Global Tank Insulation Market

市场规模(十亿美元)

CAGR :

%

USD

3.84 Billion

USD

10.30 Billion

2024

2032

USD

3.84 Billion

USD

10.30 Billion

2024

2032

| 2025 –2032 | |

| USD 3.84 Billion | |

| USD 10.30 Billion | |

| % | |

|

全球罐体绝缘市场分化,按类型(储油层和运输)、材料类型(扩大的聚苯乙烯(EPS)、Rockwool、Cellulular Glass、Fiberglass、Elastomic Foam、Polyurethane(PU等)、温度类型(热绝缘和冷绝缘)、坦克类型(Vertical Tank、横向坦克、固定坦克和挂载坦克)、坦克端口(Parabolic Dish和平地)、最终用户(Oil & Gas、能源和电力、化学、食品和饮料、水净化、废水净化等) -- -- 工业趋势和预测至2032年

Tank Insulation Market Size

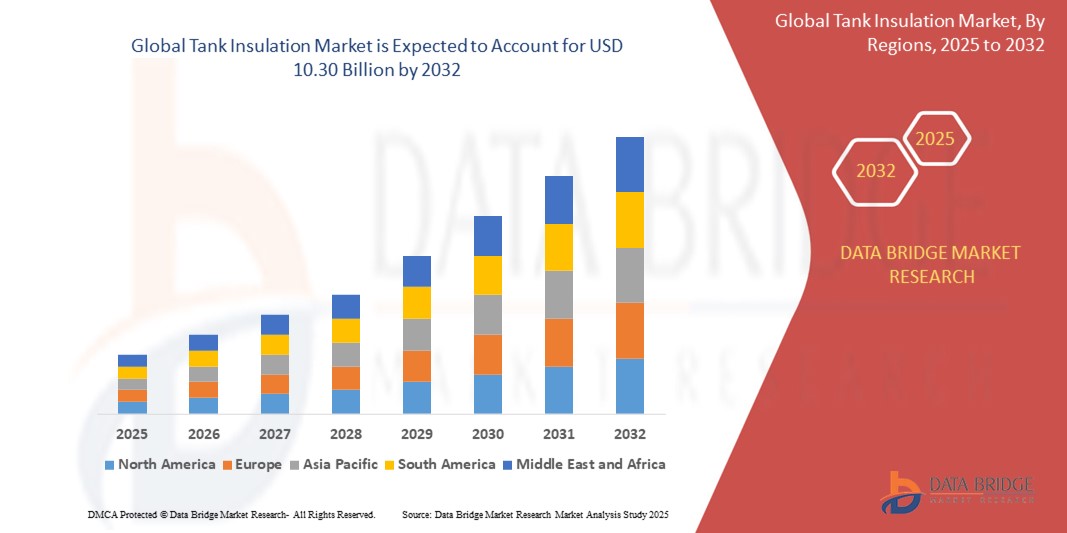

- The global tank insulation market size was valued atUSD 3.84 billion in 2024and is expected to reachUSD 10.30 billion by 2032, at aCAGR of 5.25%during the forecast period

- This growth is driven by factors such as the increasing demand for energy-efficient insulation solutions in industries such as oil & gas, energy, and chemicals

Tank Insulation Market Analysis

- Tank insulation is defined as the process in which different chemicals and materials are applied to the inside of tank and also to the surface, to maintain the temperature throughout its usage period

- Tank insulation is done to preserve the temperature inside the tank in order to minimize the heat loss

- North America is expected to dominate the tank insulations market due to its advanced infrastructure and continuous focus on technological innovations in insulation materials

- Asia-Pacific is expected to be the fastest growing region in the tank insulation market during the forecast period due to rapid industrialization and urbanization, which is driving significant demand for tank insulation solutions

- Rockwool and polyurethane (PU) segment is expected to dominate the market with a market share of 31.5% due to their high thermal insulation properties and versatility. These materials are widely used in industries such as oil and gas, chemicals, and energy due to their excellent ability to maintain the required temperature levels while ensuring energy efficiency

Report Scope and Tank Insulation Market Segmentation

|

Attributes |

Tank Insulation Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Tank Insulation Market Trends

“Advancements in Sustainable Insulation Materials”

- In recent years, there has been a significant trend towards the use of sustainable and eco-friendly insulation materials in tank insulation. Industries are increasingly focused on minimizing their environmental footprint and improving energy efficiency. Manufacturers are developing insulation solutions that are not only thermally efficient but also made from renewable or recyclable materials

- For Instance, Rockwool International A/S, which has been at the forefront of developing insulation products made from sustainable materials. Their mineral wool insulation solutions are designed to be highly energy-efficient while being recyclable, aligning with growing global sustainability goals

- The transition to a circular economy is influencing the tank insulation market. Companies are investing in materials that can be reused or recycled, reducing waste and fostering sustainability in the supply chain

- Many governments around the world are implementing stricter regulations related to energy efficiency in industrial sectors. This is pushing companies to adopt more advanced and sustainable insulation solutions that reduce energy consumption and improve temperature control for storage tanks

- Manufacturers of tank insulation are increasingly obtaining environmental certifications for their products, ensuring compliance with international standards such as LEED (Leadership in Energy and Environmental Design) and BREEAM (Building Research Establishment Environmental Assessment Method)

Tank Insulation Market Dynamics

Driver

“Increasing Energy Efficiency Demands”

- The primary driver of growth in the global tank insulation market is the increasing demand for energy efficiency. Insulated tanks help reduce energy loss during the storage and transportation of liquids, gases, and chemicals by maintaining temperature control. This is especially critical in sectors such as oil and gas, chemicals, and food processing, where temperature-sensitive materials are involved

- As the global energy crisis intensifies, industries are under pressure to optimize their energy consumption. Tank insulation solutions help minimize energy waste by maintaining the desired temperature, leading to significant energy savings

- Governments are implementing stricter regulations regarding energy use, particularly in high-consumption industries.

- For instance, the European Union's Energy Efficiency Directive mandates the reduction of energy use across industries, pushing companies to adopt solutions such as tank insulation to comply with these regulations

- Tank insulation reduces the need for additional energy resources by preventing heat loss or gain. This directly results in lower energy bills for companies that adopt these solutions, making it a cost-effective measure

- The oil and gas industry is one of the largest consumers of insulated tanks. With the growing focus on reducing operational costs, the demand for advanced insulation solutions is surging to ensure that thermal energy is not wasted during storage and transportation processes

Opportunity

“Growth in Emerging Markets”

- Emerging markets, particularly in regions such as Asia-Pacific, Latin America, and the Middle East, offer significant growth opportunities for the global tank insulation market. As these regions industrialize at a rapid pace, there is an increasing demand for tank insulation solutions across various sectors, including chemicals, oil and gas, and pharmaceuticals

- Countries in the Middle East and Asia are investing heavily in infrastructure development, including energy production and petrochemical plants. This creates opportunities for the tank insulation market, as these facilities require highly efficient thermal insulation for storage tanks to optimize energy use

- Governments in emerging markets are encouraging foreign investments and providing incentives for companies to adopt energy-efficient technologies. These incentives are a key opportunity for manufacturers of tank insulation solutions to expand their reach in these regions

- As renewable energy projects such as wind, solar, and bioenergy grow in emerging markets, there is an increasing need for efficient storage solutions. Insulated tanks are crucial in ensuring that energy storage systems function optimally, which presents an opportunity for insulation companies to cater to the renewable energy sector

- The growing food processing and pharmaceutical industries in emerging markets create new opportunities for tank insulation providers, as these industries require insulated storage tanks for temperature-sensitive materials

Restraint/Challenge

“High Initial Investment Costs”

- The installation of advanced tank insulation systems, particularly those made from high-performance materials, involves significant upfront capital investment. For many small and medium-sized enterprises (SMEs), this high initial cost can be a major barrier to adopting tank insulation solutions

- The return on investment (ROI) for insulated tanks, although positive in terms of energy savings, can take several years to materialize. This long payback period discourages many companies from making the initial investment, especially in industries with tighter profit margins

- Retrofitting existing tanks with new insulation systems can be complex and costly. Many companies face challenges when integrating insulation into their pre-existing infrastructure, leading to higher operational costs during the installation process

- The prices of raw materials used in insulation, such as fiberglass, mineral wool, and polyurethane, can fluctuate significantly. This price volatility can increase the overall cost of insulation systems and create uncertainty in the market

- In some developing regions, the awareness of the benefits of tank insulation is still low. Companies may not fully realize the long-term energy savings and operational efficiency gains that can be achieved through proper insulation, which limits market growth in these areas

Tank Insulation Market Scope

The market is segmented on the basis type, material type, temperature type, tank type, tank ends, and end-user.

|

Segmentation |

Sub-Segmentation |

|

By Type |

|

|

By Material Type |

|

|

By Temperature Type |

|

|

By Tank Type |

|

|

By Tank Ends |

|

|

By End-User |

|

In 2025, the rockwool and polyurethane (PU) is projected to dominate the market with a largest share in material type segment

The rockwool and polyurethane (PU) segment is expected to dominate the tank insulation market with the largest share of 31.5% in 2025 due to their high thermal insulation properties and versatility. These materials are widely used in industries such as oil and gas, chemicals, and energy due to their excellent ability to maintain the required temperature levels while ensuring energy efficiency.

The hot insulation is expected to account for the largest share during the forecast period in temperature market

In 2025, the got insulation segment is expected to dominate the market with the largest market share of 51.31% due to preventing heat loss and protecting equipment, ensuring that industrial processes remain within safe temperature limits. Hot insulation solutions help companies save on heating costs and reduce energy consumption, making this a highly demanded segment across various industries.

Tank Insulation Market Regional Analysis

“North America Holds the Largest Share in the Tank Insulation Market”

- North America remains a dominant player in the global tank insulation market due to its advanced infrastructure and continuous focus on technological innovations in insulation materials. The region is home to a highly developed chemical, oil & gas, and energy sector, all of which rely heavily on insulated tanks for storage and transportation of liquids and gases

- Stringent regulations related to energy efficiency and safety standards have prompted companies in North America to adopt tank insulation solutions. These regulations not only ensure operational safety but also contribute to energy conservation and reduction of carbon footprints

- The oil & gas sector, especially in the U.S. and Canada, is a major consumer of tank insulation, where insulated tanks are essential to maintaining temperature control for both storage and transportation. The sector's growth, driven by the need for storage tanks for crude oil and natural gas, further bolsters market demand

- North America has well-established manufacturing capabilities for tank insulation materials such as polyurethane, polystyrene, and fiberglass, enabling a strong supply chain to meet local and international demand

- Increasing investments in energy efficiency across various industries, especially in power generation and industrial manufacturing, have further driven the demand for insulated tanks in this region, making North America a market leader

“Asia-Pacific is Projected to Register the Highest CAGR in the Tank Insulation Market”

- The Asia-Pacific region, particularly countries such as China, India, and South Korea, is experiencing rapid industrialization and urbanization, which is driving significant demand for tank insulation solutions. Industries such as chemicals, oil & gas, and food processing are growing rapidly, creating a high need for insulated tanks

- Several governments in APAC are focusing on enhancing industrial infrastructure, which includes the construction of storage facilities and refineries that require tank insulation solutions. Government incentives for energy-efficient solutions and compliance with environmental regulations are contributing to the region's growth in this market

- As energy consumption in the region rises, particularly in emerging economies such as India and China, there is a growing need to store and transport energy-efficient materials, requiring the installation of insulated tanks to maintain temperature stability and minimize energy losses

- APAC is seeing significant growth in its petrochemical industry, with major projects coming online, particularly in countries such as China and India. These industries are among the biggest consumers of tank insulation systems to store chemicals at safe temperatures

- The adoption of more affordable and locally manufactured insulation materials, such as fiberglass and mineral wool, is driving market growth in the APAC region. The lower costs of production and raw materials have made insulated tank solutions more accessible to a larger number of companies in this region

Tank Insulation Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Commercial Thermal Solutions, Inc. (U.S.)

- Dow(U.S.)

- GILSULATE INTERNATIONAL, INC. (U.S.)

- ITW INSULATION SYSTEMS(U.S.)

- J.H. Ziegler GmbH(Germany)

- Knauf Insulation (U.S.)

- PolarClad Tank Insulation (U.S.)

- ARMACELL LLC (U.S.)

- Kingspan Group (Ireland)

- Synavax (U.S.)

- Johns Manville (U.S.)

- Mayes Coatings & Insulation, Inc. (U.S.)

- Thermacon (U.S.)

- Gulf Cool Therm Factory LTD (UAE)

- ROCKWOOL International A/S (Denmark)

- Cabot Corporation (U.S.)

- SPX Transformer Solutions Inc. (U.S.)

- DUNMORE (U.S.)

- T.F. Warren Group (U.S.)

- Saint-Gobain (France)

- Huntsman International LLC (U.S.)

- Corrosion Resistant Technologies, Inc. (U.S.)

- Röchling (Germany)

Latest Developments in Global Tank Insulation Market

- In May 2025, Rockwool International A/S Expands Product Line, the new products are designed with improved fire resistance and better thermal performance, catering to industries with stringent regulatory requirements

- In March 2025, Dow Launches New Polyurethane-Based Insulation, designed to enhance the performance and energy efficiency of tank insulation systems. The new product features improved thermal resistance properties and lower environmental impact due to the use of renewable materials

- In January 2025, Knauf Insulation Partners with Large Industrial Clients, to supply tank insulation materials for large-scale oil and gas refineries and chemical plants. The collaboration aims to enhance the energy efficiency of storage and transportation tanks used in these industries

- In December 2024, ITW Insulation Systems Launches Advanced Insulation Solutions for High-Temperature Applications, designed for hot tanks in the petrochemical industry. The products feature enhanced resistance to thermal stress and are designed to improve energy conservation in high-demand environments

- In September 2024, Johns Manville Introduces Recyclable Insulation Products, made from sustainable materials. These products are aimed at companies looking to reduce their environmental impact while maintaining high insulation performance

- In June 2024, Armacell LLC Expands Operations in Asia-Pacific, expanded its operations in the Asia-Pacific region by opening a new production facility in India. This facility will cater to the growing demand for tank insulation in industries such as oil & gas and chemicals

SKU-

目录

表2. 全球市场

导言

1.1 研究1.2市场定义的目标 1.3 全球市场概况 1.4 价格和定价 1.5 限额 1.6 市场覆盖

2个市场部分

2.1 市场涵盖2.2个地理范围 2.3年,用于研究 2.4 成本和价格 2.5 底盘数据估价模型 2.6 技术生命线模型 2.7 多维模型 2.8 初步访问 关键操作导师 2.9 底盘市场定位 2.10 市场应用

3个市场概况

3.1 驾驶员

3.1.1 从石油和气体工业中引入需求 3.1.2 在液化贮存和运输中不断增长的

3.2 障碍

3.2.1 推进放射性物质价格 3.2.2 通过制造原料3.2.3 无法生产原料,使工业在坦克克储存移动金属 3.2.4 化学原料在化学工业中自由扩散

3.3 机会

3.3.1 中国和印度种植植物制药业对塔克的高度需求 3.3.2 在水中塔克制造材料的不断增长的需求,用于多种品种和商用建筑 3.3.3 在新兴产业中鼓励工业

3.4 挑战

3.4.1 在坦克制造材料的火灾和对化学反应的爆炸 3.4.2 制造材料的健康危害

4 执行摘要 5 序言 6种工业特征 按类型分列的7个全球坦克证券市场

7.1 概述 7.2 储存 7.3 运输

按材料类型分列的8个全球坦克证券市场

8.1 概述 8.2 聚苯乙烯(EPS) 8.3 罗克沃克 8.4 CELLLLAR GLAS 8.5 FIBERGLAS 8.6 聚苯乙烯(PU) 8.7 其他

9 按期分列的全球坦克证券市场

9.1 概述 9.2 危险事件 9.3 危险事件

按坦克类型分列的10个全球坦克入侵市场

10.1 概述 10.2 铁罐体 10.3 直径 10.4 固定铁罐体 10.5 模拟铁罐体

11 坦克入侵市场,按坦克ENDS

11.1 概述 11.2 PARABOLIC DISH 11.3 FLAT

12 按最终用户分列的全球坦克证券市场

12.1 概述 12.2 石油和气体

12.2.1 石油工业

12.2.1.1 铁矿石 12.2.1.2 其他铁矿石

12.2.2 气体

12.2.2.1 天然气体 12.2.2.2 合成气体

12.3 能源和动力 12.4 化学 12.5 食物和饮料

12.5.1 食物 12.5.2 饮料

12.5.2.1 酒精饮料 12.5.2.2 酒类 12.5.2.3 饮料 12.5.2.4 酒类和氟水 12.5.2.5 其他

12.6 用水

12.6.1 商业建筑 12.6.2 博物馆 12.6.3 建筑

12.7 废水净化

12.7.1 商业建筑 12.7.2 博物馆 12.7.3 建筑

12.8 其他人员

13 按格鲁吉亚分列的全球坦克起义市场

13.1 概况 13.2 北美

13.2.1 美国 13.2.2 加拿大 13.2.3 墨西哥

13.3 欧洲

13.3.1 德国 13.3.2 英国 13.3.3 法国 13.3.4 法国 13.3.5 西班牙 13.3.6 瑞士 13.3.7 俄罗斯 13.3.8 土耳其 13.3.9比利时 13.3.10 荷兰 13.3.11 剩余欧元

13.4 亚太

13.4.1 中国 13.4.2 印度 13.4.3 韩国 13.4.4 日本 13.4.5 澳大利亚 13.4.6 新加坡 13.4.7 泰国 13.4.8 印度 13.4.9 马来西亚 13.4.10 菲律宾 13.4.11 亚洲-太平洋

13.5 南美洲

13.5.1 巴西 13.5.2 阿根廷 13.5.3 南美洲南部

13.6 中东和非洲

13.6.1 阿联酋 13.6.2 沙特阿拉伯 13.6.3 以色列 13.6.4 南部非洲 13.6.5 埃及 13.6.6

14 坦克公司全球保险市场,公司土地

14.1 公司共享分析:全球 14.2 公司共享分析:北美 14.3 公司共享分析:欧洲 14.4 公司共享分析:亚洲-太平洋 14.5 市场和市场分析 14.6 新的产品开发和核准 14.7 伙伴关系和其他战略发展

15个公司简介

15.1 萨斯克

15.1.1 公司会计 15.1.2 软分析 15.1.3 恢复分析 15.1.4 公司共享分析 15.1.5 地球物理环境 15.1.6 出产PortFOLIO 15.1.7 最新发展 15.1.8 数据基础市场研究分析 15.1.8

15.2 DOW化学公司

15.2.1 公司会计 15.2.2 系统分析 15.2.3 恢复分析 15.2.4 公司共享分析 15.2.5 地球物理环境 15.2.6 生产PORFOLIO 15.2.7 最新发展 15.2.8 数据基础市场研究分析 15.2.8

15.3 萨摩亚

15.3.1 公司会计 15.3.2 系统分析 15.3.3 恢复分析 15.3.4 公司共享分析 15.3.5 地球科学调查 15.3.6 生产港口 15.3.7 最新发展 15.3.8 数据基础市场研究分析

15.4 胡图斯曼国际书记处

15.4.1 公司会计 15.4.2 系统分析 15.4.3 恢复分析 15.4.4 公司共享分析 15.4.5 地球物理环境 15.4.6 生产移植材料 15.4.7 最近的发展 15.4.8 数据基础市场研究分析

15.5 国王集团

15.5.1 公司会计 15.5.2 系统分析 15.5.3 恢复分析 15.5.4 公司共用分析 15.5.5 地球物理环境 15.5.6 生产材料 15.5.7 最新发展情况 15.5.8 数据分析市场分析

15.6 军火销售有限责任公司

15.6.1 公司会计 15.6.2 恢复分析 15.6.3 地理环境 15.6.4 生产材料 15.6.5 最新动态

15.7 行政办公室

15.7.1 公司会计 15.7.2 恢复分析 15.7.3 地理环境 15.7.4 生产港口 15.7.5 最新发展情况

15.8 商业热液溶液,INC.

15.8.1 公司会计 15.8.2 生产

15.9 综合技术。

15.9.1 公司会计 15.9.2 产品组合 15.9.3 最近的发展

15.10 邓莫雷

15.10.1 公司会计 15.10.2 地理环境 15.10.3

15.11 国际、尼加拉瓜妇女理事会。

15.11.1 公司会计学 15.11.2 产品组合 15.11.3 最新动态

15.12 古尔弗·科尔·特克特尔(LTD)

15.12.1 公司会计 15.12.2 生产

15.13 岩溶系统

15.13.1 公司会计学 15.13.2 地理环境 15.13.3 生产港口 15.13.4 最新动态

15.14 乔汉斯·曼维尔

15.14.1 公司会计 15.14.2 地理环境 15.14.3 生产 港口 15.14.4 最新动态

15.15 J.H. ZIEGLLER GMBH

15.15.1 公司会计 15.15.2 地理环境 15.15.3 生产

15.16 KNAUF 起义

15.16.1 公司会计 15.16.2 地理环境 15.16.3 生产

15.17 Mays Coatings & Insulaction, INC. 互联网档案馆的存檔,存档日期2013-12-21.

15.17.1 公司会计制度 15.17.2 产品组合 15.17.3 最新动态

15.18 OWENS 旋转

15.18.1 公司会计 15.18.2 恢复分析 15.18.3 地理环境 15.18.4

15.19 POLARCLAD TANK 起义

15.19.1 公司会计 15.19.2 生产

15.20 罗克林集团

15.20.1 公司会计制度 15.20.2 地理环境 15.20.3 生产

15.21 国际公路运输协会

15.21.1 公司会计制度 15.21.2 恢复分析 15.21.3 地理环境 15.21.4 生产材料 15.21.5 最新动态

15.22 SPX变相解决办法

15.22.1 公司会计制度 15.22.2 产品组合 15.22.3 最新动态

15.23 锡纳瓦克斯

15.23.1 公司会计 15.23.2 溶剂组合 15.23.3 最新动态

15.24 瑟玛康

15.24.1 公司会计 15.24.2 产品组合 15.24.3 最近的发展

15.25 T.F.瓦伦集团

15.25.1 公司会计 15.25.2 地理环境 15.25.3 生产 15.25.4 最新发展情况

16 问 题 17 结论 18份有关报告

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。