

- The rapid growth of electronic control units, infotainment systems, sensors, and safety technologies is significantly expanding the volume of wiring installed in modern vehicles. This increasing electrical complexity requires reliable insulation materials that ensure stable performance and minimize the risk of electrical failures

- Automotive manufacturers are investing heavily in electrification technologies, which further increases the demand for heat shrink tubing capable of insulating high-voltage cables and battery wiring assemblies. These applications require tubing solutions that provide strong dielectric strength and thermal resistance

- The continuous expansion of electronic components in vehicles is reinforcing the importance of protective insulation solutions within automotive wiring systems. This increasing electrical integration is therefore strengthening the demand for heat shrink tubing across the global automotive industry

Restraint/Challenge

Fluctuating Prices of Polymer and Fluoropolymer Raw Materials

- The heat shrink tubing for automotive market faces challenges due to fluctuating prices of polymer and fluoropolymer raw materials that are essential for manufacturing high-performance tubing products. Variations in raw material costs create uncertainty for manufacturers and influence overall production expenses

- For instance, DuPont produces fluoropolymer materials used in high-performance heat shrink tubing for demanding automotive applications. Changes in the pricing and supply availability of such specialized materials can significantly affect manufacturing costs and product pricing across the supply chain

- Heat shrink tubing production relies on polymers such as polyolefin and fluoropolymers that must meet strict performance and durability standards for automotive environments. Price volatility in these materials can disrupt cost planning and reduce profit margins for manufacturers

- Supply chain disruptions in petrochemical feedstocks and specialty polymers further contribute to cost instability across the heat shrink tubing manufacturing sector. These fluctuations create challenges for companies attempting to maintain competitive pricing while ensuring product quality

- The ongoing variability in polymer and fluoropolymer prices continues to influence manufacturing economics within the market. This challenge requires industry participants to optimize sourcing strategies and production efficiency while maintaining the high-performance standards required for automotive applications

Asia-Pacific Heat Shrink Tubing for Automotive Market Scope

The market is segmented on the basis of application, material, color, type, voltage, fuel type, sales channel, and vehicle type.

- By Application

On the basis of application, the heat shrink tubing for automotive market is segmented into hoses, connectors, ring terminals, in-line splices, brake pipes, diesel injection clusters, under bonnet cable protection, gas pipes, and miniature splices. The connectors segment dominated the market with the largest market revenue share in 2025, driven by the extensive use of electrical connectors in modern vehicles for power distribution and signal transmission. Automotive heat shrink tubing is widely applied on connectors to provide insulation, mechanical protection, and environmental sealing against moisture, chemicals, and vibration. The growing integration of electronic components, sensors, and control units in vehicles has significantly increased the need for durable insulation around connectors. In addition, heat shrink tubing improves reliability and longevity of connector assemblies under extreme temperature and mechanical stress conditions commonly experienced in automotive environments.

The under bonnet cable protection segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the increasing complexity of engine compartment wiring and rising demand for durable protection solutions. Heat shrink tubing is widely used to shield wiring harnesses and cables from heat, abrasion, oil exposure, and harsh environmental conditions inside the engine bay. The growing use of high-performance engines and advanced electronics in vehicles has intensified the need for reliable cable insulation and protection under the bonnet. In addition, automakers are focusing on improving electrical system durability and safety, which further drives demand for advanced heat shrink tubing solutions for under bonnet cable protection.

- By Material

On the basis of material, the heat shrink tubing for automotive market is segmented into polyolefin, polyvinyl chloride, polytetrafluoroethylene, fluorinated ethylene propylene, perfluoroalkoxy alkane, ethylene tetrafluoroethylene, and others. The polyolefin segment dominated the market with the largest market revenue share of 35.3% in 2025, driven by its excellent balance of flexibility, durability, and electrical insulation properties. Polyolefin heat shrink tubing is widely preferred in automotive applications due to its resistance to moisture, chemicals, and mechanical stress, which helps maintain stable performance in demanding environments. The material also provides effective insulation for wiring harnesses and electrical connections while maintaining ease of installation. In addition, its cost efficiency and availability in various shrink ratios make polyolefin tubing a widely adopted solution across several automotive electrical applications.

The polytetrafluoroethylene segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing demand for high-performance materials capable of withstanding extreme temperatures and aggressive chemicals. PTFE heat shrink tubing offers superior thermal stability, low friction, and exceptional resistance to oils and fuels, making it suitable for critical automotive electrical systems. The growing use of advanced electronics and high-temperature components in vehicles has increased the need for high-performance insulation materials. In addition, PTFE tubing is increasingly used in specialized automotive applications requiring reliable performance under harsh operating conditions.

- By Color

On the basis of color, the heat shrink tubing for automotive market is segmented into red, yellow, and others. The others segment dominated the market with the largest market revenue share in 2025, driven by the widespread use of black heat shrink tubing for general automotive electrical insulation and protection. Black tubing is widely adopted due to its ability to provide UV resistance, durability, and aesthetic compatibility with vehicle wiring harnesses. Automotive manufacturers commonly utilize black tubing for protecting electrical cables and connectors as it blends well with standard wiring systems. In addition, its effectiveness in concealing dirt and maintaining visual uniformity within vehicle electrical assemblies further supports its widespread adoption.

The yellow segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing emphasis on color-coded wiring systems and improved identification of electrical circuits. Yellow heat shrink tubing is often used for safety-related wiring and specialized electrical connections where quick identification is necessary during maintenance or inspection. The rising complexity of automotive electrical systems has increased the need for clear labeling and organized cable management solutions. In addition, the use of colored tubing helps technicians quickly identify circuits, improving repair efficiency and system reliability.

- By Type

On the basis of type, the heat shrink tubing for automotive market is segmented into single wall shrink tubing and dual wall shrink tubing. The single wall shrink tubing segment dominated the market with the largest market revenue share in 2025, driven by its widespread use in general automotive electrical insulation and wire protection. Single wall tubing provides reliable insulation and mechanical protection for wiring harnesses, connectors, and cable assemblies. Its lightweight structure, ease of installation, and cost effectiveness make it a preferred option for several standard automotive electrical applications. In addition, automotive manufacturers widely use single wall tubing in high-volume production due to its compatibility with automated assembly processes.

The dual wall shrink tubing segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the increasing demand for enhanced sealing and environmental protection in automotive electrical systems. Dual wall tubing features an inner adhesive layer that melts during shrinking, creating a strong seal against moisture, dust, and chemicals. This structure makes it highly suitable for applications exposed to harsh environmental conditions or requiring additional mechanical strength. In addition, the growing need for reliable insulation in advanced vehicle electronics and outdoor automotive components supports the increasing adoption of dual wall heat shrink tubing.

- By Voltage

On the basis of voltage, the heat shrink tubing for automotive market is segmented into low, medium, and high. The low voltage segment dominated the market with the largest market revenue share in 2025, driven by the extensive use of low voltage electrical systems in conventional automotive wiring and electronic components. Heat shrink tubing is widely applied in low voltage circuits for insulation, protection, and reinforcement of wiring harnesses. Most vehicle electrical systems such as lighting, sensors, infotainment, and control modules operate within low voltage ranges. In addition, the large number of low voltage wiring connections in vehicles significantly increases the demand for protective tubing solutions.

The medium voltage segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the increasing integration of advanced electrical systems and power distribution components in modern vehicles. Automotive systems such as high-capacity batteries, electric motors, and power electronics require reliable insulation solutions capable of handling higher voltage levels. Heat shrink tubing provides effective protection against electrical leakage and environmental exposure in these systems. In addition, the rising adoption of electrified vehicle platforms is increasing the demand for medium voltage insulation materials.

- By Fuel Type

On the basis of fuel type, the heat shrink tubing for automotive market is segmented into petrol, diesel/CNG, and electric. The petrol segment dominated the market with the largest market revenue share in 2025, driven by the high global production and ownership of petrol-powered passenger vehicles. These vehicles rely on extensive electrical wiring systems for ignition systems, sensors, and onboard electronics that require effective insulation and protection. Heat shrink tubing is widely used to protect wiring harnesses and electrical connections in petrol vehicles from heat and vibration. In addition, the large installed base of petrol vehicles continues to generate consistent demand for automotive electrical protection components.

The electric segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the rapid expansion of electric vehicle production worldwide. Electric vehicles contain complex high-voltage electrical systems, battery packs, and power electronics that require reliable insulation and protection solutions. Heat shrink tubing plays an important role in safeguarding battery wiring, connectors, and power cables from thermal and mechanical stress. In addition, the increasing focus on vehicle electrification and battery safety is significantly driving demand for advanced heat shrink tubing solutions in electric vehicles.

- By Sales Channel

On the basis of sales channel, the heat shrink tubing for automotive market is segmented into OEM and aftermarket. The OEM segment dominated the market with the largest market revenue share in 2025, driven by the large-scale use of heat shrink tubing during vehicle manufacturing and assembly processes. Automotive manufacturers integrate heat shrink tubing into wiring harness systems to ensure insulation, mechanical protection, and long-term durability. The increasing production of vehicles worldwide has significantly increased the demand for reliable electrical protection components at the manufacturing stage. In addition, OEM suppliers focus on high-quality materials and standardized components to meet automotive safety and performance requirements.

The aftermarket segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing demand for vehicle maintenance, repair, and electrical system upgrades. Heat shrink tubing is commonly used by service technicians and automotive repair facilities to restore damaged wiring insulation and improve connection reliability. The rising average vehicle age and increasing focus on maintenance of electrical systems contribute to the growth of the aftermarket segment. In addition, the growing availability of repair kits and electrical accessories supports the expanding use of heat shrink tubing in the automotive aftermarket.

- By Vehicle Type

On the basis of vehicle type, the heat shrink tubing for automotive market is segmented into passenger cars, LCV, HCV, and electric vehicles. The passenger cars segment dominated the market with the largest market revenue share in 2025, driven by the high global production and sales of passenger vehicles. Modern passenger cars incorporate numerous electronic systems including infotainment, safety sensors, control modules, and advanced driver assistance technologies. Heat shrink tubing plays an important role in protecting wiring harnesses and electrical components within these systems. In addition, the continuous integration of electronic features in passenger cars significantly increases the need for reliable insulation and cable protection materials.

The electric vehicles segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the rapid adoption of electrified mobility and supportive government policies promoting clean transportation. Electric vehicles require advanced electrical insulation solutions for battery packs, high-voltage cables, and power electronic systems. Heat shrink tubing provides reliable protection against heat, vibration, and environmental exposure in these critical components. In addition, the expansion of electric vehicle production and charging infrastructure is expected to further accelerate demand for automotive heat shrink tubing.

Asia-Pacific Heat Shrink Tubing for Automotive Market Regional Analysis

- China dominated the heat shrink tubing for automotive market with the largest revenue share in 2025, driven by its extensive automotive manufacturing ecosystem, large-scale production of wiring harnesses, and strong presence of electronics component suppliers serving both domestic and export markets

- Expanding electric vehicle production, rising automotive electronics integration, and strong supply chains for polymers and insulation materials reinforce China’s leadership in the regional market

- The presence of major automotive component manufacturers, continuous investments in EV infrastructure, and large-scale production of automotive wiring systems continue to strengthen China’s dominant position during the forecast period

Japan Heat Shrink Tubing for Automotive Market Insight

The Japan market is anticipated to grow steadily from 2026 to 2033, supported by its advanced automotive engineering capabilities and strong presence of leading vehicle manufacturers and electronics suppliers. Japanese automakers increasingly require high-performance insulation materials to protect complex wiring systems used in hybrid and electric vehicles. The demand for heat-resistant and durable tubing solutions is rising due to the country’s focus on vehicle reliability and safety standards. Continuous innovation in automotive electronics and strong collaboration between material suppliers and automotive manufacturers reinforce the market’s steady growth outlook. Japan’s emphasis on precision engineering, advanced materials, and high-quality automotive components underpins its strong regional position.

India Heat Shrink Tubing for Automotive Market Insight

India is projected to register the fastest CAGR in the Asia Pacific Heat Shrink Tubing for Automotive market during 2026–2033, driven by expanding automobile production and rapid growth of the domestic automotive component industry. Rising demand for passenger vehicles, increasing adoption of electric vehicles, and expansion of automotive electronics are accelerating the need for reliable wiring insulation solutions. Automotive manufacturers are increasingly focusing on durable and cost-effective heat shrink tubing to protect complex electrical systems within vehicles. Growing investments in automotive manufacturing facilities and strengthening supply chains for wiring harness production are improving product availability. Government initiatives supporting electric mobility and domestic automotive manufacturing further strengthen India’s emergence as the fastest-growing market in the region.

Asia-Pacific Heat Shrink Tubing for Automotive Market Share

The heat shrink tubing for automotive industry is primarily led by well-established companies, including:

- Molex (U.S.)

- TE Connectivity (Switzerland)

- Panduit (U.S.)

- ABB (Switzerland)

- 3M (U.S.)

- RADPOL S.A (Poland)

- The Zippertubing Company (U.S.)

- Dee Five (India)

- Insultab, PEXCO (U.S.)

- SHAWCOR (Canada)

- Sumitomo Electric Industries, Ltd. (Japan)

- Zeus Company Inc. (U.S.)

- HellermannTyton (U.K.)

- Shenzhen Woer Heat - Shrinkable Material Co., Ltd. (China)

- Techflex, Inc. (U.S.)

- Alpha Wire (China)

Latest Developments in Asia-Pacific Heat Shrink Tubing for Automotive Market

- In March 2025, Smiths Interconnect expanded its advanced insulation technology portfolio through the acquisition of Sensirion’s heat shrink tubing business. This strategic move enabled the company to strengthen its capabilities in high-performance interconnect and insulation solutions used in automotive electrical systems. The acquisition enhanced Smiths Interconnect’s product portfolio for wiring protection and electronic component insulation, supporting the increasing demand for reliable heat shrink tubing in modern vehicles with complex electrical architectures. It also strengthened the company’s competitive positioning in supplying advanced insulation materials to automotive manufacturers and component suppliers

- In November 2024, Avery Dennison entered a partnership with Sumitomo Electric Industries to jointly develop advanced heat-shrinkable insulation materials designed for next-generation electric vehicle wiring harness systems. The collaboration focused on improving thermal stability, durability, and insulation performance for high-voltage EV electrical networks. This partnership supported innovation in materials used for protecting critical vehicle wiring systems, contributing to the development of more reliable and efficient insulation solutions required in the rapidly expanding electric vehicle segment

- In August 2024, TE Connectivity launched a new portfolio of high-performance heat shrink tubing designed for automotive and transportation electrical applications. The product range was developed to provide improved mechanical protection, enhanced electrical insulation, and strong resistance to harsh automotive environments including vibration, heat, and chemical exposure. This product launch strengthened the company’s position in advanced connectivity and protection solutions while supporting the growing requirement for durable tubing materials in increasingly complex automotive electronics systems

- In 2024, Alpha Wire introduced a new range of high-temperature heat shrink tubing engineered to perform reliably in demanding automotive operating environments. The newly launched tubing solutions offer improved resistance to extreme temperatures, chemical exposure, and mechanical stress commonly experienced in vehicle engine compartments and electrical assemblies. This development expanded the availability of high-performance insulation materials for automotive wiring harnesses and electronic components, supporting the industry’s growing need for robust protection solutions in advanced vehicle platforms

- In 2023, 3M launched an environmentally focused heat shrink tubing product line aimed at improving sustainability in insulation and protection materials used across automotive electrical systems. The product range was designed to reduce manufacturing emissions and environmental impact while maintaining strong electrical insulation and mechanical protection capabilities. This initiative supported the automotive industry’s increasing emphasis on sustainable material development while ensuring reliable performance for wiring protection and electrical component insulation

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。