Global Mobile Operating Tables Market

市场规模(十亿美元)

CAGR :

%

USD

861.79 Billion

USD

1,126.94 Billion

2025

2033

USD

861.79 Billion

USD

1,126.94 Billion

2025

2033

| 2026 –2033 | |

| USD 861.79 Billion | |

| USD 1,126.94 Billion | |

| % | |

|

全球移動手術台市場細分,按產品類型(手動、電動、液壓和電液式)、應用(普通外科和專科外科)以及最終用戶(醫院、診斷中心、診所、門診手術中心及其他)劃分——行業趨勢及至2033年的預測

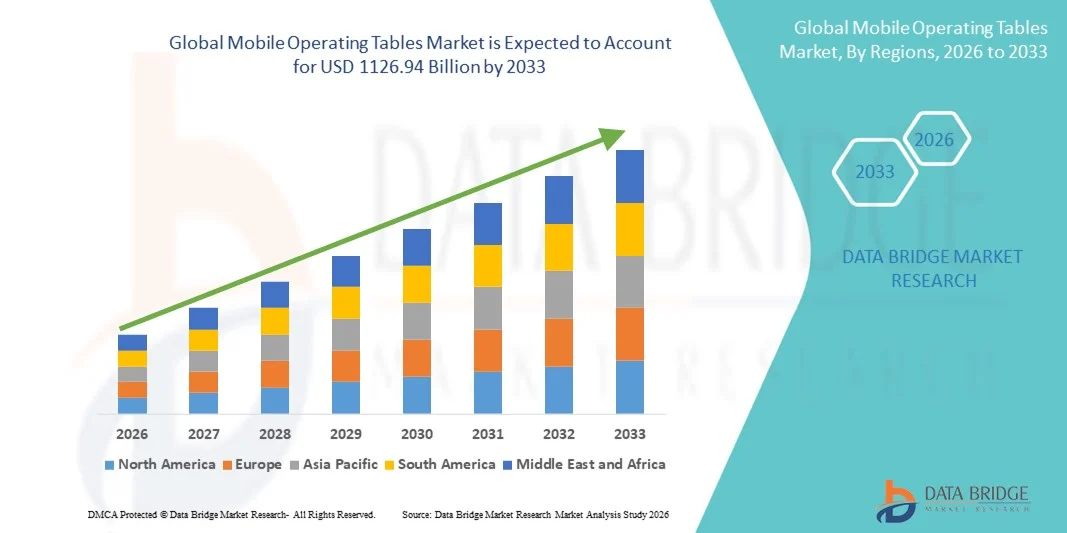

行動手術台市場規模

- 2025年全球行動手術台市場規模為8,617.9億美元 ,預估 至2033年將達1,1269.4億美元,預測期內 複合年增長率為3.41%。

- 市場成長的主要驅動力是先進手術基礎設施的日益普及和醫院設備的持續技術進步,從而提高了醫療機構手術室的現代化程度和效率。

- 此外,市場對靈活、安全且符合人體工學的手術解決方案的需求日益增長,使得行動手術台成為現代手術環境的重要組成部分。這些因素共同推動了移動手術台在醫院和手術中心的普及,從而顯著促進了市場的整體成長。

行動手術台市場分析

- 移動式手術台旨在為手術過程提供靈活性、精準定位和便捷移動,由於其適用於多種外科專科並能提高工作流程效率,因此在現代醫院和門診手術中心的手術室中日益成為不可或缺的組成部分。

- 移動式手術台需求的成長主要受以下因素驅動:手術量增加、微創手術普及率提高,以及對符合人體工學且對病人安全的先進手術設備的需求。

- 北美地區在行動手術台市場佔據主導地位,預計到2025年將以38.4%的最大市場份額領先。這得益於其先進的醫療基礎設施、高額的醫療支出、對先進手術設備的早期應用以及眾多領先醫療器材製造商的強大影響力。其中,美國憑藉其龐大的手術量和持續的醫院現代化進程,佔據了主要市場份額。

- 預計亞太地區將成為預測期內移動手術台市場成長最快的地區,複合年增長率預計達到21.2%,這主要得益於醫療基礎設施的擴張、醫療旅遊業的興起、醫院投資的增加以及新興經濟體獲得先進外科手術服務的機會不斷增長。

- 2025年,一般外科手術領域將以46.8%的市佔率佔據市場主導地位,這主要得益於全球常規手術數量的成長。

報告範圍及行動手術台市場細分

|

屬性 |

行動手術台關鍵市場洞察 |

|

涵蓋部分 |

|

|

覆蓋國家/地區 |

北美洲

歐洲

亞太

中東和非洲

南美洲

|

|

主要市場參與者 |

• Stryker (美國) |

|

市場機遇 |

|

|

加值資料資訊集 |

除了對市場狀況(如市場價值、成長率、細分、地理覆蓋範圍和主要參與者)的洞察之外,Data Bridge Market Research 精心編制的市場報告還包括深入的專家分析、患者流行病學、產品線分析、定價分析和監管框架。 |

行動手術台市場趨勢

移動手術台的技術進步和人體工學改進

- 全球行動手術台市場的一個顯著且加速發展的趨勢是手術台設計的不斷進步,重點在於提升人體工學、模組化功能和改善患者體位擺放能力。製造商正越來越多地整合先進的液壓和機電系統,以支援精確的高度調節、傾斜和多軸運動,從而提高手術效率和臨床效果。

- For instance, in October 2023, Getinge AB expanded its Maquet operating table portfolio with advanced mobile surgical tables designed to support complex cardiovascular, orthopedic, and neurosurgical procedures, offering improved radiolucency and flexible positioning options to accommodate diverse surgical requirements

- Technological innovation in mobile operating tables has enabled features such as carbon-fiber tabletops for enhanced imaging compatibility, programmable positioning memory, and modular accessories that allow quick adaptation across multiple surgical specialties. For example, Steris introduced mobile tables with advanced imaging compatibility to support hybrid operating rooms, enabling seamless integration with C-arms and intraoperative imaging systems

- The growing emphasis on minimally invasive and image-guided surgeries has further increased demand for mobile operating tables that provide unobstructed imaging access and stable patient positioning. This evolution supports higher procedural accuracy while reducing surgeon fatigue and operating room turnaround times

- This trend toward more advanced, versatile, and ergonomically optimized mobile operating tables is reshaping operating room standards worldwide. Consequently, companies such as Hillrom (now part of Baxter International) and Trumpf Medical are focusing on developing mobile operating tables that combine mobility, durability, and advanced positioning functionality

- The demand for technologically advanced mobile operating tables is increasing across hospitals, ambulatory surgical centers, and specialty clinics, as healthcare providers prioritize surgical precision, workflow efficiency, and patient safety

Mobile Operating Tables Market Dynamics

Driver

Rising Surgical Volumes and Expansion of Healthcare Infrastructure

- The increasing number of surgical procedures globally, driven by a rising burden of chronic diseases, aging populations, and trauma cases, is a major driver fueling demand for mobile operating tables. Hospitals and surgical centers are investing in advanced surgical infrastructure to accommodate growing patient volumes

- For instance, in June 2024, Steris announced investments to expand its surgical equipment manufacturing capacity, including mobile operating tables, to support rising demand from newly constructed hospitals and ambulatory surgical centers across North America and Europe. Such strategic expansions by key players are expected to drive Mobile Operating Tables market growth during the forecast period

- As healthcare systems expand and modernize, mobile operating tables offer flexibility and cost efficiency compared to fixed systems, allowing facilities to optimize operating room utilization across multiple specialties

- Furthermore, the global rise in outpatient and day-care surgeries is increasing demand for mobile, space-efficient operating tables that can be easily repositioned and adapted for different procedures

- The growing emphasis on surgical precision, infection control, and workflow optimization is encouraging hospitals to replace older equipment with modern mobile operating tables, further accelerating market adoption

Restraint/Challenge

High Capital Investment and Maintenance Requirements

- The high initial cost associated with advanced mobile operating tables poses a significant challenge to market growth, particularly for small and mid-sized healthcare facilities in cost-sensitive regions. These systems often require substantial upfront investment due to their complex mechanical systems, imaging compatibility, and modular accessories

- For instance, hospitals in emerging markets have reported budget constraints limiting large-scale procurement of advanced mobile operating tables, leading to extended replacement cycles and continued use of older, less versatile equipment

- In addition to purchase costs, ongoing maintenance, calibration, and servicing requirements add to the total cost of ownership, placing further financial strain on healthcare providers

- While technologically advanced tables offer long-term efficiency benefits, the perceived cost burden can delay adoption, especially in public hospitals with limited capital budgets

- Addressing these challenges through cost-effective product offerings, flexible financing models, and improved durability will be critical for manufacturers seeking sustained growth in the global Mobile Operating Tables market

Mobile Operating Tables Market Scope

The market is segmented on the basis of product type, application, and end use.

- By Product Type

On the basis of product type, the Global Mobile Operating Tables market is segmented into manual, electric, hydraulic, and electro-hydraulic tables. The electric mobile operating tables segment dominated the market with the largest revenue share of 41.6% in 2025, driven by their superior positioning accuracy, ease of operation, and compatibility with advanced surgical procedures. Electric tables allow precise height, tilt, and lateral adjustments, which significantly enhance surgeon ergonomics and procedural efficiency. Hospitals increasingly prefer electric tables due to reduced physical strain on staff and improved workflow in high-volume operating rooms. Integration with imaging systems such as C-arms further supports adoption. Growing demand for minimally invasive surgeries is also reinforcing segment dominance. In addition, higher investments by hospitals in technologically advanced operating room infrastructure continue to sustain strong demand. Long service life and reliability further contribute to widespread adoption across developed healthcare systems.

The electro-hydraulic segment is expected to witness the fastest CAGR of 21.5% from 2026 to 2033, owing to its combination of electric precision and hydraulic load-bearing capacity. These tables are increasingly adopted for complex and specialty surgeries requiring high stability and flexible positioning. Rising surgical volumes and growing adoption of hybrid operating rooms are driving demand. Electro-hydraulic systems offer enhanced patient safety, smooth movement, and high weight capacity, making them suitable for bariatric and orthopedic procedures. Increasing healthcare investments in emerging economies are accelerating adoption. Hospitals upgrading from manual and hydraulic systems are also contributing to rapid growth. Technological advancements and declining system costs further support market expansion.

- By Application

On the basis of application, the Global Mobile Operating Tables market is segmented into general surgical and specialty surgical procedures. The general surgical segment dominated the market with a revenue share of 46.8% in 2025, supported by the high volume of routine surgeries performed globally. General surgeries such as abdominal, gynecological, and urological procedures require versatile and mobile operating tables, driving consistent demand. The widespread presence of general operating rooms across hospitals and surgical centers supports segment dominance. Increasing incidence of chronic diseases and trauma cases further boosts procedure volumes. Cost-effectiveness and standardized table requirements also favor adoption. Moreover, general surgical tables are frequently replaced due to high utilization rates. This sustained procedural demand continues to anchor the segment’s leading position.

The specialty surgical segment is projected to grow at the fastest CAGR of 22.3% from 2026 to 2033, driven by rising volumes of orthopedic, cardiovascular, neurosurgical, and minimally invasive procedures. Specialty surgeries require advanced positioning capabilities and higher precision, increasing demand for technologically advanced mobile operating tables. Growth in aging populations and lifestyle-related disorders is accelerating specialty procedure rates. Increasing adoption of robotic-assisted and image-guided surgeries further supports segment expansion. Hospitals are increasingly investing in specialized operating rooms to improve surgical outcomes. Expanding access to advanced surgical care in emerging markets also contributes to rapid growth. Continuous innovation in table design and functionality is expected to sustain momentum.

- By End Use

根據最終用途,全球行動手術台市場可細分為醫院、診斷中心、診所、門診手術中心和其他機構。預計到2025年,醫院將佔據市場主導地位,收入份額高達52.4%,這主要得益於醫院龐大的手術量和完善的手術基礎設施。醫院進行各種普通外科和專科手術,因此各科室都需要配備多台行動手術台。熟練的外科醫生、先進的手術室和完善的急診服務保障了移動手術台的高利用率。醫院的持續擴建和現代化改造進一步推動了市場需求。已開發地區優惠的報銷政策也促進了醫院的市場主導地位。此外,老舊設備的更換也促使醫院持續採購。充足的資金預算使醫院能夠購買先進的電動和電液式手術台。

受全球醫療模式轉變為門診和日間手術的推動,預計2026年至2033年間,日間手術中心(ASC)細分市場將以23.1%的複合年增長率(CAGR)實現最快成長。 ASC優先考慮成本效益高、節省空間且便於行動裝置的設備,從而推動了對先進手術台的需求。微創手術的日益普及也促進了該領域的成長。更短的住院時間和更低的手術成本正推動ASC在全球的擴張。私人醫療機構不斷增加的投資進一步加速了ASC的普及。技術進步使得緊湊型多功能手術台的出現與ASC的需求高度契合。患者對門診治療日益增長的偏好預計將支撐ASC的長期成長。

行動手術台市場區域分析

- 北美地區在行動手術台市場佔據主導地位,預計到2025年將以38.4%的市佔率位居榜首。這主要得益於其先進的醫療基礎設施、高額的醫療支出、對先進手術設備的早期應用以及眾多領先醫療器材製造商的強大影響力。美國佔據了該地區需求的主要份額,這主要歸功於其龐大的手術量、持續的醫院現代化改造以及手術室設備頻繁的更新換代。

- 外科手術數量的增長、對微創手術需求的增加以及醫院對先進手術室基礎設施投入的不斷增長,正在推動移動手術台的普及應用。

- 此外,北美也受惠於健全的醫保報銷政策、大量技術精湛的外科醫生以及提供技術先進的手術台系統的全球主要廠商。這些因素共同促成了該地區在全球市場的領先地位。

美國行動手術台市場洞察

2025年,美國行動手術台市場在北美市場佔據最大份額,主要得益於美國高手術量和先進外科技術的快速普及。美國醫療體系對現代化和病人安全的重視,推動了手術室設備(包括行動手術台)的頻繁升級。對複雜手術需求的增長、醫院和手術中心數量的增加以及醫療旅遊的興起,也促進了市場擴張。領先的醫療器材製造商的存在和強大的研發實力,進一步推動了手術台設計和功能的創新。此外,有利的報銷機制和高額的醫療支出也持續支持電動和電液式行動手術台的大規模應用。

歐洲移動手術台市場洞察

受醫療基礎設施投資增加、手術量增長以及對先進手術室設備需求不斷增長的推動,歐洲移動手術台市場預計將在預測期內保持顯著的複合年增長率。歐洲各國政府正在對醫院設施進行現代化改造,並投資於技術先進的手術器械,以改善病患的治療效果。該地區對高品質醫療服務的重視,以及人口老化帶來的手術需求增加,都為市場成長提供了支撐。此外,微創手術和機器人輔助手術的日益普及也推動了對具有更高精度和定位能力的專用移動手術台的需求。

英國移動手術台市場洞察

受手術量增加、醫療基礎設施擴建以及醫院現代化投資成長的推動,英國行動手術台市場預計在預測期內將以顯著的複合年增長率成長。英國完善的醫療體係以及對改善手術效果日益重視,都支撐了對先進移動手術台的需求。此外,慢性病盛行率的上升和人口老化也增加了手術需求,進一步刺激了市場需求。英國政府的大力支持以及對高品質手術設備的廣泛應用,也為市場發展提供了助力。

德國移動手術台市場洞察

預計在預測期內,德國行動手術台市場將以可觀的複合年增長率增長,這主要得益於醫療保健支出不斷增加、醫院基礎設施完善以及先進手術設備的日益普及。德國對創新和先進醫療技術的重視推動了對電動和電液式移動手術台的需求。主要醫療器材製造商的存在以及強大的臨床研究活動也進一步促進了市場成長。此外,手術量的增加和醫院的持續升級改造也推動了新型手術台的更新換代。

亞太地區行動手術台市場洞察

亞太地區行動手術台市場預計將成為成長最快的地區,預測期內複合年增長率(CAGR)預計為21.2%。推動市場成長的主要因素包括:醫療基礎設施的不斷完善、醫療旅遊業的蓬勃發展、醫院投資的持續增加以及新興經濟體獲得先進外科手術服務的機會日益增多。中國、印度、日本和韓國等國家正經歷醫療支出和醫院規模的快速成長。手術數量的增加、對微創手術需求的增長以及對改善農村地區醫療服務可近性的日益重視,都為市場成長提供了支撐。此外,政府的利好政策以及國際醫療器材製造商在該地區日益增長的影響力,也促進了先進行動手術台在該地區的應用。

日本行動手術台市場洞察

由於日本醫療水平高、醫療技術先進且手術量不斷增長,行動手術台市場正穩步發展。日本人口老化導致手術需求增加,從而推動了現代化手術台的普及。此外,完善的醫院基礎設施和政府高額的醫療保健支出也為市場提供了支撐。而且,日本醫院越來越多地採用電動和電液式手術台,以提高手術精度和病人安全性。

中國移動手術台市場洞察

由於醫療基礎設施建設不斷完善、醫療支出持續成長以及手術量不斷擴大,中國移動手術台市場正迅速擴張。在政府為提升醫療服務可近性和品質而採取的各項措施的支持下,中國醫院的現代化和擴建工程正在蓬勃發展。此外,醫院數量的增加和醫療旅遊業的興起也推動了對先進移動手術台的需求。本地化生產和具有競爭力的價格進一步促進了市場成長。

行動手術台市場份額

行動手術台產業主要由一些知名企業主導,其中包括:

• Stryker (U.S.)

• Getinge AB (Sweden)

• STERIS plc (Ireland)

• Getinge (Germany)

• Skytron, LLC (U.S.)

• Alvo Medical (Poland)

• Merivaara Corp. (Finland)

• Mizuho OSI (U.S.)

• Medifa GmbH (Germany)

• Schaerer Medical AG (Switzerland)

• Lojer Group (Finland)

• UFSK-International OSYS (Germany)

• Aldon Company (U.S.)

• Brumaba GmbH (Germany)

Latest Developments in Global Mobile Operating Tables Market

- In July 2023, Hospital Products Australia introduced the Mindray HyBase V9 Operating Table, a new mobile surgical table featuring intelligent safety systems such as anti-collision sensors and automatic locking mechanisms, designed to enhance surgical safety and reduce procedural risks for a wide range of procedures

- In March 2023, Getinge AB introduced a modular hybrid operating table platform designed for seamless integration with robotic surgical systems, offering enhanced precision and flexibility in high-tech operating room environments and supporting evolving surgical workflows

- In July 2024, Getinge launched the Maquet Corin operating table along with the Maquet Ezea surgical light at the AORN Conference in Nashville, Tennessee, introducing a connected operating table designed to improve workflow efficiency and surgical outcomes, reflecting a continued focus on advanced OR solutions

- In August 2024, Getinge expanded availability of the Maquet Corin operating table and Ezea surgical light in markets including India, emphasizing user-friendly features, safety enhancements, and workflow support for healthcare facilities

- In January 2025, Mindray North America launched its first surgical table, the HyBase V6, a versatile and precise mobile operating table developed to support a broad patient population and enhance clinical and operational workflows in healthcare facilities worldwide

- In March 2025, Getinge announced a strategic partnership with Mindray to co-develop and market an integrated modular operating table platform designed to combine advanced positioning capabilities with anesthesia and monitoring ecosystems, strengthening collaborative innovation in mobile OR solutions

- In May 2025, Alvo Medical unveiled its UltraFlex operating table, a versatile platform designed to optimize positioning for a wide range of surgical procedures and improve compatibility with evolving imaging modalities and operating room workflows, demonstrating ongoing product diversification in the OR table segment

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。