Global Electrostatic Precipitator Market

حجم السوق بالمليار دولار أمريكي

CAGR :

%

USD

7.65 Billion

USD

12.40 Billion

2024

2032

USD

7.65 Billion

USD

12.40 Billion

2024

2032

| 2025 –2032 | |

| USD 7.65 Billion | |

| USD 12.40 Billion | |

| % | |

|

Global Electrostatic Precipitator Market, By Design (Plate and Tubular), Type (Dry ESP, Wet ESP, Plate Wire, Flat Plate, Tubular, and Two-stage), Offering (Hardware and Software and Services), End User (Power Generation, Chemicals and Petrochemicals, Cement, Metal Processing and Mining, Manufacturing, Marine, and Others) – Industry Trends and Forecast to 2032.

Electrostatic Precipitator Market Size

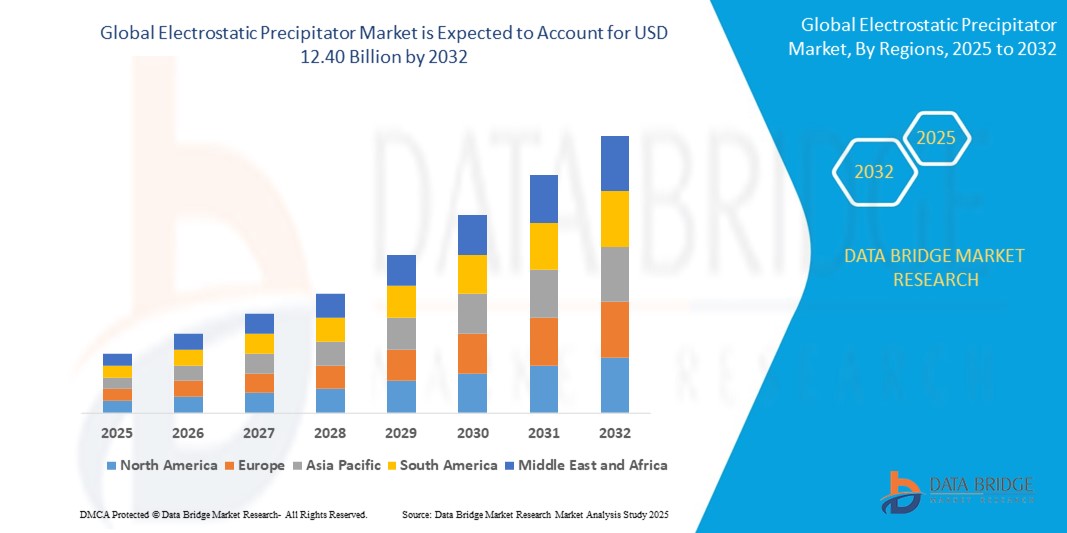

- The global electrostatic precipitator market size was valued at USD 7.65 billion in 2024 and is expected to reach USD 12.40 billion by 2032, at a CAGR of 6.22% during the forecast period

- The market growth is largely fueled by the increasing stringency of air pollution control regulations worldwide and the growing industrialization in emerging economies, leading to a higher demand for efficient particulate matter emission reduction solutions

- Furthermore, rising awareness about environmental protection and the need for sustainable industrial operations are establishing electrostatic precipitators as a preferred technology for air quality management

Electrostatic Precipitator Market Analysis

- Electrostatic precipitators (ESPs), offering highly efficient removal of particulate matter from industrial gas streams, are increasingly vital components of modern air pollution control systems across various industries due to their ability to handle large gas volumes, high temperatures, and diverse particulate characteristics

- The escalating demand for ESPs is primarily fueled by the global push for cleaner air, increasing industrial emissions, and a rising preference for cost-effective and reliable long-term particulate control technologies

- Asia-Pacific dominates the electrostatic precipitator market with the largest revenue share of 45.60% in 2025, driven by rapid industrialization, especially in emerging economies such as China and India, and a growing demand for energy coupled with increasing governmental focus on mitigating industrial air pollution

- Europe is expected to be the fastest-growing region in the electrostatic precipitator market during the forecast period, due to stringent emission standards and a strong emphasis on upgrading existing industrial facilities with advanced pollution control technologies

- The dry ESP segment is expected to dominate the electrostatic precipitator market with a market share of 61% in 2025, driven by its widespread application in power generation and cement industries, its effectiveness in capturing dry particulate matter, and lower operational complexities compared to wet ESPs

Report Scope and Electrostatic Precipitator Market Segmentation

|

Attributes |

رؤى رئيسية حول سوق المرسبات الكهروستاتيكية |

|

القطاعات المغطاة |

|

|

الدول المغطاة |

أمريكا الشمالية

أوروبا

آسيا والمحيط الهادئ

الشرق الأوسط وأفريقيا

أمريكا الجنوبية

|

|

اللاعبون الرئيسيون في السوق |

|

|

فرص السوق |

|

|

مجموعات معلومات البيانات ذات القيمة المضافة |

بالإضافة إلى الرؤى حول سيناريوهات السوق مثل القيمة السوقية ومعدل النمو والتجزئة والتغطية الجغرافية واللاعبين الرئيسيين، فإن تقارير السوق التي تم إعدادها بواسطة Data Bridge Market Research تتضمن أيضًا تحليلًا متعمقًا من الخبراء والإنتاج والقدرة التمثيلية الجغرافية للشركة وتخطيطات الشبكة للموزعين والشركاء وتحليل اتجاهات الأسعار التفصيلية والمحدثة وتحليل العجز في سلسلة التوريد والطلب. |

اتجاهات سوق المرسبات الكهروستاتيكية

" التطورات من خلال إنترنت الأشياء والذكاء الاصطناعي والصيانة التنبؤية "

- إن الاتجاه المهم والمتسارع في سوق المترسب الكهروستاتيكي العالمي (ESP) هو التكامل المتزايد مع تقنيات إنترنت الأشياء (IoT) والذكاء الاصطناعي (AI) والتحليلات المتقدمة للصيانة التنبؤية

- على سبيل المثال، تُقدّم الشركات بشكل متزايد أجهزة ESP مُدمجة بأجهزة استشعار ومنصات تحليل بيانات، مما يُتيح للمُشغّلين مُراقبة المُعاملات الرئيسية آنيًا، مثل تركيز الجسيمات ودرجة الحرارة والأداء الكهربائي. يُتيح هذا إجراء تعديلات استباقية وتحسين كفاءة جمع أجهزة ESP.

- يتيح تكامل الذكاء الاصطناعي في أنظمة ESP ميزات مثل تعلم خصائص غازات المداخن لاقتراح تحسينات تشغيلية محتملة وتوفير تنبيهات أكثر ذكاءً بناءً على انحرافات الأداء

- يُسهّل التكامل السلس لأنظمة ESP مع أنظمة الأتمتة الصناعية الأوسع والتوائم الرقمية التحكم المركزي في جوانب مختلفة من عمليات المصنع

- إن هذا الاتجاه نحو أنظمة التحكم في تلوث الهواء الأكثر ذكاءً وبديهية وترابطًا يعيد تشكيل توقعات الصناعة بشكل أساسي فيما يتعلق بالامتثال البيئي والكفاءة التشغيلية

- يتزايد الطلب على مزودي خدمات الطاقة الذين يقدمون تكاملاً سلسًا بين إنترنت الأشياء والذكاء الاصطناعي والصيانة التنبؤية بسرعة في مختلف القطاعات الصناعية، حيث تعطي الشركات الأولوية بشكل متزايد للكفاءة التشغيلية وتقليل وقت التوقف والامتثال القوي للوائح البيئية الأكثر صرامة.

ديناميكيات سوق المرسبات الكهروستاتيكية

سائق

"الحاجة المتزايدة بسبب تزايد صرامة لوائح مكافحة تلوث الهواء"

- إن الصرامة المتزايدة في لوائح مكافحة تلوث الهواء على مستوى العالم، إلى جانب تسارع وتيرة التصنيع، وخاصة في الاقتصادات الناشئة، تشكل محركًا مهمًا للطلب المتزايد على المرسبات الكهروستاتيكية

- مع فرض الحكومات في جميع أنحاء العالم حدودًا أكثر صرامة على انبعاثات الجسيمات من المصادر الصناعية، تضطر الشركات إلى الاستثمار في تقنيات مكافحة التلوث عالية الكفاءة مثل ESPs لضمان الامتثال

- على سبيل المثال، تُطبّق الهيئات التنظيمية في مناطق مختلفة، مثل وكالة حماية البيئة الأمريكية، والاتحاد الأوروبي، والهيئات البيئية الوطنية في الصين والهند، معايير انبعاثات أكثر صرامةً لصناعات مثل توليد الطاقة، والإسمنت، ومعالجة المعادن. وهذا يدفع الصناعات إلى اعتماد أو تحديث أنظمة المرسبات الكهروستاتيكية لتحقيق مستويات الانبعاثات المطلوبة.

- علاوة على ذلك، يؤدي النمو المستمر في الناتج الصناعي عبر القطاعات مثل المواد الكيميائية والتصنيع وحرق النفايات إلى زيادة أحجام غازات العادم التي تتطلب إزالة الجسيمات بشكل فعال

- إن الحاجة إلى حلول طويلة الأمد وموثوقة وعالية الكفاءة لإدارة هذه الانبعاثات تجعل من المرسبات الكهروستاتيكية خيارًا لا غنى عنه. كما أن التركيز المتزايد على الممارسات الصناعية المستدامة والمسؤولية الاجتماعية للشركات يشجع الشركات على تبني أنظمة متطورة لمكافحة التلوث.

ضبط النفس/التحدي

" استثمار رأس المال الأولي المرتفع والتعقيد التشغيلي "

- تشكل المخاوف المحيطة بالاستثمار الرأسمالي الأولي المرتفع المطلوب لتركيب المرسبات الكهروستاتيكية، إلى جانب تعقيدها التشغيلي المتأصل ومتطلبات الصيانة المحددة، تحديات كبيرة أمام اختراق السوق على نطاق أوسع.

- على سبيل المثال، غالبًا ما يتطلب تركيب نظام ESP هندسةً كبيرةً ومعداتٍ متخصصةً ودمجًا في البنية التحتية الحالية للمصنع، مما يؤدي إلى نفقات رأسمالية كبيرة. قد يُشكل هذا عائقًا للشركات الصغيرة والمتوسطة أو الصناعات ذات الميزانيات الرأسمالية المحدودة.

- إن معالجة هذه المخاوف المتعلقة بالتكلفة من خلال التصاميم المعيارية وخيارات التمويل وإثبات عائد الاستثمار طويل الأجل أمرٌ بالغ الأهمية لاعتمادها على نطاق أوسع. إضافةً إلى ذلك، تتطلب أنظمة المضخات الكهروستاتيكية (ESP) مهاراتٍ ومعرفةً متخصصةً لضمان التشغيل والصيانة الأمثل.

- يمكن أن تؤثر عوامل مثل تقلبات مقاومة الغبار، واختلافات درجات الحرارة، ووجود جسيمات لزجة أو تآكلية على أداء ESP وتتطلب مراقبة وتعديلًا دقيقين

- إن التغلب على هذه التحديات من خلال التقدم التكنولوجي الذي يقلل من تعقيد التثبيت، ويعزز الأتمتة، ويقدم حلول الصيانة التنبؤية، ويوفر برامج تدريبية شاملة سيكون أمرًا حيويًا لتحقيق نمو مستدام للسوق.

نطاق سوق المرسبات الكهروستاتيكية

يتم تقسيم السوق على أساس التصميم والنوع والعرض والمستخدم النهائي.

- حسب التصميم

بناءً على التصميم، يُقسّم سوق المرسبات الكهروستاتيكية إلى صفائح وأنبوبية. يُهيمن قطاع الصفائح على أكبر حصة من إيرادات السوق بحلول عام 2025، بفضل استخدامه الواسع في التطبيقات الصناعية واسعة النطاق، وكفاءته العالية في جمع الجسيمات بأحجام متنوعة، وقدرته على التكيف مع مختلف العمليات الصناعية. وتُفضّل تصاميم الصفائح لمتانتها وقدرتها على التعامل مع كميات كبيرة من الغاز.

من المتوقع أن يشهد قطاع الأنابيب أسرع معدل نمو بين عامي 2025 و2032، مدفوعًا بزيادة الاعتماد عليه في التطبيقات المتخصصة التي تشمل جمع النفايات السائلة، وإزالة الجسيمات الدقيقة، وحرق النفايات الخطرة. توفر أجهزة الطرد المركزي الأنبوبية مزايا في ظروف غازية محددة، وغالبًا ما توفر تصاميم أكثر إحكامًا لبعض المنشآت الصناعية.

- حسب النوع

يُقسّم سوق أجهزة الترسيب الكهروستاتيكي، حسب نوعها، إلى أجهزة ترسيب كهروستاتيكي جاف، وأجهزة ترسيب كهروستاتيكي رطب، وأجهزة سلكية، وأجهزة مسطحة، وأجهزة أنبوبية، وأجهزة ثنائية المرحلة. وقد استحوذ قطاع أجهزة الترسيب الكهروستاتيكي الجاف على أكبر حصة من إيرادات السوق في عام 2025، بفضل تطبيقه الواسع في صناعات رئيسية مثل توليد الطاقة وتصنيع الأسمنت، وفعاليته في التقاط الجسيمات الجافة، وانخفاض تعقيدات التشغيل نسبيًا في معالجة الغبار الجاف.

من المتوقع أن يشهد قطاع ESP الرطب أسرع معدل نمو سنوي مركب من عام 2025 إلى عام 2032، مدفوعًا بقدرته الفائقة على التعامل مع الجسيمات اللزجة أو المسببة للتآكل أو دون الميكرون، وفعاليته في إزالة الغازات الحمضية والمعادن الثقيلة في وقت واحد، مما يجعله مثاليًا للصناعات ذات تحديات الانبعاثات المعقدة.

- عن طريق العرض

بناءً على العرض، يُقسّم سوق المُرسِّبات الكهروستاتيكية إلى قسمين: الأجهزة والبرمجيات، والخدمات. وقد استحوذ قطاع الأجهزة والبرمجيات على أكبر حصة من إيرادات السوق في عام 2025، مدفوعًا بارتفاع الإنفاق الرأسمالي المرتبط بشراء وتركيب وحدات المُرسِّبات الكهروستاتيكية، والتي تشمل هيكل المُرسِّب، وإمدادات الطاقة، وأنظمة التحكم، والبرامج المُرتبطة بها للمراقبة والتشغيل.

The services segment is expected to witness the fastest CAGR from 2025 to 2032, fueled by the increasing need for maintenance, retrofitting, upgrades, and operational support to ensure optimal performance, extend the lifespan, and meet evolving emission standards for existing ESP installations.

- By End User

On the basis of end user, the electrostatic precipitator market is segmented into power generation, chemicals and petrochemicals, cement, metal processing and mining, manufacturing, marine, and others. The power generation segment accounted for the largest market revenue share in 2024, driven by stringent emission regulations on thermal power plants (coal and biomass) globally, and the large volume of flue gases requiring particulate control in this industry.

The marine segment is expected to witness the fastest CAGR from 2025 to 2032, driven by new regulations on exhaust gas cleaning systems from the International Maritime Organization (IMO) and increasing demand for cleaner emissions from ships to comply with sulfur and particulate matter limits in emission control areas.

Electrostatic Precipitator Market Regional Analysis

- Asia-Pacific dominates the electrostatic precipitator market with the largest revenue share of 45.60% in 2025, driven by rapid industrialization, especially in emerging economies such as China and India, and a growing demand for energy coupled with increasing governmental focus on mitigating industrial air pollution

- The region's substantial industrial base, combined with the implementation of stricter environmental policies and investment in new power plants and manufacturing facilities, significantly contributes to the high adoption of electrostatic precipitators

- This widespread use is further supported by local manufacturing capabilities and the drive for sustainable development

U.S. Electrostatic Precipitator Market Insight

The U.S. electrostatic precipitator market is projected to expand at a significant CAGR, driven by stringent environmental regulations, particularly the Clean Air Act, and the ongoing modernization of industrial infrastructure. Industries are increasingly investing in advanced emission control technologies to comply with federal and state mandates for particulate matter reduction. The focus on upgrading aging power plants and the expansion of manufacturing sectors are fueling the demand for highly efficient and reliable ESP systems. Furthermore, technological advancements in ESP designs that offer improved performance and energy efficiency are contributing to market growth in the U.S.

Europe Electrostatic Precipitator Market Insight

The European electrostatic precipitator market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by the European Union's stringent Industrial Emissions Directive (IED) and the escalating need for enhanced air quality in industrial and urban areas. The increasing focus on decarbonization and circular economy principles is fostering the adoption of advanced ESPs in sectors such as power generation, waste-to-energy, and metallurgy. European industries are also drawn to the long-term operational efficiency and low maintenance of these devices. The region is experiencing significant growth across various industrial applications, with ESPs being incorporated into both new constructions and retrofitting projects to meet ambitious emission reduction targets.

U.K. Electrostatic Precipitator Market Insight

The U.K. electrostatic precipitator market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the escalating trend of industrial modernization and a desire for heightened environmental compliance. In addition, concerns regarding air quality and public health are encouraging both industries and power generators to choose advanced particulate control solutions. The UK’s embrace of sustainable industrial practices, alongside its robust manufacturing and energy infrastructure, is expected to continue to stimulate market growth, with a particular focus on upgrading existing facilities to meet post-Brexit environmental standards.

Germany Electrostatic Precipitator Market Insight

The German electrostatic precipitator market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of industrial air quality and the demand for technologically advanced, energy-efficient, and sustainable solutions. Germany’s well-developed industrial infrastructure, combined with its emphasis on innovation and green technologies, promotes the adoption of ESPs, particularly in power generation, chemical, and cement sectors. The integration of ESPs with smart monitoring and control systems is also becoming increasingly prevalent, with a strong preference for high-performance, long-lasting solutions aligning with local industry expectations and stringent environmental regulations.

Asia-Pacific Electrostatic Precipitator Market Insight

The Asia-Pacific electrostatic precipitator market is poised to grow at the fastest CAGR, driven by increasing industrialization, rising energy demand, and rapid urbanization in countries such as China, Japan, and India. The region's growing inclination towards stricter environmental regulations, supported by government initiatives promoting cleaner production, is driving the adoption of ESPs across diverse industries. Furthermore, as APAC emerges as a manufacturing hub for industrial equipment and environmental technologies, the affordability and accessibility of ESP solutions are expanding to a wider industrial base, leading to significant market expansion.

Japan Electrostatic Precipitator Market Insight

The Japan electrostatic precipitator market is gaining momentum due to the country’s high-tech manufacturing sector, strong environmental consciousness, and demand for highly efficient and compact air pollution control solutions. The Japanese market places a significant emphasis on technological precision and reliability, and the adoption of ESPs is driven by the increasing need for advanced emission control in power plants, steel mills, and various industrial facilities. The integration of ESPs with smart monitoring, predictive maintenance, and energy-efficient designs is fueling growth. Moreover, Japan's focus on sustainable development and circular economy models is likely to spur demand for cutting-edge ESP technologies in both new projects and existing infrastructure upgrades.

China Electrostatic Precipitator Market Insight

The China electrostatic precipitator market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country's rapid industrial growth, massive energy consumption, and the government's aggressive push for environmental protection. China stands as one of the largest industrial nations, and ESPs are becoming increasingly vital in sectors such as coal-fired power generation, cement, and metallurgy to combat severe air pollution. The "Blue Sky" initiatives and ultra-low emission policies, coupled with the availability of robust domestic manufacturers and continuous technological upgrades, are key factors propelling the market in Chin.

Electrostatic Precipitator Market Share

The electrostatic precipitators industry is primarily led by well-established companies, including:

- FLSmidth Cement A/S (U.S.)

- Siemens (U.S.)

- Babcock & Wilcox Enterprises, Inc. (U.S.)

- John Wood Group PLC (U.K.)

- SEI (U.S.)

- KC Cottrell (India)

- Balcke-Dürr GmbH (Germany)

- ELEX AG (Switzerland)

- Beltran Technologies, Inc. (U.S.)

- Mitsubishi Hitachi Power, Ltd. (Japan)

- Fujian Longking Co., Ltd. (China)

- GEA Group Aktiengesellschaft (Germany)

- Thermax Limited (India)

- Sumitomo Heavy Industries, Ltd. (Japan)

- Bharat Heavy Electricals Limited (India)

Latest Developments in Global Electrostatic Precipitator Market

-

In May 2024, Ardagh Glass Packaging-Africa installed an electrostatic precipitator (ESP) at its Wadeville facility to minimize dust and smoke emissions, ensuring compliance with strict environmental regulations. This investment underscores the company’s commitment to industrial sustainability and air quality improvement. The ESP technology enhances filtration efficiency, supporting cleaner production processes while aligning with global emission standards. Ardagh continues to integrate advanced environmental solutions across its operations

- In January 2024, Babcock & Wilcox (B&W) acquired Hamon Research-Cottrell’s emissions control technologies, enhancing its portfolio of advanced air quality control systems. This strategic acquisition expands B&W’s capabilities in emissions reduction, offering customers improved solutions for cleaner energy production. By integrating Hamon Research-Cottrell’s expertise, B&W strengthens its commitment to environmental sustainability and regulatory compliance. The move reinforces B&W’s leadership in air quality control innovations

- In March 2023, GEA Group AG formed a strategic partnership with environmental engineering firms in India and Southeast Asia to expand its regional presence and deliver next-generation electrostatic precipitator (ESP) solutions. This collaboration addresses the increasing demand for air pollution control in rapidly industrializing regions, reinforcing GEA’s commitment to sustainability and advanced emissions reduction technologies. By leveraging innovative ESP systems, the partnership aims to enhance air quality and regulatory compliance across diverse industries

- In December 2022, General Electric Company introduced a technical solution aimed at reducing carbon emissions through engineering studies integrating Selective Catalytic Reduction (SCR) technology. This innovation effectively curbs nitrogen oxide (NOx) and carbon monoxide (CO) emissions by over 90%, surpassing World Bank Emissions Standards. By leveraging advanced emission control systems, GE reinforces its commitment to sustainability and cleaner energy solutions. The initiative aligns with global efforts to mitigate environmental impact and enhance air quality.

- In December 2022, ProcessBarron, a U.S.-based manufacturer specializing in air and gas handling products, established a wholly-owned subsidiary in Toronto, Canada. This expansion strengthens its presence in North America, enabling the company to provide electrostatic precipitator and air pollution control services through its Southern Field-Environmental Elements division. The subsidiary aims to enhance service offerings and operational reach, supporting industries with advanced air quality solutions. By investing in regional growth, ProcessBarron reinforces its commitment to environmental sustainability and industrial efficiency

SKU-

احصل على إمكانية الوصول عبر الإنترنت إلى التقرير الخاص بأول سحابة استخبارات سوقية في العالم

- لوحة معلومات تحليل البيانات التفاعلية

- لوحة معلومات تحليل الشركة للفرص ذات إمكانات النمو العالية

- إمكانية وصول محلل الأبحاث للتخصيص والاستعلامات

- تحليل المنافسين باستخدام لوحة معلومات تفاعلية

- آخر الأخبار والتحديثات وتحليل الاتجاهات

- استغل قوة تحليل المعايير لتتبع المنافسين بشكل شامل

منهجية البحث

يتم جمع البيانات وتحليل سنة الأساس باستخدام وحدات جمع البيانات ذات أحجام العينات الكبيرة. تتضمن المرحلة الحصول على معلومات السوق أو البيانات ذات الصلة من خلال مصادر واستراتيجيات مختلفة. تتضمن فحص وتخطيط جميع البيانات المكتسبة من الماضي مسبقًا. كما تتضمن فحص التناقضات في المعلومات التي شوهدت عبر مصادر المعلومات المختلفة. يتم تحليل بيانات السوق وتقديرها باستخدام نماذج إحصائية ومتماسكة للسوق. كما أن تحليل حصة السوق وتحليل الاتجاهات الرئيسية هي عوامل النجاح الرئيسية في تقرير السوق. لمعرفة المزيد، يرجى طلب مكالمة محلل أو إرسال استفسارك.

منهجية البحث الرئيسية التي يستخدمها فريق بحث DBMR هي التثليث البيانات والتي تتضمن استخراج البيانات وتحليل تأثير متغيرات البيانات على السوق والتحقق الأولي (من قبل خبراء الصناعة). تتضمن نماذج البيانات شبكة تحديد موقف البائعين، وتحليل خط زمني للسوق، ونظرة عامة على السوق ودليل، وشبكة تحديد موقف الشركة، وتحليل براءات الاختراع، وتحليل التسعير، وتحليل حصة الشركة في السوق، ومعايير القياس، وتحليل حصة البائعين على المستوى العالمي مقابل الإقليمي. لمعرفة المزيد عن منهجية البحث، أرسل استفسارًا للتحدث إلى خبراء الصناعة لدينا.

التخصيص متاح

تعد Data Bridge Market Research رائدة في مجال البحوث التكوينية المتقدمة. ونحن نفخر بخدمة عملائنا الحاليين والجدد بالبيانات والتحليلات التي تتطابق مع هدفهم. ويمكن تخصيص التقرير ليشمل تحليل اتجاه الأسعار للعلامات التجارية المستهدفة وفهم السوق في بلدان إضافية (اطلب قائمة البلدان)، وبيانات نتائج التجارب السريرية، ومراجعة الأدبيات، وتحليل السوق المجدد وقاعدة المنتج. ويمكن تحليل تحليل السوق للمنافسين المستهدفين من التحليل القائم على التكنولوجيا إلى استراتيجيات محفظة السوق. ويمكننا إضافة عدد كبير من المنافسين الذين تحتاج إلى بيانات عنهم بالتنسيق وأسلوب البيانات الذي تبحث عنه. ويمكن لفريق المحللين لدينا أيضًا تزويدك بالبيانات في ملفات Excel الخام أو جداول البيانات المحورية (كتاب الحقائق) أو مساعدتك في إنشاء عروض تقديمية من مجموعات البيانات المتوفرة في التقرير.