Global Vegetable Parchment Paper Market

市场规模(十亿美元)

CAGR :

%

USD

1.42 Billion

USD

2.40 Billion

2024

2032

USD

1.42 Billion

USD

2.40 Billion

2024

2032

| 2025 –2032 | |

| USD 1.42 Billion | |

| USD 2.40 Billion | |

| % | |

|

全球蔬菜羊皮紙市場細分,按產品類型(漂白、天然、樹脂處理等)、應用(食品、造紙工業等)、分銷渠道(大賣場、超市、專賣店、網店等)、類型(30-40 gsm、40-50 gsm 等)、分類(普通蔬菜羊皮紙和矽化地羊皮紙(正宗羊皮紙)- 行業 2032 年與正宗羊皮紙)

植物羊皮紙市場規模

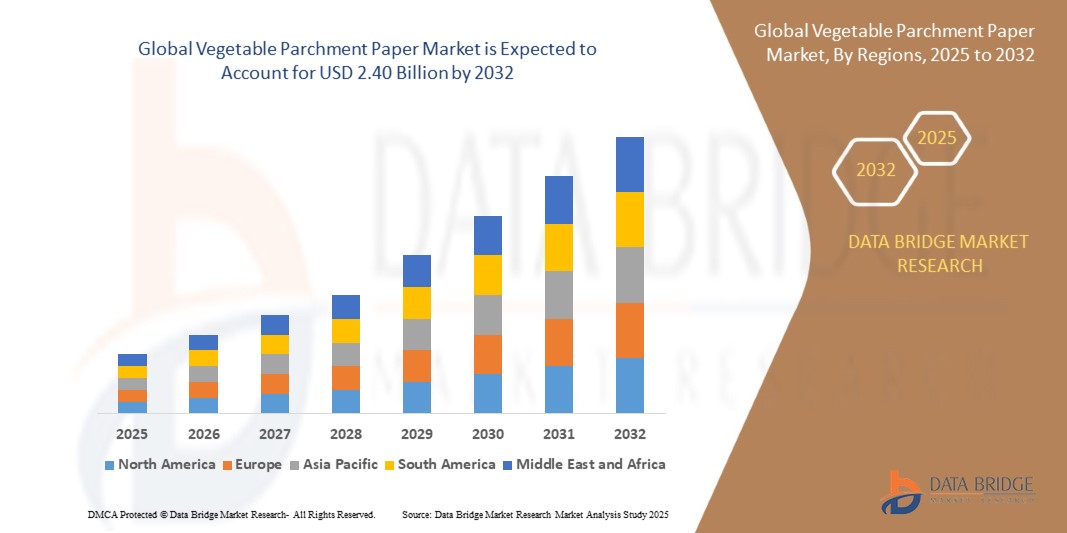

- 2024 年全球植物羊皮紙市場規模為14.2 億美元 ,預計 到 2032 年將達到 24 億美元,預測期內 複合年增長率為 6.80%。

- 市場成長主要得益於食品加工、烘焙和糖果產業對永續、不沾黏和耐油包裝解決方案日益增長的需求

- 消費者環保意識的增強,加上對塑膠使用和一次性包裝材料的嚴格監管,正在推動人們轉向可生物降解的替代品,例如植物羊皮紙

植物羊皮紙市場分析

- 蔬菜羊皮紙市場因其可堆肥、防潮、耐熱的特性而受到廣泛關注,使其成為食品級應用的理想選擇

- 烘焙和即食食品包裝的需求尤其強勁,其中羊皮紙用於烤盤、包裝和襯紙

- 受可持續和可生物降解食品包裝材料廣泛使用的影響,北美在 2024 年佔據植物羊皮紙市場主導地位,收入份額最大

- 受食品加工產業擴張、環保包裝需求成長以及快速城市化推動,亞太地區預計將成為全球植物羊皮紙市場成長率最高的地區

- 漂白羊皮紙在2024年佔據了市場主導地位,收入份額最大,這得益於其外觀潔淨、阻隔性強,廣泛應用於商業烘焙和食品包裝。食品業青睞漂白羊皮紙,因為它能夠滿足衛生標準並具有耐熱性,尤其是在烘焙和糖果領域。人們對專業級烘焙用品的日益青睞也推動了其在零售和工業通路的高需求。

報告範圍和植物羊皮紙市場細分

|

屬性 |

植物羊皮紙關鍵市場洞察 |

|

涵蓋的領域 |

|

|

覆蓋國家 |

北美洲

歐洲

亞太

中東和非洲

南美洲

|

|

主要市場參與者 |

|

|

市場機會 |

|

|

加值資料資訊集 |

除了對市場價值、成長率、細分、地理覆蓋範圍和主要參與者等市場情景的洞察之外,Data Bridge Market Research 策劃的市場報告還包括進出口分析、生產能力概覽、生產消費分析、價格趨勢分析、氣候變遷情景、供應鏈分析、價值鏈分析、原材料/消耗品概覽、供應商選擇標準、PESTLE 分析、波特分析和監管框架。 |

植物羊皮紙市場趨勢

“人們越來越青睞環保、無毒的烘焙解決方案”

- 消費者和餐飲服務業者越來越多地選擇可生物降解且不含氯的羊皮紙作為塑膠內襯的更安全替代品。這種轉變在註重健康和環保的地區尤其明顯。

- 清潔標籤運動和對無毒包裝的需求正在推動人們對未漂白羊皮紙的興趣,尤其是對於有機和手工烘焙食品

- 餐飲服務提供者正在用可堆肥的羊皮紙取代矽膠紙和塑膠塗層紙,以符合永續發展承諾和政府要求

- 加拿大和歐洲部分地區實施的禁止使用一次性塑膠的規定正在加速環保羊皮紙材料的採用

- For instance, in France, multiple commercial bakery chains have switched to chlorine-free parchment rolls to meet eco-label requirements and avoid penalties on plastic packaging waste

Vegetable Parchment Paper Market Dynamics

Driver

“Sustainability and Food Safety Driving Market Demand”

- Rising awareness about food safety, combined with global sustainability goals, is significantly boosting demand for vegetable parchment paper. It offers a hygienic, non-stick surface ideal for baking and cooking

- Derived from natural cellulose and free from chemical additives, vegetable parchment paper aligns with both consumer health priorities and regulatory food contact standards

- Its compostable and grease-resistant properties make it suitable for high-temperature applications and eco-friendly packaging, especially in commercial baking environments

- Manufacturers of frozen and ready-to-eat meals are increasingly turning to vegetable parchment paper to prevent sticking and contamination during food processing and storage

- For instance, bakery chains in Germany and Japan now use vegetable parchment paper in mass production to comply with both EU food safety standards and corporate sustainability benchmarks

Restraint/Challenge

“High Cost of Production and Limited Raw Material Availability”

- The processing of vegetable parchment paper involves specialized treatment and refining steps that increase energy and operational costs, making it less affordable for small producers

- Fluctuating availability and rising costs of sustainable cellulose pulp—its primary raw material—pose supply chain and pricing challenges, particularly in developing markets

- Compared to plastic and wax-based papers, vegetable parchment paper remains expensive, limiting its competitiveness in bulk-use segments such as street fod and takeaway services

- Many small food vendors and bakeries in cost-sensitive regions are hesitant to switch due to the higher upfront investment, despite environmental benefits

- For instance, street vendors across Southeast Asia continue to use low-cost polyethylene sheets instead of vegetable parchment paper due to affordability and lack of bulk supply access

Vegetable Parchment Paper Market Scope

The market is segmented on the basis of product type, application, distribution channel, type, and classification.

• By Product Type

On the basis of product type, the vegetable parchment paper market is segmented into bleached, natural, resin treated, and others. The bleached segment dominated the market with the largest revenue share in 2024, driven by its widespread use in commercial baking and food packaging due to its clean appearance and strong barrier properties. The food industry prefers bleached parchment for its ability to meet hygiene standards and support heat resistance, especially in bakery and confectionery applications. The rising preference for professional-grade baking supplies has also contributed to its high demand across retail and industrial channels.

The resin treated segment is expected to witness the fastest growth rate from 2025 to 2032, owing to its enhanced grease resistance and durability. This variant is especially popular in processed food and fast food packaging, offering superior performance under high-temperature conditions. Its rising use in specialty food wraps and microwaveable products is further boosting segment growth globally.

• By Application

On the basis of application, the vegetable parchment paper market is segmented into food, paper industry, and others. The food segment held the largest revenue share in 2024, primarily due to its extensive use in baking, cooking, and food wrapping applications. The shift toward eco-friendly, non-toxic food-contact materials has made vegetable parchment paper a favored choice in both home kitchens and professional bakeries. Its compostable and grease-resistant properties make it ideal for sustainable food packaging solutions.

The paper industry segment is expected to witness the fastest growth rate from 2025 to 2032, driven by increasing use in specialty printing and industrial laminates. The need for high-performance, biodegradable barrier papers in packaging, printing, and labelling is creating new opportunities for vegetable parchment paper in paper processing applications.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into hypermarkets, supermarkets, specialty stores, online stores, and others. The specialty stores segment accounted for the largest share in 2024, supported by the preference of food professionals and bakeries for premium, niche parchment brands. Specialty retailers offer a wide range of high-performance options including unbleached, silicone-coated, and embossed parchment varieties that cater to specific end uses.

The online stores segment is expected to witness the fastest growth rate from 2025 to 2032, due to the increasing adoption of e-commerce platforms for purchasing baking and packaging supplies. Consumers value the convenience of bulk ordering, variety, and access to international parchment brands via digital marketplaces, particularly in urban and semi-urban regions.

• By Type

On the basis of type, the vegetable parchment paper market is segmented into 30–40 gsm, 40–50 gsm, and others. The 40–50 gsm segment held the dominant share in 2024, as it is commonly used across a wide range of food applications, including lining baking trays, wrapping greasy items, and separating frozen foods. This thickness provides an ideal balance between strength, heat resistance, and flexibility for both domestic and industrial use.

The 30–40 gsm segment is expected to witness the fastest growth rate from 2025 to 2032, driven by rising demand for lightweight, eco-friendly food wrapping solutions in quick-service restaurants and fast-moving consumer goods. The reduced material usage and cost-effectiveness of lighter parchment contribute to its increasing popularity in emerging markets.

• 依分類

根據分類,市場細分為普通植物羊皮紙和矽化真材植物羊皮紙。普通植物羊皮紙在2024年佔據了最大的市場份額,這得益於手工烘焙店和零售食品包裝對可堆肥、不沾紙的需求不斷增長。其成本效益高且符合清潔標籤包裝趨勢,使其成為中小型企業的首選。

矽化真植物羊皮紙市場預計將在2025年至2032年期間實現最快的成長,這得益於其卓越的耐熱性、可重複使用性和防黏性。這一市場在尋求高性能、環保包裝材料的商業烘焙店、高端食品品牌和餐包供應商中越來越受歡迎。

植物羊皮紙市場區域分析

- 受可持續和可生物降解食品包裝材料廣泛使用的影響,北美在 2024 年佔據植物羊皮紙市場主導地位,收入份額最大

- 該地區受益於烘焙和加工食品行業的強勁需求,植物羊皮紙因其耐油和耐熱特性而受到青睞

- 北美消費者越來越多地尋求可堆肥、清潔標籤的包裝替代品,這符合環境法規和品牌永續發展目標

美國植物羊皮紙市場洞察

2024年,美國植物烘焙紙市場佔據北美最大的收入份額,這得益於商業烘焙行業的蓬勃發展以及對環保食品包裝紙和烘焙襯墊日益增長的需求。美國強勁的加工食品產業和強大的手工烘焙企業是市場成長的關鍵驅動力。此外,消費者對零售和家庭烘焙中有機、無毒包裝材料的偏好日益增長,也促使製造商擴大其烘焙紙產品線。

歐洲植物羊皮紙市場洞察

預計歐洲植物羊皮紙市場將在2025年至2032年期間實現最快的成長,這得益於該地區監管部門強調減少一次性塑膠使用,並推廣可回收和可堆肥的替代品。食品級羊皮紙在烘焙、乳製品和即食食品領域的應用日益廣泛。對循環經濟實踐的日益支持以及有機食品的普及,進一步提升了植物羊皮紙在法國、德國和義大利等國家的吸引力。

英國植物羊皮紙市場洞察

預計英國植物羊皮紙市場將在2025年至2032年間實現最快成長,這得益於零售和餐飲服務業對永續食品包裝需求的不斷增長。超市和專賣店正在擴大其產品線,推出環保替代品,其中包括未漂白和矽化處理的植物羊皮紙。英國各地手工烘焙和無麩質烘焙店的激增,進一步促進了高品質羊皮紙解決方案的普及。

德國植物羊皮紙市場洞察

預計2025年至2032年間,德國植物羊皮紙市場將迎來最快的成長速度,這得益於其強大的環保意識和消費者對食品級包裝的高期望。德國重視食品生產中可生物降解和可回收材料的使用,並制定了嚴格的食品安全標準,這使得工業烘焙和家庭應用對植物羊皮紙的需求強勁。此外,德國包裝產業正越來越多地將植物羊皮紙納入其永續創新管道。

亞太植物羊皮紙市場洞察

受食品安全問題日益嚴重、包裝食品消費成長以及城鎮化進程加快的推動,亞太地區植物羊皮紙市場預計將在2025年至2032年間實現最快成長。中國、印度、日本和韓國等國家在烘焙、零食包裝和乳製品領域對植物羊皮紙的使用日益增加。該地區快餐店 (QSR) 和國內烘焙連鎖店的快速擴張也加速了羊皮紙的使用,以促進衛生和永續發展。

日本植物羊皮紙市場洞察

預計日本植物羊皮紙市場將在2025年至2032年間實現最快成長,因為消費者越來越重視食品包裝的清潔、安全和環保。羊皮紙廣泛應用於烘焙和糖果行業,傳統糖果(和果子)領域也越來越受到青睞。日本成熟的包裝產業和對食品外觀的文化重視,正鼓勵食品生產商在日常生產中轉向美觀且可生物降解的羊皮紙材料。

中國植物紙市場洞察

2024年,中國植物油紙市場佔據亞太地區最大收入份額,這得益於烘焙產品消費的成長以及中國向綠色包裝解決方案的轉變。隨著政府在「綠色發展」倡議下大力推廣永續食品包裝,對可堆肥和無毒植物油紙的需求日益增長。國內植物油紙製造商正在擴大產量,以滿足本土食品加工商和注重環保供應鏈的國際出口商的需求。

植物羊皮紙市場份額

植物羊皮紙產業主要由知名公司主導,其中包括:

- 雷諾消費品(美國)

- 帕特森太平洋羊皮紙公司(美國)

- Amol Paper Mills Pvt. Ltd(印度)

- 卡爾帕塔魯(印度)

- Livriite Ventures(印度)

- JK紙業(印度)

- 黑標紙業公司(美國)

- 北歐紙業(瑞典)

- 樂購(英國)

- Ahlstrom-Munksjö(芬蘭)

- Pudumjee 紙製品公司(印度)

- 紹興天明紙業股份有限公司 (中國)

- 日出報(印度)

- Rockdude Impex Pvt. Ltd.(印度)

- 卡夫互動(印度)

- 泰安百川紙業股份有限公司(中國)

- McNairn Packaging(加拿大)

- COREX集團(比利時)

- Scan Holdings(印度)

全球植物羊皮紙市場的最新發展

- 2023年5月,尼普羅集團(Nipro Corporation)的子公司尼普羅製藥包裝國際有限公司(Nipro PharmaPackaging International NV)收購了克羅埃西亞知名玻璃醫藥包裝生產商Piramida。此次收購是在Piramida被藍海資本收購後取得顯著增長之後進行的,彰顯了尼普羅致力於拓展其在歐洲及全球醫藥包裝市場的決心。

- 2022年9月,格雷斯海姆股份公司與斯蒂瓦那托集團有限公司合作開發了高端即用型 (RTU) 解決方案平台,初期專注於採用斯蒂瓦那托集團 EZ-fill 技術的小瓶。此次合作可望幫助客戶提高生產力、提高品質標準、加快產品上市速度、降低總擁有成本 (TCO) 並降低供應鏈風險。

- 2022年7月,Nipro Corporation Japan在克羅埃西亞投資1億克羅埃西亞庫納新建一座玻璃包裝廠。該工廠位於薩格勒布郊區塞斯韋特,專門生產用於藥品的玻璃安瓿瓶和小瓶,旨在滿足救命藥品的需求。

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。