Global Medical Nonwoven Disposables Market

市场规模(十亿美元)

CAGR :

%

USD

10.59 Billion

USD

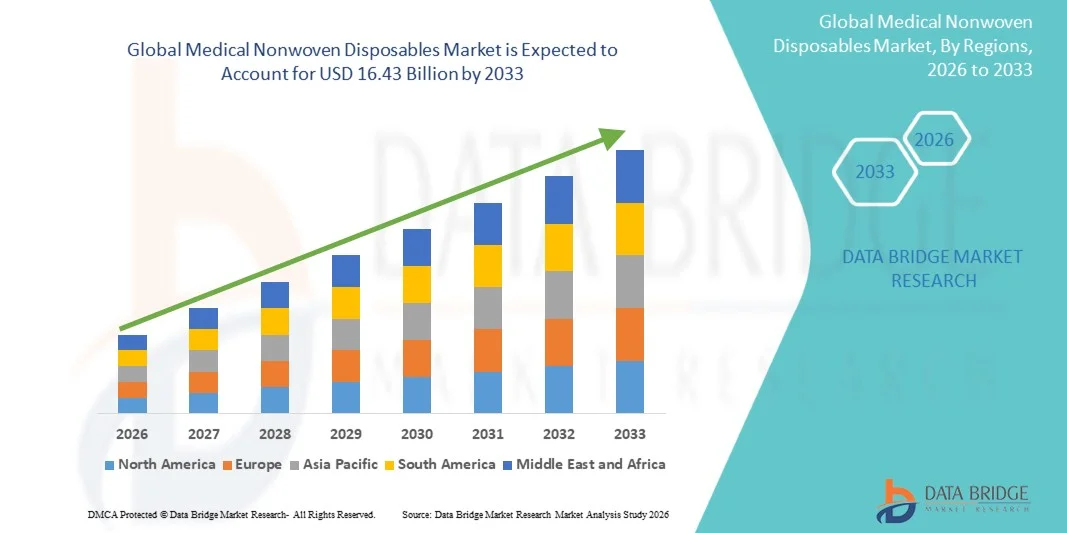

16.43 Billion

2025

2033

USD

10.59 Billion

USD

16.43 Billion

2025

2033

| 2026 –2033 | |

| USD 10.59 Billion | |

| USD 16.43 Billion | |

| % | |

|

全球醫用無紡布一次性用品市場細分,按產品(失禁用品和外科產品)、分銷管道(醫院藥房、零售藥房和其他分銷管道)劃分-行業趨勢及至2033年的預測

醫用不織布一次性用品市場規模

- 2025年全球醫用無紡布一次性用品市場規模為105.9億美元 ,預計 2033年將達164.3億美元,預測期內 複合年增長率為5.63%。

- 市場成長主要受醫療機構對感染預防和衛生管理需求不斷增長的推動,而手術量、住院人數的增加以及患者安全監管標準的日益嚴格,都促使發達和新興醫療體系廣泛採用醫用無紡布一次性產品。

- 此外,人們對交叉感染風險的認識不斷提高,以及對一次性防護醫療產品(如防護服、口罩、手術鋪巾和濕巾)的需求日益增長,使得醫用無紡布一次性用品成為必不可少的醫療耗材。這些因素共同推動了醫用不織布一次性用品解決方案的普及,從而顯著促進了該行業的成長。

醫用不織布一次性用品市場分析

- 醫用無紡布一次性用品,包括外科口罩、手術服、手術鋪巾和滅菌包裝,因其高阻隔性、成本效益和一次性使用的便利性,能夠降低污染風險,因此在醫院、門診手術中心和診斷機構的現代感染控制方案中日益成為不可或缺的組成部分。

- 醫用不織布一次性用品需求的不斷增長,主要受以下因素推動:手術量增加、人們對醫院感染(HAI)的認識不斷提高、醫療基礎設施不斷擴建,以及已開發國家和新興醫療體系對一次性防護醫療產品的偏好日益增強。

- 預計到2025年,北美將以36.8%的最大市佔率主導醫用不織布一次性用品市場。北美地區擁有先進的醫療基礎設施、高額的醫療支出、嚴格的感染預防監管標準以及眾多大型醫療耗材製造商。其中,美國醫院和門診手術機構的需求成長尤其顯著。

- 預計在預測期內,亞太地區將成為醫用不織布一次性用品市場成長最快的地區,複合年增長率將達到8.9%。這主要得益於醫院網路的擴張、醫療保健投資的增加、患者數量的增長以及中國、印度和東南亞等國家衛生和感染控制意識的提高。

- 外科產品細分市場佔據市場主導地位,預計到2025年將佔據58.6%的最大收入份額,這主要得益於全球外科手術數量的持續增長以及醫療機構實施的嚴格感染防控措施。

報告範圍及醫用無紡布一次性用品市場細分

|

屬性 |

醫用不織布一次性用品市場關鍵洞察 |

|

涵蓋部分 |

|

|

覆蓋國家/地區 |

北美洲

歐洲

亞太

中東和非洲

南美洲

|

|

主要市場參與者 |

|

|

市場機遇 |

|

|

加值資料資訊集 |

除了對市場價值、成長率、細分、地理覆蓋範圍和主要參與者等市場狀況的洞察之外,Data Bridge Market Research 精心編制的市場報告還包括深入的專家分析、病患流行病學、研發管線分析、定價分析和監管框架。 |

醫用不織布一次性用品市場趨勢

“日益重視感染預防和一次性衛生用品”

- 全球醫用不織布一次性用品市場的一個顯著且加速發展的趨勢是,醫療機構越來越重視感染預防、衛生合規性以及一次性防護產品的廣泛應用。

- 醫院和診所正越來越多地轉向使用一次性不織布材料,以最大限度地降低交叉感染和醫院獲得性感染(HAI)的風險。

- 例如,手術室和重症監護室廣泛使用一次性手術服、手術鋪巾、口罩、手術帽和鞋套已成為標準臨床實踐,確保了更高的無菌水平並提高了患者安全性。

- 紡粘、熔噴和SMS(紡粘-熔噴-紡粘)非織造布製造技術的不斷進步,使得輕便、透氣且防護性能優異的醫用一次性用品得以開發,這些用品在保持強大防護屏障的同時,也提高了醫護人員的舒適度。

- 此外,醫療機構正越來越多地採用高性能抗菌和防液體滲透的非織造材料,以滿足已開發市場和新興市場日益嚴格的感染控制指南和監管標準。

- 全球對疫情防範、防護物資緊急儲備和加強醫院衛生規程的日益重視,進一步加速了醫用不織布一次性產品的普及應用。

- 因此,製造商正在擴大產能,並推出創新的可生物降解和可持續的非織造材料,以滿足全球對安全、衛生和環保一次性醫療產品日益增長的需求。

醫用不織布一次性用品市場動態

司機

“增加外科手術量和擴大醫療基礎設施”

- 全球外科手術數量的不斷增加,是慢性病日益普遍、人口老化以及醫療保健服務覆蓋範圍擴大所驅動的,也是醫用不織布一次性用品需求的主要驅動因素。

- 例如,新興經濟體中醫院、門診手術中心和專科診所的快速擴張,導致一次性手術鋪巾、手術衣、消毒包裝和傷口護理產品的消耗量增加。

- 隨著醫療機構不斷將感染預防和營運效率放在首位,拋棄式不織布產品透過減少消毒需求和提高臨床環境中的工作流程效率,提供了經濟高效的解決方案。

- 此外,政府對醫療現代化、醫療支出增加以及公共衛生體系的加強,都顯著促進了全球醫用不織布一次性用品市場的穩定成長。

克制/挑戰

“環境問題與廢棄物管理挑戰”

- 一次性無紡布產品產生的醫療廢棄物量不斷增長,由此引發的環境問題對市場成長構成了重大挑戰。一次性防護設備和手術耗材的大規模使用加重了全球醫療廢棄物管理系統的負擔。

- 例如,世界衛生組織2024年的報告指出,印度和巴西的醫院每年產生超過50萬噸的一次性無紡布醫療廢物,這給妥善分類、處理和處置這些廢物帶來了巨大挑戰。

- 此外,傳統非織造布生產對石油基原料的依賴,引發了監管機構、醫療保健機構和環保組織的可持續性擔憂。

- 透過開發可生物降解的非織造材料、推行回收計劃以及改進醫療廢物處理基礎設施來應對這些挑戰,對於確保醫用非織造一次性用品市場的可持續長期增長至關重要。

醫用不織布一次性用品市場範圍

市場按產品和分銷管道細分。

• 副產品

依產品類型,全球醫用無紡布一次性用品市場可分為失禁用品和外科用品。外科用品細分市場佔據主導地位,預計到2025年將佔據58.6%的最大市場份額,這主要得益於全球外科手術數量的持續增長以及醫療機構實施的嚴格感染防控措施。醫院和門診手術中心越來越依賴一次性不織布手術鋪巾、手術衣、口罩和滅菌包裝來維持無菌環境並減少醫院獲得性感染(HAI)。新興經濟體醫療基礎設施的擴張以及微創手術的日益普及進一步支撐了對外科不織布一次性用品的持續需求。此外,監管機構要求手術室使用一次性無菌防護設備,也大大促進了該細分市場的強勁發展。透氣性、防液體滲透性和抗菌性不織布材料的技術進步也在提升產品的性能和安全性,促使醫療機構從可重複使用的紡織品轉向一次性替代品。新冠疫情強化了機構長期採購策略,即維持外科防護產品的緊急儲備,這在後疫情時代依然鞏固了該領域的領先地位。門診手術量的增加和全球專科診所的擴張也持續推動產品的穩定消費。隨著人口老化和慢性病盛行率上升,手術量持續成長,預計外科產品領域將在整個預測期內保持其市場領先地位。

The incontinence products segment is anticipated to witness the fastest CAGR of 7.9% from 2026 to 2033, supported by the rapidly expanding geriatric population and increasing awareness regarding personal hygiene and long-term care management. Rising life expectancy across both developed and developing countries has significantly increased the number of individuals experiencing urinary and fecal incontinence conditions, thereby driving sustained demand for disposable incontinence pads, underpads, and protective garments. Growth is further supported by increasing adoption of home healthcare services and assisted living facilities, where disposable hygiene solutions are preferred due to convenience and infection control advantages. Product innovations such as ultra-thin absorbent cores, skin-friendly breathable fabrics, and odor-control technologies are enhancing user comfort and encouraging higher adoption rates. In addition, rising healthcare expenditure and improved insurance coverage for long-term care products in several regions are expanding patient access to incontinence supplies. Growing awareness campaigns and reduced social stigma associated with incontinence management are also contributing to market expansion. The increasing availability of premium adult diaper products through retail pharmacies and online channels is further accelerating segment growth. As the global elderly population continues to grow substantially over the coming decades, the incontinence products segment is expected to emerge as one of the most dynamic revenue contributors in the overall medical nonwoven disposables market.

• By Distribution Channel

On the basis of distribution channel, the Global Medical Nonwoven Disposables market is segmented into Hospital Pharmacies, Retail Pharmacies, and Other Distribution Channels. The hospital pharmacies segment held the largest market revenue share of 49.3% in 2025, driven by the high-volume procurement of surgical gowns, drapes, masks, and other disposable protective products directly by hospitals and large healthcare institutions. Centralized purchasing systems within hospitals enable bulk procurement contracts with manufacturers and distributors, ensuring continuous supply for routine medical procedures and emergency preparedness. The increasing number of hospital admissions, surgical procedures, and infection-control regulations requiring single-use protective materials are major factors supporting segment dominance. Hospitals also maintain long-term supply agreements with medical disposable manufacturers to stabilize pricing and ensure quality compliance, further strengthening the importance of this distribution channel. Growth in multispecialty hospitals, expansion of public healthcare systems in emerging markets, and increasing government healthcare spending continue to boost hospital-based procurement. Furthermore, institutional purchasing departments prioritize certified, high-performance nonwoven products that meet stringent regulatory standards, which drives consistent demand through hospital pharmacy channels. The integration of automated inventory management systems within hospitals also enhances procurement efficiency and replenishment cycles. As surgical volumes and hospital infrastructure continue expanding globally, hospital pharmacies are expected to remain the primary distribution channel for medical nonwoven disposables.

The retail pharmacies segment is projected to witness the fastest CAGR of 8.4% from 2026 to 2033, supported by the increasing demand for home-based healthcare products such as disposable masks, wound care products, adult incontinence supplies, and home nursing consumables. The growing trend toward outpatient care and home recovery following surgeries is encouraging patients and caregivers to purchase medical disposables directly from retail pharmacies and online pharmacy platforms. Rising consumer awareness regarding hygiene, infection prevention, and chronic disease management is further strengthening retail demand. The rapid expansion of organized pharmacy chains in developing countries and improved accessibility to healthcare products in semi-urban and rural areas are also contributing to segment growth. In addition, the availability of private-label medical disposable brands at competitive pricing is attracting cost-conscious consumers and increasing sales volumes. The expansion of e-pharmacy services and same-day delivery models is significantly improving convenience for consumers, particularly elderly patients requiring recurring purchases of hygiene products. Increasing physician recommendations for at-home wound care and long-term patient monitoring are also encouraging retail purchases of disposable medical supplies. As healthcare delivery models increasingly shift toward decentralized and home-based care, the retail pharmacies segment is expected to experience robust expansion over the forecast period.

Medical Nonwoven Disposables Market Regional Analysis

- North America dominated the medical nonwoven disposables market with the largest revenue share of 36.8% in 2025, supported by advanced healthcare infrastructure, high healthcare spending, strong regulatory standards for infection prevention, and the presence of major medical consumable manufacturers

- The region is witnessing increasing adoption of disposable surgical gowns, drapes, masks, and sterilization wraps across hospitals, clinics, and ambulatory surgical centers

- Rising awareness of infection prevention, robust healthcare reimbursement frameworks, and continuous product innovations in nonwoven disposables are driving overall market growth

U.S. Medical Nonwoven Disposables Market Insight

The U.S. medical nonwoven disposables market captured a major share of the North American market, driven by high adoption of disposable medical products across hospitals, outpatient surgical facilities, and diagnostic centers. Increasing surgical volumes, growing awareness of hygiene and infection control, and strong regulatory support are key factors supporting demand. Continuous product innovations, such as fluid-resistant gowns, sterilization wraps, and single-use protective covers, are enhancing both patient safety and healthcare provider convenience. The expanding network of hospitals and outpatient surgical centers, coupled with favorable reimbursement policies, is further propelling market growth in the country.

Europe Medical Nonwoven Disposables Market Insight

The Europe medical nonwoven disposables market is projected to expand at a substantial CAGR during the forecast period, driven by stringent infection-control regulations, high surgical volumes, and increasing adoption of disposable protective products in hospitals, clinics, and ambulatory surgical centers. Countries such as Germany, France, and the U.K. are witnessing rising demand for nonwoven surgical gowns, drapes, masks, and sterilization wraps, fueled by regulatory emphasis on hygiene standards, growing hospital capacities, and continuous modernization of healthcare facilities. Increasing awareness of patient safety, combined with the focus on sustainable and eco-friendly nonwoven materials, is further supporting the region’s market expansion.

U.K. Medical Nonwoven Disposables Market Insight

The U.K. medical nonwoven disposables market is anticipated to grow at a noteworthy CAGR due to expanding surgical procedures, high adoption of disposable hygiene products in hospitals and clinics, and growing emphasis on infection prevention and patient safety. Increasing investments in hospital infrastructure and the integration of advanced nonwoven materials with antimicrobial and fluid-resistant properties are driving demand across public and private healthcare sectors.

Germany Medical Nonwoven Disposables Market Insight

Germany medical nonwoven disposables market is expected to expand at a considerable CAGR, supported by its well-developed healthcare infrastructure, strong regulatory framework, and growing adoption of technologically advanced, eco-conscious disposable nonwoven products. Hospitals and specialty care centers are increasingly implementing nonwoven disposables in surgical, diagnostic, and outpatient procedures to enhance hygiene compliance and reduce cross-contamination risks.

Asia-Pacific Medical Nonwoven Disposables Market Insight

亞太市場預計將在2026年至2033年間以8.9%的複合年增長率實現最快增長,這主要得益於醫院網路的擴張、醫療保健投資的增加、患者數量的增長以及人們對衛生和感染控制措施日益增強的意識。中國、印度、日本和東南亞國家等市場正經歷快速的需求成長,這主要歸功於手術量的增加、新醫院和診所的建設,以及公立和私立醫療機構對一次性無紡布產品的廣泛應用。區域製造中心的興起提高了醫用不織布耗材的可負擔性和可近性,從而促進了其在城鄉醫療機構的更廣泛應用。

日本醫用不織布一次性用品市場洞察

日本醫用無紡布一次性用品市場成長的驅動因素包括人口老化、感染控制意識增強以及醫院基礎設施先進。醫院和長期照護機構越來越多地採用一次性手術服、手術鋪面和防護罩,以維持高標準的衛生條件並提高病人安全。

中國醫用不織布一次性用品市場洞察

到2025年,中國醫用不織布一次性用品市場預計將佔據亞太地區最大的市場份額,這主要得益於快速的城市化進程、不斷增長的醫療支出以及醫院網路的擴張。不斷壯大的中產階級、日益增強的感染預防意識以及政府為改善醫療衛生習慣而採取的各項舉措,都推動了對醫用無紡布一次性用品的強勁需求。為滿足不斷增長的市場需求,中國本土生產商正在擴大生產規模,並推出包括防液體滲透和可生物降解材料在內的創新無紡布材料。

醫用不織布一次性用品市場份額

醫用不織布一次性用品產業主要由一些成熟企業主導,其中包括:

- 3M公司(美國)

- 康德樂公司(美國)

- Medline Industries, LP(美國)

- Mölnlycke Health Care AB(瑞典)

- 保羅·哈特曼股份公司(德國)

- 金佰利公司(美國)

- 歐文斯-邁納公司(美國)

- Halyard Health(歐文斯和邁納)(美國)

- 安塞爾有限公司(澳洲)

- 賽默飛世爾科技公司(美國)

- Dynarex公司(美國)

- Steris plc(愛爾蘭)

- Lohmann & Rauscher GmbH & Co. KG(德國)

- Medicom集團(加拿大)

- 勝利醫療股份有限公司(中國)

- 振德醫療股份有限公司 (中國)

- 蘇州康奈爾醫療股份有限公司 (中國)

- Surgichem Pvt. Ltd.(印度)

- Paul Hartmann 有限公司(英國)

- 恆安國際集團有限公司(中國)

全球醫用不織布一次性用品市場最新發展動態

- 2023年7月,貝裡全球推出了SustainaMed系列產品,這是一款用於醫用防護服和口罩的可生物降解無紡布產品線,旨在減少對環境的影響,同時保持臨床性能,以滿足日益增長的對可持續一次性醫療解決方案的需求。該系列產品的目標客戶是那些尋求更環保替代方案,同時又不願降低衛生防護標準的醫院。

- 2024年8月,Manjushree Spntek推出了專為化療服設計的Hightex混合無紡布,該面料在增強對有害藥物和化學品的防護的同時,也能確保醫護人員的舒適度。 Hightex已獲得全球實驗室認證,符合嚴格的ASTM安全標準,從而進一步推動了其在臨床環境中的應用。

- 2024年1月,歐文斯-邁納公司完成了其位於泰國的醫用手術鋪巾生產工廠的擴建,顯著提升了Halyard AERO無紡布一次性產品的產能,以滿足亞太地區日益增長的需求。 *此次擴建旨在增強當地供應的韌性,並縮短醫療機構的交貨週期。

- 2024年2月,3M宣布以約63億美元的價格將其醫療保健業務出售給貝恩資本。這項策略措施影響了其非織造一次性外科產品組合,包括手術服、手術單和其他個人防護裝備,並將重塑全球醫用非織造一次性用品市場的競爭格局。

- 2024年5月,史賽克與美敦力工業公司達成策略合作,共同開發和銷售一系列新型無紡布手術鋪巾和手術服,利用史賽克在手術系統方面的專業知識和美敦力廣泛的分銷網絡,加速該產品在全球醫院的推廣應用。

- 2024年6月,金佰利公司宣布與美敦力公司達成策略合作,共同開發新一代一次性不織布手術服,旨在擴大供應能力並提升感染控制性能。

- 2025年3月,莫爾尼克醫療保健公司推出了一款採用專有無紡布的新一代一次性手術服,該不織布增強了防護性能和穿著舒適度,鞏固了該公司在全球醫用無紡布產品領域的競爭地位。

- 2025年2月,貝裡全球宣布與美敦力工業公司建立策略夥伴關係,共同開發和生產一系列一次性醫用無紡布產品,旨在增強北美和歐洲地區的供應鏈韌性並縮短交貨週期。

- 2025年4月,Intco Medical在全球推出了Syntex合成一次性乳膠手套,旨在為醫療專業人員在醫療操作過程中提供更佳的防護和舒適度。這些手套豐富了全球醫用不織布一次性用品產品線,擴大了醫用不織布個人防護裝備的供應範圍。

- 2025年9月,Lohmann & Rauscher收購了葡萄牙紗布、不織布及其他醫用一次性用品製造商ADA集團49%的股份,從而鞏固了Lohmann & Rauscher在醫用無紡布一次性用品領域的地位。

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。