Global Drilling Fluid Additives Market

市场规模(十亿美元)

CAGR :

%

USD

1.60 Billion

USD

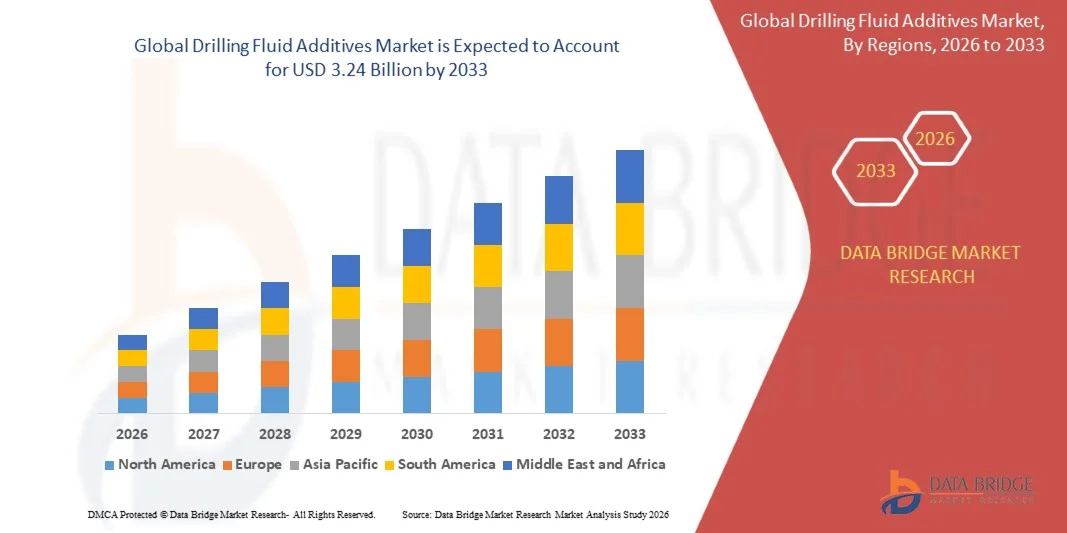

3.24 Billion

2025

2033

USD

1.60 Billion

USD

3.24 Billion

2025

2033

| 2026 –2033 | |

| USD 1.60 Billion | |

| USD 3.24 Billion | |

| % | |

|

全球鑽井液添加劑市場細分,按類型(表面改質劑、分散劑、緩蝕劑、增稠劑、殺菌劑、消泡劑及其他)、流體形成(合成基、水基和油基)劃分-產業趨勢及至2033年的預測

鑽井液添加劑市場規模

- 2025年全球鑽井液添加劑市場規模為16億美元,預計2033年將達32.4億美元,預測期間內 複合年增長率為9.20%。

- 市場成長主要得益於陸上和海上油氣勘探與生產活動的增加,從而推動了對高性能鑽井液和先進添加劑解決方案的需求。

- 此外,隨著技術先進的鑽井方法和高性能鑽井液配方(例如緩蝕劑、增稠劑和降濾失劑)的日益普及,鑽井液添加劑正成為現代鑽井作業的關鍵組成部分。這些因素共同推動了專用添加劑的廣泛應用,從而顯著促進了行業的成長。

鑽井液添加劑市場分析

- 鑽井液添加劑,包括表面改質劑、分散劑、緩蝕劑和增稠劑,在維持井眼穩定性、優化鑽井效率以及防止設備在嚴苛的油藏和環境條件下腐蝕方面,發揮著日益重要的作用。

- 鑽井液添加劑需求的不斷增長主要源於複雜深水油藏勘探活動的增加、對作業效率日益重視以及監管機構對環保且可持續的鑽井液解決方案的日益關注。

- 由於先進鑽井技術的日益普及以及該地區勘探和生產活動的不斷增加,北美地區預計將在2025年佔據鑽井液添加劑市場約30%的份額,成為該市場的主導力量。

- 由於中國、印度和澳洲等國的勘探和生產活動不斷增加,預計亞太地區將在預測期內成為鑽井液添加劑市場成長最快的地區。

- 由於其成本效益高、符合環保要求以及在陸上鑽井作業中的廣泛應用,水基鑽井液在2025年佔據了41.7%的市場份額,成為市場主導力量。水基鑽井液因其易於配製、原料易得以及與多種添加劑相容等優點而備受青睞,使作業者能夠高效地優化鑽井性能。此外,監管部門的支持以及對減少環境影響日益增長的關注也推動了該細分市場的強勁需求,使水基鑽井液成為傳統鑽井作業的標準選擇。不斷改進的配方,例如提升潤滑性、熱穩定性和控制失水性能,持續鞏固該細分市場的領先地位。

報告範圍及鑽井液添加劑市場細分

|

屬性 |

鑽井液添加劑市場關鍵洞察 |

|

涵蓋部分 |

|

|

覆蓋國家/地區 |

北美洲

歐洲

亞太

中東和非洲

南美洲

|

|

主要市場參與者 |

|

|

市場機遇 |

|

|

加值資料資訊集 |

除了對市場狀況(如市場價值、成長率、細分、地理覆蓋範圍和主要參與者)的洞察之外,Data Bridge Market Research 精心編制的市場報告還包括進出口分析、產能概覽、生產消費分析、價格趨勢分析、氣候變遷情境、供應鏈分析、價值鏈分析、原材料/消耗標準概覽、供應商選擇、PESTLE 分析、五力分析和監管框架。 |

鑽井液添加劑市場趨勢

“高性能環保添加劑的應用日益廣泛”

- A significant trend in the drilling fluid additives market is the increasing adoption of high-performance and environmentally friendly additives that improve drilling efficiency, maintain wellbore stability, and reduce environmental impact. Operators are seeking fluid formulations that can withstand extreme temperatures and pressures while minimizing ecological footprint, making advanced additives essential for modern drilling projects

- For instance, Halliburton’s BaraXtreme water-based drilling fluid system incorporates advanced fluid loss control and high-performance additives designed to enhance hydraulic efficiency in challenging sandstone and shale formations. Such solutions are strengthening operational reliability and reducing downtime in complex drilling environments

- The use of biodegradable and low-toxicity additives is growing rapidly as companies strive to comply with stringent environmental regulations in regions such as North America and Europe. This is positioning eco-friendly additives as critical components in deepwater and onshore drilling projects where sustainability requirements are increasingly enforced

- Exploration in unconventional reservoirs, such as shale and tight gas formations, is boosting demand for multi-functional additives that provide improved rheology, cuttings transport, and shale inhibition. The rising integration of advanced chemical formulations into drilling fluids is improving performance under high-pressure, high-temperature conditions and enhancing overall wellbore stability

- Energy companies are increasingly investing in research and development to formulate additives that can reduce operational risks and enhance recovery rates. This trend is accelerating innovation in fluid chemistry, driving a stronger preference for additives capable of optimizing drilling performance while maintaining environmental compliance

- The market is witnessing strong growth in regions such as the U.S., Brazil, and the North Sea where high-performance drilling operations require specialized additives to meet operational and regulatory demands. The incorporation of these advanced additives is reinforcing the transition toward more efficient, sustainable, and safe drilling operations across the globe

Drilling Fluid Additives Market Dynamics

Driver

“Rising Exploration and Production Activities in Onshore and Offshore Oil & Gas”

- The growing demand for drilling fluid additives is primarily driven by the expansion of onshore and offshore oil and gas exploration and production activities. Companies are increasingly relying on additives to maintain wellbore stability, prevent corrosion, and optimize drilling efficiency in complex reservoirs

- For instance, SLB (Schlumberger) has supplied advanced drilling fluid systems and additives for Shell’s offshore deepwater projects, enhancing operational reliability and wellbore safety. Such deployments highlight the critical role of additives in enabling complex drilling operations and improving recovery rates

- The rising focus on deepwater and unconventional drilling operations in regions such as the Gulf of Mexico, Brazil, and West Africa is boosting the adoption of specialized fluid additives. These additives are essential to address the challenges posed by high pressures, extreme temperatures, and chemically reactive formations

- Energy companies are increasingly investing in technologically advanced additives that provide multi-functional benefits, such as improved rheology, fluid loss control, and shale stabilization. This is reinforcing the adoption of high-performance fluid systems capable of reducing operational risks and enhancing efficiency

- The expanding global energy landscape, with new wells being drilled across diverse environments, continues to strengthen this driver. The increasing need for reliable, high-performance, and environmentally compliant additives is propelling adoption across onshore, offshore, and unconventional drilling projects

Restraint/Challenge

“High Cost and Complexity of Advanced Drilling Fluid Formulations”

- The drilling fluid additives market faces challenges due to the high cost and technical complexity involved in developing advanced fluid formulations. Producing multi-functional additives that meet performance requirements under extreme conditions requires significant investment in research, testing, and specialized equipment

- For instance, companies such as Baker Hughes invest in high-precision chemical development and laboratory testing to create biodegradable, high-performance additives. These rigorous processes increase production costs and extend product development timelines, limiting price flexibility in the market

- The complexity of blending additives to provide corrosion inhibition, fluid loss control, and rheological stability in a single formulation adds operational and manufacturing challenges. Maintaining consistent quality across diverse reservoir conditions further complicates production and application processes

- The reliance on specialized raw materials, such as proprietary polymers and surfactants, increases supply-chain vulnerability and can contribute to price volatility. Manufacturers must balance performance, regulatory compliance, and cost efficiency while meeting growing demand

- Scaling up high-performance additive production while maintaining reliability, environmental compliance, and competitive pricing continues to be a key constraint. These challenges collectively place pressure on manufacturers to innovate efficiently and optimize operational and production processes to sustain market growth

Drilling Fluid Additives Market Scope

The market is segmented on the basis of type and fluid formation.

• By Type

On the basis of type, the drilling fluid additives market is segmented into surface modifiers, dispersants, corrosion inhibitors, fluid viscosifiers, biocides, defoamers, and others. The corrosion inhibitors segment dominated the market with the largest revenue share in 2025, driven by their critical role in protecting drilling equipment and pipelines from rust and chemical degradation during drilling operations. Operators increasingly prioritize corrosion inhibitors to ensure operational efficiency, reduce downtime, and extend the life of expensive drilling machinery. The segment also benefits from advancements in environmentally friendly formulations that meet regulatory standards, enhancing their adoption in offshore and onshore drilling projects. Strong compatibility with various drilling fluid systems further contributes to their widespread use, making corrosion inhibitors a staple in modern drilling operations.

The fluid viscosifiers segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by rising demand for stable drilling operations under extreme temperature and pressure conditions. For instance, companies such as M-I SWACO are developing advanced viscosifiers that enhance the rheological properties of drilling fluids, allowing for better cuttings suspension and transport. Increasing offshore exploration and deepwater drilling activities are driving the need for additives that maintain consistent fluid viscosity, ensuring wellbore stability. The ability of modern viscosifiers to reduce fluid loss and improve drilling efficiency further accelerates market growth. In addition, their integration with multi-functional drilling fluids provides operational benefits, making fluid viscosifiers highly sought after in new drilling projects.

• By Fluid Formation

On the basis of fluid formation, the drilling fluid additives market is segmented into synthetic-based, water-based, and oil-based fluids. The water-based segment dominated the market with the largest revenue share of 41.7% in 2025, driven by its cost-effectiveness, environmental compliance, and widespread use across onshore drilling operations. Water-based drilling fluids are preferred for their ease of preparation, availability of raw materials, and compatibility with a broad range of additives, allowing operators to optimize drilling performance efficiently. The segment also sees strong demand due to regulatory support and the growing focus on reducing environmental impact, making water-based fluids a standard choice in conventional drilling activities. Enhanced formulations that improve lubricity, thermal stability, and fluid loss control continue to strengthen the segment’s market position.

The synthetic-based segment is expected to witness the fastest CAGR from 2026 to 2033, fueled by its superior performance in extreme drilling conditions and deepwater operations. For instance, companies such as Halliburton are expanding their synthetic-based additive portfolios to enhance drilling efficiency while minimizing environmental impact. Synthetic fluids provide better thermal stability, reduced toxicity, and improved shale inhibition compared to traditional water-based fluids, driving adoption in complex drilling projects. Rising investments in offshore and unconventional resource exploration increase demand for high-performance drilling fluids. In addition, the growing need for customized fluid solutions tailored to challenging reservoir conditions further accelerates the adoption of synthetic-based formations.

Drilling Fluid Additives Market Regional Analysis

- North America dominated the drilling fluid additives market with the largest revenue share of around 30% in 2025, driven by the growing adoption of advanced drilling technologies and increasing exploration and production activities in the region

- Oil and gas operators in North America prioritize high-performance additives that enhance drilling efficiency, reduce equipment wear, and provide effective corrosion and fluid loss control in both onshore and offshore operations

- This widespread adoption is further supported by well-established oilfield infrastructure, technological expertise, and stringent regulatory standards, establishing drilling fluid additives as a critical component in modern drilling operations

U.S. Drilling Fluid Additives Market Insight

The U.S. drilling fluid additives market captured the largest revenue share in 2025 within North America, fueled by high exploration activity and extensive shale development initiatives. Operators are increasingly focusing on additives that improve wellbore stability, reduce operational downtime, and meet environmental regulations. The adoption of high-performance synthetic and water-based additives, alongside growing investments in unconventional resource extraction, is driving market growth. Moreover, increasing technological integration for real-time monitoring of drilling fluids enhances operational efficiency and promotes the use of advanced additives.

Europe Drilling Fluid Additives Market Insight

預計在預測期內,歐洲鑽井液添加劑市場將以顯著的複合年增長率成長,主要驅動力來自日益嚴格的環境和營運法規以及對高性能鑽井解決方案的需求。挪威和荷蘭等國的近海勘探活動不斷增加,推動了腐蝕抑制劑、增稠劑和特殊添加劑的應用。歐洲營運商也非常重視環保配方和先進的流體系統,以優化鑽井效率並減少對環境的影響。此外,發達的油氣基礎設施和流體管理系統方面的技術專長也為市場發展提供了強力支撐。

英國鑽井液添加劑市場洞察

受北海海上勘探活動和先進流體技術應用的推動,英國鑽井液添加劑市場預計在預測期內將以顯著的複合年增長率成長。營運商越來越多地使用添加劑來確保井眼穩定性、防止腐蝕並提高複雜環境下的鑽井效率。英國對監管合規、安全和永續營運的重視,正在推動對符合環保標準的鑽井液和添加劑的需求。此外,專業服務提供者和鑽井化學領域的研究措施預計也將促進市場擴張。

德國鑽井液添加劑市場洞察

受陸上和海上油氣勘探活動日益活躍以及對可持續鑽井實踐日益重視的推動,德國鑽井液添加劑市場預計在預測期內將以顯著的複合年增長率增長。德國先進的技術基礎設施和嚴格的環境法規促進了高性能環保添加劑的使用。營運商正加大對能夠提高效率、降低作業風險並最大限度減少環境影響的流體系統的投資。此外,與服務提供者和添加劑製造商的合作也有助於開發和應用針對複雜鑽井條件的客製化流體解決方案。

亞太地區鑽井液添加劑市場洞察

亞太地區鑽井液添加劑市場預計將在2026年至2033年的預測期內以最快的複合年增長率成長,這主要得益於中國、印度和澳洲等國家勘探和生產活動的不斷增加。城市化、工業化進程的加速以及能源需求的增加,正在推動陸上和海上鑽井計畫的投資。該地區對先進鑽井技術和高性能添加劑的日益普及,確保了在嚴苛的油藏條件下也能高效作業。此外,亞太地區作為鑽井液和添加劑製造中心的地位日益凸顯,提高了產品的供應能力並降低了成本,從而擴大了當地營運商的採購管道。

日本鑽井液添加劑市場洞察

由於海上勘探活動的蓬勃發展、技術的進步以及對作業效率的重視,日本鑽井液添加劑市場正呈現成長動能。營運商越來越多地採用能夠為深水和複雜油藏提供卓越熱穩定性、防腐蝕保護和流體損失控制的添加劑。日本對永續和環保作業的重視也促進了合成和水基鑽井液添加劑的應用。此外,將即時監測系統與鑽井液管理系統結合,也提高了添加劑在整個鑽井作業中的性能和可靠性。

中國鑽井液添加劑市場洞察

預計到2025年,中國鑽井液添加劑市場將佔據亞太地區最大的市場份額,主要得益於中國不斷增長的油氣產量、快速的工業化進程以及技術應用。高性能添加劑在陸上和海上工程中被廣泛用於優化鑽井效率、防止腐蝕並維持井眼穩定性。政府支持能源基礎建設的舉措,以及國內強大的添加劑製造基礎,是推動市場成長的關鍵因素。此外,高性價比添加劑的供應以及非常規油氣資源勘探的不斷深入,進一步鞏固了中國在亞太地區領先市場的地位。

鑽井液添加劑市場份額

鑽井液添加劑產業主要由一些老牌企業主導,其中包括:

- 阿克蘇諾貝爾公司(荷蘭)

- 巴斯夫股份公司(德國)

- 雪佛龍菲利普斯化學公司(美國)

- 陶氏公司(美國)

- Innospec Inc.(美國)

- Tetra Technologies, Inc.(美國)

- 哈里伯頓公司(美國)

- 斯倫貝謝有限公司(法國)

- 貝克休斯公司(美國)

- Newpark Resources Inc.(美國)

- 美國國民油井華高公司(National Oilwell Varco, Inc.)

- 威德福國際有限公司(瑞士)

- 科萊恩股份公司(瑞士)

- 科萊達國際有限公司(英國)

- 路博潤公司(美國)

全球鑽井液添加劑市場最新發展動態

- 2025年9月,Newpark Fluids Systems與Intelligent Mud Solutions (IMS)達成策略合作,將即時鑽井液測量與分析技術整合到鑽井作業中。此舉將增強作業者持續監測流體行為、優化鑽井性能並最大限度減少非生產時間的能力。將自主監測技術與先進的流體添加劑結合,可望推動高性能鑽井液在北美和其他成熟市場得到更廣泛的應用,從而提高效率、降低作業風險,並凸顯數據驅動的流體管理在複雜鑽井環境中的重要性。

- 2025年1月,哈里伯頓公司獲得多年期合同,將為巴西的深水井和勘探井供應其先進的鑽井液系統和降濾失添加劑。這鞏固了哈里伯頓在海上市場的地位,並凸顯了市場對能夠在極端條件下維持井筒穩定性的高性能添加劑日益增長的需求。該合約強調了添加劑在減少鑽井複雜性、優化作業和支援大規模海上勘探方面的戰略作用,也顯示市場對技術先進的流體解決方案的依賴性日益增強。

- 2025年,貝克休斯透過收購一家專注於可生物降解鑽井液添加劑的特種化學品製造商,擴展了其鑽井液添加劑產品組合。此舉顯著提升了公司提供環保鑽井解決方案的能力,以滿足面臨日益嚴格監管要求的營運商的需求。這項進展可望加速全球市場對永續添加劑的採用,推動鑽井液添加劑產業中註重環保的細分市場成長,同時提升營運效率與環境安全。

- 2024年9月,SCF Partners, Inc.完成了對Newpark Fluids Systems流體業務部門的收購,從而增強了其鑽井液和完井液的產品和服務。此次擴張使SCF能夠針對不同的油藏條件提供更客製化的解決方案,鞏固其在北美的競爭地位。此次收購預計將促進添加劑配方方面的創新,擴大市場覆蓋範圍,並推動高性能鑽井液在陸上和海上作業的應用。

- 2024年8月,AES鑽井液公司收購了HydroLite Operating LLC,拓展了其在鑽井和清井流體系統方面的能力。此次收購增強了AES的市場地位,並使其能夠利用專用添加劑服務於更廣泛的油藏條件。這項進展有望提升對先進流體解決方案的需求,這些解決方案能夠增強井眼穩定性、優化鑽井效率並減少作業停機時間,凸顯了流體添加劑在現代鑽井專案中的關鍵作用。

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。