Global Antiviral Drugs Market

市场规模(十亿美元)

CAGR :

%

USD

78.12 Billion

USD

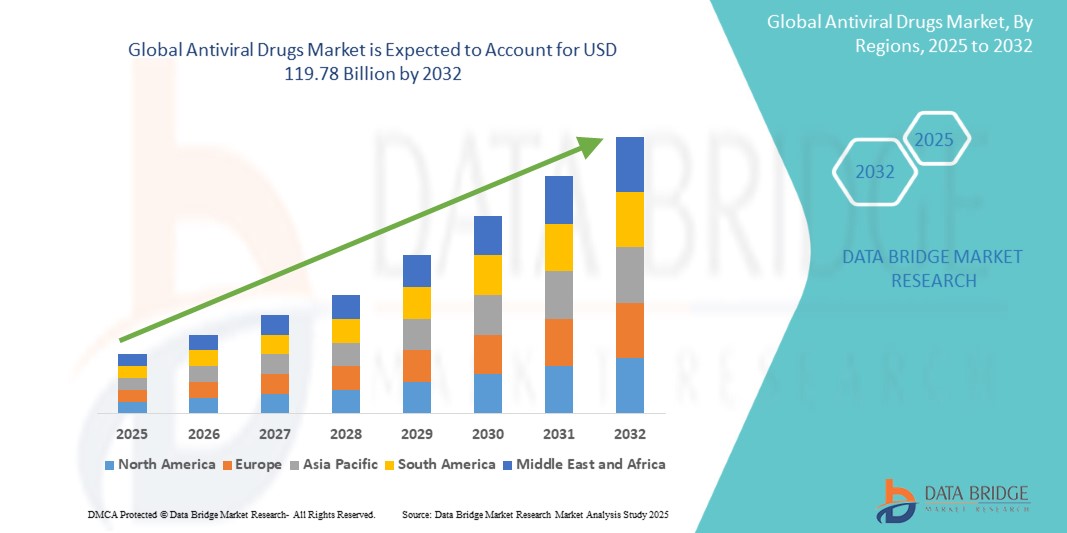

119.78 Billion

2024

2032

USD

78.12 Billion

USD

119.78 Billion

2024

2032

| 2025 –2032 | |

| USD 78.12 Billion | |

| USD 119.78 Billion | |

| % | |

|

全球抗病毒藥物市場細分,按適應症(流感、人類免疫缺陷病毒 (HIV)、C型肝炎病毒 (HCV)、呼吸道合胞病毒、單純皰疹病毒、人類巨細胞病毒 (HCMV)、水痘帶狀皰疹病毒 (VZV)、B型肝炎病毒(HBV)、冠狀病毒感染等)、病患類型(兒童、成人和老年人)、產品(口服、外用和腸外)、藥物類型(仿製藥和品牌藥)、最終用戶(醫院、診所、家庭醫療保健、專科中心、門診中心等)、分銷渠道(醫院藥房、網上藥房和零售藥房) - 行業趨勢和預測到 2032 年

抗病毒藥物市場規模

- 2024 年全球抗病毒藥物市場規模為781.2 億美元,預計到 2032 年將達到 1,197.8 億美元,預測期內 複合年增長率為 5.5%。

- 市場成長主要得益於愛滋病毒、肝炎、流感和皰疹等病毒感染的盛行率不斷上升,以及全球越來越重視透過先進的抗病毒療法預防和控制傳染病

- 此外,藥物研發技術的進步、醫療基礎設施投資的不斷增長以及新興市場醫療服務覆蓋範圍的不斷擴大,正在加速抗病毒藥物的普及。這些因素共同推動了已開發地區和發展中地區的強勁需求,從而顯著促進了該行業的成長。

抗病毒藥物市場分析

- 抗病毒藥物可以抑制病毒在體內的發展和複製,由於其具有針對性的作用、降低病毒載量的能力以及在預防疾病進展和傳播方面的作用,已成為治療和管理急性和慢性各種病毒感染的必需藥物。

- 對抗病毒藥物的需求不斷增長,主要原因是愛滋病毒、肝炎和流感等感染在全球範圍內的流行率不斷上升,新興經濟體醫療保健服務的普及,藥物製劑的進步,以及人們對早期診斷和及時抗病毒幹預的認識不斷提高

- 由於製藥業成熟、醫療基礎設施強大以及公共和私人對抗病毒研究和治療項目投入大量資金,北美在抗病毒藥物市場佔據主導地位, 2024 年市場份額達到58.66%

- 由於醫療保健意識的提高、醫療保健基礎設施的改善以及病毒感染負擔的增加,預計亞太地區抗病毒藥物市場在預測期內將以 6.7% 的最快複合年增長率增長

- 流感藥物在抗病毒藥物市場佔據主導地位,2024 年的市場份額最大,為 34.54%,因為這些適應症在全球範圍內更為普遍

報告範圍和抗病毒藥物市場細分

|

屬性 |

抗病毒藥物關鍵市場洞察 |

|

涵蓋的領域 |

|

|

覆蓋國家 |

北美洲

歐洲

亞太

中東和非洲

南美洲

|

|

主要市場參與者 |

|

|

市場機會 |

|

|

加值資料資訊集 |

除了對市場價值、成長率、細分、地理覆蓋範圍和主要參與者等市場情景的洞察之外,Data Bridge Market Research 策劃的市場報告還包括深度專家分析、患者流行病學、管道分析、定價分析和監管框架。 |

抗病毒藥物市場趨勢

“病毒感染日益普及”

- 抗病毒藥物市場的一個重要且加速的趨勢是病毒感染(如愛滋病毒、B型肝炎和C肝、流感以及包括冠狀病毒株在內的新興病毒威脅)的盛行率不斷上升,這加劇了全球對抗病毒療法開發的關注

- 例如,全球B肝患者超過2.5億,每年的流感疫情導致數百萬重症病例和數十萬人死亡,迫切需要有效的抗病毒治療

- 人畜共通傳染病溢出的頻率不斷增加,傳染性病毒在全球蔓延,促使醫療保健系統和製藥公司優先考慮抗病毒準備和應對措施,鼓勵開發預防和治療解決方案

- 各國政府和國際衛生組織正為抗病毒研究、監測計畫和儲備基本抗病毒藥物撥出更多資金,以加強公共衛生部門對病毒爆發的防範

- 這一趨勢也激發了人們對將現有抗病毒藥物重新用於多種適應症以及加快監管審批流程以便在大流行期間快速部署治療的興趣

- 全球範圍內病毒感染的日益流行正在重塑醫療保健的優先事項,並將抗病毒藥物開發定位為醫藥創新和公共衛生投資的關鍵領域

抗病毒藥物市場動態

司機

“新型抗病毒藥物研發的進展”

- 新型抗病毒藥物研發的快速進步是抗病毒藥物市場成長的重要驅動力,製藥公司投資於新型分子、改進的配方和有針對性的輸送系統,以提高療效並減少抗藥性

- 例如,2024 年 1 月,輝瑞啟動了針對多種流感病毒株的下一代口服抗病毒藥物的 II 期試驗,這反映了業界在開發廣譜抗病毒藥物的同時,考慮到大流行防範的廣泛努力

- 隨著病毒變異和新興病原體的全球威脅日益加劇,研究越來越集中於開發特異性更高、半衰期更長、副作用更少的抗病毒藥物,以確保更好的患者依從性和治療效果

- 分子生物學、高通量篩選和計算建模的進步也加速了藥物創新,加速了藥物的發現和設計

- 這些創新正在推動更強大的抗病毒產品線,並有望改變慢性、急性和新發病毒感染的治療模式,從而擴大各個醫療保健領域的市場潛力

克制/挑戰

“抗病毒藥物成本高”

- 抗病毒藥物的高成本對藥物的廣泛可及性和持續的市場成長構成了重大挑戰,特別是在醫療預算和保險覆蓋範圍往往有限的中低收入國家

- 例如,用於治療丙型肝炎或愛滋病毒等的品牌抗病毒藥物的價格可能超過每個治療週期數千美元,這給公共衛生系統和個別患者都帶來了負擔能力障礙

- 某些地區成本效益高的仿製藥替代品供應有限,進一步加劇了這一問題,限制了公平獲得基本藥物的機會,並阻礙了治療依從性

- 全球醫療保健系統的報銷挑戰和不一致的定價政策可能會延遲採用,特別是在藥品採購框架不發達的國家

- 應對這項挑戰需要協調努力,支持仿製藥生產,提高定價透明度,並實施患者援助計劃,以確保更廣泛的人群能夠獲得有效的抗病毒療法,同時又不損害財務可持續性

抗病毒藥物市場範圍

市場根據適應症、患者類型、產品、藥物類型、最終用戶和分銷管道進行細分。

- 按適應症

根據適應症,抗病毒藥物市場細分為流感、人類免疫缺陷病毒 (HIV)、C型肝炎病毒 (HCV)、呼吸道合胞病毒、單純皰疹病毒、人類鉅細胞病毒 (HCMV)、水痘帶狀皰疹病毒 (VZV)、B型肝炎病毒 (HBV)、冠狀病毒感染和其他。預計到 2024 年,流感藥物將佔據全球抗病毒藥物市場的主導地位,市場份額為 34.54%,這主要是因為流感具有廣泛性和反覆性,會導致可預測的季節性流行病,並在全球範圍內造成沉重的疾病和死亡負擔。病毒的不斷進化進一步擴大了這種持續的需求,因此需要不斷開發新的抗病毒藥物和更新的疫苗,同時提高人們的認識並採取強有力的公共衛生措施,促進早期診斷和治療,特別是在老年人和幼兒等弱勢群體中。

預計丙型肝炎(HCV)領域將在2025年至2032年期間實現最快的複合年增長率,這得益於診斷率的提高以及透過直接抗病毒藥物(DAA)提供的治癒性治療方案。公共衛生部門為消除C型肝炎而加大的力度,尤其是在亞太地區和東歐地區,加上仿製藥競爭帶來的價格下降,正在提高丙型肝炎的可及性和採用率。

- 依患者類型

根據患者類型,市場細分為兒童、成人和老年人。預計老年人群體將在2024年佔據全球抗病毒藥物市場的主導地位,市場份額最高,達到49.11%,這主要是由於全球人口老齡化以及隨著年齡增長而出現的免疫功能下降(免疫衰老)。免疫系統的自然衰弱使老年人更容易感染各種病毒,包括常見的流感病毒和呼吸道合胞病毒 (RSV),以及更嚴重的皰疹病毒,甚至愛滋病毒和肝炎等慢性病毒感染。

The adult segment is anticipated to experience the fastest growth from 2025 to 2032. The adult population, encompassing a broad age range, is highly susceptible to a wide array of viral infections, including chronic conditions like HIV/AIDS and hepatitis, as well as seasonal illnesses such as influenza and emerging viral threats. The increasing global prevalence and incidence of these viral diseases among adults create a constant and growing demand for effective antiviral treatments.

- By Products

On the basis of product type, the market is segmented into Oral, Topical, and Parenteral. The oral segment is expected to dominate the global antiviral drugs market with a largest market share of 64.44% in 2024 primarily due to the overwhelming preference for oral administration among both patients and healthcare providers. Oral medications offer unparalleled convenience, ease of self-administration at home, and are non-invasive, eliminating the pain and discomfort associated with injections. This significantly improves patient adherence to treatment regimens, particularly for chronic viral infections requiring long-term therapy (like HIV and hepatitis) or for early intervention in acute conditions (like influenza and COVID-19).

The parenteral segment is forecasted to grow at the fastest CAGR during 2025–2032. This is due to rising emphasis on long-acting injectable (LAI) antiviral therapies, particularly for chronic conditions like HIV and hepatitis. These LAIs offer significant advantages in terms of patient adherence by reducing the frequency of dosing from daily pills to monthly or even bimonthly injections, thereby improving treatment outcomes and quality of life. This is especially beneficial for patients who struggle with daily oral medication regimens or face challenges related to compliance.

- By Drug Type

On the basis of drug type, the market is categorized into Branded and Generic drugs. The generic segment is expected to dominate the global antiviral drugs market with a largest market share of 65.58% in 2024 primarily due to the expiration of patents for numerous blockbuster branded antiviral drugs. This patent cliff allows generic manufacturers to produce and market bioequivalent versions of these drugs at significantly lower prices. The inherent cost-effectiveness of generics makes them highly attractive to patients, healthcare providers, and governments worldwide, who are increasingly focused on controlling rising healthcare expenditures and improving access to affordable medication.

Meanwhile, the branded drug segment is expected to expand at the fastest rate from 2025 to 2032. This is due to relentless focus on innovation and the introduction of novel, highly effective therapies for unmet medical needs. While generics dominate in terms of volume due to their affordability, branded drugs are at the forefront of developing breakthrough treatments for difficult-to-treat or emerging viral infections where no generic alternatives exist. These include therapies with novel mechanisms of action, improved safety profiles, enhanced patient convenience (such as long-acting injectables or single-pill regimens for chronic conditions), and those targeting drug-resistant viral strains. Significant investments in research and development by major pharmaceutical companies, coupled with robust patent protection, allow them to command premium pricing for these innovative products.

- By End User

On the basis of end user, the market is segmented into Hospitals, Clinics, Home Healthcare, Specialty Centers, Ambulatory Centers, and Others. Hospitals held the dominant market share of 52.00% in 2024 due to their critical role in managing severe viral infections, inpatient care for high-risk groups, and immediate access to parenteral formulations. They also serve as primary centers for diagnosis, viral load monitoring, and treatment initiation, especially for life-threatening infections.

Home healthcare is projected to register the fastest CAGR from 2025 to 2032. With the expansion of oral antivirals and digital health solutions, more patients are managing chronic conditions such as HIV and HBV from home. Rising preference for decentralized care, the convenience of home delivery of medications, and increased availability of telemedicine consultations are key contributors to the shift.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into Hospital Pharmacy, Online Pharmacy, and Retail Pharmacy. Hospital pharmacies held the leading share of 54.07% in 2024 due to the centralization of drug dispensing in inpatient settings and the critical need for controlled administration of specialized antivirals. Hospitals often stock a broader range of formulations including injectables and emergency antivirals not readily available at retail.

The online pharmacy segment is expected to record the highest CAGR from 2025 to 2032. Factors such as increasing internet penetration, e-prescriptions, rising consumer inclination towards doorstep delivery, and the growing number of patients managing chronic infections at home are boosting this channel. Regulatory support and the rise of digital health platforms also play a key role in expanding online access to antiviral drugs.

Antiviral Drugs Market Regional Analysis

- North America dominated the antiviral drugs market with the largest revenue share of 58.66% in 2024, driven by well-established pharmaceutical industry, strong healthcare infrastructure, and significant public and private investment in antiviral research and treatment programs

- The region’s high prevalence of chronic viral infections such as HIV, HBV, and HCV, along with widespread access to advanced diagnostics and antiviral therapies, drives consistent market demand

- In addition, proactive government initiatives, extensive awareness campaigns, and early adoption of novel antiviral drugs contribute to North America's leading position in both treatment accessibility and innovation

U.S. Antiviral Drugs Market Insight

U.S. antiviral drugs market captured the largest revenue share of 74.87% of North America in 2024, propelled by the high disease burden, favorable regulatory pathways, and strong presence of global pharmaceutical companies. The growing incidence of influenza and sexually transmitted viral infections, coupled with continuous innovation in drug development and delivery mechanisms, further drives demand. Furthermore, the U.S. benefits from well-funded healthcare programs such as Medicaid and Medicare, which support widespread access to antiviral medications.

Europe Antiviral Drugs Market Insight

Europe antiviral drugs market is projected to witness robust growth during the forecast period, driven by rising government investments in infectious disease control and increasing adoption of preventive therapies. High awareness about viral diseases such as HIV, HCV, and seasonal flu among the population leads to consistent demand for both treatment and prophylactic antivirals. European health systems' emphasis on evidence-based medicine, early screening, and universal healthcare access enhances treatment coverage, while regulatory support for generic drug manufacturing is also reshaping market dynamics.

U.K. Antiviral Drugs Market Insight

U.K. antiviral drugs market is expected to grow at a notable CAGR, driven by increasing awareness of viral infections and the presence of strong public health infrastructure. The National Health Service (NHS) plays a key role in facilitating access to antiviral treatments, especially for chronic infections such as HIV and HBV. Moreover, ongoing clinical trials and collaborative efforts with academic research institutions are contributing to the development of next-generation antivirals.

Germany Antiviral Drugs Market Insight

預計德國抗病毒藥物市場將穩定成長,這得益於高昂的醫療支出、強勁的藥品研發以及規範的藥品審批流程。德國專注於早期診斷和遵循標準化治療方案,這促進了抗病毒療法的普及,尤其是在皰疹、鉅細胞病毒(CMV)和流感等疾病的治療方面。德國人口老化也推動了針對免疫功能低下人口的抗病毒預防和治療需求。

亞太抗病毒藥物市場洞察

預計在2025年至2032年的預測期內,亞太地區抗病毒藥物市場將以最快的複合年增長率增長,這得益於醫療保健意識的提升、醫療基礎設施的改善以及病毒感染負擔的加重。在政府措施和全球衛生夥伴關係的支持下,中國、印度和日本等國家獲得診斷和治療的管道正在增加。該地區人口的成長、中產階級的壯大以及抗病毒藥物價格的不斷下降(尤其是透過仿製藥生產),進一步推動了市場擴張。

日本抗病毒藥物市場洞察

日本抗病毒藥物市場正蓬勃發展,得益於其積極的公共衛生政策、高水準的技術創新以及龐大的老齡人口。日本高度重視季節性免疫以及流感和皰疹等病毒感染的早期治療。日本製藥公司正在大力投資新型抗病毒藥物的開發,同時數位健康整合也提高了抗病毒治療方案的依從性和監測能力。

中國抗病毒藥物市場洞察

2024年,受政府支持的醫療改革、快速都市化以及乙肝病毒(HBV)、丙肝病毒(HCV)和愛滋病毒(HIV)盛行率上升的推動,中國抗病毒藥物市場佔據亞太地區最大收入份額。中國不斷擴張的生物製藥產業,加上強大的國內生產能力,提升了抗病毒藥物的可近性和可負擔性。持續進行的公共衛生工作,包括大規模疫苗接種和篩檢活動,進一步促進了持續的需求。

抗病毒藥物市場份額

抗病毒藥物產業主要由知名公司主導,包括:

- 吉利德科學公司(美國)

- F. Hoffmann-La Roche Ltd(瑞士)

- 葛蘭素史克公司(英國)

- Abbvie(美國)

- 默克公司(美國)

- 強生服務公司(美國)

- 百時美施貴寶公司(美國)

- 西普拉公司(印度)

- 奧羅賓多製藥(印度)

- 雷迪博士實驗室有限公司(印度)

- Zydus Pharmaceuticals, Inc.(印度)

- 邁蘭製藥 ULC(美國)

- Teva Pharmaceuticals USA, Inc.(美國)

- 新興(美國)

- 太陽製藥工業有限公司(印度)

- Avet Pharmaceuticals Inc.(美國)

- 輝瑞公司(美國)

- SIGA Technologies(美國)

- NAVINTA LLC.(美國)

- 麥克勞茲製藥有限公司(印度)

- BioCryst Pharmaceuticals, Inc.(美國)

- 異性戀(印度)

全球抗病毒藥物市場最新動態

- 2023年5月,美國食品藥物管理局(FDA)批准Paxlovid作為第一個用於治療高風險成人輕度至中度COVID-19的口服抗病毒藥物,標誌著抗病毒藥物市場的一個重要里程碑。此次批准提高了美國乃至全球口服抗病毒藥物的市場滲透率,推動了創新和競爭,同時也強化了向更便捷的門診COVID-19治療方案的轉變,從而進一步推動了市場擴張。

- 2023年1月,默克公司(簡稱MSD)宣布已透過其子公司成功完成對Imago Biosciences, Inc.(納斯達克股票代碼:IMGO)所有流通普通股的現金要約收購,收購價格為每股36.00美元,不計利息,但需扣除任何必要的預扣稅。此次收購將有助於公司收入的成長。

- 2022年1月,魯賓有限公司(Lupin Limited)在印度獲得緊急使用授權,成功上市莫努皮拉韋(Molnupiravir),為病情進展風險較高的新冠肺炎患者拓展了治療選擇,從而顯著影響了抗病毒藥物市場。該藥物的上市刺激了口服抗病毒藥物的需求,尤其是在新興市場,從而加速了疫情持續期間的市場成長。

- 2021年4月,Zydus Pharmaceuticals, Inc.宣布已獲得印度藥品管理總局(DCGI)的限制性緊急使用批准,允許使用抗病毒藥物Virafin治療中度COVID-19感染。這將有助於該公司提升其在全球其他地區的全球影響力和聲譽。

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。