Global Cladding System Market

市场规模(十亿美元)

CAGR :

%

USD

278.81 Billion

USD

444.38 Billion

2024

2032

USD

278.81 Billion

USD

444.38 Billion

2024

2032

| 2025 –2032 | |

| USD 278.81 Billion | |

| USD 444.38 Billion | |

| % | |

|

全球覆層系統市場細分,按材料(陶瓷、木材、灰泥和 EIFS、磚和石材、金屬、乙烯基、纖維水泥等)、組件(屋頂、牆壁、門窗等)、功能(絕緣、空氣和蒸汽控制、降水控制、運動接頭和裂縫控制等)、覆層類型(幕牆、夾層板、專利玻璃、懸掛、金屬型光、磚和磚石

覆層系統市場規模

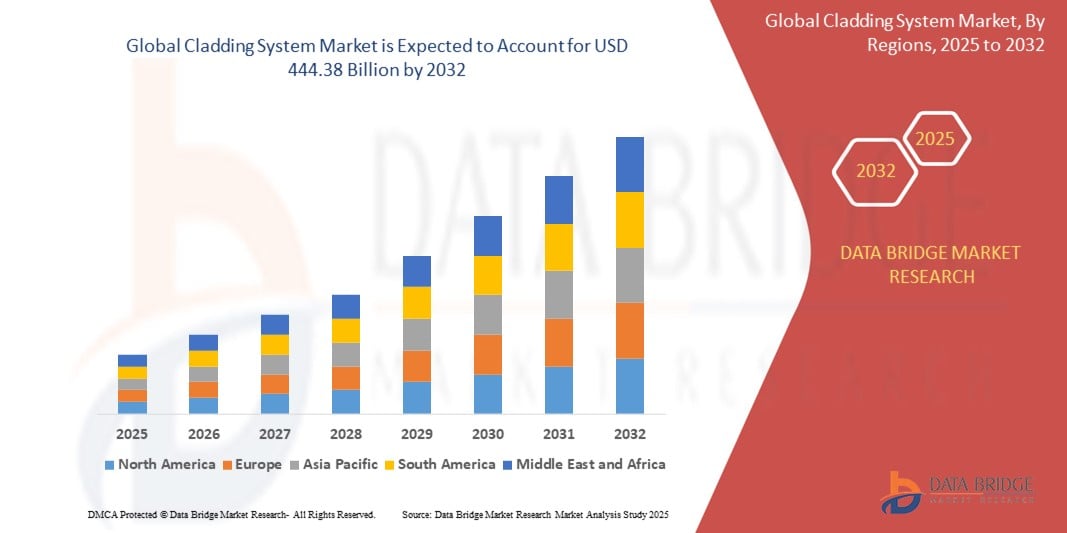

- 2024 年全球覆層系統市場規模為2,788.1 億美元 ,預計 到 2032 年將達到 4,443.8 億美元,預測期內 複合年增長率為 6.00%。

- 市場成長主要受到建築活動的增加、對節能建築解決方案的需求不斷增長以及提高耐用性和美觀性的覆層材料的進步的推動

- 消費者對永續和低維護建築材料的偏好日益增長,加上推行綠建築的嚴格法規,進一步加速了住宅和非住宅應用中覆層系統的採用

覆層系統市場分析

- 覆層系統用於為建築物外部提供保護層和裝飾層,由於其能夠增強隔熱性、耐候性和美觀性,是現代建築的重要組成部分。

- 快速的城市化、對永續建築實踐的日益關注以及對節能建築圍護結構的需求推動了覆層系統需求的激增

- 北美在覆層系統市場佔據主導地位,2024 年其收入份額最大,為 38.5%,這得益於強勁的建築活動、先進建築材料的廣泛採用以及主要行業參與者的存在

- 預計亞太地區將成為預測期內成長最快的地區,這得益於中國、印度和日本等國家快速的城市化、基礎設施投資的增加以及可支配收入的增加

- 陶瓷產業在 2024 年佔據了最大的市場收入份額,達到 32%,這得益於其耐用性、低維護性和美觀性,使其成為住宅和商業應用的首選

報告範圍和覆層系統市場細分

|

屬性 |

覆層系統關鍵市場洞察 |

|

涵蓋的領域 |

|

|

覆蓋國家 |

北美洲

歐洲

亞太

中東和非洲

南美洲

|

|

主要市場參與者 |

|

|

市場機會 |

|

|

加值資料資訊集 |

除了對市場價值、成長率、細分、地理覆蓋範圍和主要參與者等市場情景的洞察之外,Data Bridge Market Research 策劃的市場報告還包括進出口分析、生產能力概覽、生產消費分析、價格趨勢分析、氣候變遷情景、供應鏈分析、價值鏈分析、原材料/消耗品概覽、供應商選擇標準、PESTLE 分析、波特分析和監管框架。 |

覆層系統市場趨勢

“智慧技術與永續材料的日益融合”

- 全球覆層系統市場正經歷一個重要的趨勢,即整合智慧技術和永續材料,以提高建築性能和環境影響

- 智慧外牆系統融合了相變材料 (PCM) 和感測器等技術,能夠自適應地響應環境條件,透過調節建築溫度來提高能源效率。例如,PCM 增強型外牆系統可將冷凍能耗降低高達 30%。

- 隨著建築師和建築商優先考慮綠色建築認證和永續發展目標,再生鋁複合材料、竹子和低碳纖維水泥等再生環保材料的使用越來越受到關注

- James Hardie 等公司正在開發低碳水泥技術,其產品如 Hardie® Artisan Lap Siding 因其永續性和氣候適應性而獲得認可

- This trend enhances the appeal of cladding systems for both residential and non-residential applications, aligning with global sustainability initiatives such as the European Green Deal, which aims for climate neutrality by 2050

Cladding System Market Dynamics

Driver

“Rising Demand for Energy-Efficient and Aesthetically Appealing Buildings”

- Increasing consumer and regulatory demand for energy-efficient buildings is a major driver for the global cladding system market, fueled by stringent building codes and sustainability standards worldwide

- Cladding systems enhance energy efficiency by providing thermal insulation, moisture control, and air and vapor barriers, reducing heat transfer and lowering energy consumption for heating and cooling

- The growing construction industry, particularly in emerging economies, drives demand for cladding systems that offer both functional protection and aesthetic appeal to meet modern architectural preferences

- Government initiatives, such as the European Union’s energy efficiency targets and housing programs such as Brazil’s Casa Verde e Amarela, are boosting the adoption of cladding systems

- The rise in urbanization and infrastructure development, especially in Asia-Pacific countries such as China and India, further accelerates demand for advanced cladding solutions in residential and non-residential projects

Restraint/Challenge

“High Installation Costs and Stringent Safety Regulations”

- The high initial costs of cladding system installation, including materials, labor, and integration, pose a significant barrier, particularly in cost-sensitive emerging markets

- Complex installation processes for advanced cladding types, such as curtain walling or rainscreen systems, can lead to delays and increased expenses, deterring adoption in some regions

- Stringent fire safety regulations, driven by high-profile incidents such as cladding-related fires, require manufacturers to comply with rigorous standards, increasing production and compliance costs

- Volatility in raw material prices, such as metals, wood, and polymers, impacts profitability and can limit market growth, especially for smaller manufacturers

- Concerns over maintenance and durability, particularly for materials such as wood that require regular upkeep, and the complexity of repairing systems such as metal cladding, further challenge market expansion

Cladding System market Scope

The market is segmented on the basis of material, component, function, type of cladding, and application

- By Material

On the basis of material, the global cladding system market is segmented into ceramic, wood, stucco and EIFS, brick and stone, metal, vinyl, fiber cement, and others. The ceramic segment dominated the largest market revenue share of 32% in 2024, driven by its durability, low maintenance, and aesthetic appeal, making it a preferred choice for both residential and commercial applications. Ceramic cladding is widely used for tile cladding in various settings, including bathrooms, kitchens, and public buildings, due to its resistance to pollutants and weather conditions.

The fiber cement segment is expected to witness the fastest growth rate from 2025 to 2032, with a projected CAGR of 7.8%. This growth is fueled by its cost-effectiveness, high durability, and ability to withstand high-pressure winds and rainwater, making it ideal for sustainable and low-maintenance cladding solutions in residential and non-residential construction.

- By Component

On the basis of component, the global cladding system market is segmented into roof, walls, windows and doors, and others. The wall segment dominated the market with a revenue share of 42.3% in 2024, attributed to its extensive surface area in buildings and its dual role in providing protection against environmental elements and enhancing aesthetic appeal. Wall cladding is critical for energy efficiency and structural durability, particularly in regions with extreme weather conditions.

The roof segment is anticipated to experience the fastest growth rate from 2025 to 2032, driven by the increasing adoption of metal and fiber cement roofing solutions in commercial and industrial buildings. These materials offer superior weather resistance and insulation, contributing to energy savings and building longevity.

- By Function

On the basis of function, the global cladding system market is segmented into insulation, air and vapor control, precipitation control, movement joints and crack control, and others. The insulation segment held the largest market revenue share of 38% in 2024, driven by stringent building codes and green building standards mandating energy-efficient solutions. Insulation-focused cladding systems, such as rainscreen assemblies and insulated metal panels, are increasingly adopted to reduce energy consumption and enhance building performance.

The precipitation control segment is expected to witness significant growth from 2025 to 2032, as cladding systems designed to protect against rain, snow, and moisture gain traction in regions prone to harsh weather. These systems prevent structural deterioration and mold growth, ensuring long-term durability.

- By Type of Cladding

依覆層類型,全球覆層系統市場細分為帷幕牆、夾芯板、專利玻璃、雨幕、金屬型材覆層、磚塊、磁磚掛片等。 2024年,帷幕牆市場收入份額最高,達到30%,這得益於其美觀、輕質以及隔熱隔音性能,在商業建築中廣泛應用。

預計2025年至2032年期間,雨幕市場將以最快的速度成長,這得益於其在現代建築設計中管理濕度和提高能源效率的能力。雨幕因其多功能性和可持續性,在城市地區越來越受歡迎。

- 按應用

根據應用領域,全球帷幕牆系統市場可分為住宅帷幕牆系統市場和非住宅帷幕牆系統市場。住宅帷幕牆系統市場佔據主導地位,2024年的收入份額為43.7%,這得益於住宅市場對節能美觀的幕牆系統解決方案的需求不斷增長。對永續建築實踐的關注以及政府推廣綠建築的舉措進一步推動了這一領域的發展。

預計非住宅建築領域在2025年至2032年間將實現8.2%的最快成長率,這得益於商業、工業和機構建築建設的增加。非住宅建築中的覆層系統可增強耐候性、防火性和視覺吸引力,尤其是在辦公空間、購物中心和公共設施中。

覆層系統市場區域分析

- 北美在覆層系統市場佔據主導地位,2024 年其收入份額最大,為 38.5%,這得益於強勁的建築活動、先進建築材料的廣泛採用以及主要行業參與者的存在

- 消費者優先考慮覆層系統的隔熱性、耐候性和增強建築美觀性,尤其是在氣候條件多樣的地區

- 陶瓷、纖維水泥和金屬等覆層材料的進步以及住宅和非住宅應用的日益普及推動了成長

美國覆層系統市場洞察

受住宅和商業建築領域強勁需求的推動,美國覆層系統市場在2024年佔據北美地區最大的收入份額,達75.7%。消費者對能源效率和永續建築實踐的意識日益增強,推動了乙烯基和纖維水泥等先進覆層材料的採用。嚴格的建築規範和現代建築設計的潮流進一步推動了市場擴張。

歐洲覆層系統市場洞察

預計歐洲覆層系統市場將迎來顯著成長,這得益於監管部門對節能建築和永續建築實踐的重視。消費者更青睞具有隔熱、降水控制和美觀功能的覆層系統。由於城市發展不斷推進以及環境法規的出台,例如德國和法國,綠色建築解決方案的採用率顯著提升。

英國覆層系統市場洞察

英國建築外牆系統市場預計將經歷快速成長,這主要得益於城市和郊區對節能環保且美觀的建築外牆的需求。人們對隔熱效益的認識不斷提高,並嚴格遵守建築安全法規,這促進了建築外牆系統的採用。磚片和金屬型材外牆等材料的使用在新建和改造工程中都越來越受到青睞。

德國覆層系統市場洞察

由於德國先進的建築業和對能源效率的高度重視,德國預計將迎來其覆層系統市場的強勁成長。德國消費者青睞陶瓷和纖維水泥等高性能覆層材料,這些材料能夠降低能耗並增強建築耐久性。高端住宅和商業項目中覆層系統的整合將支持市場的持續成長。

亞太地區覆層系統市場洞察

預計亞太地區將迎來最快的成長速度,這得益於中國、印度和日本等國家快速的城市化進程、建築活動的擴張以及可支配收入的提高。對可持續且美觀的建築解決方案的需求不斷增長,推動了覆層系統的採用。政府推動能源效率和綠建築的措施進一步加速了市場的成長。

日本覆層系統市場洞察

日本的外牆系統市場預計將經歷快速成長,這得益於消費者對高品質、耐用且能夠提升建築安全性和美觀度的外牆材料的強烈偏好。大型建築公司的入駐以及先進外牆系統在住宅和非住宅項目中的集成,推動了市場滲透率的提升。人們對永續建築的興趣日益濃厚,也促進了市場的成長。

中國帷幕牆系統市場洞察

中國佔據亞太地區建築覆層系統市場的最大份額,這得益於快速城鎮化、不斷增長的建築項目以及對節能建築解決方案日益增長的需求。中國不斷壯大的中產階級和對永續城市發展的重視,推動了金屬和乙烯基等先進覆層材料的採用。強大的國內製造能力和極具競爭力的價格增強了市場准入。

覆層系統市佔率

覆層系統產業主要由知名公司主導,包括:

- Kingspan集團(愛爾蘭)

- 聖戈班(法國)

- Carea 立面(倫敦)

- MF Murray Companies, Inc.(美國)

- CGL外牆(英國)

- Rockwool A/S(丹麥)

- 巴斯夫公司(德國)

- Sto SE & Co KGaA(德國)

- Dryvit(美國)

- ParexGroup LTD(法國)

- Terraco Holdings Ltd(英國)

- Etex集團(比利時)

- FunderMax(奧地利)

- Euramax 包層(荷蘭)

- Cupa Pizarras(美國)

- Danpal(法國)

全球覆層系統市場的最新發展是什麼?

- 2025年5月,Kingspan集團和Etex集團透過策略性收購和創新產品發布,持續推動覆層和建築材料市場的成長。兩家公司均強調其產品系列的永續性、能源效率和高效能解決方案。 Kingspan推進了其「Completing the Envelope」(完善建築圍護結構)策略,專注於低碳建築圍護結構;而Etex則擴展了其輕質建築產品組合,鞏固了其在全球市場的地位。這些持續的努力反映了產業對綠色建築解決方案和韌性基礎設施的廣泛趨勢,兩家公司在塑造永續建築的未來方面都發揮著關鍵作用。

- 2024年7月,隨著奈米技術驅動的自清潔外牆技術的推出,外牆裝飾產業迎來了一項重大創新。這些先進的塗層通常以二氧化鈦 (TiO₂) 和氧化鋅 (ZnO) 為基礎,利用光催化和親水特性分解有機污染物,並利用雨水沖刷污垢,從而減少人工清潔的需求。這些解決方案可透過噴塗或浸塗的方式應用,增強建築外牆的耐用性、美觀性和永續性。這一發展滿足了現代和歷史建築對低維護、持久耐用材料日益增長的需求。

- 2024年6月,Sotech Optima推出了其Optima FC+雨幕牆系統的突破性變體-Optima Meadow,這是一款與Vertical Meadow合作開發的全整合式「綠牆」解決方案。這款創新系統採用鉸鍊式穿孔前面板,可插入種子膜,使植物能夠直接在外牆上生長。該解決方案以乾燥狀態交付至現場,並透過整合灌溉、Wi-Fi和電力系統激活,從而支援城市生物多樣性,減少碳足跡並簡化維護。此次發布反映了牆體和建築行業日益增長的可持續親生物設計趨勢。

- In January 2023, Aquarian Cladding, a UK-based specialist in brick façade systems, launched Gebrik Modular, a factory-produced, panelized cladding solution tailored for the modular housing market. Designed for buildings under 11 meters, Gebrik Modular consists of lightweight, non-load-bearing insulated panels that are quick to install and compatible with most common substrates. With over 700 clay brick finishes available, the system offers both aesthetic flexibility and thermal efficiency, enabling faster construction timelines and reduced reliance on traditional bricklaying labor. This launch addresses key industry challenges such as labour shortages, weather dependency, and the need for offsite construction efficiency

- In March 2022, Mitrex, a Canadian solar technology innovator, launched Solar Brick, a groundbreaking building-integrated photovoltaic (BIPV) solution that transforms traditional brick facades into renewable energy-generating surfaces. Designed to mimic the appearance of classic masonry, Solar Brick panels integrate monocrystalline solar cells capable of generating up to 330W per panel, all while maintaining architectural aesthetics. The product is ideal for both new construction and retrofits, offering a seamless blend of design, durability, and sustainability. This launch underscores Mitrex’s mission to revolutionize the cladding sector by embedding solar functionality into everyday building materials

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。