Global Optical Coherence Tomography For Ophthalmology Market

市场规模(十亿美元)

CAGR :

%

USD

265.96 Million

USD

449.16 Million

2025

2033

USD

265.96 Million

USD

449.16 Million

2025

2033

| 2026 –2033 | |

| USD 265.96 Million | |

| USD 449.16 Million | |

| % | |

|

全球眼科光學相干斷層掃描市場細分,按產品(手持式OCT設備、桌上型OCT設備和導管式OCT設備)、技術(時域OCT、頻域OCT、空間編碼頻率、光譜域和掃頻源)、類型(半自動和全自動)以及最終用戶(醫院、診所、門診手術中心、醫生辦公室及其他)劃分——行業趨勢及至2033年的預測

眼科光學相干斷層掃描市場規模

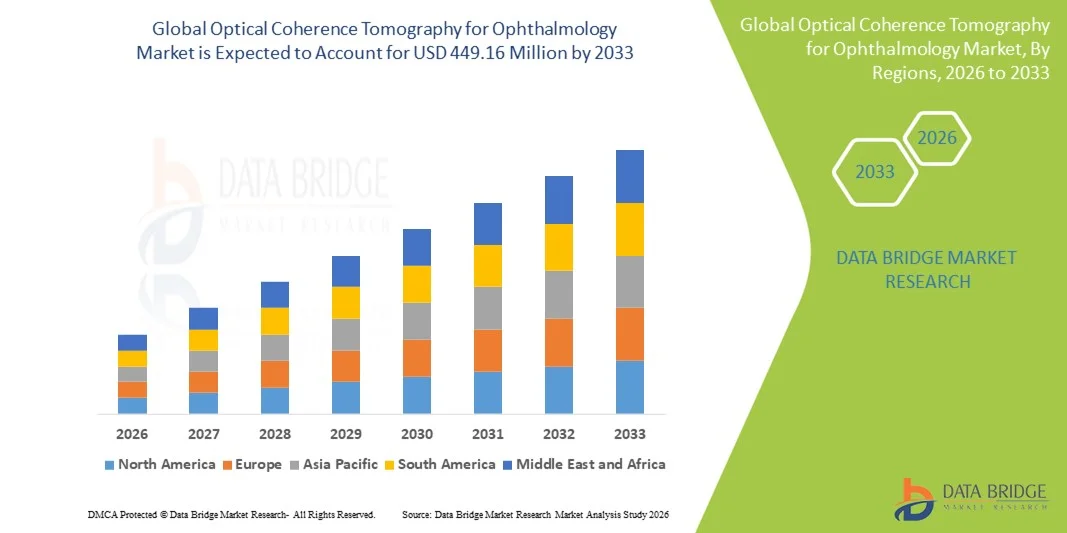

- 2025年全球眼科光學相干斷層掃描市場規模為2.6596億美元 ,預計 2033年將達到4.4916億美元,預測期間內 複合年增長率為6.77%。

- 市場成長主要得益於先進眼科影像技術的日益普及和光學相干斷層掃描系統的持續技術進步,從而提高了醫院和眼科診所對視網膜和眼前節疾病的診斷準確性和早期檢測能力。

- 此外,對非侵入性、高解析度影像解決方案的需求不斷增長,以及青光眼、糖尿病視網膜病變和黃斑部病變等老年眼部疾病的日益普遍,正使光學相干斷層掃描(OCT)成為眼科的核心診斷手段。這些因素共同推動了光學相干斷層掃描解決方案的普及,從而顯著促進了整體市場成長。

眼科光學相干斷層掃描市場分析

- 光學相干斷層掃描系統能夠對眼部組織進行高解析度、非侵入性的橫斷面成像,由於其能夠早期發現和監測視網膜和視神經疾病,因此在醫院和眼科診所的現代眼科診斷中日益成為至關重要的組成部分。

- 光學相干斷層掃描(OCT)系統的需求不斷增長,主要原因是青光眼、糖尿病視網膜病變和老年黃斑部病變等眼部疾病的盛行率不斷上升,以及能夠提高診斷準確性和臨床決策能力的先進成像技術的日益普及。

- 北美地區在眼科光學相干斷層掃描(OCT)市場佔據主導地位,預計到2025年將佔約42.5%的市場份額,成為最大的收入來源。這得益於先進的醫療基礎設施、創新眼科成像技術的廣泛應用、有利的醫保報銷政策以及領先的OCT設備製造商的強大市場地位,其中美國佔據了該地區需求的主要份額。

- 預計在預測期內,亞太地區將成為眼科光學相干斷層掃描(OCT)市場成長最快的地區,複合年增長率約為20.9%,這主要得益於人口快速老化、視力相關疾病發生率上升、眼科醫療服務覆蓋範圍擴大以及新興經濟體醫療保健投資的增加。

- 到2025年,半自動成像設備將佔據最大的市場份額,達到53.2%,這主要得益於臨床控制下手動操作在精確成像方面的廣泛應用。

報告範圍及眼科光學相干斷層掃描市場細分

|

屬性 |

眼科光學相干斷層掃描關鍵市場洞察 |

|

涵蓋部分 |

|

|

覆蓋國家/地區 |

北美洲

歐洲

亞太

中東和非洲

南美洲

|

|

主要市場參與者 |

|

|

市場機遇 |

|

|

加值資料資訊集 |

除了對市場價值、成長率、細分、地理覆蓋範圍和主要參與者等市場狀況的洞察之外,Data Bridge Market Research 精心編制的市場報告還包括深入的專家分析、病患流行病學、研發管線分析、定價分析和監管框架。 |

眼科光學相干斷層掃描市場趨勢

透過人工智慧整合和自動化成像提高診斷精度

- 全球眼科光學相干斷層掃描(OCT)市場的一大趨勢是人工智慧(AI)與OCT系統的融合日益增強。 AI賦能的OCT技術提高了診斷準確率,縮短了判讀時間,使臨床醫生能夠更早、更準確地檢測出視網膜疾病。

- For instance, AI algorithms are now being used to automatically detect retinal abnormalities, classify disease severity, and provide quantitative analysis of retinal layers. This automation helps ophthalmologists to streamline workflow and deliver faster patient care

- AI integration also supports real-time image enhancement and noise reduction, allowing clearer visualization of retinal structures even in challenging imaging conditions

- The adoption of AI-driven OCT is especially significant in the management of diseases such as diabetic retinopathy, age-related macular degeneration (AMD), glaucoma, and retinal vein occlusion, where early detection is critical

- This trend is reshaping clinical expectations, driving demand for more advanced OCT systems that combine high-resolution imaging, AI analysis, and cloud-based data management

Optical Coherence Tomography for Ophthalmology Market Dynamics

Driver

Growing Prevalence of Retinal Disorders and Rising Demand for Early Diagnosis

- Increasing incidence of retinal diseases such as diabetic retinopathy, glaucoma, and AMD is a key driver for OCT market growth. The global rise in diabetes and aging populations is contributing to higher demand for advanced retinal imaging

- OCT systems offer non-invasive, high-resolution cross-sectional imaging of retinal layers, making them essential for early diagnosis and monitoring of progressive eye disorders

- For instance, Hospitals in the US and Europe widely use OCT for routine retinal screening, especially for diabetic patients

- The expanding adoption of OCT in ophthalmology clinics, hospitals, and diagnostic centers is further boosting market demand

- Increasing awareness about vision care and preventive ophthalmology is encouraging patients to undergo regular eye examinations, supporting the growth of OCT adoption

- Technological advancements, such as swept-source OCT, OCT angiography, and handheld OCT devices, are expanding the clinical applications and improving patient accessibility

Restraint/Challenge

High Equipment Cost and Limited Reimbursement Policies

- One major challenge for OCT market growth is the high initial cost of advanced OCT systems, which can limit adoption, especially in developing regions and smaller clinics

- Many advanced OCT devices require significant capital investment, and limited reimbursement policies for diagnostic imaging can discourage providers from upgrading equipment

- For instance, in several developing countries, reimbursement for OCT diagnostics is limited, making it difficult for clinics to justify the investment

- In addition, training and expertise requirements for interpreting OCT images can be a barrier in regions with fewer specialized ophthalmologists

- Ensuring affordability through cost-effective devices and bundled service models will be essential for broader market penetration

Optical Coherence Tomography for Ophthalmology Market Scope

The market is segmented on the basis of product, technology, type, and end user.

- By Product

On the basis of product, the Optical Coherence Tomography for Ophthalmology market is segmented into handheld OCT devices, tabletop OCT devices, and catheter-based OCT devices. The tabletop OCT devices segment dominated the largest market revenue share of 45.8% in 2025, driven by its high-resolution imaging and wide adoption in hospitals and advanced ophthalmology clinics. Tabletop OCT systems are preferred for their stability, ease of use, and integration with existing diagnostic workflows. These devices provide superior image clarity, enabling accurate retinal and glaucoma diagnosis. Hospitals and large clinics invest heavily in tabletop OCT due to their advanced features and long-term reliability. Their strong presence in developed regions contributes significantly to revenue share. Furthermore, tabletop OCT systems support multi-modality imaging and AI integration, which enhances diagnostic efficiency. These devices are also widely used for clinical trials and research, boosting adoption. As a result, tabletop OCT remains the dominant product segment in the global market.

The handheld OCT devices segment is anticipated to witness the fastest CAGR of 22.4% from 2026 to 2033, driven by growing demand for portable diagnostics in remote and pediatric healthcare settings. Handheld OCT is increasingly used in neonatal and pediatric ophthalmology, where patient cooperation is limited. Its portability enables on-site imaging in outreach programs and rural clinics. Rising prevalence of eye disorders in underserved regions supports adoption. Manufacturers are improving handheld device accuracy, making them comparable to tabletop systems. Reduced cost and ease of transportation also encourage usage. In addition, handheld OCT is becoming essential in emergency and critical care units for rapid eye assessment. Continuous technological advancements, such as wireless connectivity and AI-assisted imaging, further boost growth. Overall, handheld OCT is expected to expand rapidly in emerging markets and mobile healthcare environments.

- By Technology

On the basis of technology, the Optical Coherence Tomography for Ophthalmology market is segmented into time domain OCT, frequency domain OCT, spatial encoded frequency, spectral-domain, and swept-source. The spectral-domain OCT segment dominated the largest market revenue share of 47.6% in 2025, driven by its high imaging speed and superior resolution for retinal diagnosis. Spectral-domain OCT is widely used in retinal clinics and hospitals due to its reliable performance in diagnosing macular degeneration and diabetic retinopathy. The technology enables fast acquisition of high-quality images, which improves patient throughput. It also supports advanced analytics and AI-based diagnostic tools. Many leading OCT manufacturers focus on spectral-domain systems, strengthening their market dominance. Clinical preference for spectral-domain OCT remains strong due to established evidence and long-term adoption. In addition, integration with ophthalmic EMR systems increases its utility in large healthcare facilities. As a result, spectral-domain OCT holds the largest revenue share in 2025.

The swept-source OCT segment is expected to witness the fastest CAGR of 23.1% from 2026 to 2033, fueled by its deeper tissue penetration and enhanced imaging speed. Swept-source OCT is increasingly used for posterior segment imaging and glaucoma assessment. It provides accurate axial length measurement and supports advanced IOL planning. The growing adoption of swept-source OCT in premium eye care centers is driving market growth. Increasing research and development in swept-source technology is expanding its clinical applications. Also, its compatibility with multimodal imaging platforms enhances adoption. The growing trend of personalized ophthalmic diagnostics further accelerates demand. As a result, swept-source OCT is expected to experience rapid expansion in the forecast period.

- By Type

On the basis of type, the Optical Coherence Tomography for Ophthalmology market is segmented into semi-automatic and fully automatic. The semi-automatic segment dominated the largest market revenue share of 53.2% in 2025, driven by the widespread use of manual operation with clinical control for accurate imaging. Semi-automatic OCT devices are preferred in hospitals and diagnostic centers where trained technicians perform scans. The ability to adjust imaging parameters manually provides high flexibility and better control in complex cases. This type is especially popular in retinal and glaucoma clinics where detailed image capture is essential. Semi-automatic systems are also cost-effective compared to fully automatic solutions, supporting adoption in developing regions. Many clinics prefer semi-automatic devices due to existing staff expertise and workflow familiarity. Moreover, semi-automatic OCT offers better customization for complex patients. As a result, it remains the dominant segment in 2025.

The fully automatic segment is anticipated to witness the fastest CAGR of 21.9% from 2026 to 2033, driven by the growing demand for AI-enabled imaging and simplified workflow. Fully automatic OCT devices are preferred in high-volume settings such as large hospitals and surgical centers. These systems reduce operator dependency and provide faster scan acquisition. Increasing integration of AI for automatic diagnosis and report generation boosts adoption. Fully automatic OCT is also gaining traction in clinics aiming to reduce training requirements. The demand for remote ophthalmic screening and telemedicine is accelerating growth. As a result, fully automatic OCT devices are expected to expand rapidly during the forecast period.

- By End User

On the basis of end user, the Optical Coherence Tomography for Ophthalmology market is segmented into hospitals, clinics, ASCs, physicians’ offices, and others. The hospitals segment accounted for the largest market revenue share of 41.9% in 2025, driven by high patient volumes and advanced ophthalmic infrastructure. Hospitals invest in OCT systems to support large-scale retinal and glaucoma screening. The presence of skilled ophthalmologists and strong diagnostic capabilities enhances adoption. In addition, hospitals are central hubs for clinical trials and research, increasing OCT utilization. High budget allocation and strong reimbursement support further drive hospital adoption. The need for multi-modal imaging in tertiary care settings strengthens market dominance. Hospitals also focus on premium patient care and accurate diagnostics, supporting OCT investment. As a result, hospitals remain the largest end-user segment.

The clinics segment is expected to witness the fastest CAGR of 22.6% from 2026 to 2033, driven by the expansion of specialty ophthalmology centers and outpatient services. Clinics are increasingly adopting OCT systems to improve diagnostic efficiency and patient experience. Rising prevalence of eye disorders and growing outpatient surgery demand are key growth drivers. Lower cost of ownership and improved portability make OCT suitable for clinics. Clinics also benefit from AI-enabled diagnostic tools, which reduce dependency on specialist interpretation. The expansion of private eye care chains in emerging markets further boosts adoption. As a result, clinics are expected to grow rapidly during the forecast period.

Optical Coherence Tomography for Ophthalmology Market Regional Analysis

- North America dominated the optical coherence tomography for ophthalmology market with the largest revenue share of approximately 42.5% in 2025. This strong position is supported by advanced healthcare infrastructure, high adoption of innovative ophthalmic imaging technologies, favorable reimbursement policies, and a strong presence of leading OCT manufacturers

- 該市場佔據了區域需求的大部分。此外,該地區眼部疾病(如老年黃斑部病變(AMD)、糖尿病視網膜病變和青光眼)的發生率也很高,這增加了對先進OCT診斷的需求。

- 此外,人工智慧整合式光學相干斷層掃描(OCT)系統和OCT血管攝影技術的快速普及,提高了診斷準確性和患者預後,進一步推動了市場成長。

美國眼科光學相干斷層掃描市場洞察

預計到2025年,美國眼科光學相干斷層掃描(OCT)市場在北美地區將佔據最大的市場份額。這一增長主要得益於對早期診斷和先進眼科護理服務的重視。尖端成像系統的快速普及、高昂的醫療保健支出以及完善的眼科診所和醫院體係是支撐市場成長的主要因素。此外,有利的報銷政策和OCT設備的持續技術創新也加速了美國市場的擴張。

歐洲眼科光學相干斷層掃描市場洞察

受完善的醫療基礎設施、公眾對眼科疾病日益增長的認識以及視網膜疾病患病率不斷上升的推動,預計歐洲眼科光學相干斷層掃描(OCT)市場在預測期內將以顯著的複合年增長率增長。與醫療診斷相關的嚴格監管以及醫院和診斷中心對先進影像系統的日益普及也促進了市場成長。此外,該地區糖尿病相關眼部併發症和青光眼病例的增加也推高了對OCT設備的需求。

英國眼科光學相干斷層掃描市場洞察

英國眼科光學相干斷層掃描(OCT)市場預計將以顯著的複合年增長率增長,這主要得益於視網膜疾病早期檢測需求的不斷增長以及先進眼科成像技術的日益普及。公共和私人醫療機構對現代診斷工具的高採用率,以及政府對視力保健的日益重視,預計將推動市場成長。此外,英國驗光診所對OCT的使用率也不斷提高,改善了患者獲得先進視網膜診斷服務的機會。

德國眼科光學相干斷層掃描市場洞察

預計在預測期內,德國眼科光學相干斷層掃描(OCT)市場將顯著成長,這主要得益於德國對醫療創新和先進診斷技術的大力投入。德國完善的醫療基礎設施和對醫療設備的高額投資,促進了醫院和專科診所對OCT設備的廣泛應用。此外,人們對眼部保健和預防性眼科的日益重視,也進一步推動了對OCT系統的需求。

亞太地區眼科光學相干斷層掃描市場洞察

預計在預測期內,亞太地區眼科光學相干斷層掃描(OCT)市場將成為成長最快的地區,複合年增長率(CAGR)約為20.9%。這一快速成長主要受人口老化加劇、視力相關疾病發生率上升、眼科醫療服務覆蓋範圍擴大以及新興經濟體醫療保健投資增加等因素所驅動。醫療基礎設施的不斷完善、可支配收入的提高以及眼科診所數量的增加,正在推動中國、印度和日本等國家對OCT設備的採用。此外,人們對眼科保健和疾病早期診斷意識的提高也促進了該地區的市場成長。

日本眼科光學相干斷層掃描市場洞察

由於日本老年眼疾高發生率以及醫療設備技術的快速發展,眼科光學相干斷層掃描(OCT)市場正蓬勃發展。該國人口老化和高昂的醫療保健支出也推動了對先進視網膜成像系統的需求。此外,日本正在推廣OCT血管攝影和人工智慧OCT解決方案,從而提高視網膜疾病的早期檢出率。

中國眼科光學相干斷層掃描市場洞察

預計到2025年,中國眼科光學相干斷層掃描(OCT)市場將佔據亞太地區最大的市場份額,這主要得益於醫療保健投資的增加、眼科診所數量的增長以及先進診斷成像設備應用的日益普及。中國不斷壯大的中產階級人口以及糖尿病相關眼疾的高發生率正在推動對OCT系統的需求。此外,政府日益重視改善醫療服務和醫療基礎設施也促進了OCT市場的成長。

眼科光學相干斷層掃描市場份額

眼科光學相干斷層掃描(OCT)產業主要由一些成熟企業主導,其中包括:

- 卡爾蔡司醫療科技公司(德國)

- 海德堡工程(德國)

- 拓普康公司(日本)

- 日本尼德克株式會社

- 佳能醫療系統(日本)

- Optovue(美國)

- 愛爾康(瑞士)

- 強生視力保健(美國)

- 博士倫(美國)

- 佳能(日本)

- Optos(英國)

- OptoVue(美國)

- 托米株式會社(日本)

- 卡爾蔡司(德國)

- Quantel Medical(法國)

- Optikon(義大利)

全球眼科光學相干斷層掃描市場最新進展

- In August 2023, Heidelberg Engineering launched an upgraded Spectralis OCT 2 platform, which incorporated enhanced imaging capabilities and deep-learning analysis tools to assist in more precise diagnosis and disease monitoring of glaucoma and other retinal conditions. This upgrade brought new software algorithms and improved hardware responsiveness that expanded clinical utility, particularly in large eye care centers and research hospitals. Adoption of Spectralis OCT 2 contributed to Heidelberg’s leadership in advanced ophthalmic imaging technologies

- In September 2023, Orbis International partnered with Heidelberg Engineering Inc. to expand vision services and training programs, including OCT education, especially in underserved regions. The partnership focused on enabling clinicians in developing countries to use advanced OCT technologies more effectively through webinars, funded teaching opportunities, and resource support. This collaboration enhanced OCT training outreach and supported broader global access to advanced ocular diagnostics

- In September 2023, Topcon Healthcare expanded its AI integration efforts in OCT by partnering with RetInSight GmbH, aiming to integrate RetInSight’s AI-based retinal biomarker analysis with Topcon’s OCT imaging systems. This collaboration sought to enhance the diagnostic precision and automated analysis capabilities of OCT devices, especially in chronic retinal disease screening workflows

- In June 2024, NIDEK Co., Ltd. launched its RS-1 Glauvas OCT system, a next-generation ophthalmic OCT device featuring 250 kHz scan speed and deep, wide-area imaging capabilities, along with integrated deep-learning analytics to assist clinicians in managing glaucoma and retinal diseases more effectively. The launch expanded NIDEK’s presence in high-performance imaging for eye care and demonstrated increasing industry emphasis on AI-assisted ocular diagnostics

- In May 2024, ZEISS Medical Technology announced enhancements to its CIRRUS 6000 OCT platform, including an expanded U.S. OCT reference database and enhanced cybersecurity features, strengthening its data-driven imaging solutions for ophthalmologists and enabling more secure and integrated clinical workflows. These enhancements reinforced the platform’s competitive edge in advanced retinal imaging and patient data handling

- In July 2024, Heidelberg Engineering received FDA clearance for the SPECTRALIS OCTA Module with SHIFT technology, which significantly reduced image acquisition times by up to 50% while delivering high-resolution OCT angiography imaging. This regulatory milestone expanded the clinical usability and adoption potential of advanced OCTA imaging in the U.S. market, supporting rapid vascular assessments in retinal disease management

- In May 2025, Intalight received CE Mark approval for its DREAM OCT platform, enabling commercialization throughout Europe. This next-generation swept-source OCT system offered ultrawide-field and super-depth imaging with integrated OCT angiography capabilities, enhancing retinal diagnostics and contributing to broader adoption of advanced OCT technologies in European ophthalmic practices

- In July 2024, EssilorLuxottica confirmed the acquisition of an 80% stake in Heidelberg Engineering, a major strategic consolidation that unified one of the world’s largest eyewear/eyecare services groups with a key OCT imaging technology provider. This acquisition (announced mid-2024 and finalized in late 2024) is expected to expand direct clinical channel access for OCT innovations through EssilorLuxottica’s global clinical and retail ecosystem

- In May 2025, Optos announced that global sales of its MonacoPro integrated ultra-widefield and OCT imaging solutions surpassed a major adoption milestone, reflecting strong clinical demand for combined imaging platforms that streamline workflow and improve diagnostic insights. Concurrently, Optos launched a comprehensive U.S. OCT/ultra-widefield imaging reference database to support AI-driven analysis and improved diagnostic precision in clinical settings

- In March 2025, Alcon announced its acquisition of Cylite, a developer of hyperparallel “whole-eye” OCT imaging intellectual property, signaling a strategic commitment to advancing full-eye OCT imaging capabilities for improved surgical planning and ophthalmic diagnostic workflows. This acquisition positions Alcon to integrate cutting-edge OCT IP into broader surgical and diagnostic portfolios

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。