Global Blood Collection Devices Market

حجم السوق بالمليار دولار أمريكي

CAGR :

%

USD

6.90 Billion

USD

11.13 Billion

2024

2032

USD

6.90 Billion

USD

11.13 Billion

2024

2032

| 2025 –2032 | |

| USD 6.90 Billion | |

| USD 11.13 Billion | |

| % | |

|

Global Blood Collection Devices Market Segmentation, By Product (Blood Collection Tubes, System Type, Needles and Syringes, Blood Bags, Blood Collection Systems/Monitors, and Lancets), Method (Manual Blood Collection, and Automated Blood Collection), Application (Diagnostics, and Therapeutic), End-User (Hospital, Blood Bank Centre, Academics, and Home Care) - Industry Trends and Forecast to 2032

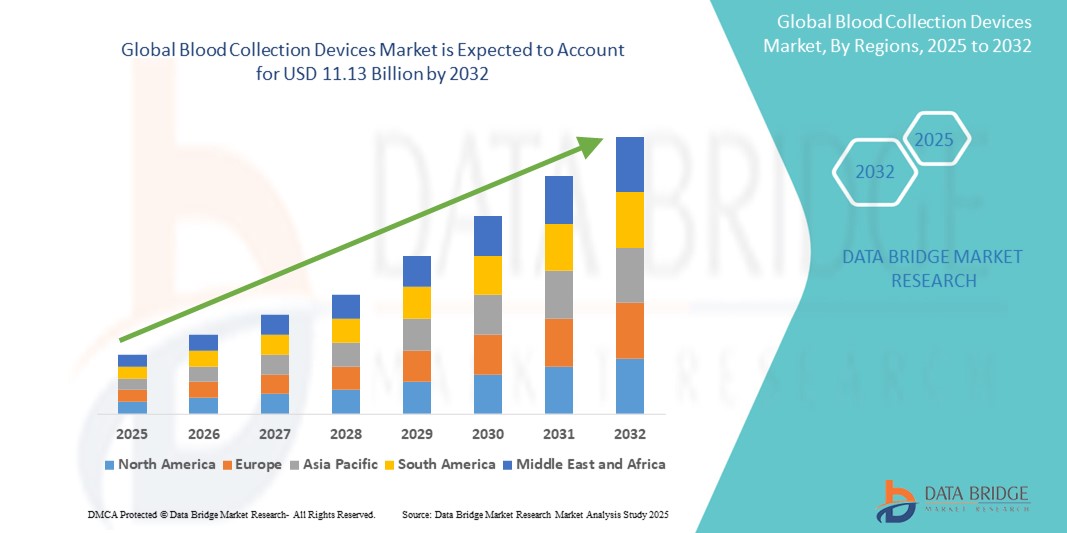

Blood Collection Devices Market Size

- The global blood collection devices market size was valued at USD 6.90 billion in 2024 and is expected to reach USD 11.13 billion by 2032, at a CAGR of 6.16% during the forecast period

- The Blood Collection Devices market growth is largely fueled by the increasing prevalence of chronic and infectious diseases, coupled with advancements in medical technology, leading to an increased demand for diagnostic testing and therapeutic procedures

- Furthermore, rising healthcare expenditure and growing awareness among consumers about the importance of early diagnosis and regular health monitoring are establishing blood collection devices as an essential component of modern healthcare systems. These converging factors are accelerating the uptake of blood collection devices solutions, thereby significantly boosting the industry's growth

Blood Collection Devices Market Analysis

- Blood collection devices, encompassing a range of instruments and consumables for drawing and processing blood samples, are increasingly vital components of modern healthcare systems in both diagnostic and therapeutic settings due to their enhanced safety features, efficiency, and critical role in disease management and patient care

- The escalating demand for blood collection devices is primarily fuelled by the rising global prevalence of chronic and infectious diseases, growing awareness about early disease detection, and continuous technological advancements leading to more efficient and patient-friendly collection methods

- North America dominates the blood collection devices market with the largest revenue share of 40.7% in 2024, characterized by advanced healthcare infrastructure, substantial R&D investments, and a strong presence of key industry players

- Asia-Pacific is expected to be the fastest growing region in the blood collection devices market during the forecast period, with a projected CAGR of 8.6% from 2025 to 2032, due to increasing urbanization, rising disposable incomes, a higher prevalence of infections, and growing demand for advanced blood collection technologies across countries such as China, India, and Japan

- The blood collection tubes segment dominates the blood collection devices market with an estimated share of 33.8% in 2024, driven by the increasing prevalence of chronic diseases and the need for routine diagnostics. Innovations in tube technology and adherence to regulatory guidelines also support its dominant position

Report Scope and Blood Collection Devices Market Segmentation

|

Attributes |

Blood Collection Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Blood Collection Devices Market Trends

“Deepening Integration with Advanced Automation Systems and Smart Data Analytics”

- A significant and accelerating trend in the global blood collection devices market is the deepening integration with advanced automation systems and smart data analytics. This fusion of technologies is significantly enhancing efficiency, precision, and patient experience during blood collection procedures

- على سبيل المثال، يجري تطوير أجهزة فصد دم آلية تستخدم تقنيات تصوير متطورة لتحديد مواقع بزل الوريد المثلى، مما يسمح بسحب دم أكثر دقة وتناسقًا. وبالمثل، تُدمج أنابيب سحب الدم الذكية ميزات تُمكّن من وضع العلامات والتتبع الآلي للعينات، مما يُبسط مرحلة ما قبل التحليل في الاختبارات المعملية.

- يُتيح دمج التحليلات المتقدمة في أجهزة سحب الدم ميزاتٍ مثل تعلم معايير بزل الوريد المثلى بناءً على الخصائص الديموغرافية للمريض وخصائص الوريد، والتنبؤ بالمضاعفات المحتملة، وتوفير تنبيهات ذكية للانحرافات في جودة العينة. على سبيل المثال، تستخدم بعض الأنظمة المتقدمة خوارزميات لتحسين دقة تصوير الوريد بمرور الوقت، ويمكنها إرسال تنبيهات ذكية في حال اكتشاف خطأ في سحب الدم. علاوةً على ذلك، تُتيح قدرات الأتمتة لمقدمي الرعاية الصحية سهولة التشغيل دون استخدام اليدين للمهام المتكررة، مما يُتيح لهم التركيز بشكل أكبر على تفاعل المريض واتخاذ القرارات الحاسمة.

- يُسهّل التكامل السلس لأجهزة سحب الدم مع أنظمة معلومات المختبرات (LIS) والسجلات الصحية الإلكترونية (EHR) التحكم المركزي في مختلف جوانب سير عمل التشخيص. من خلال واجهة واحدة، يُمكن للمستخدمين إدارة طلبات المرضى، وتتبع العينات، والوصول إلى النتائج، مما يُوفر تجربة تشخيصية موحدة وآلية.

- هذا التوجه نحو أنظمة سحب دم أكثر ذكاءً وسهولةً في الاستخدام وترابطًا يُحدث تغييرًا جذريًا في توقعات المستخدمين فيما يتعلق بالكفاءة وراحة المرضى في التشخيص. ونتيجةً لذلك، تُطوّر الشركات أجهزة سحب دم آلية مزودة بميزات مثل بزل الوريد الآلي لضمان تناسق عمليات السحب، ومعالجة العينات آليًا لتقليل التعامل اليدوي.

ديناميكيات سوق أجهزة سحب الدم

سائق

"الحاجة المتزايدة بسبب ارتفاع معدل انتشار الأمراض والطلب على التشخيص"

- إن الانتشار العالمي المتزايد لمختلف الأمراض المزمنة والمعدية، إلى جانب التركيز المتزايد على التشخيص المبكر والفحوصات الصحية الروتينية، يشكل محركًا مهمًا للطلب المتزايد على أجهزة جمع الدم.

- على سبيل المثال، يتطلب ارتفاع معدل الإصابة بمرض السكري وأمراض القلب والأوعية الدموية ومختلف الأمراض المُعدية (مثل الإنفلونزا، وكوفيد-19، وفيروس نقص المناعة البشرية/الإيدز) إجراء فحوصات دم دورية للتشخيص والمراقبة وإدارة العلاج. ومن المتوقع أن تُسهم هذه التحديات الصحية المستمرة في نمو صناعة أجهزة سحب الدم خلال الفترة المتوقعة.

- مع تزايد وعي مقدمي الرعاية الصحية بأهمية نتائج التشخيص الدقيقة وفي الوقت المناسب، والسعي إلى تعزيز سلامة المرضى أثناء الجمع، توفر أجهزة جمع الدم الحديثة ميزات متقدمة مثل الإبر المصممة للسلامة، والأنابيب ذات الباركود المسبق، وأنظمة الجمع المعقمة، مما يوفر ترقية مقنعة على الطرق التقليدية.

- علاوة على ذلك، فإن الشعبية المتزايدة لتشخيصات نقطة الرعاية (PoC) والرغبة في تبسيط سير العمل المختبري تجعل أجهزة جمع الدم المتقدمة جزءًا لا يتجزأ من هذه الأنظمة، مما يوفر تكاملاً سلسًا مع المحللين الآليين وأنظمة معلومات المختبر.

- تُعدّ سهولة استخدام طرق جمع الدم الأقل تدخلاً (مثل جمع الدم الشعري)، وانخفاض خطر إصابات وخز الإبر، والقدرة على ضمان سلامة العينة، عوامل رئيسية تدفع نحو اعتماد أجهزة جمع الدم في المستشفيات والعيادات، وحتى في مراكز الرعاية المنزلية. كما يُسهم التوجه نحو الاختبارات اللامركزية وتزايد توافر خيارات جمع الدم سهلة الاستخدام في نمو السوق.

ضبط النفس/التحدي

"مخاوف بشأن سلامة العينة والتكاليف الأولية المرتفعة"

- تُشكّل المخاوف المتعلقة باحتمالية حدوث مشاكل في سلامة العينات (مثل انحلال الدم، والتخثر، والتلوث) أثناء جمع الدم تحديًا كبيرًا أمام انتشار بعض الأجهزة المتطورة على نطاق أوسع في السوق. ونظرًا لاعتماد جمع الدم على تقنيات دقيقة وظروف معقمة، فإن سوء الجمع أو التعامل قد يؤدي إلى نتائج غير دقيقة للاختبارات، مما يثير قلق أخصائيي الرعاية الصحية بشأن موثوقية التشخيص.

- على سبيل المثال، يمكن أن تؤدي التقارير عن العينات التالفة بسبب الاستخدام غير الصحيح لأنبوب التجميع أو ظروف التخزين غير المناسبة إلى تردد بعض مرافق الرعاية الصحية في تبني منهجيات جمع الدم الجديدة أو الأكثر تعقيدًا دون تدريب مكثف.

- إن معالجة هذه المخاوف من خلال مراقبة جودة دقيقة، وبروتوكولات تدريب موحدة، وتعليمات واضحة للجهاز أمرٌ بالغ الأهمية لبناء ثقة المستخدم. غالبًا ما تُركز الشركات على تصميم أجهزتها لسهولة الاستخدام وميزات تقلل من تدهور العينات. إضافةً إلى ذلك، فإن التكلفة الأولية المرتفعة نسبيًا لبعض أنظمة جمع الدم الآلية المتقدمة والأجهزة المتخصصة، مقارنةً بالطرق اليدوية التقليدية، قد تُشكل عائقًا أمام تبنيها في مرافق الرعاية الصحية ذات الميزانية المحدودة، وخاصةً في المناطق النامية أو العيادات الصغيرة. في حين أن لوازم جمع الدم الأساسية لا تزال في متناول اليد، إلا أن الميزات المتميزة، مثل تصوير الأوردة المتكامل، والأنظمة الروبوتية، وآليات السلامة المتقدمة، غالبًا ما تكون أعلى سعرًا.

- في حين أن أسعار بعض المكونات تتناقص تدريجيًا، فإن التكلفة العالية المتوقعة لتكنولوجيا الأتمتة والسلامة المتطورة لا تزال قادرة على إعاقة التبني على نطاق واسع، وخاصة بالنسبة لأولئك الذين لا يرون عائدًا فوريًا على الاستثمار للميزات المتقدمة المقدمة.

- إن التغلب على هذه التحديات من خلال برامج تدريبية محسنة، وإظهار واضح للفعالية من حيث التكلفة وفوائد سلامة المرضى، وتطوير خيارات جمع الدم عالية الجودة وبأسعار معقولة سيكون أمرًا حيويًا للنمو المستدام للسوق.

نطاق سوق أجهزة سحب الدم

يتم تقسيم سوق أجهزة جمع الدم إلى أربعة قطاعات بارزة بناءً على المنتج والطريقة والتطبيق والمستخدم النهائي.

- حسب المنتج

بناءً على المنتج، يُقسّم سوق أجهزة سحب الدم العالمية إلى أنابيب سحب الدم، والإبر والمحاقن، وأكياس الدم، وأنظمة/أجهزة مراقبة سحب الدم، والمشارط. يُهيمن قطاع أنابيب سحب الدم على أكبر حصة من إيرادات السوق بنسبة 33.8% في عام 2024، مدفوعًا بتزايد انتشار الأمراض المزمنة التي تتطلب تشخيصًا روتينيًا والتطورات المستمرة في تكنولوجيا الأنابيب. تُعدّ هذه الأنابيب أساسية لمختلف الاختبارات، وتُعزز الابتكارات في الإضافات والتصميمات استقرار العينات وكفاءة المختبرات.

من المتوقع أن يشهد قطاع الوخز بالإبر أسرع معدل نمو بنسبة 7.9% بين عامي 2025 و2032، مدفوعًا بارتفاع معدلات الإصابة بالأمراض المزمنة مثل داء السكري، مما يزيد الطلب على أخذ عينات دم شعرية بشكل متكرر لأغراض المراقبة. ويدعم هذا النمو أيضًا تزايد شعبية الاختبارات المنزلية وطرق جمع العينات الأقل تدخلاً.

- حسب الطريقة

بناءً على المنهجية المتبعة، يُقسّم سوق أجهزة سحب الدم العالمي إلى جمع الدم يدويًا وجمع الدم آليًا. وقد استحوذ قطاع جمع الدم اليدوي على أكبر حصة من إيرادات السوق، بنسبة 67.1% في عام 2024، بفضل فعاليته من حيث التكلفة، وإمكانية تطبيقه على نطاق واسع في مختلف مرافق الرعاية الصحية، وراحة المرضى. ولا تزال هذه الطريقة مستخدمة على نطاق واسع في المستشفيات والعيادات ومختبرات التشخيص، مدعومةً بالتطورات المستمرة في تكنولوجيا الإبر وإجراءات جمع الدم المبسطة.

من المتوقع أن يشهد قطاع جمع الدم الآلي أسرع معدل نمو سنوي مركب بنسبة 7.7% بين عامي 2025 و2032، مدفوعًا بالطلب المتزايد على إجراءات جمع أكثر أمانًا وكفاءةً وتوحيدًا. تُقلل الأتمتة من الأخطاء البشرية، وتُحسّن جودة العينات، وتُحسّن كفاءة سير العمل، مما يجعلها أكثر جاذبيةً للبيئات ذات الكميات الكبيرة.

- حسب الطلب

بناءً على التطبيق، يُقسّم سوق أجهزة سحب الدم العالمية إلى قسمين: التشخيص والعلاج. ويتصدر قطاع التشخيص السوق بحصة سوقية تبلغ 65.6% في عام 2024، مدفوعًا بالطلب المتزايد باستمرار على فحوصات الدم لتشخيص مجموعة واسعة من الأمراض المزمنة، مثل السرطان والسكري وأمراض القلب والأوعية الدموية. وتُعدّ عينات الدم أساسية لتأكيد التشخيص، ومراقبة تطور المرض، وتوجيه قرارات العلاج في مختلف التخصصات الطبية.

من المتوقع أن يسجل قطاع العلاج أسرع معدل نمو سنوي مركب بنحو 7.2% من عام 2025 إلى عام 2032، مدفوعًا بالطلب المتزايد على مراقبة الدم في الإجراءات العلاجية، مثل عمليات نقل الدم، وفصل مكونات الدم، والابتكارات في الطب الشخصي التي تتطلب جمع مكونات دم محددة.

- حسب المستخدم النهائي

On the basis of end-user, the global blood collection devices market is segmented into hospitals, blood bank centers, academics, and home care. The hospital segment accounted for the largest market revenue share of 34.2% in 2024, driven by the high volume of diagnostic tests performed daily, increased blood transfusion needs related to surgeries and chronic conditions, and the comprehensive range of medical services offered. Hospitals serve as primary points of care for a large patient influx requiring blood collection.

The blood bank center segment is expected to register the fastest CAGR of 7.5% during the forecast period, fueled by advancements in blood sampling technologies and the rising number of specialized diagnostic tests conducted in these dedicated facilities.

Blood Collection Devices Market Regional Analysis

- North America dominates the blood collection devices market with the largest revenue share of 40.7% in 2024, driven by its highly advanced healthcare infrastructure and significant investments in research and development

- Healthcare providers in the region highly value the enhanced patient safety features, improved accuracy, and streamlined workflows offered by modern blood collection devices, which seamlessly integrate with electronic health records and laboratory information systems

- This widespread adoption is further supported by high healthcare expenditure, a strong focus on preventive diagnostics and early disease detection, and the prominent presence of key industry players actively engaged in developing innovative blood collection technologies. This positions blood collection devices as an essential component for efficient and safe patient care across North America

U.S. Blood Collection Devices Market Insight

The U.S. blood collection devices market captured the largest revenue share of 72.6% in 2024 within North America, fueled by the swift adoption of advanced diagnostic technologies and the expanding healthcare infrastructure. Healthcare providers are increasingly prioritizing patient safety and efficiency through integrated, high-quality blood collection systems. The growing preference for advanced pre-analytical solutions, combined with robust demand for automated systems and integrated data management, further propels the blood collection devices industry. Moreover, the increasing integration of healthcare IT systems and a strong focus on clinical outcomes are significantly contributing to the market's expansion.

Europe Blood Collection Devices Market Insight

The Europe blood collection devices market is projected to expand at a substantial CAGR from 2025 to 2032, primarily driven by the rising prevalence of chronic and infectious diseases and the escalating need for enhanced diagnostic capabilities in hospitals and laboratories. The increase in aging populations, coupled with the demand for safer and more efficient blood collection methods, is fostering the adoption of advanced devices. European healthcare systems are also drawn to the precision and reliability these devices offer. The region is experiencing significant growth across hospital, diagnostic center, and blood bank applications, with advanced blood collection devices being incorporated into both new facility designs and existing laboratory upgrades.

U.K. Blood Collection Devices Market Insight

The U.K. blood collection devices market is anticipated to grow at a noteworthy CAGR from 2025 to 2032, driven by the escalating demand for advanced diagnostics and a desire for heightened patient comfort and safety during blood draws. In addition, concerns regarding healthcare efficiency and reduced risk of needlestick injuries are encouraging both healthcare providers and patients to choose modern blood collection solutions. The U.K.'s embrace of advanced medical technologies, alongside its robust healthcare infrastructure, is expected to continue to stimulate market growth.

Germany Blood Collection Devices Market Insight

The Germany blood collection devices market is expected to expand at a considerable CAGR from 2025 to 2032, fueled by increasing awareness of diagnostic accuracy and the demand for technologically advanced, high-quality solutions. Germany’s well-developed healthcare infrastructure, combined with its emphasis on innovation and stringent quality standards, promotes the adoption of advanced blood collection devices, particularly in hospitals and clinical laboratories. The integration of blood collection solutions with laboratory automation systems is also becoming increasingly prevalent, with a strong preference for secure, patient-focused solutions aligning with local healthcare expectations.

Asia-Pacific Blood Collection Devices Market Insight

The Asia-Pacific blood collection devices market is poised to grow at the fastest CAGR of 8.6% during the forecast period of 2025 to 2032, driven by increasing urbanization, rising disposable incomes, and significant technological advancements in countries such as China, Japan, and India. The region's growing healthcare expenditure, supported by government initiatives promoting access to diagnostics, is driving the adoption of advanced blood collection devices. Furthermore, as APAC emerges as a manufacturing hub for medical components and systems, the affordability and accessibility of blood collection devices are expanding to a wider healthcare consumer base.

China Blood Collection Devices Market Insight

The China blood collection devices market accounted for a significant revenue share in Asia Pacific in 2024, attributed to the country's expanding middle class, rapid urbanization, and high rates of healthcare technological adoption. China stands as one of the largest markets for medical devices, and blood collection devices are becoming increasingly essential in hospitals, diagnostic centers, and blood banks. The push towards modernizing healthcare infrastructure and the availability of increasingly sophisticated blood collection options, alongside strong domestic manufacturers, are key factors propelling the market in China.

India Blood Collection Devices Market Insight

The India blood collection devices market is expected to witness the highest CAGR of 8.15% from 2025 to 2032, fueled by the rapidly improving healthcare infrastructure, rising awareness about early disease diagnosis, and a large patient pool. The increasing prevalence of infectious and chronic diseases necessitates a growing volume of blood tests. Government initiatives aimed at improving healthcare accessibility and affordability, coupled with increasing private investments in diagnostic laboratories and hospitals, are significant drivers for the adoption of blood collection devices across the country.

Blood Collection Devices Market Share

The blood collection devices industry is primarily led by well-established companies, including:

- Abbott (U.S.)

- Medtronic (Ireland)

- BD (U.S.)

- Terumo Corporation (Japan)

- NIPRO (Japan)

- QIAGEN (Germany)

- MEDICAL S.r.l. (Italy)

- TERUMO BCT, Inc. (U.S.)

- Fresenius Kabi AG (Germany)

- Grifols, S.A. (Spain)

- Jiangsu Micsafe Medical Technology Co., Ltd. (China)

- SARSTEDT AG & Co. KG (Germany)

- Retractable Technologies, Inc. (U.S.)

- FL MEDICAL s.r.l. Unipersonale (Italy)

- AB Medical Academy (Netherlands)

Latest Developments in Global Blood Collection Devices Market

- In April 2024, Streck introduced Protein Plus BCT, a new direct draw whole blood collection tube designed to stabilize plasma protein concentrations during storage at room temperature. This launch expands the company's product portfolio and strengthens its competitive position in the market

- In April 2024, Becton, Dickinson and Company (BD) introduced the BD Vacutainer UltraTouch Push Button Blood Collection Set in India. This innovative product features BD RightGauge technology, allowing the use of a thinner needle for blood collection, and BD PentaPoint technology to significantly reduce insertion pain for patients

- In January 2025, Fresenius Kabi announced that the FDA granted 510(k) clearance for its Adaptive Nomogram, an alternative algorithm for the Aurora Xi Plasmapheresis System, aimed at optimizing plasma collection efficiency

- In March 2025, BD (Becton, Dickinson and Company) and Babson Diagnostics announced results of new studies demonstrating that common blood tests using several drops of blood collected via the BD MiniDraw Capillary Blood Collection System are as accurate as higher-volume draws from veins, potentially improving patient access to testing

- In October 2024, Terumo Blood and Cell Technologies kicked off the U.S. launch of the Reveos Automated Blood Processing System with Blood Centers of America. Used globally for over a decade, Reveos targets efficiency and bolstering the platelet supply

- In November 2023, BD introduced the PIVO Pro Needle-free Blood Collection Device, which allows blood samples to be drawn directly from a patient's peripheral IV line without using a traditional needle. This device builds upon BD's existing PIVO technology

- In January 2023, Capitainer collaborated with AstraZeneca to use a novel device from Capitainer to develop protocols for biomarkers relevant to AstraZeneca's clinical drug programs

SKU-

احصل على إمكانية الوصول عبر الإنترنت إلى التقرير الخاص بأول سحابة استخبارات سوقية في العالم

- لوحة معلومات تحليل البيانات التفاعلية

- لوحة معلومات تحليل الشركة للفرص ذات إمكانات النمو العالية

- إمكانية وصول محلل الأبحاث للتخصيص والاستعلامات

- تحليل المنافسين باستخدام لوحة معلومات تفاعلية

- آخر الأخبار والتحديثات وتحليل الاتجاهات

- استغل قوة تحليل المعايير لتتبع المنافسين بشكل شامل

منهجية البحث

يتم جمع البيانات وتحليل سنة الأساس باستخدام وحدات جمع البيانات ذات أحجام العينات الكبيرة. تتضمن المرحلة الحصول على معلومات السوق أو البيانات ذات الصلة من خلال مصادر واستراتيجيات مختلفة. تتضمن فحص وتخطيط جميع البيانات المكتسبة من الماضي مسبقًا. كما تتضمن فحص التناقضات في المعلومات التي شوهدت عبر مصادر المعلومات المختلفة. يتم تحليل بيانات السوق وتقديرها باستخدام نماذج إحصائية ومتماسكة للسوق. كما أن تحليل حصة السوق وتحليل الاتجاهات الرئيسية هي عوامل النجاح الرئيسية في تقرير السوق. لمعرفة المزيد، يرجى طلب مكالمة محلل أو إرسال استفسارك.

منهجية البحث الرئيسية التي يستخدمها فريق بحث DBMR هي التثليث البيانات والتي تتضمن استخراج البيانات وتحليل تأثير متغيرات البيانات على السوق والتحقق الأولي (من قبل خبراء الصناعة). تتضمن نماذج البيانات شبكة تحديد موقف البائعين، وتحليل خط زمني للسوق، ونظرة عامة على السوق ودليل، وشبكة تحديد موقف الشركة، وتحليل براءات الاختراع، وتحليل التسعير، وتحليل حصة الشركة في السوق، ومعايير القياس، وتحليل حصة البائعين على المستوى العالمي مقابل الإقليمي. لمعرفة المزيد عن منهجية البحث، أرسل استفسارًا للتحدث إلى خبراء الصناعة لدينا.

التخصيص متاح

تعد Data Bridge Market Research رائدة في مجال البحوث التكوينية المتقدمة. ونحن نفخر بخدمة عملائنا الحاليين والجدد بالبيانات والتحليلات التي تتطابق مع هدفهم. ويمكن تخصيص التقرير ليشمل تحليل اتجاه الأسعار للعلامات التجارية المستهدفة وفهم السوق في بلدان إضافية (اطلب قائمة البلدان)، وبيانات نتائج التجارب السريرية، ومراجعة الأدبيات، وتحليل السوق المجدد وقاعدة المنتج. ويمكن تحليل تحليل السوق للمنافسين المستهدفين من التحليل القائم على التكنولوجيا إلى استراتيجيات محفظة السوق. ويمكننا إضافة عدد كبير من المنافسين الذين تحتاج إلى بيانات عنهم بالتنسيق وأسلوب البيانات الذي تبحث عنه. ويمكن لفريق المحللين لدينا أيضًا تزويدك بالبيانات في ملفات Excel الخام أو جداول البيانات المحورية (كتاب الحقائق) أو مساعدتك في إنشاء عروض تقديمية من مجموعات البيانات المتوفرة في التقرير.