Europe Interventional Cardiology Peripheral Vascular Devices Market

市场规模(十亿美元)

CAGR :

%

USD

4.91 Billion

USD

8.43 Billion

2025

2033

USD

4.91 Billion

USD

8.43 Billion

2025

2033

| 2026 –2033 | |

| USD 4.91 Billion | |

| USD 8.43 Billion | |

| % | |

|

Europe Interventional Cardiology and Peripheral Vascular Devices Market Segmentation, By Product (Angioplasty Balloons, Stent, Catheters, Endovascular Aneurysm Repair Stent Grafts, Inferior Vena Cava (IVC) Filters, Plaque Modification Devices, Accessories and Hemodynamic Flow Alteration Devices), Type (Conventional and Standard), Procedure (Iliac Intervention, Femoropopliteal Interventions, Tibial (Below-The-Knee) Interventions, Peripheral Angioplasty, Arterial Thrombectomy and Peripheral Atherectomy), Indication (Peripheral Arterial Disease and Coronary Intervention), Age Group (Geriatric, Adults and Pediatric), End User (Hospitals, Ambulatory Surgery Centers, Nursing Facilities, Clinics and Others), Distribution Channel (Direct Tender, Third Party Distributors and Others)- Industry Trends and Forecast to 2033

Europe Interventional Cardiology and Peripheral Vascular Devices Market Size

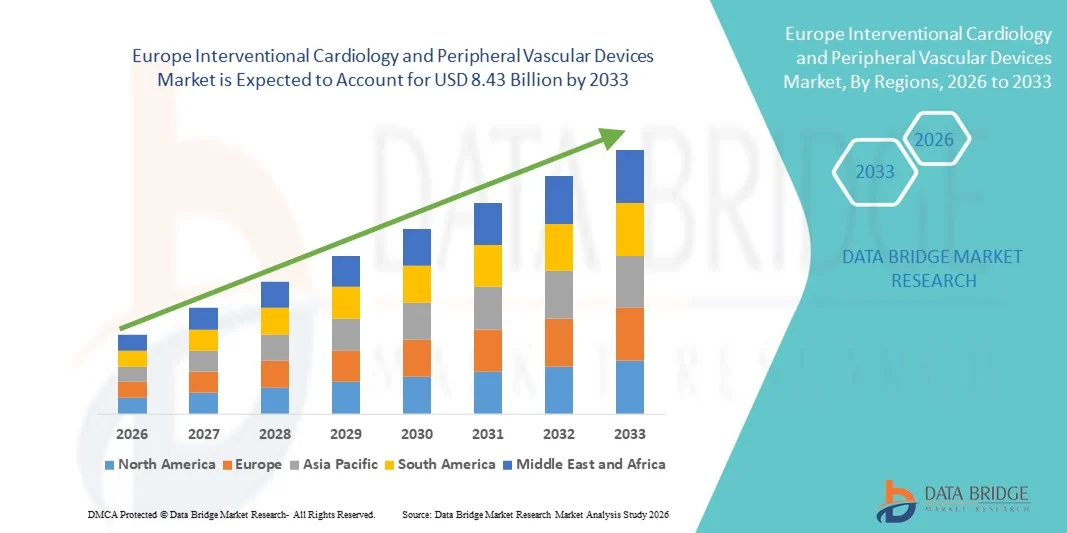

- The Europe interventional cardiology and peripheral vascular devices market size was valued at USD 4.91 billion in 2025 and is expected to reach USD 8.43 billion by 2033, at a CAGR of 7.00% during the forecast period

- The market growth is largely fueled by rising prevalence of cardiovascular diseases, increasing adoption of minimally invasive procedures, and ongoing technological innovation in interventional cardiology and vascular devices, which together are enhancing procedural efficiency and clinical outcomes across European healthcare systems

- Furthermore, supportive regulatory frameworks strong healthcare infrastructure, and a growing geriatric population demanding advanced cardiac care solutions are driving heightened adoption of interventional cardiology and peripheral vascular devices across hospitals and specialty cardiac centers, reinforcing the market’s robust expansion throughout the forecast timeline

Europe Interventional Cardiology and Peripheral Vascular Devices Market Analysis

- Interventional cardiology and peripheral vascular devices, including angioplasty balloons, stents, catheters, endovascular aneurysm repair stent grafts, IVC filters, and plaque modification devices, are increasingly vital components of modern cardiovascular care in both hospitals and specialty cardiac centers due to their minimally invasive nature, procedural efficiency, and ability to improve patient outcomes

- The escalating demand for these devices is primarily fueled by the rising prevalence of peripheral arterial disease and coronary artery disease, growing adoption of minimally invasive procedures such as peripheral angioplasty, arterial thrombectomy, and femoropopliteal interventions, and continuous technological advancements enhancing procedural safety, effectiveness, and ease of use

- Germany dominated the market with the largest revenue share of 28.5% in 2025, characterized by advanced healthcare infrastructure, high healthcare spending, and a strong presence of key medical device players

- Poland is expected to be the fastest-growing country during the forecast period due to increasing healthcare investments, expanding hospital networks, and rising awareness of minimally invasive cardiovascular treatments among adult and geriatric populations

- The stent segment dominated the market with a market share of 42.1% in 2025, driven by its proven clinical effectiveness, wide adoption across multiple procedures, and ongoing innovations improving safety and long-term patient outcomes

Report Scope and Europe Interventional Cardiology and Peripheral Vascular Devices Market Segmentation

|

Attributes |

Europe Interventional Cardiology and Peripheral Vascular Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Europe Interventional Cardiology and Peripheral Vascular Devices Market Trends

Advancements in Minimally Invasive and Image-Guided Procedures

- A significant and accelerating trend in the European interventional cardiology and peripheral vascular devices market is the growing adoption of minimally invasive and image-guided procedures, which improve patient outcomes while reducing recovery times

- For instance, drug-eluting stents and bioresorbable scaffolds are increasingly combined with intravascular imaging techniques such as IVUS and OCT to enhance procedural precision and safety

- Integration of advanced imaging and navigation systems with interventional devices allows cardiologists to optimize device placement, predict procedural outcomes, and reduce complication risks, improving overall procedural efficiency

- These innovations enable centralized procedural planning and real-time monitoring, facilitating better clinical decision-making across hospitals and specialized cardiac centers

- This trend toward more precise, efficient, and patient-friendly interventions is fundamentally reshaping expectations for cardiovascular care, with companies such as Boston Scientific and Abbott developing image-guided stent systems with real-time feedback for operators

- The demand for interventional devices that support advanced minimally invasive procedures and imaging integration is growing rapidly across hospitals and specialty centers, as patients and providers increasingly prioritize safety, efficiency, and procedural success

- Enhanced device interoperability with digital health platforms and electronic patient records is enabling better post-procedural monitoring and outcome tracking, boosting device utilization and clinical decision-making

Europe Interventional Cardiology and Peripheral Vascular Devices Market Dynamics

Driver

Rising Prevalence of Cardiovascular Diseases and Aging Population

- The increasing prevalence of cardiovascular diseases and a growing geriatric population are significant drivers for the heightened demand for interventional cardiology and peripheral vascular devices

- For instance, in March 2025, Abbott launched next-generation stents and balloon catheters in Europe designed for complex peripheral and coronary interventions, driving adoption across hospitals

- As cardiovascular disease incidence rises, interventional procedures offer minimally invasive, life-saving alternatives to open surgery, providing compelling advantages for both patients and providers

- Furthermore, the expansion of specialized cardiac centers and advanced catheterization labs is making interventional devices an integral component of modern cardiovascular care, supporting higher procedural volumes

- The increasing awareness of treatment options, coupled with technological innovations such as drug-eluting stents and advanced catheter systems, is propelling the adoption of these devices across adult and geriatric populations

- For instance, hospitals are increasingly using peripheral angioplasty and arterial thrombectomy devices to treat complex cases, expanding the market for specialized products

- Increasing collaborations between device manufacturers and research institutions are driving the development of novel devices and improved procedural techniques, further boosting market growth

Restraint/Challenge

High Device Costs and Regulatory Compliance Hurdles

- The relatively high cost of advanced interventional devices and the stringent regulatory requirements across European countries pose a significant challenge to market growth

- For instance, reimbursement delays and complex EU MDR approval processes can limit the timely adoption of new stents, catheters, and endovascular devices in hospitals and specialized centers

- Addressing these cost and compliance challenges through health insurance support, value-based pricing models, and regulatory guidance is crucial for wider market penetration

- In addition, some healthcare facilities in emerging European countries may face budget constraints, which can delay adoption of premium devices such as bioresorbable scaffolds or advanced IVC filters

- While procedural outcomes are improving, the combination of device cost, compliance hurdles, and training requirements for staff can hinder rapid adoption, particularly in smaller hospitals or clinics

- Overcoming these challenges through cost-effective device options, streamlined regulatory processes, and operator training programs will be vital for sustained market growth

- For instance, hospitals may face delays in integrating new devices due to the need for specialized staff training and equipment upgrades, slowing adoption rates

- Inconsistent reimbursement policies across European countries can create barriers for smaller hospitals or clinics, limiting access to advanced interventional devices despite strong clinical demand

Europe Interventional Cardiology and Peripheral Vascular Devices Market Scope

The market is segmented on the basis of product, type, procedure, indication, age group, end user, and distribution channel.

- By Product

On the basis of product, the market is segmented into angioplasty balloons, stents, catheters, endovascular aneurysm repair stent grafts, inferior vena cava (IVC) filters, plaque modification devices, accessories, and hemodynamic flow alteration devices. The stent segment dominated the market with the largest market revenue share of 42.1% in 2025, driven by its clinical effectiveness in both coronary and peripheral interventions. Stents provide reliable vessel patency, reducing restenosis rates, and are widely adopted in hospitals and specialty centers. Their broad range of types, including drug-eluting and bioresorbable variants, addresses different patient needs and complex lesions. The extensive clinical evidence supporting stent safety and outcomes further reinforces adoption. Leading players focus on stent innovation to enhance delivery systems, flexibility, and procedural ease. Hospitals often prioritize stents for high-volume procedures and for treating multi-vessel disease. Strong reimbursement support in Germany, France, and the U.K. also fuels their widespread use.

The angioplasty balloons segment is expected to witness the fastest growth during the forecast period, fueled by the increasing adoption of peripheral angioplasty procedures in geriatric and adult populations. Balloons are essential for pre-dilatation before stent placement and for standalone interventions in smaller or below-the-knee vessels. Advances such as drug-coated balloons and specialty balloons for complex lesions are driving adoption. Their minimally invasive nature, effectiveness in restoring blood flow, and lower procedural risks make them highly attractive. Growing awareness among physicians and expanding catheterization lab infrastructure in emerging European countries further contribute to growth. Manufacturers are introducing innovative balloon designs to improve crossing profile, deliverability, and safety, enhancing clinician preference.

- By Type

On the basis of type, the market is segmented into conventional and standard devices. The standard segment dominated the market in 2025 due to its proven clinical efficacy, broad availability, and compatibility with multiple procedures. Standard devices, including widely used stents and balloons, are preferred for their predictable outcomes and well-documented safety profiles. Hospitals and ambulatory centers often stock standard devices for common interventions, ensuring procedural readiness. Regulatory approvals and reimbursement coverage for standard devices are also well-established in Europe, contributing to adoption. Established manufacturers continue to optimize standard devices for enhanced performance and ease of use. Clinicians often rely on standard devices for routine coronary and peripheral interventions. Training and familiarity among healthcare professionals further reinforce their dominance.

The conventional segment is expected to witness the fastest growth during the forecast period, driven by technological innovations and the increasing adoption of new-generation conventional devices, such as bioresorbable stents and advanced IVC filters. These devices are gaining traction in specialized procedures and complex interventions. Their ability to reduce long-term complications, ease implantation, and improve hemodynamic outcomes makes them highly attractive. Emerging hospitals in Eastern Europe and expanding catheterization labs in countries such as Poland and Spain are contributing to this growth. Companies are focusing on R&D to develop conventional devices with enhanced flexibility, durability, and clinical performance, boosting market uptake.

- By Procedure

On the basis of procedure, the market is segmented into iliac intervention, femoropopliteal interventions, tibial (below-the-knee) interventions, peripheral angioplasty, arterial thrombectomy, and peripheral atherectomy. The femoropopliteal interventions segment dominated the market in 2025, accounting for the largest revenue share, due to the high prevalence of peripheral arterial disease in the femoropopliteal region. Femoropopliteal interventions often require stents, balloons, and specialized catheters, making them critical revenue drivers for device manufacturers. Hospitals and specialty centers prioritize devices suited for these procedures due to high patient volumes and clinical effectiveness. Technological advances in flexible stents and drug-coated balloons have improved outcomes in this segment. Clinicians increasingly prefer minimally invasive procedures in the femoropopliteal artery due to reduced recovery times and lower complication rates. Widespread adoption in Germany, France, and the U.K. further solidifies its dominance.

The peripheral angioplasty segment is expected to witness the fastest growth during the forecast period, fueled by rising demand for minimally invasive interventions in below-the-knee and small vessel lesions. Advances in drug-coated and specialty angioplasty balloons improve patency and reduce restenosis. Increasing prevalence of diabetes and peripheral artery disease in adults and geriatric patients is expanding procedure volumes. Hospitals in emerging European countries are investing in catheterization lab infrastructure, further driving adoption. Device manufacturers focus on delivering high-performance, low-profile balloons suitable for complex lesions. Training and procedural familiarity are improving adoption rates among interventional cardiologists.

- By Indication

On the basis of indication, the market is segmented into peripheral arterial disease and coronary intervention. The coronary intervention segment dominated the market in 2025, driven by the high prevalence of coronary artery disease and the large procedural volumes in Western Europe. Devices such as stents, balloons, and catheters are widely used in coronary interventions, supported by well-established clinical evidence and reimbursement policies. Hospitals prioritize coronary devices for routine PCI procedures, particularly in Germany, France, and the U.K. Innovations such as drug-eluting and bioresorbable stents further boost adoption. Clinicians favor minimally invasive coronary interventions for reduced hospital stays and faster recovery. Advanced imaging integration with coronary devices enhances procedural precision and outcomes.

The peripheral arterial disease segment is expected to witness the fastest growth during the forecast period, fueled by increasing prevalence of PAD among geriatric and adult populations. Interventions for femoropopliteal, tibial, and iliac arteries are expanding rapidly, driving demand for balloons, stents, and atherectomy devices. Technological advancements in drug-coated and specialty devices improve clinical outcomes, safety, and long-term patency. Hospitals and ambulatory surgery centers are increasingly adopting PAD-focused interventions. Expansion in emerging European markets and rising awareness among physicians contribute to the rapid growth.

- By Age Group

On the basis of age group, the market is segmented into geriatric, adults, and pediatric. The geriatric segment dominated the market in 2025, driven by the increasing prevalence of cardiovascular diseases and peripheral arterial disease among older populations. Geriatric patients frequently require stents, balloons, and catheters for coronary and peripheral interventions, making this segment a key revenue contributor. Hospitals prioritize device selection based on safety and clinical effectiveness for elderly patients. Technological advancements, such as low-profile stents and bioresorbable scaffolds, are particularly beneficial for geriatric interventions. Clinical guidelines emphasize minimally invasive procedures in this group, further boosting device adoption. Growing awareness and screening programs in Europe enhance procedural uptake.

The adult segment is expected to witness the fastest growth during the forecast period, fueled by rising incidence of cardiovascular risk factors, such as diabetes, hypertension, and obesity, in adults aged 30–65 years. Minimally invasive interventions are increasingly preferred over open surgery, driving demand for advanced stents, balloons, and catheter systems. Hospitals and specialty centers are investing in high-performance devices suitable for adult patients. Awareness campaigns and preventive care programs are increasing procedural volumes. Emerging European countries with expanding catheterization labs are supporting adult patient interventions. Manufacturers focus on developing devices optimized for adults to improve clinical outcomes and procedural efficiency.

- By End User

On the basis of end user, the market is segmented into hospitals, ambulatory surgery centers, nursing facilities, clinics, and others. The hospitals segment dominated the market in 2025, accounting for the largest revenue share, due to the availability of advanced infrastructure, catheterization labs, and specialized cardiology teams. Hospitals perform high-volume procedures requiring a broad range of stents, balloons, and catheter devices. They also have established procurement processes and access to reimbursement schemes, driving device adoption. Leading hospitals in Germany, France, and the U.K. are early adopters of new technologies and innovations. Integration of imaging-guided interventions in hospital settings enhances procedural success. Hospitals also serve as training centers for interventional cardiologists, further reinforcing device use.

The ambulatory surgery centers segment is expected to witness the fastest growth during the forecast period, fueled by the shift toward minimally invasive procedures and outpatient interventions. ASC adoption is rising due to lower procedural costs, reduced hospital stays, and growing patient preference for same-day treatments. Peripheral angioplasty, stent placement, and thrombectomy procedures are increasingly being performed in ASCs. Expansion of ASCs in emerging European countries supports this growth. Manufacturers are targeting ASCs with compact, easy-to-use devices suitable for outpatient procedures. Rising healthcare awareness and insurance coverage for outpatient interventions further drive adoption.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, third-party distributors, and others. The direct tender segment dominated the market in 2025, accounting for the largest share, due to strong relationships between device manufacturers and hospitals. Direct tender allows hospitals to procure high-value interventional devices such as stents and balloons at negotiated prices. Leading players maintain direct sales teams to provide training, technical support, and procedural guidance. Direct tender agreements in Germany, France, and the U.K. ensure timely availability of devices for high-volume interventions. Hospitals prefer direct channels for complex devices requiring ongoing service and support. Strong regulatory compliance and reimbursement coverage also favor direct procurement.

The third-party distributors segment is expected to witness the fastest growth during the forecast period, driven by expanding reach into emerging European countries and smaller clinics or ambulatory centers. Distributors provide a cost-effective and flexible supply of devices such as balloons, catheters, and accessories. They facilitate rapid market penetration for new products and ensure timely delivery to remote facilities. Manufacturers leverage distributor networks to increase device adoption and reduce logistical challenges. Growth in Eastern Europe and rising demand for minimally invasive procedures further support distributor channel expansion. Third-party distributors also enable product training and support in markets where direct sales presence is limited.

Europe Interventional Cardiology and Peripheral Vascular Devices Market Regional Analysis

- Germany dominated the market with the largest revenue share of 28.5% in 2025, characterized by advanced healthcare infrastructure, high healthcare spending, and a strong presence of key medical device players

- Patients and clinicians in Germany highly value the clinical efficacy, minimally invasive nature, and procedural precision offered by stents, balloons, and catheter-based interventions, which improve patient outcomes and reduce recovery times

- This widespread adoption is further supported by well-established reimbursement policies, high healthcare spending, and the presence of leading device manufacturers and innovative startups, establishing Germany as a key hub for both coronary and peripheral interventions

The Germany Interventional Cardiology and Peripheral Vascular Devices Market Insight

The Germany market captured the largest revenue share of 28.5% in 2025, driven by a high prevalence of coronary artery disease and peripheral arterial disease, combined with advanced hospital infrastructure and well-equipped catheterization labs. Hospitals and specialty cardiac centers prioritize minimally invasive procedures using stents, balloons, and catheter-based interventions for better patient outcomes. The presence of leading device manufacturers, innovative startups, and strong reimbursement policies further propels market growth. Integration of advanced imaging-guided procedures enhances procedural accuracy and safety, increasing clinician confidence in device adoption. Germany’s focus on patient-centered care and training programs for interventional cardiologists supports consistent procedural volumes. Moreover, technological innovation in stent and balloon design is fostering demand across coronary and peripheral interventions.

France Interventional Cardiology and Peripheral Vascular Devices Market Insight

The France market accounted for 17.3% of the European revenue share in 2025, driven by rising cardiovascular disease prevalence and increased procedural adoption in hospitals and ambulatory centers. French healthcare providers emphasize minimally invasive interventions to reduce hospital stays and improve recovery outcomes. Strong government reimbursement support and well-established hospital networks facilitate widespread device adoption. Hospitals increasingly rely on advanced stents, drug-coated balloons, and catheter systems for both coronary and peripheral interventions. Continuous training for interventional cardiologists and integration of imaging technologies contribute to the high procedural success rates. France is also witnessing growth in peripheral interventions, creating demand for specialized balloons, atherectomy devices, and stent systems.

U.K. Interventional Cardiology and Peripheral Vascular Devices Market Insight

The U.K. market is anticipated to grow at a noteworthy CAGR, driven by the increasing prevalence of cardiovascular conditions and a growing focus on minimally invasive procedures. Hospitals and specialty centers are expanding their catheterization labs and adopting new-generation stents, balloons, and IVC filters. Rising patient awareness of treatment options and strong reimbursement policies are facilitating higher procedural volumes. Clinicians are increasingly using imaging-guided interventions for both coronary and peripheral treatments. The U.K.’s well-developed healthcare infrastructure and focus on advanced cardiovascular care drive steady device adoption. Demand is growing across both adult and geriatric populations, supporting a wide range of product segments in the market.

Poland Interventional Cardiology and Peripheral Vascular Devices Market Insight

The Poland market is expected to witness the fastest growth in Europe during the forecast period, fueled by increasing healthcare investments and expanding hospital networks. Emerging catheterization labs are adopting stents, balloons, and peripheral intervention devices for both coronary and peripheral arterial disease. Rising awareness among physicians and patients about minimally invasive procedures is accelerating device adoption. International and local manufacturers are expanding distribution networks to support growing demand. The government’s healthcare initiatives and reimbursement schemes are facilitating market penetration. Furthermore, technological advancements such as drug-eluting and bioresorbable stents are attracting clinicians, supporting rapid market expansion.

Europe Interventional Cardiology and Peripheral Vascular Devices Market Share

The Europe Interventional Cardiology and Peripheral Vascular Devices industry is primarily led by well-established companies, including:

- Abbott (U.S.)

- Medtronic (Ireland)

- B. Braun SE (Germany)

- BIOTRONIK (Germany)

- Biosensors International Group, Ltd. (Switzerland)

- Boston Scientific Corporation (U.S.)

- Terumo Corporation (Japan)

- Edwards Lifesciences Corporation (U.S.)

- Cook (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Cardionovum GmbH (Germany)

- AngioDynamics, Inc. (U.S.)

- BD (U.S.)

- Merit Medical Systems, Inc. (U.S.)

- Cordis (U.S.)

- iVascular S.L.U. (Spain)

- Balton Sp. z o.o. (Poland)

- MicroPort Inc. (China)

- Lepu Medical Technology Co., Ltd. (China)

What are the Recent Developments in Europe Interventional Cardiology and Peripheral Vascular Devices Market?

- In January 2026, ACIST Medical Systems launched the ACIST Pro Diagnostic System in selected European markets under CE Mark, offering next‑generation automated contrast management designed to improve safety, precision, and efficiency in image‑guided cardiovascular procedures across cath labs

- In June 2025, Philips launched and supported the first patient cases in Europe of its VeriSight Pro 3D ICE catheter, a miniaturized steerable intracardiac 3D imaging device that enhances real‑time ultrasound guidance during structural heart and interventional cardiology procedures, improving procedural accuracy without general anesthesia

- In April 2025, Edwards Lifesciences’ SAPIEN M3 Transfemoral TMVR system received CE Mark approval in Europe, becoming the first transcatheter mitral valve replacement device using a transfemoral approach for patients with symptomatic mitral regurgitation who are unsuitable for surgery or transcatheter edge‑to‑edge therapy, expanding structural heart treatment options across European cath labs

- In September 2024, AngioDynamics announced CE Mark approval for the Auryon Atherectomy System for Peripheral Artery Disease (PAD), introducing a solid‑state laser atherectomy platform capable of treating a wide range of lesion types above and below the knee, thus broadening treatment options for complex PAD cases in European vascular practices

- In September 2022, Haemonetics received CE Mark certification for its Vascade vascular and venous closure systems, enabling commercialization of innovative femoral arterial and venous closure solutions used in interventional cardiology and peripheral vascular procedures, improving hemostasis and reducing patient recovery times

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。