Global Micro Services In Healthcare Market

市场规模(十亿美元)

CAGR :

%

USD

457.11 Billion

USD

4.35 Billion

2024

2032

USD

457.11 Billion

USD

4.35 Billion

2024

2032

| 2025 –2032 | |

| USD 457.11 Billion | |

| USD 4.35 Billion | |

| % | |

|

Global Micro Services in Healthcare Market Segmentation, By Delivery Model (Cloud-Based and On-Premises), Component (Services and Platforms), End-User (Healthcare Payers, Clinical Laboratories, Healthcare Providers and Life Sciences Organizations), Distribution Channel (Direct Sales and Distributor Sales) - Industry Trends and Forecast to 2032

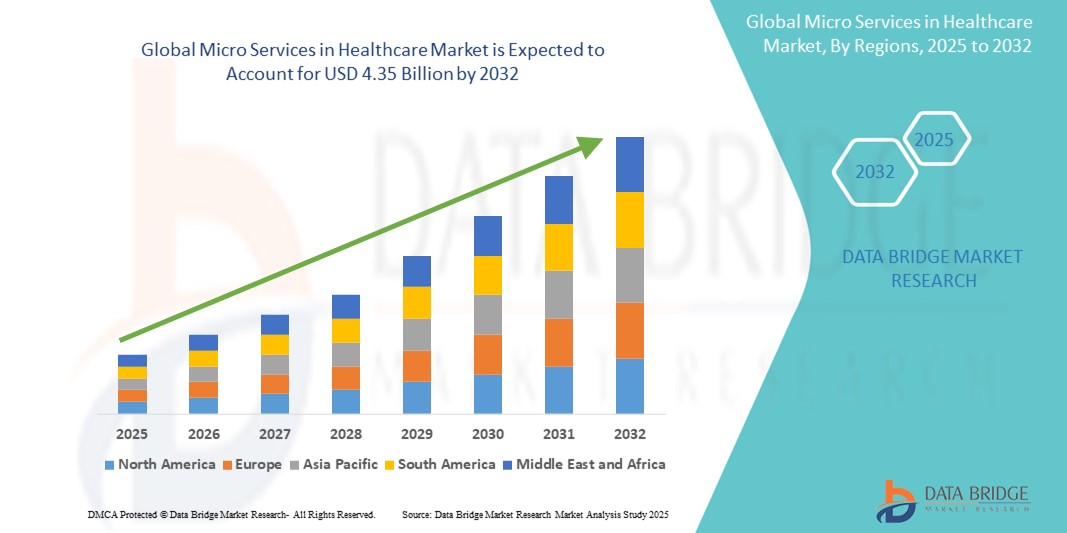

Global Micro Services in Healthcare Market Size

- The global micro services in healthcare size was valued atUSD 457.11 million in 2024and is expected to reachUSD 4.35 billion by 2032, at aCAGR of 32.55%during the forecast period

- This growth is driven by factors such as enhanced interoperability and data exchange and agility and innovation in healthcare delivery

Global Micro Services in Healthcare Market Analysis

- Microservices in healthcare refer to a modular approach to building and managing healthcare software systems, where applications are divided into small, independent services that each perform a specific business function. These services communicate via APIs and can be developed, deployed, and scaled independently

- The demand for microservices in healthcare is significantly driven by the need for enhanced interoperability, real-time patient data exchange, and customized healthcare solutions. With the shift toward value-based care and patient-centric models, microservices enable organizations to break down large monolithic systems into modular components that can be individually managed, scaled, and updated

- North America is expected to dominate the global microservices in healthcare market during the forecast period holding an estimated market share of approximately 47.5%. This dominance is attributed to its advanced IT infrastructure, adoption of digital health technologies, high healthcare spending, and the presence of key market players focused on delivering scalable, cloud-based healthcare solutions.

- Asia-Pacific is projected to be the fastest-growing region in the microservices in healthcare market due to rising investments in healthcare infrastructure, increasing digitalization of healthcare systems, and growing awareness of the benefits of microservice-based healthcare platforms. Countries such as India, China, and Japan are making significant advancements in eHealth and telemedicine, which is further fuelling market expansion

- Platform segment is expected to dominate the micro services in healthcare market with the largest share of 52.22% in 2025 as it offers modular solutions for integrating multiple services (EHRs, telemedicine, diagnostics), enabling rapid innovation and deployment of healthcare applications.

Report Scope and Global Micro Services in Healthcare Market Segmentation

|

Attributes |

Global Micro Services in Healthcare Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Global Micro Services in Healthcare Market Trends

“Advancements in Microservices Architecture for Healthcare Digital Transformation”

- One prominent trend in the evolution of healthcare IT is the rapid adoption of microservices architecture, enabling modular, scalable, and independently deployable services that revolutionize healthcare software development

- These advancements enhance agility and efficiency in healthcare systems by allowing real-time integration of clinical data, personalized patient services, and seamless interoperability across platforms. This modularity is crucial for responding to changing healthcare demands, regulatory requirements, and patient needs

- For instance, microservices allow healthcare organizations to independently update components such as electronic health records (EHR), telemedicine platforms, billing systems, or patient portals without disrupting the entire system. This flexibility accelerates digital innovation and supports complex, data-driven applications such as AI-powered diagnostics and real-time patient monitoring

- These innovations are transforming the healthcare delivery model, enabling faster deployment of solutions, improved patient experiences, and cost savings through efficient resource utilization. As a result, the demand for microservices-based healthcare systems is surging globally, especially among providers seeking to modernize legacy systems and implement future-ready digital health infrastructure

Global Micro Services in Healthcare Market Dynamics

Driver

“Surging Demand for Agile, Scalable Digital Healthcare Systems”

- The increasing need for agile and modular healthcare IT infrastructures is a major driver of growth in the global microservices in healthcare market. Microservices enable healthcare organizations to break down large monolithic systems into independently deployable, scalable modules, allowing quicker development and deployment of applications

- With the growing adoption of electronic health records (EHRs), telemedicine platforms, and remote patient monitoring systems, healthcare providers require highly adaptable solutions that can be integrated and updated without causing system-wide disruptions

- Microservices also improve system resilience, fault isolation, and maintenance efficiency, making them particularly appealing for large hospitals and health networks seeking to modernize legacy software and infrastructure

For instance,

- In January 2024, a report by Healthcare IT News highlighted that over 70% of U.S. health systems are planning to adopt microservices-based architectures by 2026 to enhance their digital transformation strategies. The flexibility and cost-efficiency of this model are key reasons behind the shift

- As the demand for real-time healthcare services, such as virtual consultations and instant diagnostics, continues to grow, microservices architecture is becoming essential for future-ready healthcare systems

Opportunity

“Revolutionizing Patient Care through AI-Integrated Microservices”

- The integration of AI with microservices architecture offers significant opportunities for innovation in healthcare. AI-powered modules can be independently deployed and scaled within a microservices framework, facilitating smarter decision-making and personalized treatment recommendations.

- AI-driven microservices can also handle natural language processing (NLP), predictive analytics, and clinical decision support, enabling more accurate diagnoses and proactive interventions.

- In addition, microservices enable continuous updates and integration of AI models across EHRs, imaging systems, and diagnostic platforms, improving system performance without downtime.

For instance,

- According to a study published in Nature Digital Medicine (March 2025), healthcare systems using AI-powered microservices reported up to 25% improvements in clinical workflow efficiency and a 40% reduction in diagnostic errors in radiology and pathology services

- This AI-microservices synergy is paving the way for automated patient triage, real-time clinical alerts, and enhanced remote monitoring, all of which contribute to improved patient outcomes and reduced healthcare costs

Restraint/Challenge

“Complex Implementation and Integration Barriers”

- Despite its advantages, the implementation of microservices in healthcare is often challenged by integration complexity, especially in organizations with legacy systems or outdated IT infrastructures

- The transition from monolithic architectures to microservices requires substantial investment, skilled developers, and coordinated efforts across IT and clinical teams. Without proper management, this can lead to data silos, communication failures, or security vulnerabilities

- Moreover, aligning multiple microservices to function cohesively within strict regulatory environments such as HIPAA or GDPR adds additional layers of compliance complexity

For instance,

- In a 2024 report from Frost & Sullivan, it was found that over 40% of mid-sized healthcare organizations in Europe faced difficulties integrating microservices due to limited technical expertise and inadequate data governance frameworks

- These challenges can delay digital transformation initiatives and widen the technology gap between advanced and resource-constrained healthcare systems, potentially affecting service delivery and patient care continuity

Global Micro Services in Healthcare Market Scope

The market is segmented on the basis of delivery model, component, end user and distribution channel.

|

Segmentation |

Sub-Segmentation |

|

By Delivery Model |

|

|

By Component |

|

|

By End User |

|

|

By Distribution Channel |

|

In 2025, the platform is projected to dominate the market with a largest share in technology segment

The platform segment is expected to dominate the micro services in healthcare market with the largest share of 52.22% in 2025 as it offers modular solutions for integrating multiple services (EHRs, telemedicine, diagnostics), enabling rapid innovation and deployment of healthcare applications. Platforms serve as the foundational infrastructure enabling healthcare organizations to rapidly innovate and deploy digital applications, streamlining clinical workflows and improving patient outcomes. Their flexibility supports the development of personalized care models, real-time data sharing, and automation—key drivers in today’s evolving healthcare environment.

The cloud-based delivery model is expected to account for the largest share during the forecast period in delivery model market

In 2025, the cloud-based delivery model segment is expected to dominate the market with the largest market share of 20.39% due to scalability and flexibility. Reduced infrastructure costs and subscription-based pricing models make cloud solutions more affordable for healthcare providers.

Global Micro Services in Healthcare Market Regional Analysis

“North America Holds the Largest Share in the Global Micro Services in Healthcare Market”

- North America leads the global microservices in healthcare market, holding an estimated 47.5 share, due to its advanced healthcare infrastructure, high technology adoption, and significant investments in healthcare innovation. The region's strong presence of healthcare providers and favorable regulatory environment also contribute to its dominance

- U.S. holds a dominant market share of around 41.5%. attributed to its advanced IT infrastructure, due to adoption of digital health technologies, high healthcare spending, and the presence of key market players focused on delivering scalable, cloud-based healthcare solutions

- The adoption of microservices technologies is fueled by the need for faster, more scalable, and flexible healthcare solutions to manage and treat these conditions. Continuous advancements in medical technologies and improved patient outcomes support the market’s expansion.

- The presence of major healthcare providers, technology companies, and medical device manufacturers fosters rapid innovation and integration of microservices solutions, enhancing healthcare delivery worldwide

“Asia-Pacific is Projected to Register the Highest CAGR in the Global Micro Services in Healthcare Market”

- Asia-Pacific is projected to be the fastest-growing region in the microservices in healthcare market due to rising investments in healthcare infrastructure, increasing digitalization of healthcare systems, and growing awareness of the benefits of microservice-based healthcare platforms

- Countries such as China, India, and Japan are emerging as key markets in the global microservices healthcare sector, driven by their large populations, rapid healthcare digitization, and increasing demand for personalized healthcare services

- Japan, a leader in adopting advanced medical technology, is a key market for microservices in healthcare. The country's healthcare system is highly digitalized, and there is a growing emphasis on improving operational efficiency, patient outcomes, and system interoperability. IT innovations, supports the demand for microservices technologies in the healthcare sector

- China is witnessing rapid growth in the microservices healthcare market due to the country’s large population and increasing prevalence of chronic diseases

- Fastest Growing Country: India is currently the fastest-growing market for microservices in healthcare in the Asia Pacific region. With a growing number of healthcare startups, a focus on healthcare IT adoption, and government-led initiatives to improve healthcare accessibility and affordability, India is rapidly embracing microservices to support scalable, cost-effective healthcare solutions

Global Micro Services in Healthcare Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Amazon Web Services, Inc.(U.S.)

- Microsoft (U.S.)

- Salesforce, Inc.(U.S.)

- Infosys Limited(India)

- IBM Corporation(U.S.)

- NGINX (U.S.)

- Oracle (U.S.)

- Atos SE (U.S.)

- Cognizant (U.S.)

- Datawire, Inc. (U.S.)

- Software GmbH (Germany)

- Red Hat, Inc. (U.S.)

- Cloud Software Group, Inc. (U.S.)

- SAP SE (Germany)

Latest Developments in Global Micro Services in Healthcare Market

- In March 2024, NVIDIA Healthcare launched generative AI microservices to advance drug discovery, MedTech, and digital health, offering a catalog of NVIDIA NIM and GPU-accelerated microservices for biology, chemistry, imaging, and healthcare data running in every NVIDIA DGX Cloud, enabling faster, scalable, and flexible healthcare solutions globally

- In March 2018, DevCool Inc. launched HiPaaS, a next-generation healthcare platform built on microservices and Dell Boomi iPaaS, enabling hospitals and insurance companies to quickly integrate new technologies such as blockchain, AI, telemedicine, and wearable devices while reducing costs by 60%

- In March 2024, Abridge partners with NVIDIA to enhance generative AI-powered clinical documentation, leveraging NVIDIA’s compute resources and NIM inference microservices, while receiving investment from NVentures to scale its AI solutions for clinicians and improve healthcare efficiency

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。