Global 2nd Generation Lentiviral Vector Market

市场规模(十亿美元)

CAGR :

%

USD

117.81 Million

USD

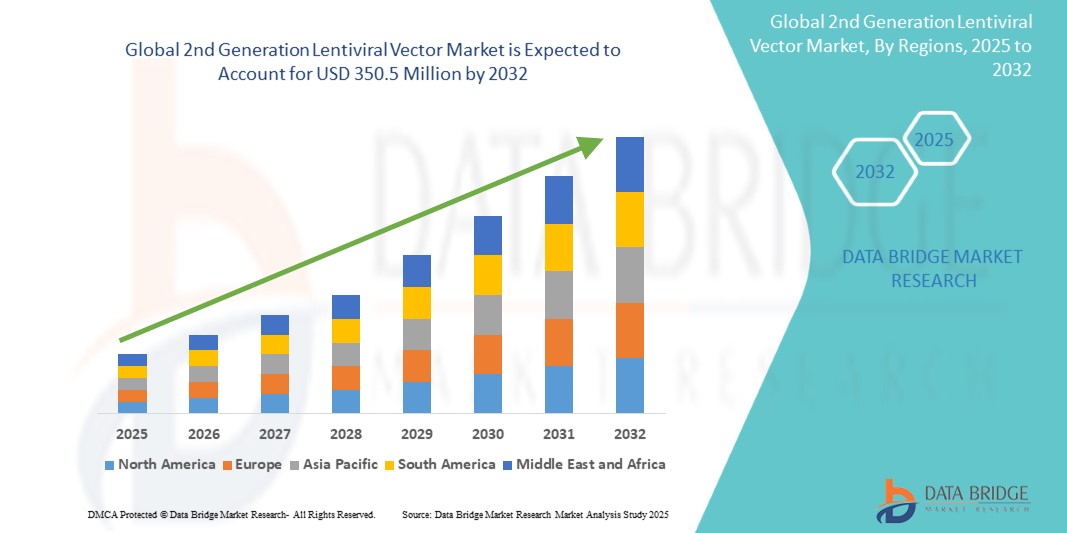

350.50 Million

2024

2032

USD

117.81 Million

USD

350.50 Million

2024

2032

| 2025 –2032 | |

| USD 117.81 Million | |

| USD 350.50 Million | |

| % | |

全球第二代慢病毒載體市場細分,按產品類型(預包裝載體和定制載體)、按應用(基因治療、癌症免疫治療、遺傳性疾病和 HIV 治療)、按最終用戶(生物製藥公司、學術和研究機構以及合約開發和製造組織)——行業趨勢和預測到 2032 年

全球第二代慢病毒載體市場分析

由於對先進基因療法、個人化醫療的需求不斷增加,以及針對遺傳疾病和癌症等複雜疾病的創新療法的興起,全球第二代慢病毒載體市場正在經歷大幅增長。第二代慢病毒載體因其與前幾代相比增強的安全性和效率而特別受重視,使其成為基因治療應用中的重要工具。慢病毒載體通常用於將治療基因遞送到患者細胞中,以糾正基因缺陷或治療慢性疾病,例如愛滋病毒和某些類型的癌症。生物製藥研究的進步、政府對基因療法的投資增加以及對精準醫療的日益關注進一步推動了市場的發展。此外,不斷擴大的基因治療產品線和利用慢病毒載體的臨床試驗正在推動市場成長。

全球第二代慢病毒載體市場規模

2024 年全球第二代慢病毒載體市場規模為 1.1781 億美元,預計到 2032 年將達到 3.505 億美元,2025 年至 2032 年預測期內的複合年增長率為 14.60%。除了對市場價值、成長率、細分、地理覆蓋範圍和主要參與者等市場情景的洞察外,Data Bridge Market Research 策劃的市場報告還包括深度專家分析、患者流行病學、管道分析、定價分析和監管框架。

全球第二代慢病毒載體市場趨勢

“基因治療和個人化醫療的進展”

全球第二代慢病毒載體市場的一個關鍵趨勢是越來越多地採用個人化醫療,特別是在治療遺傳疾病和癌症方面。第二代慢病毒載體被視為基因治療最有前途的工具之一,為將新的或校正的基因引入患者細胞提供了一種有效且安全的方法。鐮狀細胞性貧血和β-地中海貧血等基因療法的成功率不斷提高,為慢病毒載體在治療遺傳疾病方面創造了重大機會。此外,腫瘤學研究和癌症免疫療法的興起進一步加速了慢病毒載體在基因治療中的應用,這種治療可以改變免疫細胞,更有效地對抗癌症。個人化治療方法(根據個人基因圖譜客製化治療)正變得越來越普遍,這為慢病毒載體融入臨床實踐創造了新的途徑。因此,個人化基因治療的趨勢預計將顯著推動市場對第二代慢病毒載體的需求。

全球數位基因組市場細分

|

屬性 |

全球第二代慢病毒載體市場洞察 |

|

涵蓋的領域 |

|

|

覆蓋國家 |

美國、加拿大、墨西哥、德國、法國、英國、荷蘭、瑞士、比利時、俄羅斯、義大利、西班牙、土耳其、歐洲其他地區、中國、日本、印度、韓國、新加坡、馬來西亞、澳洲、泰國、印尼、菲律賓、亞太其他地區、沙烏地阿拉伯、阿聯酋、南非、埃及、以色列、中東和非洲其他地區、巴西、阿根廷、南美洲其他地區 |

|

主要市場參與者 |

默克集團(德國)、龍沙集團(瑞士)、富士膠片 Diosynth Biotechnologies USA Inc.(美國)、Cobra Biologics Ltd.(英國)、Brammer Bio(美國)、Waisman Biomanufacturing、Genezen(美國)、YPOSKESI(法國)、Advanced BioScience(美國)、Laborator(美國)、Laborers(美國)、Advanced BioScience Inc. SAS(法國)、ATVIO Biotech Ltd(英國) |

|

市場機會 |

|

|

加值資料資訊集 |

除了對市場價值、成長率、細分、地理覆蓋範圍和主要參與者等市場情景的洞察之外,Data Bridge Market Research 策劃的市場報告還包括深度專家分析、患者流行病學、管道分析、定價分析和監管框架。 |

全球第二代慢病毒載體市場定義

第二代慢病毒載體是一種早期基因傳遞系統,它在第一代系統的安全性和效率上有所改善。這些載體主要用於將遺傳物質轉移到目標細胞中,特別是用於研究目的,它們是更先進的第三代和第四代系統的前身。

全球第二代慢病毒載體市場

驅動程式

- 基因治療需求不斷成長

全球對基因治療的需求成長是第二代慢病毒載體市場成長的主要驅動力。慢病毒載體,尤其是第二代慢病毒載體,具有將治療基因高效、穩定地遞送到目標細胞中的能力,是基因治療中必不可少的工具。這對於治療遺傳疾病、癌症和其他以前難以透過傳統療法治療的疾病尤其重要。使用慢病毒載體的臨床試驗和FDA批准的基因治療產品數量的不斷增加凸顯了該技術在現代醫學中日益增長的重要性。隨著越來越多的罕見疾病和遺傳疾病透過基因為基礎的解決方案得到治療,對第二代慢病毒載體等先進、更安全的病毒載體系統的需求持續上升。

- 第二代慢病毒載體安全性和有效性的提高

第二代慢病毒載體在安全性和功效方面較早版本有了顯著的改進,使其在基因傳遞應用中越來越受歡迎。第二代載體經過精心設計,可降低插入誘變(插入的遺傳物質破壞宿主基因組)的風險並提高基因整合的精確度,從而解決舊載體系統的主要問題之一。這些改進,例如移除可能造成有害影響的病毒基因,使得第二代慢病毒載體在臨床和治療應用方面更具吸引力。隨著研究人員和臨床醫生不斷尋求更安全、更有效的基因治療方法,第二代慢病毒載體的使用預計將擴大,從而推動市場成長。

機會

- 腫瘤學和遺傳疾病應用的擴展

第二代慢病毒載體市場最重要的機會之一是這些載體在腫瘤學和遺傳疾病領域的應用日益廣泛。慢病毒載體越來越多地被用於基於基因的癌症免疫療法的開發,它們用於傳遞增強免疫系統瞄準和摧毀癌細胞的能力的基因。此外,對於鐮狀細胞性貧血、血友病和遺傳性失明等遺傳性疾病,第二代慢病毒載體提供了一個有希望的解決方案。隨著對越來越多的遺傳疾病的了解,使用這些載體的基因療法成為可行的治療選擇,創造了巨大的成長機會。隨著技術的進步,市場可能會繼續擴大,更成功的臨床結果將導致基於慢病毒載體的療法更廣泛的接受和採用。

- 政府和私營部門對基因治療研究的支持日益增加

慢病毒載體市場的另一個重大機會是政府和私部門投資者對基因治療研發的支持不斷增加。美國和歐洲等地區的政府正在為基因療法的開發提供補助和資金,並認識到基因療法在治療以前無法治癒的疾病方面的潛力。包括生技公司和製藥公司在內的私人企業也大力投資基因療法,作為其新療法研發線的一部分。不斷增長的資金支持使得對第二代慢病毒載體的研究更加深入,進一步推動了該技術的發展並提高了其應用範圍。隨著更多資源用於改善基因治療結果,第二代慢病毒載體市場在未來幾年可能會強勁成長。

限制/挑戰

- 生產成本高且複雜

第二代慢病毒載體市場面臨的主要挑戰之一是生產成本高且製造這些載體的複雜性。慢病毒載體的生產涉及複雜的過程,包括病毒顆粒的產生、生產細胞的轉染和純化,這些過程可能耗時且昂貴。生產具有所需純度和感染力的高品質慢病毒載體的成本很高。因此,高昂的銷售成本(COGS)可能會限制慢病毒載體療法的可及性,尤其是在醫療預算較為緊張的中低收入國家。此外,製造流程的複雜性可能導致生產的多變性以及擴大臨床或商業用途生產的挑戰。

- 監管障礙和漫長的審批時間

Regulatory challenges and lengthy approval processes present another restraint for the market. Gene therapies using lentiviral vectors require rigorous clinical trials and regulatory scrutiny before they can reach the market. Regulatory bodies like the FDA and EMA demand extensive safety and efficacy data before granting approval for gene therapy products. As gene therapies are relatively new, there are no well-established guidelines for these products, and regulatory agencies must develop new frameworks to assess their safety and effectiveness. The long approval timelines and regulatory hurdles can delay the commercial availability of gene therapy products, thereby affecting market growth. Furthermore, ensuring compliance with evolving regulatory standards, especially in different regions, can be challenging for companies developing lentiviral vector-based therapies.

This market report provides details of new recent developments, trade regulations, import-export analysis, production analysis, value chain optimization, market share, impact of domestic and localized market players, analyses opportunities in terms of emerging revenue pockets, changes in market regulations, strategic market growth analysis, market size, category market growths, application niches and dominance, product approvals, product launches, geographic expansions, technological innovations in the market. To gain more info on the market contact Data Bridge Market Research for an Analyst Brief, our team will help you take an informed market decision to achieve market growth.

Global 2nd Generation Lentiviral Vector Market Scope

The market is segmented by product type, application, end user and region. The growth amongst these segments will help you analyse meagre growth segments in the industries and provide the users with a valuable market overview and market insights to help them make strategic decisions for identifying core market applications.

Product Type

- Pre-packaged Vectors

- Custom Vectors

Application

- Gene Therapy

- Cancer Immunotherapy

- Genetic Disorders

- HIV Treatment

End-User

- Biopharmaceutical Companies

- Academic & Research Institutions

- Contract Development and Manufacturing Organizations

Global 2nd Generation Lentiviral Vector Market Regional Analysis

The market is analysed and market size insights and trends are provided by type, application, end user, and region as referenced above.

The countries covered in the market are U.S., Canada, Mexico, Germany, France, U.K., Netherlands, Switzerland, Belgium, Russia, Italy, Spain, Turkey, rest of Europe, China, Japan, India, South Korea, Singapore, Malaysia, Australia, Thailand, Indonesia, Philippines, rest of Asia-Pacific, Saudi Arabia, U.A.E., South Africa, Egypt, Israel, rest of Middle East and Africa, Brazil, Argentina, and rest of South America.

North America dominates the global 2nd generation lentiviral vector market, with the United States being a key contributor due to its advanced healthcare infrastructure, significant research investments, and established regulatory frameworks. The U.S. is home to numerous biotech companies and research institutions focusing on the development and application of gene therapies, which is driving the demand for lentiviral vectors. The market is further boosted by the presence of key market players, as well as the active involvement of regulatory bodies such as the FDA in facilitating the approval of gene therapies. The growing number of clinical trials and the increasing prevalence of genetic disorders and cancer are other factors contributing to North America's market leadership. Moreover, the region has a highly developed healthcare system, which ensures the swift adoption of innovative therapies, including those utilizing second-generation lentiviral vectors. With continuous advancements in biotechnology and gene therapy, North America is expected to maintain its dominance throughout the forecast period.

The Asia-Pacific region is the fastest growing market for second-generation lentiviral vectors, driven by rapid advancements in biotechnology and an expanding healthcare infrastructure. Countries like China, Japan, India, and South Korea are increasingly investing in biotechnology research and development, leading to a surge in clinical trials and the application of gene therapies. The growing focus on healthcare modernization and the rising prevalence of genetic disorders and cancer in the region further stimulate the demand for gene-based treatments, thus boosting the adoption of lentiviral vectors. In addition, the expansion of the biopharmaceutical industry, particularly in China and India, has increased the availability of gene therapies and lentiviral vector products. As Asia-Pacific countries embrace gene therapies as a standard treatment modality, the region is expected to experience the highest growth rate in the global market, with increasing government support and a growing number of biotech startups contributing to its expansion. The rise of medical tourism in countries like India, which offers affordable and advanced gene therapy options, also plays a role in the market’s rapid growth in this region.

報告的國家部分還提供了影響個別市場因素以及影響市場當前和未來趨勢的國內市場監管變化。下游和上游價值鏈分析、技術趨勢和波特五力分析、案例研究等數據點是用於預測各國市場情景的一些指標。此外,在對國家數據進行預測分析時,還考慮了全球品牌的存在和可用性及其因來自本地和國內品牌的大量或稀缺的競爭而面臨的挑戰、國內關稅和貿易路線的影響。

全球第二代慢病毒載體市場份額

市場競爭格局提供了競爭對手的詳細資訊。詳細資訊包括公司概況、公司財務狀況、收入、市場潛力、研發投資、新市場計劃、全球影響力、生產基地和設施、生產能力、公司優勢和劣勢、產品發布、產品寬度和廣度、應用優勢。以上提供的數據點僅與公司對市場的關注有關。

在全球第二代慢病毒載體市場中營運的領導者有:

- 默克集團(德國)

- 龍沙(瑞士)

- 富士軟片 Diosynth Biotechnologies USA Inc.(美國)

- Cobra Biologics Ltd.(英國)

- Brammer Bio(美國)

- Waisman 生物製造、治療(美國)

- YPOSKESI(法國)

- 先進生物科學(美國)

- Laboratories Inc.(ABL Inc.)(美國)

- Novasep Holding SAS(法國)

- ATVIO Biotech Ltd(英國)

全球第二代慢病毒載體市場最新進展

- 2022 年 6 月,Avid Bioservices, Inc. 開放了其分析和製程開發 (AD/PD) 套件。這些套件是該公司慢病毒載體開發和現行良好生產規範 (CGMP) 製造設施的一部分

- 2022年5月,AGC Biologics表示將在科羅拉多州朗蒙特的商業級場地增加病毒載體懸浮技術和空間。這將使研究和製作基因療法變得更加容易

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。