Global Neuroendocrine Tumors Market

حجم السوق بالمليار دولار أمريكي

CAGR :

%

USD

3.56 Billion

USD

7.87 Billion

2024

2032

USD

3.56 Billion

USD

7.87 Billion

2024

2032

| 2025 –2032 | |

| USD 3.56 Billion | |

| USD 7.87 Billion | |

| % | |

|

Global Neuroendocrine Tumors Market Segmentation, By Classification (Functional NET and Non-Functional NET), Site (Lung, Pancreas, Gastrointestinal Tract (GI), and Appendicular), Grade (Grade 1, Grade 2, and Grade 3), Type (Diagnosis and Treatment), Product (Somatostatin Analogs, Targeted Therapy, and Chemotherapy), End User (Hospitals, Specialty Clinics, Radiation Centers, Home Healthcare, and Others), Distribution Channel (Direct Tender, Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, and Other) - Industry Trends and Forecast to 2032

Neuroendocrine Tumors Market Size

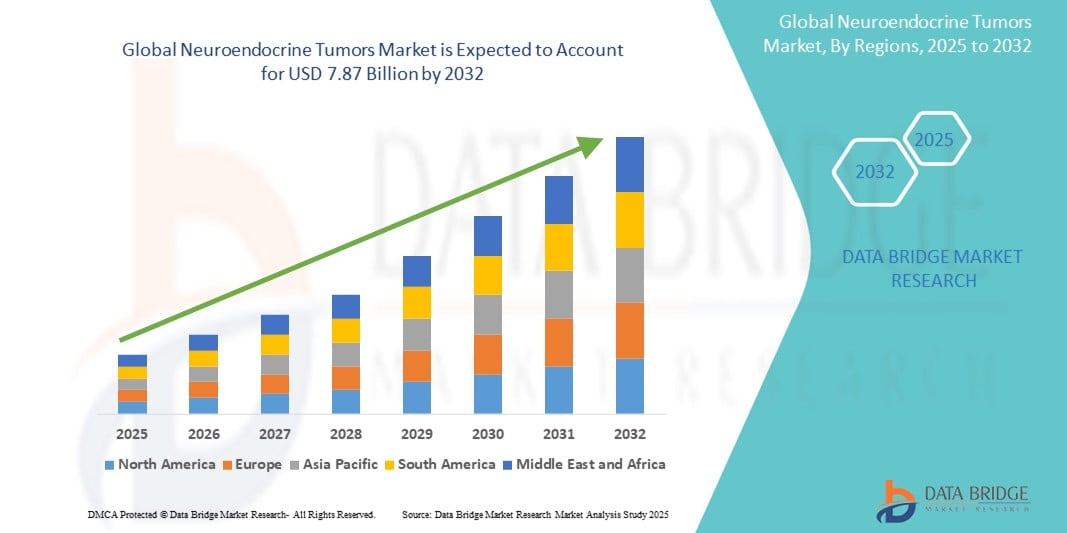

- The global neuroendocrine tumors market size was valued at USD 3.56 billion in 2024 and is expected to reach USD 7.87 billion by 2032, at a CAGR of 10.4% during the forecast period

- The market growth is largely fueled by the increasing incidence and prevalence of neuroendocrine tumors, coupled with significant advancements in diagnostic techniques leading to earlier and more accurate detection

- Furthermore, rising research and development activities, particularly in targeted therapies and novel treatment modalities such as peptide receptor radionuclide therapy (PRRT) and immunotherapies, are expanding treatment options and driving the adoption of these solutions, thereby significantly boosting the industry's growth

Neuroendocrine Tumors Market Analysis

- Neuroendocrine tumors (NETs), a diverse group of cancers originating from neuroendocrine cells, are increasingly recognized as a critical area in oncology. Their varied presentation and often slow growth necessitate advanced diagnostic and treatment modalities across both functional and non-functional types

- The escalating demand for neuroendocrine tumor treatments is primarily fueled by the increasing incidence and prevalence of these tumors globally, significant advancements in diagnostic techniques leading to earlier and more accurate detection, and a rising focus on research and development for novel and targeted therapies

- North America dominates the neuroendocrine tumors market with the largest revenue share of 42.5% in 2024, characterized by a robust healthcare infrastructure, high healthcare expenditure, the presence of key pharmaceutical and biotechnology companies, and a higher awareness and diagnosis rate of NETs. The U.S. specifically drives substantial growth due to extensive research initiatives and patient access to cutting-edge therapies

- Asia-Pacific is expected to be the fastest growing region in the neuroendocrine tumors market during the forecast period due to improving healthcare infrastructure, increasing awareness about NETs, rising disposable incomes, and a growing patient population seeking advanced treatment options

- Non-Functional NET segment dominates the neuroendocrine tumors market with a market share of 52.1% in 2024, driven by its asymptomatic nature leading to later diagnosis at more advanced stages, and increased incidental detection due to the widespread use of advanced imaging techniques

Report Scope and Neuroendocrine Tumors Market Segmentation

|

Attributes |

Neuroendocrine Tumors Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Neuroendocrine Tumors Market Trends

“Advancements in Targeted Therapies and Precision Medicine”

- A significant and accelerating trend in the global neuroendocrine tumors (NETs) market is the continuous development and adoption of highly targeted therapies and precision medicine approaches. This involves understanding the specific molecular characteristics of individual tumors to tailor treatments, moving beyond traditional chemotherapy

- For instance, targeted drugs such as Everolimus and Sunitinib have been approved for pancreatic NETs, demonstrating improved progression-free survival. Similarly, Peptide Receptor Radionuclide Therapy (PRRT), such as with Lutathera has revolutionized the treatment of somatostatin receptor-positive NETs by delivering targeted radiation directly to tumor cells, offering a more precise and effective option for advanced cases

- The complex and heterogeneous nature of NETs is fostering a trend towards multidisciplinary team approaches and the establishment of specialized neuroendocrine tumor centers. These centers bring together endocrinologists, oncologists, surgeons, radiologists, and pathologists to provide comprehensive, individualized patient care, leading to optimized treatment strategies and improved outcomes. This coordinated approach is essential for managing the diverse clinical presentations and treatment pathways associated with NETs

- There is a robust trend of increasing research and development investment in the NET field, exploring new therapeutic avenues beyond existing options. This includes investigations into novel targeted therapies, immunotherapies, and combination regimens to overcome resistance and improve response rates. The focus is on identifying new molecular targets and developing drugs that can specifically interfere with the growth and spread of NET cells, aiming to provide more effective and durable treatment options for patients

- This trend towards more intelligent, precise, and integrated diagnostic and treatment approaches is fundamentally reshaping the landscape of neuroendocrine tumor management

Neuroendocrine Tumors Market Dynamics

Driver

“Increasing Incidence and Advancements in Diagnosis and Treatment”

- The increasing incidence and prevalence of neuroendocrine tumors (NETs) globally, coupled with significant advancements in diagnostic techniques and the continuous development of novel therapeutic options, are major drivers for the heightened demand in the neuroendocrine tumors market

- For instance, the global incidence of NETs has been rising steadily, with improved diagnostic methods such as Gallium-68 DOTATATE PET/CT scans allowing for earlier and more accurate detection. Companies are actively investing in R&D, with new targeted therapies and radioligand treatments expanding treatment landscapes and improving patient outcomes

- As healthcare providers become more adept at identifying NETs and as research yields more effective and targeted treatments, there is a compelling push for comprehensive management strategies. This is further supported by a growing understanding of the disease's complexity and the benefits of multidisciplinary care.

- Furthermore, increased awareness among both the medical community and the public regarding NETs is leading to more patients seeking timely diagnosis and treatment. The development of personalized medicine approaches, tailored to individual tumor characteristics, is also propelling the market by offering more effective and less toxic treatment options

- The rising number of clinical trials for innovative therapies, coupled with increasing investments from pharmaceutical and biotechnology companies in this therapeutic area, are key factors propelling the growth of the neuroendocrine tumors market. The focus on addressing unmet needs and improving the quality of life for NET patients further contributes to market expansion

Restraint/Challenge

“High Cost of Diagnosis and Treatment, and Diagnostic Complexities”

- Concerns surrounding the substantial financial burden of diagnosing and treating neuroendocrine tumors (NETs) pose a significant challenge to broader market penetration and patient access. The high costs associated with advanced diagnostic imaging, specialized pathology, and innovative therapies can be prohibitive for many patients and strain healthcare budgets globally

- For instance, treatments such as Peptide Receptor Radionuclide Therapy, while highly effective, come with a significant price tag. Similarly, sophisticated diagnostic tools such as Gallium-68 DOTATATE PET/CT scans, though crucial for accurate staging, represent a considerable expense. These high costs can lead to treatment delays or non-adherence, particularly in healthcare systems with limited reimbursement policies or in developing regions

- Addressing these financial barriers through robust reimbursement frameworks, patient assistance programs, and the development of more cost-effective generic or biosimilar options for some treatments is crucial for improving patient access

- In addition, the inherent complexities in diagnosing NETs present another major hurdle. Their rarity, diverse clinical presentations, and often non-specific symptoms can lead to prolonged diagnostic journeys and misdiagnoses

- The lack of universally accepted and easily accessible early diagnostic biomarkers contributes to this complexity. This diagnostic challenge can delay appropriate treatment initiation, potentially leading to disease progression and poorer outcomes

Neuroendocrine Tumors Market Scope

The market is segmented on the basis of classification, site, grade, type, product, end user, and distribution channel.

- By Classification

On the basis of classification, the neuroendocrine tumors market is segmented into functional NET and non-functional NET. The non-functional NET segment dominates the market with a market share of 52.1% in 2024, driven by its asymptomatic nature leading to later diagnosis at more advanced stages, and increased incidental detection due to the widespread use of advanced imaging techniques. These tumors often remain undetected until they cause symptoms due to their mass effect rather than hormone secretion.

The non-functional NET segment is also projected to be the fastest-growing segment, driven by continued improvements in diagnostic imaging leading to higher detection rates of previously undiscovered asymptomatic tumors

- By Site

On the basis of site, the neuroendocrine tumors market is segmented into lung, pancreas, gastrointestinal tract (GI), and appendicular. The gastrointestinal tract (GI) segment held the largest market revenue share in 2024. This dominance is attributed to the fact that Gastroenteropancreatic NETs collectively represent the most common subtype, comprising 55–70% of all NETs, making the GI tract the most frequent primary location.

The gastrointestinal tract (GI) segment is also expected to witness the fastest compound annual growth rate (CAGR) from 2025 to 2032 in the global neuroendocrine tumors (NETs) market, driven by the increasing prevalence of gastric cancer and the presence of a strong product pipeline. This segment's growth is further supported by advancements in diagnostic techniques and the development of novel therapeutic options.

- By Grade

On the basis of grade, the neuroendocrine tumors market is segmented into grade 1, grade 2, and grade 3. The grade 2 segment is expected to hold a significant market share in 2024, as many diagnosed NETs fall into this intermediate proliferative category, requiring ongoing monitoring and therapeutic interventions

The grade 3 segment is anticipated to witness the fastest growth rate, fueled by the aggressive nature of these high-grade tumors which necessitate immediate and intensive systemic treatment regimens, including novel and high-cost therapies, driving demand for these solutions.

- By Type

On the basis of type, the neuroendocrine tumors market is segmented into diagnosis and treatment. The treatment segment held the largest market revenue share in 2024, driven by the continuous and long-term need for therapeutic interventions once NETs are diagnosed, encompassing various treatment modalities from medical to surgical options

The diagnosis segment is expected to witness the fastest growth rate, fueled by continuous advancements in imaging technologies and the discovery of novel biomarkers that facilitate earlier and more precise detection of NETs, thereby increasing the patient pool entering the treatment pathway

- By Product

On the basis of product, the neuroendocrine tumors market is segmented into somatostatin analogs, targeted therapy, and chemotherapy. The somatostatin analogs segment dominates the neuroendocrine tumors market with the largest revenue share of 74% in 2024. This is driven by their established efficacy in both controlling symptoms and inhibiting tumor growth in a large proportion of somatostatin receptor-positive NETs, positioning them as a first-line and long-term treatment option

The targeted therapy segment is anticipated to witness the fastest CAGR during the forecast period, fueled by ongoing research and development efforts leading to the approval of new, highly specific drugs that offer improved efficacy and a more favorable side-effect profile for various NET subtypes

- By End User

On the basis of end user, the neuroendocrine tumors market is segmented into hospitals, specialty clinics, radiation centers, home healthcare, and others. The Hospitals segment held the largest market revenue share in 2024, driven by their comprehensive infrastructure, access to multidisciplinary teams, advanced diagnostic capabilities, and the capacity to administer complex, often inpatient, treatments such as PRRT and specialized surgeries.

The specialty clinics segment is anticipated to grow at the highest CAGR during the forecast period, which can be attributed to patients' increasing preference for outpatient care models and specialized expertise offered by these centers, leading to greater patient traffic

- By Distribution Channel

On the basis of end user, the neuroendocrine tumors market is segmented into Direct Tender, Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, and Other. The retail pharmacies segment accounted for the largest market revenue share in 2024, driven by their widespread accessibility, established consumer trust, and the ability to offer a broad range of products, from over-the-counter medications to prescription drugs. Retail pharmacies are often the first point of contact for individuals seeking medications, making them a crucial part of the healthcare system.

The direct tender segment is expected to witness the fastest compound annual growth rate (CAGR) from 2025 to 2032 in the global neuroendocrine tumors market, driven by the increasing focus on cost-effective procurement strategies by healthcare providers and the growing presence of suppliers in the market. This segment's growth is further supported by the expansion of healthcare infrastructure and the rising demand for specialized treatments for neuroendocrine tumors

Neuroendocrine Tumors Market Regional Analysis

- North America dominates the neuroendocrine tumors market with the largest revenue share of 42.5% in 2024, driven by characterized by a robust healthcare infrastructure, high healthcare expenditure, the presence of key pharmaceutical and biotechnology companies, and a higher awareness and diagnosis rate of NETs

- يقدر المستهلكون ومقدمو الرعاية الصحية في أمريكا الشمالية بشكل كبير إمكانية الوصول إلى تقنيات التشخيص المتقدمة والعلاجات المستهدفة المتطورة، إلى جانب سياسات السداد القوية التي تسهل اعتماد العلاجات الجديدة

- ويتم دعم هذا التبني الواسع النطاق من خلال الإنفاق المرتفع على الرعاية الصحية، والبنية التحتية الطبية المتقدمة من الناحية التكنولوجية، والتفضيل المتزايد لأساليب الطب الشخصي، مما يجعل أمريكا الشمالية مركزًا رئيسيًا للابتكار في إدارة الأمراض العصبية التنكسية.

نظرة عامة على سوق أورام الغدد الصماء العصبية في الولايات المتحدة

استحوذ سوق أورام الغدد الصماء العصبية في الولايات المتحدة على أكبر حصة من الإيرادات في أمريكا الشمالية، بنسبة 74% في عام 2024، مدفوعًا بالتوسع السريع في استخدام وسائل التشخيص المتقدمة والتوافر المتزايد للخيارات العلاجية الجديدة. ويولي مقدمو الرعاية الصحية أولوية متزايدة لتحسين إدارة أورام الغدد الصماء العصبية من خلال أدوات تشخيص دقيقة وأنظمة علاجية فعالة. ويعزز التفضيل المتزايد لمراكز الرعاية المتخصصة، إلى جانب الطلب القوي على العلاجات الموجهة وأساليب الطب الشخصي، نمو صناعة أورام الغدد الصماء العصبية. علاوة على ذلك، يُسهم التكامل المتزايد للبحث والتطوير السريري، بدعم من التمويل الحكومي القوي والاستثمارات الدوائية، بشكل كبير في توسع السوق.

نظرة عامة على سوق أورام الغدد الصماء العصبية في أوروبا

من المتوقع أن يشهد سوق أورام الغدد الصماء العصبية في أوروبا نموًا بمعدل نمو سنوي مركب كبير خلال فترة التوقعات، مدفوعًا بشكل رئيسي بزيادة الإنفاق على البحث والتطوير، وسياسات تعويض الرعاية الصحية المواتية، والتعاون الاستراتيجي بين الجهات الفاعلة الرئيسية. إن زيادة حالات أورام الغدد الصماء العصبية، إلى جانب التركيز المتزايد على التشخيص المبكر والإدارة متعددة التخصصات، تعزز اعتماد علاجات متقدمة لأورام الغدد الصماء العصبية. كما تستفيد أنظمة الرعاية الصحية الأوروبية من فوائد بروتوكولات العلاج المعمول بها وحملات التوعية المتزايدة التي تنظمها جماعات مناصرة المرضى. تشهد المنطقة نموًا ملحوظًا في مختلف أساليب العلاج، مع دمج علاجات جديدة في الممارسة السريرية والمبادئ التوجيهية الوطنية.

نظرة عامة على سوق أورام الغدد الصماء العصبية في المملكة المتحدة

من المتوقع أن ينمو سوق أورام الغدد الصماء العصبية في المملكة المتحدة بمعدل نمو سنوي مركب ملحوظ خلال فترة التوقعات، مدفوعًا بالتركيز المتزايد على تحسين نتائج علاج السرطان والرغبة في زيادة فرص الحصول على علاجات مبتكرة. إضافةً إلى ذلك، تُشجع المخاوف المتعلقة بالتشخيص المتأخر لأورام الغدد الصماء العصبية كلاً من مقدمي الرعاية الصحية والمرضى على البحث عن حلول تشخيصية وعلاجية متقدمة. ومن المتوقع أن يواصل نظام الرعاية الصحية القوي في المملكة المتحدة، إلى جانب استثماراته المتزايدة في أبحاث السرطان والتجارب السريرية، تحفيز نمو السوق.

نظرة عامة على سوق أورام الغدد الصماء العصبية في ألمانيا

من المتوقع أن يشهد سوق أورام الغدد الصماء العصبية في ألمانيا نموًا بمعدل نمو سنوي مركب كبير خلال الفترة المتوقعة، مدفوعًا بتزايد الوعي بالسرطانات النادرة والطلب على حلول رعاية صحية متطورة تكنولوجيًا وعالية الجودة. تُعزز البنية التحتية المتطورة في ألمانيا، إلى جانب تركيزها على الابتكار وسياسات السداد الفعّالة، اعتماد تشخيصات وعلاجات متقدمة لأورام الغدد الصماء العصبية، لا سيما في مراكز الأورام المتخصصة. ويتماشى تكامل مناهج الطب الدقيق والتفضيل القوي للحلول المدعومة بالأبحاث مع توقعات المستهلكين المحليين والقطاع الطبي، مما يُعزز توسع السوق.

نظرة عامة على سوق الأورام الغدد الصماء العصبية في منطقة آسيا والمحيط الهادئ

من المتوقع أن يشهد سوق أورام الغدد الصماء العصبية في منطقة آسيا والمحيط الهادئ نموًا بأسرع معدل نمو سنوي مركب خلال الفترة المتوقعة، مدفوعًا بتزايد حالات أورام الغدد الصماء العصبية، وارتفاع نفقات الرعاية الصحية، والتقدم التكنولوجي في دول مثل الصين واليابان والهند. ويساهم التوجه المتزايد في المنطقة نحو تحسين رعاية مرضى السرطان، بدعم من المبادرات الحكومية التي تشجع على تطوير البنية التحتية للرعاية الصحية، في تعزيز اعتماد علاجات أورام الغدد الصماء العصبية المتقدمة. علاوة على ذلك، ومع تزايد التركيز في منطقة آسيا والمحيط الهادئ على التشخيص المبكر وتوفير العلاجات المبتكرة، فإن تكلفة إدارة أورام الغدد الصماء العصبية وسهولة الوصول إليها تتوسع لتشمل قاعدة أوسع من المرضى.

نظرة عامة على سوق أورام الغدد الصماء العصبية في اليابان

يشهد سوق أورام الغدد الصماء العصبية في اليابان نموًا متزايدًا بفضل البنية التحتية المتطورة للرعاية الصحية في البلاد، والتركيز على الطب الدقيق، والطلب على رعاية متخصصة عالية الجودة. ويولي السوق الياباني اهتمامًا بالغًا بدقة التشخيص وفعالية العلاج، ويعود اعتماد علاجات أورام الغدد الصماء العصبية المتقدمة إلى تزايد عدد الحالات المُشخَّصة والأبحاث السريرية. ويساهم دمج مناهج الرعاية متعددة التخصصات مع التقنيات الطبية المتقدمة الأخرى، مثل التصوير المتطور، في تعزيز هذا النمو. علاوة على ذلك، من المتوقع أن يؤدي ارتفاع نسبة كبار السن في اليابان إلى زيادة الطلب على حلول فعالة وشاملة لإدارة أورام الغدد الصماء العصبية.

نظرة عامة على سوق أورام الغدد الصماء العصبية في الهند

استحوذ سوق أورام الغدد الصماء العصبية في الهند على أكبر حصة من إيرادات السوق في منطقة آسيا والمحيط الهادئ عام 2024، ويعزى ذلك إلى توسع الطبقة المتوسطة في البلاد، والتوسع الحضري السريع، وتحسين الوصول إلى المرافق الطبية المتخصصة. وتُعد الهند سوقًا سريعة النمو في مجال رعاية مرضى السرطان، وتزداد شعبية التشخيصات والعلاجات المتقدمة لأورام الغدد الصماء العصبية في المناطق الحضرية الكبرى. ويُعد السعي نحو تحسين برامج فحص السرطان وزيادة توافر خدمات الأورام المتخصصة، إلى جانب تنامي القدرات الدوائية المحلية، عوامل رئيسية تدفع عجلة نمو السوق في الهند.

حصة سوق أورام الغدد الصماء العصبية

وتدار صناعة الأورام الغدد الصماء العصبية بشكل أساسي من قبل شركات راسخة، بما في ذلك:

- شركة إف. هوفمان-لا روش المحدودة (سويسرا)

- بريستول مايرز سكويب (الولايات المتحدة)

- شركة فياتريس (الولايات المتحدة)

- شركة ثيرمو فيشر العلمية (الولايات المتحدة)

- شركة نوفارتيس إيه جي (سويسرا)

- شركة ريجينيرون للأدوية (الولايات المتحدة)

- شركة صن للصناعات الدوائية المحدودة (الهند)

- شركة تيفا للصناعات الدوائية المحدودة (إسرائيل)

- ليلي (الولايات المتحدة)

- لوبين (الهند)

- شركة العلوم الدقيقة (الولايات المتحدة)

- شركة فايزر (الولايات المتحدة)

- إيبسين فارما (فرنسا)

- شركة Advanced Accelerator Applications SA (فرنسا)

- شركة بيوسينثيما (الولايات المتحدة)

- شركة بيونانو جينوميكس (الولايات المتحدة)

- شركة إيلومينا (الولايات المتحدة)

- شركة جلاكسو سميث كلاين (المملكة المتحدة)

- هاتشميد (الصين)

أحدث التطورات في سوق الأورام الغدد الصماء العصبية العالمية

- في أبريل 2025، فُتح باب التسجيل في تجربة سريرية جديدة من المرحلة الأولى في مركز سيلفستر الشامل للسرطان، التابع لكلية الطب بجامعة ميامي ميلر، للمرضى المصابين بأورام الغدد الصماء العصبية عالية الدرجة. ستختبر هذه التجربة مزيجًا جديدًا من أدوية العلاج المناعي (نيفولوماب وإيبيليموماب) مقترنًا بفيروس مُذيب للأورام (SVV-001) (فيروس وادي سينيكا-001)، يُحقن مباشرةً في الأورام.

- في فبراير 2025، وافقت إدارة الغذاء والدواء الأمريكية (FDA) على دواء ميرداميتينيب (غوميكلي) لعلاج الورم العصبي الليفي من النوع الأول (NF1) لدى المرضى المصابين بأورام عصبية ليفية ضفيرة عرضية لا تستجيب للاستئصال الجراحي الكامل. ورغم أن الورم العصبي الليفي من النوع الأول ليس ورمًا غدديًا عصبيًا بشكل مباشر، إلا أنه اضطراب وراثي يمكن أن يسبب أورامًا مختلفة، بما في ذلك بعض الأورام ذات السمات الغددية العصبية. وتوفر هذه الموافقة خيارًا غير جراحي هامًا لنوع ورم صعب ضمن فئة مرضى مماثلة.

- في أبريل 2024، حصلت نوفارتس على موافقة إدارة الغذاء والدواء الأمريكية (FDA) على دواء لوتاثيرا لعلاج أورام الغدد الصماء العصبية المعدية المعوية لدى الأطفال. تُمثل هذه الموافقة تقدمًا كبيرًا، حيث أصبح لوتاثيرا أول علاج مُشعّ مُعتمد خصيصًا للأطفال المصابين بأورام الغدد الصماء العصبية المعدية المعوية، مما يُقدم أملًا جديدًا للمرضى الصغار ويوسع نطاق الطب الدقيق في طب أورام الأطفال.

- في مارس 2024، أعلنت شركة كرينيتكس للأدوية عن نتائج إيجابية في المرحلة الثانية من دراستها المفتوحة لدواء بالتوسوتين، وهو ناهض فموي تجريبي غير ببتيدي لمستقبلات السوماتوستاتين من النوع 2 (SST2)، لعلاج متلازمة الكارسينويد. وقد تبين أن بالتوسوتين يُحدث انخفاضًا سريعًا ومستدامًا في وتيرة وشدة نوبات الاحمرار وحركات الأمعاء المرتبطة بأورام الغدد الصماء العصبية.

- في ديسمبر 2023، أعلنت شركة بريستول مايرز سكويب (BMS) عن استحواذها على شركة رايزبيو مقابل حوالي 4.1 مليار دولار أمريكي. رايزبيو هي شركة أدوية إشعاعية في المرحلة السريرية، وعنصرها الرئيسي هو RYZ101، الذي يستهدف مستقبل السوماتوستاتين 2 (SSTR2)، والذي يُعبَّر عنه بشكل مفرط في أورام الخلايا البدينة الظهارية (GEP-NETs) وفي سرطان الرئة صغير الخلايا في مراحله المتقدمة (ES-SCLC). يُوسِّع هذا الاستحواذ حضور شركة BMS بشكل كبير في مجال العلاجات الصيدلانية الإشعاعية (RPTs)، ويهدف إلى تعزيز خط إنتاجها في مجال الأورام.

SKU-

احصل على إمكانية الوصول عبر الإنترنت إلى التقرير الخاص بأول سحابة استخبارات سوقية في العالم

- لوحة معلومات تحليل البيانات التفاعلية

- لوحة معلومات تحليل الشركة للفرص ذات إمكانات النمو العالية

- إمكانية وصول محلل الأبحاث للتخصيص والاستعلامات

- تحليل المنافسين باستخدام لوحة معلومات تفاعلية

- آخر الأخبار والتحديثات وتحليل الاتجاهات

- استغل قوة تحليل المعايير لتتبع المنافسين بشكل شامل

منهجية البحث

يتم جمع البيانات وتحليل سنة الأساس باستخدام وحدات جمع البيانات ذات أحجام العينات الكبيرة. تتضمن المرحلة الحصول على معلومات السوق أو البيانات ذات الصلة من خلال مصادر واستراتيجيات مختلفة. تتضمن فحص وتخطيط جميع البيانات المكتسبة من الماضي مسبقًا. كما تتضمن فحص التناقضات في المعلومات التي شوهدت عبر مصادر المعلومات المختلفة. يتم تحليل بيانات السوق وتقديرها باستخدام نماذج إحصائية ومتماسكة للسوق. كما أن تحليل حصة السوق وتحليل الاتجاهات الرئيسية هي عوامل النجاح الرئيسية في تقرير السوق. لمعرفة المزيد، يرجى طلب مكالمة محلل أو إرسال استفسارك.

منهجية البحث الرئيسية التي يستخدمها فريق بحث DBMR هي التثليث البيانات والتي تتضمن استخراج البيانات وتحليل تأثير متغيرات البيانات على السوق والتحقق الأولي (من قبل خبراء الصناعة). تتضمن نماذج البيانات شبكة تحديد موقف البائعين، وتحليل خط زمني للسوق، ونظرة عامة على السوق ودليل، وشبكة تحديد موقف الشركة، وتحليل براءات الاختراع، وتحليل التسعير، وتحليل حصة الشركة في السوق، ومعايير القياس، وتحليل حصة البائعين على المستوى العالمي مقابل الإقليمي. لمعرفة المزيد عن منهجية البحث، أرسل استفسارًا للتحدث إلى خبراء الصناعة لدينا.

التخصيص متاح

تعد Data Bridge Market Research رائدة في مجال البحوث التكوينية المتقدمة. ونحن نفخر بخدمة عملائنا الحاليين والجدد بالبيانات والتحليلات التي تتطابق مع هدفهم. ويمكن تخصيص التقرير ليشمل تحليل اتجاه الأسعار للعلامات التجارية المستهدفة وفهم السوق في بلدان إضافية (اطلب قائمة البلدان)، وبيانات نتائج التجارب السريرية، ومراجعة الأدبيات، وتحليل السوق المجدد وقاعدة المنتج. ويمكن تحليل تحليل السوق للمنافسين المستهدفين من التحليل القائم على التكنولوجيا إلى استراتيجيات محفظة السوق. ويمكننا إضافة عدد كبير من المنافسين الذين تحتاج إلى بيانات عنهم بالتنسيق وأسلوب البيانات الذي تبحث عنه. ويمكن لفريق المحللين لدينا أيضًا تزويدك بالبيانات في ملفات Excel الخام أو جداول البيانات المحورية (كتاب الحقائق) أو مساعدتك في إنشاء عروض تقديمية من مجموعات البيانات المتوفرة في التقرير.