Global Oxygen Free Copper Market

市场规模(十亿美元)

CAGR :

%

USD

30.90 Billion

USD

49.83 Billion

2024

2032

USD

30.90 Billion

USD

49.83 Billion

2024

2032

| 2025 –2032 | |

| USD 30.90 Billion | |

| USD 49.83 Billion | |

| % | |

|

全球无氧铜市场,按等级分列(无氧铜电子(Cu-OFE),无氧铜(Cu-OF)),产品(电线,脱口而出,罗德斯,布斯巴等),工业(电子和电气,汽车)——2032年工业趋势和预测

Oxygen-Free Copper Market Size

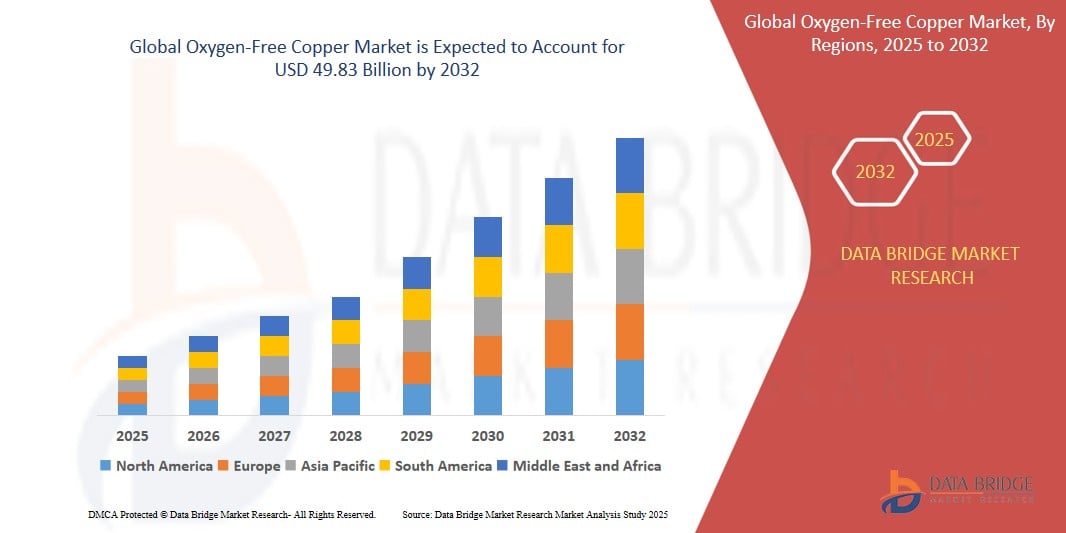

- The Global Oxygen-Free Copper Market size was valued atUSD 30.9 Billion in 2024 and is expected to reachUSD 49.83 Billion by 2032, at aCAGR of 4.13%during the forecast period

- This growth is driven by factors such as Increasing Demand for High-Quality Electrical Conductors and Technological Advancements in Copper Manufacturing

Oxygen-Free Copper Market Analysis

- Oxygen-Free Copper is widely used in high-performance electrical components such as connectors, conductors, and wiring, ensuring superior conductivity and minimal signal loss. It plays a crucial role in industries like telecommunications, automotive, and renewable energy.

- The demand for oxygen-free copper is driven by the rising need for high-quality conductors in electric vehicles (EVs), renewable energy systems, and consumer electronics, where efficiency and conductivity are paramount.

- North America is expected to dominate the Oxygen-Free Copper market due to its strong automotive and electronics sectors, along with continuous advancements in manufacturing technologies that improve the quality and availability of oxygen-free copper.

- The Asia-Pacific region is anticipated to be the fastest-growing market for oxygen-free copper, driven by rapid industrialization, increased investment in renewable energy, and a booming electronics industry.

- The electric vehicle segment is expected to lead the market, accounting for a significant share due to the high demand for oxygen-free copper in EV wiring, battery systems, and charging infrastructure, all requiring superior conductivity for optimal performance

Report Scope andOxygen-Free Copper Market Segmentation

|

Attributes |

Oxygen-Free Copper KeyMarket Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Oxygen-Free Copper Market Trends

“Advancements in Operating Microscopes & 3D Visualization for Intraocular Surgery”

- The oxygen-free copper market is witnessing significant growth, driven by increasing demand for high-quality electrical conductors across industries like automotive, electronics, and renewable energy. With the rise of electric vehicles (EVs), superior conductivity is crucial for wiring, battery systems, and charging infrastructure, thus boosting demand for oxygen-free copper. For instance, leading EV manufacturers like Tesla rely on these materials to enhance performance.

- Another trend is the growing adoption of renewable energy systems, including solar and wind power, where oxygen-free copper is essential for efficient energy transmission. The demand for this material will continue to rise as more countries invest in green technologies.

- Technological advancements in copper production, such as continuous casting and vacuum melting, are enhancing the efficiency and quality of oxygen-free copper, reducing costs, and making it more accessible for various high-demand applications.

For instance,

- Advancements in continuous casting technology have enabled companies like Wieland Group to produce oxygen-free copper more efficiently. This process reduces impurities and improves conductivity, allowing manufacturers to meet the growing demand in industries such as electric vehicles, where high-quality materials are essential for performance and durability.

Oxygen-Free Copper Market Dynamics

Driver

“Increasing Demand for High-Quality Electrical Conductors”

- The global shift towards renewable energy sources and electric vehicles has significantly boosted the demand for high-quality conductors. Oxygen-free copper, known for its superior conductivity and minimal oxidation, is the material of choice for these applications. As industries continue to adopt greener technologies, the need for oxygen-free copper will rise.

- Furthermore, the rising demand for consumer electronics, including smartphones and laptops, is also driving the need for oxygen-free copper. These products rely heavily on efficient power systems, where superior conductivity is essential for optimal performance. As technology advances, so does the demand for higher-quality materials.

- In addition, the automotive industry, especially electric vehicles, relies on oxygen-free copper for its wiring and electrical components. This demand is expected to surge as more automotive manufacturers prioritize electric vehicle production to meet environmental goals. Oxygen-free copper ensures durability and higher efficiency in these applications.

- The construction and infrastructure sectors are also contributing to the increased need for oxygen-free copper. With growing urbanization and the need for energy-efficient buildings, the material's properties make it ideal for electrical systems, lighting, and wiring in residential and commercial structures.

For instance,

- The increasing demand for high-quality electrical conductors is evident in the growing adoption of electric vehicles (EVs). EV manufacturers require oxygen-free copper for wiring and battery systems to ensure efficient power transmission and minimal energy loss, driving a surge in demand for superior conductors in the automotive sector.

Opportunity

“Growth in Renewable Energy Sector”

- The global shift toward renewable energy sources, such as solar and wind power, presents significant growth opportunities for the oxygen-free copper market. These energy systems require high-quality conductors to ensure efficient energy transmission and minimal loss. As renewable energy adoption continues to rise, the demand for oxygen-free copper will naturally follow.

- Moreover, the increased installation of electric grids and energy storage systems will further fuel the market's growth. Oxygen-free copper’s high conductivity and resistance to oxidation make it a crucial component in these advanced electrical infrastructures, opening up new opportunities for manufacturers and suppliers.

- The transition towards sustainable energy is also driving investments in green technologies and electric vehicles, all of which require superior materials like oxygen-free copper. As governments and corporations prioritize environmental sustainability, the market for this material will continue to expand.

- Oxygen-free copper is also essential in the development of more efficient battery technologies used in renewable energy systems. As energy storage technologies advance, so will the use of high-quality copper to support the transmission and storage of renewable energy.

Restraint/Challenge

“High Production Costs”

- Oxygen-free copper, due to its complex manufacturing process, is more expensive than conventional copper. The additional steps required to remove oxygen impurities, such as high-temperature refining and vacuum melting, lead to higher operational costs. This makes oxygen-free copper less cost-effective for industries seeking to minimize material costs.

- The higher price of oxygen-free copper could also hinder its adoption in price-sensitive markets, particularly in developing regions where cost efficiency is a critical factor. As industries in these areas opt for cheaper alternatives, the demand for oxygen-free copper may be limited.

- Additionally, the production costs are influenced by fluctuations in the price of raw copper and energy costs, further driving up the overall expense. Manufacturers may struggle to maintain competitive pricing while ensuring the high-quality standards required for oxygen-free copper.

- Despite its superior properties, the high production costs could deter small and medium-sized enterprises (SMEs) from using oxygen-free copper. This limits its widespread adoption, especially in industries with limited budgets for specialized materials.

Oxygen-Free Copper Market Scope

Oxygen-free copper market is segmented on the basis of grade, product and industry.

|

Segmentation |

Sub-Segmentation |

|

By Grade |

|

|

By Product |

|

|

By Industry |

|

In 2025, the Copper Oxygen-free Electronic (Cu-OFE) segmentis projected to dominate the market with a largest share in grade segment

In the Global Oxygen-Free Copper Market, the Copper Oxygen-free Electronic (Cu-OFE) grade is expected to dominate the market. This grade is highly sought after for its superior conductivity and is extensively used in high-performance electronics and electrical applications, including connectors, conductors, and circuit boards. Cu-OFE is known for its high purity, making it essential for industries requiring excellent electrical conductivity and minimal signal loss.

Thewireis expected to account for the largest share during the forecast period in product segment

In 2025, the wire in product segment is anticipated to hold the largest market share. Oxygen-free copper wire is critical for various applications, including in the automotive industry, electrical systems, and renewable energy solutions. Its demand is driven by the increasing use of advanced electrical systems in electric vehicles, consumer electronics, and power distribution.

Oxygen-Free Copper Market Regional Analysis

“North America Holds the Largest Share in the Oxygen-Free Copper Market”

- North America holds the largest share in the Oxygen-Free Copper Market due to its advanced manufacturing capabilities, high demand for precision electrical components in industries like electronics and aerospace, and the growing adoption of electric vehicles and renewable energy technologies.

- The U.S. holds a significant share in the Oxygen-Free Copper Market due to its advanced manufacturing infrastructure, high demand for high-quality conductors in electronics, automotive, and renewable energy sectors, and strong presence of key market players.

- The availability of well-established supply chains and increasing investments in electric vehicle (EV) production, smart grids, and renewable energy technologies further strengthen the market.

- Additionally, the growing adoption of electric vehicles and the demand for high-precision components in industries like telecommunications and aerospace is fueling market expansion across the region.

“Asia-Pacific is Projected to Register the Highest CAGR in the Oxygen-Free Copper Market”

- The Asia-Pacific region is expected to witness the highest growth rate in the Oxygen-Free Copper Market, driven by rapid industrialization, increased demand for electric vehicles (EVs), and expanding renewable energy projects.

- • Countries such as China, India, and Japan are emerging as key markets due to the booming automotive, electronics, and telecommunications sectors, which require high-quality conductors for improved performance and energy efficiency.

- • Japan, with its advanced manufacturing capabilities and focus on high-precision components for automotive and electronics industries, remains a crucial market for oxygen-free copper. The country continues to lead in the adoption of advanced materials to enhance product quality and functionality.

- • China and India, with their large industrial sectors and rising demand for smart grids, consumer electronics, and EVs, are witnessing increased investments in advanced manufacturing technologies. The growing presence of global manufacturers and government incentives further contribute to market growth in the region.

Oxygen-Free Copper Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- KME Germany GmbH & Co KG (Germany)

- Freeport-McMoRan (U.S.)

- KGHM (Poland)

- Zhejiang Libo Holding Group Co., Ltd. (China)

- Wieland Group (Germany)

- SOUTHWIRE COMPANY LLC (U.S.)

- Aviva Metals (U.S.)

- FURUKAWA ELECTRIC CO., LTD. (Japan)

- Hitachi Metals, Ltd. (Japan)

- Metrod Holdings Berhad (Malaysia)

- Mitsubishi Materials Corporation (Japan)

- Pan Pacific Copper Co., Ltd. (Japan)

- Sam Dong America (U.S.)

- Cupori Oy (Finland)

- Citizen Metalloys Limited (India)

- Farmer's Copper Ltd (U.S.)

- IBC Advanced Alloys Corp (Canada)

- Sequoia Brass & Copper (U.S.)

- Aurubis (Germany)

- Shanghai Metal Corporation (China)

- Hussey Copper (U.S.)

- Copper Braid Products (U.S.)

- Heyco Metals Inc (U.S.)

- MILLARD WIRE & SPECIALTY STRIP COMPANY (U.S.)

Latest Developments in Global Oxygen-Free Copper Market

- In November 2023, SK Nexilis commenced production of ultra-thin oxygen-free copper (4 microns) at its new facility in Malaysia, with an annual capacity of 57,000 tons. This $690 million investment aims to meet the growing demand for high-conductivity materials in electronics and automotive sectors.

- In April 2023, SPSX, a U.S.-based wire company, acquired L&K, a European producer of oxygen-free copper. This acquisition enhances SPSX's position in the electric vehicle supply chain by providing high-efficiency windings for drive motors and securing a reliable supply of oxygen-free copper for EV components.

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。