Asia Pacific Cardiopulmonary Bypass Accessory Equipment Market

حجم السوق بالمليار دولار أمريكي

CAGR :

%

USD

2.94 Billion

USD

5.56 Billion

2025

2033

USD

2.94 Billion

USD

5.56 Billion

2025

2033

| 2026 –2033 | |

| USD 2.94 Billion | |

| USD 5.56 Billion | |

| % | |

|

تقسيم سوق معدات ملحقات جراحة القلب والرئة في منطقة آسيا والمحيط الهادئ، حسب المنتج (جهاز الأكسجة، جهاز الأكسجة الغشائية خارج الجسم، المضخات، القنية، أجهزة مراقبة درجة الحرارة، المبادل الحراري، المرشحات، مشابك الأنابيب، أجهزة تركيز الدم، لوحة النظام، أجهزة الاستشعار وملحقاتها، التحكم في توقف القلب، الخزان، كاشف الفقاعات، خلاط الغاز الإلكتروني، جهاز إغلاق الوريد الكهربائي، مشبك خط الوريد وملحقاته)، التشغيل (يدويًا، كهربائيًا، يعمل بالبطارية)، التطبيق (جراحة القلب، أجهزة أكسجة جراحة القلب، علاج الفشل التنفسي الحاد، سرطان الرئة، عمليات الزرع، وغيرها)، الفئة العمرية (البالغون، كبار السن، والأطفال)، المستخدم النهائي (المستشفيات، مراكز القلب، المؤسسات البحثية والأكاديمية، مراكز الجراحة الخارجية، وغيرها)، قناة التوزيع (المناقصات المباشرة، موزعو الطرف الثالث، ومبيعات التجزئة) - اتجاهات الصناعة وتوقعاتها حتى عام 2033

حجم سوق معدات ملحقات المجازة القلبية الرئوية في منطقة آسيا والمحيط الهادئ

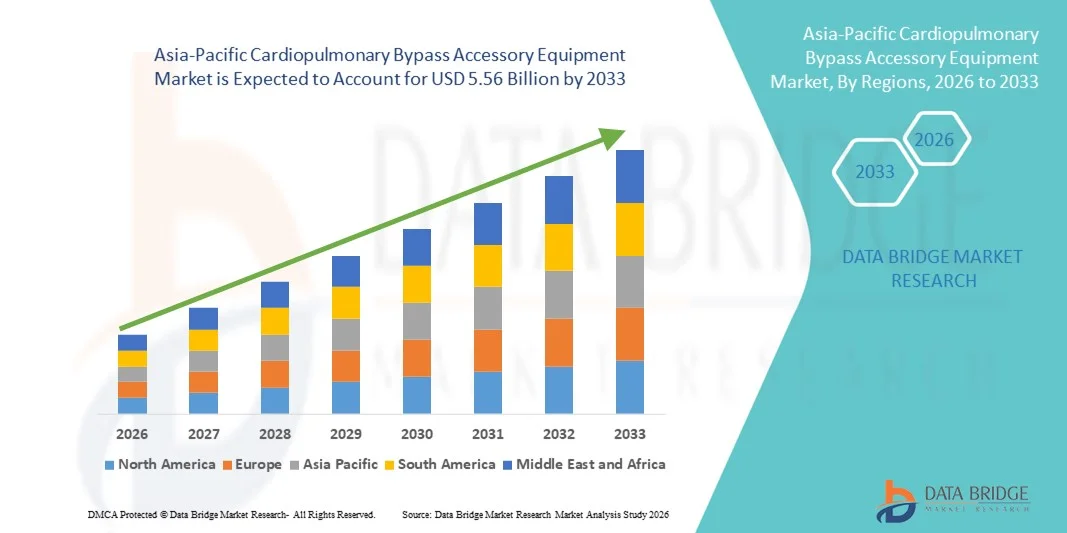

- بلغت قيمة سوق معدات ملحقات المجازة القلبية الرئوية في منطقة آسيا والمحيط الهادئ 2.94 مليار دولار أمريكي في عام 2025، ومن المتوقع أن تصل إلى 5.56 مليار دولار أمريكي بحلول عام 2033 ، بمعدل نمو سنوي مركب قدره 8.3% خلال فترة التوقعات.

- يعود نمو السوق إلى حد كبير إلى ارتفاع معدل انتشار أمراض القلب والأوعية الدموية، وزيادة الإنفاق على الرعاية الصحية، والتقدم التكنولوجي السريع في أنظمة الدورة الدموية خارج الجسم والمكونات الملحقة بها.

- علاوة على ذلك، فإن الطلب المتزايد على حلول أكثر أمانًا وكفاءة لجراحة القلب المفتوح، فضلًا عن تحسين إمكانية الوصول إلى خدمات رعاية القلب، يُرسّخ مكانة هذه الملحقات كعناصر أساسية في الممارسة الجراحية الحديثة. وتساهم عوامل متضافرة، مثل مبادرات الحكومات لتطوير مرافق الرعاية الصحية، وارتفاع وعي المرضى بالتدخلات القلبية المتقدمة، في تسريع اعتماد معدات جراحة القلب المفتوح في جميع أنحاء المنطقة، مما يعزز نمو هذا القطاع بشكل ملحوظ.

تحليل سوق معدات ملحقات المجازة القلبية الرئوية في منطقة آسيا والمحيط الهادئ

- تُعدّ معدات المجازة القلبية الرئوية، بما في ذلك أجهزة الأكسجة، والقنيات، ومجموعات الأنابيب، والمضخات، مكونات بالغة الأهمية في جراحة القلب الحديثة، إذ تُمكّن من توفير دعم آمن وفعال للقلب والرئتين أثناء العمليات الجراحية المعقدة في المستشفيات ومراكز القلب المتخصصة، وذلك بفضل دقتها وموثوقيتها وتوافقها مع الأنظمة الجراحية المتقدمة.

- يرجع الطلب المتزايد على هذه الملحقات في المقام الأول إلى ارتفاع معدل انتشار أمراض القلب والأوعية الدموية، وزيادة عدد جراحات القلب، والتركيز المتزايد على تحسين نتائج العمليات الجراحية من خلال تقنيات الدورة الدموية خارج الجسم المتقدمة.

- هيمنت الصين على سوق معدات جراحة القلب والرئة المساعدة في منطقة آسيا والمحيط الهادئ بحصة إيرادات بلغت 35.8% في عام 2025، مدفوعة بالتوسع السريع في البنية التحتية لرعاية القلب، ومبادرات الرعاية الصحية الحكومية، وزيادة اعتماد أنظمة المجازة المتقدمة في المستشفيات الرائدة، مع زيادة كبيرة في جراحات القلب في المناطق الحضرية الكبرى مما ساهم في نمو السوق

- من المتوقع أن تكون الهند أسرع الدول نموًا في السوق خلال فترة التوقعات، وذلك بسبب زيادة الاستثمارات في البنية التحتية للرعاية الصحية، وارتفاع مستوى وعي المرضى، وتوسع نطاق عمليات جراحة القلب في كل من المستشفيات العامة والخاصة.

- هيمنت أجهزة الأكسجة على سوق معدات ملحقات المجازة القلبية الرئوية في المنطقة بحصة بلغت 42.3% في عام 2025، مدفوعة بدورها الحاسم في تبادل الغازات أثناء عمليات المجازة وتوافقها مع مختلف التجهيزات الجراحية

نطاق التقرير وتجزئة سوق معدات ملحقات المجازة القلبية الرئوية في منطقة آسيا والمحيط الهادئ

|

صفات |

أهم المعلومات السوقية حول معدات ملحقات جهاز القلب والرئة الاصطناعي في منطقة آسيا والمحيط الهادئ |

|

القطاعات التي تم تغطيتها |

|

|

الدول المشمولة |

منطقة آسيا والمحيط الهادئ

|

|

اللاعبون الرئيسيون في السوق |

|

|

فرص السوق |

|

|

مجموعات بيانات القيمة المضافة |

بالإضافة إلى المعلومات المتعمقة حول سيناريوهات السوق مثل قيمة السوق ومعدل النمو والتجزئة والتغطية الجغرافية واللاعبين الرئيسيين، تتضمن تقارير السوق التي أعدتها شركة داتا بريدج لأبحاث السوق أيضًا تحليلاً معمقًا من قبل الخبراء، وبيانات وبائية للمرضى، وتحليلاً لخطوط الإنتاج، وتحليلاً للتسعير، والإطار التنظيمي. |

اتجاهات سوق معدات ملحقات المجازة القلبية الرئوية في منطقة آسيا والمحيط الهادئ

التطورات التكنولوجية وتكاملها مع الجراحة طفيفة التوغل

- يُعدّ دمج أجهزة الأكسجة المتقدمة ومجموعات الأنابيب والقنيات مع جراحات القلب طفيفة التوغل والجراحات القلبية بمساعدة الروبوت اتجاهًا هامًا ومتسارعًا في سوق معدات ملحقات المجازة القلبية الرئوية في منطقة آسيا والمحيط الهادئ، مما يُحسّن كفاءة الإجراءات وسلامتها ونتائج المرضى.

- فعلى سبيل المثال، تسمح أحدث أنظمة التحويل المعيارية بالتوافق السلس مع منصات الجراحة الروبوتية، مما يُمكّن الجراحين من إجراء عمليات معقدة بدقة محسّنة وتقليل أوقات العمليات الجراحية

- تُمكّن أجهزة الاستشعار والمراقبة المتطورة المُدمجة في معدات المجازة القلبية الرئوية من الكشف الفوري عن تدفق الدم وضغطه ومستوى الأكسجين فيه، مما يوفر تنبيهات أكثر دقة أثناء الجراحة. فعلى سبيل المثال، تتضمن بعض نماذج أجهزة الأكسجة مراقبة مدعومة بالذكاء الاصطناعي للتنبؤ باضطرابات التروية الدموية وتحسين سلامة المريض.

- يتيح دمج ملحقات المجازة القلبية الرئوية مع أنظمة إدارة سير العمل الجراحي مراقبة مركزية لمعايير متعددة، مما يضمن قدرة جميع أعضاء الفريق الجراحي على تتبع العلامات الحيوية للمريض وأداء الجهاز في وقت واحد.

- يُعيد هذا التوجه نحو حلول المجازة القلبية الأكثر ترابطًا وذكاءً والمخصصة لكل إجراء تشكيل التوقعات السريرية لجراحة القلب بشكل جذري. ونتيجة لذلك، تعمل شركات مثل ميدترونيك وتيرومو على تطوير معدات مجازة قلبية معيارية مزودة بأجهزة استشعار، ومتوافقة مع التدخلات القلبية طفيفة التوغل.

- يتزايد الطلب على ملحقات المجازة القلبية التي توفر تكاملاً سلساً مع التقنيات الجراحية المتقدمة بسرعة في المستشفيات العامة والخاصة على حد سواء، حيث يولي جراحو القلب أولوية متزايدة للكفاءة وسلامة المرضى ودقة النتائج.

- إن الاهتمام المتزايد بغرف العمليات الهجينة، التي تجمع بين أنظمة التصوير ومعدات المجازة القلبية الرئوية المتقدمة، يدفع الطلب بشكل أكبر على ملحقات المجازة القلبية الرئوية المتكاملة والمتعددة الاستخدامات.

ديناميكيات سوق معدات ملحقات المجازة القلبية الرئوية في منطقة آسيا والمحيط الهادئ

السائق

تزايد عبء أمراض القلب والأوعية الدموية وتوسع عمليات جراحة القلب

- يُعدّ تزايد انتشار أمراض القلب والأوعية الدموية في جميع أنحاء دول آسيا والمحيط الهادئ، إلى جانب تزايد أعداد جراحات القلب، عاملاً مهماً في زيادة الطلب على المعدات المساعدة لجراحة القلب والرئة.

- فعلى سبيل المثال، أعلنت شركة تيرومو في مارس 2025 عن إطلاق نظام أكسجة متطور لمراكز القلب ذات الحجم الكبير في الصين، بهدف تعزيز كفاءة وسلامة المجازة القلبية الرئوية أثناء العمليات الجراحية المعقدة.

- As hospitals expand cardiac care services and patient awareness rises, bypass accessories with enhanced monitoring, disposable tubing, and improved oxygenators offer a compelling upgrade over older surgical setups

- Furthermore, the growing number of cardiac centers and government initiatives to expand healthcare infrastructure are making advanced bypass equipment essential for modern cardiac surgery procedures

- Improved device ergonomics, ease of setup, and compatibility with multiple cardiac interventions are key factors propelling the adoption of bypass accessories in both public and private hospitals. The trend toward standardization of disposable components and modular setups further contributes to market growth

- For instance, India’s increasing cardiac surgery volume in tier-1 and tier-2 cities is driving hospitals to invest in high-performance bypass equipment for better patient outcomes

- Increasing collaborations between device manufacturers and hospital networks to provide training, service, and maintenance support is further accelerating adoption across Asia-Pacific healthcare facilities

Restraint/Challenge

High Costs and Regulatory Compliance Hurdles

- The high cost of advanced cardiopulmonary bypass accessories, coupled with stringent regulatory requirements across APAC countries, poses a significant challenge to wider market penetration

- For instance, new devices must comply with both national medical device regulations and international safety standards, which can delay product launches and adoption in smaller hospitals

- Addressing cost and regulatory hurdles through local manufacturing, bulk procurement, and adherence to regional certification protocols is crucial for building hospital trust. Companies such as Medtronic and Getinge emphasize compliance and quality certifications to reassure healthcare providers

- Furthermore, limited trained personnel to operate advanced bypass systems in some regions and the perceived complexity of modular setups can hinder adoption in smaller healthcare facilities

- Overcoming these challenges through government support programs, training initiatives, and cost optimization strategies will be vital for sustained growth in the APAC cardiopulmonary bypass accessory equipment market

- For instance, some hospitals in Southeast Asia delay adoption of advanced bypass equipment due to budget constraints and complex approval processes

- In addition, the need to maintain strict sterilization and single-use protocols for disposable bypass accessories increases operational costs, limiting adoption in smaller or resource-constrained hospitals

Asia-Pacific Cardiopulmonary Bypass Accessory Equipment Market Scope

The market is segmented on the basis of product, operation, application, age, end user, and distribution channel.

- By Product

On the basis of product, the market is segmented into oxygenator, ECMO machine, pumps, cannula, temperature monitors, heat exchanger, filters, tubing clamps, hemoconcentrators, system panel, sensor and accessories, cardioplegia control, reservoir, bubble detector, electronic gas blender, electrical venous occluder, venous line clamp and accessories. The oxygenator segment dominated the market with the largest revenue share of 42.3% in 2025, driven by its critical role in gas exchange during cardiopulmonary bypass procedures and its compatibility with a wide range of surgical setups. Hospitals prioritize oxygenators due to their reliability, ease of integration with various bypass systems, and improvements in membrane technology enhancing patient safety. High adoption in both adult and pediatric cardiac surgeries also strengthens the segment’s market position. Modular oxygenators that allow single-use disposables are increasingly preferred for infection control and operational efficiency. Advanced oxygenators with integrated sensors are enabling real-time monitoring during surgery, improving perfusion accuracy. Innovations in low-prime oxygenators for minimally invasive surgeries further expand adoption across tertiary care hospitals.

The pumps segment is anticipated to witness the fastest growth at a CAGR of 14.5% from 2026 to 2033, fueled by technological advances in electrically operated and AI-assisted perfusion pumps. These pumps provide precise blood flow control during surgery, reduce human error, and integrate with advanced monitoring systems. The growing demand for minimally invasive and hybrid cardiac procedures further contributes to pump adoption. Continuous innovation in compact, portable pump designs enhances usability across hospitals and cardiac centers. For instance, some hospitals in Japan and India are adopting automated pumps for high-volume surgeries to improve efficiency. Rising awareness of perfusionist workflow optimization and reduced intraoperative complications also drives adoption.

- By Operation

On the basis of operation, the market is segmented into manually operated, electrically operated, and battery-operated devices. The electrically operated segment dominated the market with a 51.2% share in 2025, driven by widespread hospital adoption of automated systems for precision and safety during complex cardiac surgeries. Electrically operated devices reduce perfusionist workload, allow integration with monitoring systems, and improve consistency in flow rates and oxygenation levels. Hospitals prefer these systems for large-scale cardiac procedures and high-volume surgical centers due to their reliability. They are particularly favored in adult and geriatric cardiac surgeries where precise control is essential. Advanced electrically operated pumps and monitors also enable real-time data logging for post-operative analysis. Continuous maintenance and calibration support provided by manufacturers reinforce hospital preference for electrically operated devices.

The battery-operated segment is expected to witness the fastest growth at a CAGR of 15.2% from 2026 to 2033, fueled by demand in ambulatory surgical centers, emergency cardiac care, and remote hospitals where electrical supply may be limited. Portable battery-operated pumps, oxygenators, and monitors provide flexibility and continuity of care. Improvements in battery efficiency and reliability allow their use in transport cases and smaller facilities. Hospitals with hybrid operating rooms and mobile cardiac units increasingly rely on battery-powered devices. Integration with compact monitoring systems also supports adoption in ICUs and pediatric cardiac care. Rising focus on uninterrupted patient care during power fluctuations further drives this segment.

- By Application

On the basis of application, the market is segmented into cardiac surgery, cardiac surgery oxygenators, acute respiratory failure treatment, lung cancer, transplant operation, and others. The cardiac surgery segment dominated the market with a revenue share of 47.5% in 2025, driven by the increasing number of cardiac procedures in APAC countries such as China, India, and Japan. Hospitals and cardiac centers prioritize high-quality bypass accessories for adult, pediatric, and geriatric surgeries. Rising cardiovascular disease prevalence and government initiatives to expand cardiac care infrastructure contribute to dominance. High adoption of oxygenators, pumps, and cannulas in major cardiac centers further strengthens market leadership. Hospitals benefit from modular bypass systems that improve surgical efficiency and reduce post-operative complications. The focus on reducing surgical risks and enhancing patient outcomes drives continued investment in this segment.

The acute respiratory failure treatment segment is expected to witness the fastest growth at a CAGR of 16.1% from 2026 to 2033, fueled by rising demand for ECMO machines and oxygenation devices in ICUs across APAC. Growing awareness of respiratory care and increasing lung disease prevalence drive adoption. Expansion of tertiary hospitals in urban and semi-urban regions further supports growth. ECMO integration with advanced monitoring devices enhances precision in patient management. Some hospitals are deploying portable ECMO systems for emergency respiratory care, boosting uptake. Rising government and private hospital investments in respiratory support technology also contribute to the rapid growth of this segment.

- By Age

On the basis of age, the market is segmented into adult, geriatric, and pediatric. The adult segment dominated the market with a revenue share of 54.7% in 2025, due to the higher incidence of cardiovascular diseases in adults and the large number of cardiac surgeries performed in hospitals across APAC. Hospitals invest in advanced bypass equipment to manage complex adult cardiac cases. Adult-specific oxygenators and pumps are preferred for flow capacity and compatibility with standard perfusion protocols. High adoption rates in metropolitan hospitals and private cardiac centers support dominance. Advanced monitoring accessories for adults further enhance perfusion safety. Integration of adult bypass equipment with hybrid operating rooms improves surgical efficiency and patient outcomes.

The pediatric segment is anticipated to witness the fastest growth at a CAGR of 15.8% from 2026 to 2033, driven by rising awareness of congenital heart disease management, increasing neonatal and pediatric cardiac surgeries, and miniaturized oxygenators, cannulas, and pumps. Specialized pediatric bypass systems reduce trauma and improve safety. Adoption is increasing in children’s hospitals and tertiary cardiac centers. Technological advances allow better perfusion control for smaller patients. Modular pediatric systems improve workflow for surgical teams. Training programs for pediatric perfusionists further support adoption across APAC.

- By End User

On the basis of end user, the market is segmented into hospitals, cardiac centers, research and academic institutions, ambulatory surgical centers, and others. The hospitals segment dominated the market with a revenue share of 59.4% in 2025, driven by large volumes of cardiac surgeries and well-equipped surgical infrastructure in tertiary hospitals. Hospitals invest in complete bypass setups, including oxygenators, pumps, monitors, and disposable accessories. High patient throughput and advanced surgical suites contribute to dominance. Hospitals benefit from direct manufacturer support for maintenance and training. The segment also sees strong adoption for adult, pediatric, and geriatric cardiac care. Established procurement processes and quality certifications reinforce hospital preference.

The cardiac centers segment is expected to witness the fastest growth at a CAGR of 16.3% from 2026 to 2033, fueled by specialized cardiac care centers in urban APAC regions. These centers increasingly adopt modular, sensor-enabled bypass equipment for precise cardiac surgeries. Expansion of private cardiac centers and collaborations with device manufacturers for training and service support drive adoption. Centers focus on patient outcome optimization and high-volume surgeries. Integration with minimally invasive and hybrid surgical systems further supports growth. Rising investments in private cardiac care infrastructure also boost market expansion.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, third-party distributor, and retail sales. The direct tender segment dominated the market with a revenue share of 63.2% in 2025, due to large hospitals and government institutions procuring equipment directly from manufacturers for quality, service support, and bulk discounts. Direct procurement ensures compliance with specifications and long-term service contracts. Hospitals handling high-volume surgeries prefer direct tender for reliability. Tertiary care centers adopt integrated bypass solutions through tenders. Established relationships with manufacturers facilitate training and maintenance support. Bulk orders reduce cost per unit and ensure timely delivery for critical surgeries.

The third-party distributor segment is expected to witness the fastest growth at a CAGR of 15.9% from 2026 to 2033, driven by increasing penetration in tier-2 and tier-3 cities, small-scale hospitals, and ambulatory surgical centers. Distributors provide faster delivery, flexible payment options, and multi-brand solutions. Smaller hospitals benefit from local service support and convenience. Adoption is rising in hospitals with limited procurement infrastructure. Distributors also offer bundled solutions including consumables and disposables. Growing network of distributors across APAC supports wider accessibility of advanced bypass technologies.

Asia-Pacific Cardiopulmonary Bypass Accessory Equipment Market Regional Analysis

- China dominated the Asia-Pacific cardiopulmonary bypass accessory equipment market with the largest revenue share of 35.8% in 2025, driven by rapid expansion of cardiac care infrastructure, government healthcare initiatives, and rising adoption of advanced bypass systems in top-tier hospitals, with a significant increase in cardiac surgeries in metropolitan areas fueling market growth

- Hospitals and cardiac centers in China highly prioritize patient safety, reliability, and integration of modular bypass accessories such as oxygenators, pumps, and cannulas, leading to strong demand for high-quality, sensor-enabled equipment

- This widespread adoption is further supported by government healthcare initiatives, growing patient awareness about cardiovascular diseases, and investments in modern surgical facilities, establishing cardiopulmonary bypass accessories as essential tools in both public and private hospitals

The China Cardiopulmonary Bypass Accessory Equipment Market Insight

The China cardiopulmonary bypass accessory equipment market captured the largest revenue share of 35.8% in 2025, fueled by rapid expansion of cardiac care infrastructure and increasing volumes of cardiac surgeries. Hospitals and cardiac centers are prioritizing advanced oxygenators, pumps, and cannulas to enhance patient safety and procedural efficiency. Growing awareness of cardiovascular diseases, coupled with government healthcare initiatives, is further driving adoption. Integration of modular and sensor-enabled bypass equipment into surgical workflows is becoming standard in top-tier hospitals. Moreover, rising investments in tertiary care facilities and high-volume cardiac centers are supporting sustained market growth across both adult and pediatric segments.

Japan Cardiopulmonary Bypass Accessory Equipment Market Insight

The Japan market is gaining momentum due to advanced cardiac care infrastructure, a strong base of experienced cardiac surgeons, and increasing demand for minimally invasive surgeries. Hospitals are adopting sensor-enabled oxygenators, automated pumps, and monitoring accessories to optimize perfusion and reduce surgical risks. Integration with hybrid operating rooms and advanced imaging systems is enhancing surgical precision. Japan’s high emphasis on patient safety and technological innovation is driving consistent adoption. In addition, the growing geriatric population is increasing demand for reliable bypass equipment for complex cardiac procedures. The country’s regulatory support and well-developed hospital network further strengthen market growth.

India Cardiopulmonary Bypass Accessory Equipment Market Insight

The India market accounted for the largest market revenue share in APAC after China in 2025, driven by rapid urbanization, expanding cardiac surgery volumes, and growing healthcare infrastructure. Hospitals and cardiac centers are increasingly adopting modular and portable bypass systems for adult, pediatric, and geriatric patients. Government initiatives for cardiac care, along with the rise of private cardiac centers, are accelerating adoption. Training programs for perfusionists and collaborations with device manufacturers support proper utilization of advanced bypass accessories. Rising awareness of congenital and acquired heart disease, coupled with affordable solutions from domestic manufacturers, is boosting the overall market penetration in India.

South Korea Cardiopulmonary Bypass Accessory Equipment Market Insight

يشهد سوق كوريا الجنوبية نموًا متزايدًا نتيجة ارتفاع معدلات جراحة القلب وزيادة الاستثمارات في البنية التحتية للمستشفيات لتوفير رعاية جراحية متقدمة. وتعتمد المستشفيات أجهزة الأكسجة والمضخات وأجهزة دعم الحياة خارج الجسم (ECMO) المعيارية لتحسين كفاءة العمليات الجراحية ونتائج المرضى. ويُعزى هذا النمو إلى التركيز على جودة رعاية المرضى، وتكامل أنظمة المراقبة، والطلب المتزايد على الإجراءات الجراحية طفيفة التوغل. كما تُسهم المبادرات الحكومية الداعمة للبنية التحتية لرعاية القلب في تعزيز هذا التوجه. إضافةً إلى ذلك، يُسهم تركيز كوريا الجنوبية على البحث والابتكار والتكنولوجيا الطبية المتقدمة في تسريع تبني أنظمة المجازة القلبية الآلية والمزودة بأجهزة استشعار.

حصة سوق معدات ملحقات المجازة القلبية الرئوية في منطقة آسيا والمحيط الهادئ

تتصدر شركات راسخة صناعة معدات المجازة القلبية الرئوية في منطقة آسيا والمحيط الهادئ، بما في ذلك:

- ميدترونيك (أيرلندا)

- شركة جيتينج إيه بي (السويد)

- شركة ليفانوفا بي إل سي (المملكة المتحدة)

- شركة تيرومو (اليابان)

- شركة إدواردز لايف ساينسز (الولايات المتحدة الأمريكية)

- يوروسيتس إس آر إل (إيطاليا)

- شركة بوسطن ساينتيفيك (الولايات المتحدة الأمريكية)

- أبوت (الولايات المتحدة)

- شركة شنيل الطبية (سويسرا)

- شركة نيبرو (اليابان)

- شركة زينوس المساهمة (ألمانيا)

- شركة تيليفليكس (الولايات المتحدة الأمريكية)

- شركة APC لأمراض القلب والأوعية الدموية المحدودة (المملكة المتحدة)

- برايل بيوميديكا المحدودة (البرازيل)

- شركة فريزينيوس ميديكال كير إيه جي وشركاه كي جي إيه إيه (ألمانيا)

- بي براون إس إي (ألمانيا)

- MC3 القلب والرئتين (الولايات المتحدة)

- شركة مايكروبورت العلمية (الصين)

- سيرج لأمراض القلب والأوعية الدموية (الولايات المتحدة)

- BD (الولايات المتحدة)

ما هي التطورات الأخيرة في سوق معدات ملحقات المجازة القلبية الرئوية في منطقة آسيا والمحيط الهادئ؟

- في يوليو 2025، حصل نظام VitalFlow ECMO من شركة Medtronic على علامة CE في أوروبا، مما يشير إلى اعتماد تنظيمي أوسع وتوافر عالمي مُحسّن لهذه التقنية؛ في حين أن الموافقة ليست خاصة بمنطقة آسيا والمحيط الهادئ، فإن علامة CE غالبًا ما تسبق وتدعم التوسع في اعتماد وتوزيع هذه التقنية في أسواق الرعاية الصحية في منطقة آسيا والمحيط الهادئ.

- في سبتمبر 2024، أطلقت شركة ميدترونيك نظام VitalFlow™، وهو نظام جديد للأكسجة الغشائية خارج الجسم (ECMO) مصمم لربط الرعاية السريرية والنقل داخل المستشفى، حيث يقدم حلاً مبسطًا وقابلاً للتكوين لنظام واحد للدعم القلبي الرئوي الحرج. يوسع هذا الإطلاق خيارات ECMO المتقدمة التي تعتبر أساسية لاستخدام ملحقات المجازة القلبية الرئوية والدعم القلبي الرئوي الطارئ.

- في أغسطس 2023، كشفت شركة LivaNova النقاب عن جهاز مراقبة الدم المدمج Essenz الحاصل على موافقة إدارة الغذاء والدواء الأمريكية (FDA 510(k)) وعلامة CE، مما يعزز قدرات المراقبة أثناء العمليات الجراحية التي تُعد ملحقات بالغة الأهمية أثناء جراحة القلب المفتوح والإجراءات ذات الصلة.

- في مارس 2023، حصلت شركة LivaNova PLC على موافقة إدارة الغذاء والدواء الأمريكية (FDA) بموجب البند 510(k) لجهاز Essenz Heart-Lung Machine، وهو نظام مجازة قلبية رئوية مصمم لتحسين كفاءة سير العمل ودعم التروية الفردية أثناء عمليات المجازة. وتؤثر موافقة إدارة الغذاء والدواء وخطط التوزيع العالمية على اعتماد الجهاز والثقة السريرية في مراكز جراحة القلب والصدر في منطقة آسيا والمحيط الهادئ.

- في مارس 2023، أفادت العديد من وسائل الإعلام المتخصصة في الصناعة بحصول شركة ليفانوفا على موافقة إدارة الغذاء والدواء الأمريكية لنظام إيسنز للتروية، وهو جهاز متكامل للقلب والرئة وشاشة عرض، مما يسلط الضوء على تأثيره المحتمل على رعاية التروية القائمة على البيانات أثناء عمليات المجازة القلبية الرئوية. ويؤكد هذا التطور التقدم السريري في تقنيات دعم المجازة القلبية الرئوية الأساسية ذات الصلة بالبرامج الجراحية في منطقة آسيا والمحيط الهادئ.

SKU-

احصل على إمكانية الوصول عبر الإنترنت إلى التقرير الخاص بأول سحابة استخبارات سوقية في العالم

- لوحة معلومات تحليل البيانات التفاعلية

- لوحة معلومات تحليل الشركة للفرص ذات إمكانات النمو العالية

- إمكانية وصول محلل الأبحاث للتخصيص والاستعلامات

- تحليل المنافسين باستخدام لوحة معلومات تفاعلية

- آخر الأخبار والتحديثات وتحليل الاتجاهات

- استغل قوة تحليل المعايير لتتبع المنافسين بشكل شامل

منهجية البحث

يتم جمع البيانات وتحليل سنة الأساس باستخدام وحدات جمع البيانات ذات أحجام العينات الكبيرة. تتضمن المرحلة الحصول على معلومات السوق أو البيانات ذات الصلة من خلال مصادر واستراتيجيات مختلفة. تتضمن فحص وتخطيط جميع البيانات المكتسبة من الماضي مسبقًا. كما تتضمن فحص التناقضات في المعلومات التي شوهدت عبر مصادر المعلومات المختلفة. يتم تحليل بيانات السوق وتقديرها باستخدام نماذج إحصائية ومتماسكة للسوق. كما أن تحليل حصة السوق وتحليل الاتجاهات الرئيسية هي عوامل النجاح الرئيسية في تقرير السوق. لمعرفة المزيد، يرجى طلب مكالمة محلل أو إرسال استفسارك.

منهجية البحث الرئيسية التي يستخدمها فريق بحث DBMR هي التثليث البيانات والتي تتضمن استخراج البيانات وتحليل تأثير متغيرات البيانات على السوق والتحقق الأولي (من قبل خبراء الصناعة). تتضمن نماذج البيانات شبكة تحديد موقف البائعين، وتحليل خط زمني للسوق، ونظرة عامة على السوق ودليل، وشبكة تحديد موقف الشركة، وتحليل براءات الاختراع، وتحليل التسعير، وتحليل حصة الشركة في السوق، ومعايير القياس، وتحليل حصة البائعين على المستوى العالمي مقابل الإقليمي. لمعرفة المزيد عن منهجية البحث، أرسل استفسارًا للتحدث إلى خبراء الصناعة لدينا.

التخصيص متاح

تعد Data Bridge Market Research رائدة في مجال البحوث التكوينية المتقدمة. ونحن نفخر بخدمة عملائنا الحاليين والجدد بالبيانات والتحليلات التي تتطابق مع هدفهم. ويمكن تخصيص التقرير ليشمل تحليل اتجاه الأسعار للعلامات التجارية المستهدفة وفهم السوق في بلدان إضافية (اطلب قائمة البلدان)، وبيانات نتائج التجارب السريرية، ومراجعة الأدبيات، وتحليل السوق المجدد وقاعدة المنتج. ويمكن تحليل تحليل السوق للمنافسين المستهدفين من التحليل القائم على التكنولوجيا إلى استراتيجيات محفظة السوق. ويمكننا إضافة عدد كبير من المنافسين الذين تحتاج إلى بيانات عنهم بالتنسيق وأسلوب البيانات الذي تبحث عنه. ويمكن لفريق المحللين لدينا أيضًا تزويدك بالبيانات في ملفات Excel الخام أو جداول البيانات المحورية (كتاب الحقائق) أو مساعدتك في إنشاء عروض تقديمية من مجموعات البيانات المتوفرة في التقرير.