Middle East And Africa Silicone Textile Chemicals Market

حجم السوق بالمليار دولار أمريكي

CAGR :

%

USD

18.90 Billion

USD

28.82 Billion

2024

2032

USD

18.90 Billion

USD

28.82 Billion

2024

2032

| 2025 –2032 | |

| USD 18.90 Billion | |

| USD 28.82 Billion | |

| % | |

|

Middle East and Africa Silicone Textile Chemicals Market Segmentation, By Type (Silicon Softeners, Micro Emulsion Silicon and Others), Form (Fluids, Emulsions and Antifoams), Silicone Technology (Polydimethylsiloxanes and Special Silicone Fluids), Silicone Modifications (Methyl Group, Amino Group, Hydrophilic Group, Hydrogen Group, and Other Organo Modifications), Textile Type (Component Fibers and Synthetic Fibers and Inorganic Fibers), Application (Apparel, Home And Office Furnishing, Technical Textiles and Others) - Industry Trends and Forecast to 2032

Silicone Textile Chemicals Market Size

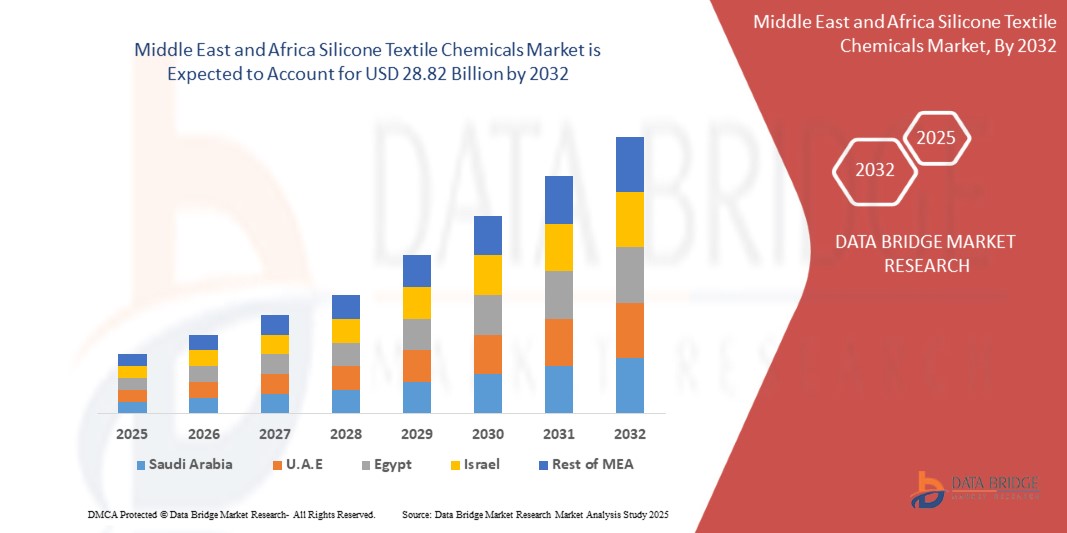

- The Middle East and Africa Silicone Textile Chemicals Market size was valued at USD 18.90 billion in 2024 and is expected to reach USD 28.82 billion by 2032, at a CAGR of 4.8% during the forecast period

- The market growth is largely fueled by the rising shift in consumer inclination towards foreign textile brands

- Furthermore, the rising research and development proficiencies on green or bio-based chemicals that are prepared from renewable resources, rising adoption of green chemicals and growth and expansion of various end user verticals such as chemicals and materials industry especially in the developing economies is further anticipated to propel the growth of the silicone textile chemicals market

Silicone Textile Chemicals Market Analysis

- The rise in the use of silicone textile chemicals for a wide range of end user applications such as apparel, home and office furnishing, technical textiles and others, strong influence of social media and surge in industrialization especially in the developing countries is escalating the growth of silicone textile chemicals market

- Silicone technology has brought in a revolution in the textile industry. Silicone textile chemicals are high purity silicone-based chemicals that are usually added in the pre-treatment of textiles. Some of the commonly used textile chemicals silicone textile chemicals are used in the form of fluids, emulsions, oils and antifoams

- Saudi Arabia dominates the Silicone Textile Chemicals market with the largest revenue share of 44.16% in 2025, characterized by the nation's strategic investments in diversifying its economy under the Vision 2030 initiative.

- South Africa is expected to be the fastest growing region in the Silicone Textile Chemicals market during the forecast period due to increasing demand for high-performance materials across various industries

- Silicon softeners segment is expected to dominate the Silicone Textile Chemicals market with a market share of 40.21% in 2025, driven by its cost-effectiveness, ease of formulation, and broad applicability across textile types

Report Scope and Silicone Textile Chemicals Market Segmentation

|

Attributes |

Silicone Textile Chemicals Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Silicone Textile Chemicals Market Trends

“Growing Integration of Smart Finishing Technologies in Textile Processing”

- A notable trend in the Middle East and Africa Silicone Textile Chemicals Market is the increasing use of smart finishing technologies to enhance textile properties such as softness, elasticity, water repellency, and durability. Advanced silicone-based finishes are enabling manufacturers to offer high-performance textiles for various end-use applications.

- For instance, new-generation amino-functional silicones provide better compatibility with synthetic and natural fibers, leading to improved hand feel and fabric resilience, especially in sportswear and home textiles.

- The trend also includes the development of multifunctional silicones that combine benefits such as anti-pilling, wrinkle resistance, and antimicrobial features, reducing the need for multiple chemical treatments.

- In parallel, the adoption of silicone-based softeners and hydrophobes that align with eco-certifications is rising, addressing both performance and sustainability criteria.

- These advancements are reshaping the Silicone Textile Chemicals landscape, supporting innovation in sustainable fabric enhancement while meeting evolving consumer and industry expectations.

Silicone Textile Chemicals Market Dynamics

Driver

“Rising Demand for Sustainable and High-Performance Textile Finishes”

- The growing demand for textile products with enhanced comfort, stretchability, and environmental compatibility is a major driver of the Silicone Textile Chemicals market. Silicone-based finishes offer superior softness, fabric protection, and long-lasting effects compared to conventional chemicals.

- Increasing consumer preference for eco-friendly and premium-quality garments is pushing textile manufacturers to adopt silicone solutions that meet both performance standards and regulatory compliance.

- Additionally, the shift toward water-efficient and low-VOC formulations is aligning with global sustainability trends, further boosting the market for silicone-based textile chemicals.

Restraint/Challenge

“Cost Sensitivity and Limited Adoption in Price-Conscious Markets”

- The relatively higher cost of silicone-based chemicals compared to traditional textile finishes remains a key restraint, particularly in price-sensitive markets such as Southeast Asia and parts of Africa.

- Smaller textile mills may hesitate to invest in silicone solutions due to budget constraints and uncertainty over immediate ROI, slowing adoption in emerging regions.

- Addressing this challenge requires pricing strategies, technological simplification, and awareness campaigns to demonstrate the long-term benefits and sustainability advantages of silicone textile chemicals.

Silicone Textile Chemicals Market Scope

The market is segmented on the basis of type, form, silicone technology, silicone modifications, textile type, and application.

- By Type

On the basis of type, the silicone textile chemicals market is segmented into silicon softeners, micro emulsion silicon, and others. The silicon softeners segment dominates the largest market revenue share of 40.21% in 2025, driven by its cost-effectiveness, ease of formulation, and broad applicability across textile types. Manufacturers favor silicon softeners due to their compatibility with traditional and modern textile finishes, and their ability to impart softness, flexibility, and enhanced hand-feel to fabrics. The market also sees rising demand due to environmentally compliant formulations and their proven performance in bulk dyeing and finishing operations.

The micro emulsion silicon segment is anticipated to witness the fastest growth rate of 21.7% from 2025 to 2032, fueled by its superior penetration, smoother surface finish, and versatility in blending with other softeners. Increasing use in high-end garments and technical fabrics supports this growth, along with the demand for sustainable, high-performance finishes in premium textile products.

- By Form

On the basis of form, the silicone textile chemicals market is segmented into fluids, emulsions, and antifoams. The fluids held the largest market revenue share in 2025 of, driven by their easy integration into manufacturing lines, stable performance under various processing conditions, and strong demand from the apparel and home furnishing sectors. These fluid forms allow high efficiency in the treatment process and are often tailored for specific textile properties like softness, drape, and static control.

The emulsions segment is expected to witness the fastest CAGR from 2025 to 2032, supported by increasing demand for cost-effective and water-based alternatives to conventional oils. Emulsions offer environmental compliance and versatility across applications, making them a favorable choice for textile processors seeking enhanced finishing results with reduced environmental impact.

- By Silicone Technology

On the basis of silicone technology, the meat testing market is segmented into polydimethylsiloxanes and special silicone fluids. The polydimethylsiloxanes segment accounted for the largest market revenue share in 2025, attributed to their well-established safety profile, cost-efficiency, and broad compatibility with textile formulations. Their consistent performance in imparting softness and improved tear strength positions them as a preferred base for a wide range of fabric softeners.

The special silicone fluids segment is projected to witness the fastest CAGR from 2025 to 2032, driven by growing demand in niche markets such as technical and medical textiles. These fluids offer enhanced durability, resistance to washing, and hydrophobicity, making them ideal for advanced textile finishes and high-performance fabrics.

- By Silicone Modifications

On the basis of silicone modifications, the meat testing market is segmented into methyl group, amino group, hydrophilic group, hydrogen group, and other organo modifications. The amino group segment dominates the largest market revenue share in 2025, due to its superior softening effects, fabric smoothness, and excellent compatibility with various textile chemistries. It is highly preferred in cotton and synthetic finishing processes for its long-lasting soft feel.

The hydrophilic group segment is expected to register the fastest CAGR from 2025 to 2032, owing to increasing demand for breathable, quick-drying, and moisture-managing fabrics in sportswear and technical textiles. Enhanced wearer comfort and rising consumer preference for functional garments further fuel this growth.

- By Textile Type

On the basis of textile type, the meat testing market is segmented into component fibers, synthetic fibers, and inorganic fibers. The synthetic fibers segment accounted for the largest market revenue share in 2025, owing to the high usage of polyester and nylon in mass textile manufacturing. The compatibility of silicone finishes with synthetic substrates enhances fabric softness, dye uptake, and aesthetic value.

The inorganic fibers segment is anticipated to witness the fastest CAGR from 2025 to 2032, supported by growing adoption in protective clothing, insulation materials, and specialty applications. These fibers benefit from silicone treatments for thermal stability and enhanced surface functionality, crucial in high-performance end-uses.

- By Application

On the basis of application, the meat testing market is segmented into apparel, home and office furnishing, technical textiles, and others. The apparel segment accounted for the largest market revenue share in 2025, driven by rising fashion trends, increased disposable income, and demand for comfortable, durable clothing. Silicone treatments are widely used to enhance softness, stretch, and wrinkle resistance in garments.

The technical textiles segment is projected to experience the fastest CAGR from 2025 to 2032, fueled by its growing importance in automotive, medical, and industrial sectors. The demand for performance-enhancing finishes, such as water repellency, antimicrobial effects, and thermal resistance, positions silicone treatments as essential in this high-growth category.

Silicone Textile Chemicals Market Regional Analysis

- Saudi Arabia dominates the Silicone Textile Chemicals Market with the largest revenue share of 44.16% in 2024, driven by the nation's strategic investments in diversifying its economy under the Vision 2030 initiative, which emphasizes the development of high-tech industries, including textiles.

- The presence of major chemical manufacturers like SABIC enhances the country's capacity to produce and supply silicone-based chemicals essential for textile applications.

- وعلاوة على ذلك، يتماشى تركيز المملكة العربية السعودية على الابتكار التكنولوجي والممارسات المستدامة مع الطلب العالمي على حلول النسيج المتقدمة، مما يعزز ريادتها في سوق المواد الكيميائية السيليكونية للنسيج في المنطقة.

نظرة عامة على سوق الكيماويات النسيجية السيليكونية في جنوب أفريقيا

من المتوقع أن يشهد سوق كيماويات النسيج السيليكونية في جنوب أفريقيا نموًا بمعدل نمو سنوي مركب يتجاوز 7.7% خلال الفترة المتوقعة من 2025 إلى 2032، مدفوعًا بتزايد الطلب على المواد عالية الأداء في مختلف القطاعات، بما في ذلك قطاعات السيارات والصناعة والملابس الواقية. تتميز كيماويات النسيج السيليكونية بخصائص مُحسّنة، مثل مقاومة درجات الحرارة والمتانة والمرونة، مما يجعلها مثالية للتطبيقات في هذه الصناعات. إضافةً إلى ذلك، يُسهم توسع قطاع التصنيع في جنوب أفريقيا والاستثمارات في تطوير البنية التحتية في تعزيز اعتماد تقنيات النسيج المتقدمة. كما تُسهم المبادرات الاستراتيجية للبلاد لتعزيز الإنتاج الصناعي وتركيزها على الابتكار في تسريع نمو سوق كيماويات النسيج السيليكونية.

نظرة عامة على سوق الكيماويات النسيجية السيليكونية في الإمارات العربية المتحدة

يشهد سوق كيماويات النسيج السيليكونية في الإمارات العربية المتحدة زخمًا متزايدًا بفضل توسع صناعة النسيج والملابس، والطلب المتزايد على المنسوجات التقنية في قطاعات مثل السيارات والرعاية الصحية. ويساهم تركيز الدولة على الابتكار وممارسات التصنيع المستدامة في زيادة اعتماد التشطيبات النسيجية القائمة على السيليكون لخصائص مثل مقاومة الماء والمرونة والمتانة. كما تدعم المبادرات الحكومية الاستراتيجية، مثل "عملية 300 مليار" لتعزيز النمو الصناعي، توسع السوق بشكل أكبر.

حصة سوق المواد الكيميائية النسيجية المصنوعة من السيليكون

إن صناعة المواد الكيميائية المصنوعة من السيليكون للنسيج يقودها في المقام الأول شركات راسخة، بما في ذلك:

- شركة ميتسوبيشي للكيماويات (اليابان)

- شركة شين إيتسو الكيميائية المحدودة (اليابان)

- شركة هانتسمان الدولية ذ.م.م (الولايات المتحدة)

- شركة واكر كيمي إيه جي (ألمانيا)

- مومنتيف (الولايات المتحدة)

- شركة إيفونيك للصناعات (ألمانيا)

- شركة إلكيم آسا (النرويج)

- شركة نيكا الولايات المتحدة الأمريكية المحدودة (الولايات المتحدة)

- شركة بيدمونت للصناعات الكيميائية (الولايات المتحدة)

- شركة CHT ألمانيا المحدودة (ألمانيا)

- شركة ويفانغ رويجوانج الكيميائية المحدودة (الصين)

- مجموعة zxchem (الصين)

- داو (الولايات المتحدة)

- نوريون (هولندا)

أحدث التطورات في سوق الكيماويات النسيجية السيليكونية في الشرق الأوسط وأفريقيا

- في يوليو 2024، أنشأت شركة جاي للصناعات الكيميائية الخاصة المحدودة منشأة تصنيع متطورة في سايخة، بالقرب من داهج، تُركز على إنتاج مشتقات أكسيد الإيثيلين وأكسيد البروبيلين، بالإضافة إلى منتجات مُركّبة تُستخدم بشكل رئيسي في المواد المساعدة للنسيج. تلعب هذه المشتقات دورًا حيويًا في خفض التوتر السطحي والتوتر البيني، مما يُحسّن استقرار وطول عمر مختلف المواد.

- في فبراير 2024، طرحت شركة بيرلا سيليلوز منتجها المبتكر "بيرلا فيسكوز - إنتلي كولور" (Birla Viscose – Intellicolor)، وهو حل نسيجي مُبتكر كُشف النقاب عنه في معرض بهارات تكس. يُعالج هذا الابتكار التحديات طويلة الأمد في الصباغة التفاعلية التقليدية، وذلك من خلال دمج الأصباغ الأساسية والكاتيونية، مما يُحقق استنفادًا للصبغة بنسبة تزيد عن 95%. والنتيجة هي ألوان أكثر حيوية، وتقليل استخدام المواد الكيميائية، وزيادة متانة القماش، وتسريع عمليات الإنتاج بشكل ملحوظ.

- في عام ٢٠٢٣، كثّفت شركات كيميائية رائدة، مثل داو، وأركيما، وباسف، اعتمادها للتقنيات الرقمية لتعزيز الكفاءة التشغيلية. وكان لهذا التحول دورٌ حاسمٌ في تحسين إنتاجية المواد الكيميائية النسيجية، بما في ذلك التركيبات القائمة على السيليكون، في ظل تقلب أسعار المواد الخام ومشاكل سلسلة التوريد المستمرة.

- في عام ٢٠٢٢، شهد القطاع تحولًا قويًا نحو حلول السيليكون المستدامة والصديقة للبيئة. وعززت شركات مثل Wacker Chemie وMomentive استثماراتها في تطوير بدائل صديقة للبيئة للمواد الكيميائية النسيجية التقليدية، ويعزى ذلك بشكل رئيسي إلى تزايد الوعي البيئي وتشديد المعايير التنظيمية العالمية.

SKU-

احصل على إمكانية الوصول عبر الإنترنت إلى التقرير الخاص بأول سحابة استخبارات سوقية في العالم

- لوحة معلومات تحليل البيانات التفاعلية

- لوحة معلومات تحليل الشركة للفرص ذات إمكانات النمو العالية

- إمكانية وصول محلل الأبحاث للتخصيص والاستعلامات

- تحليل المنافسين باستخدام لوحة معلومات تفاعلية

- آخر الأخبار والتحديثات وتحليل الاتجاهات

- استغل قوة تحليل المعايير لتتبع المنافسين بشكل شامل

منهجية البحث

يتم جمع البيانات وتحليل سنة الأساس باستخدام وحدات جمع البيانات ذات أحجام العينات الكبيرة. تتضمن المرحلة الحصول على معلومات السوق أو البيانات ذات الصلة من خلال مصادر واستراتيجيات مختلفة. تتضمن فحص وتخطيط جميع البيانات المكتسبة من الماضي مسبقًا. كما تتضمن فحص التناقضات في المعلومات التي شوهدت عبر مصادر المعلومات المختلفة. يتم تحليل بيانات السوق وتقديرها باستخدام نماذج إحصائية ومتماسكة للسوق. كما أن تحليل حصة السوق وتحليل الاتجاهات الرئيسية هي عوامل النجاح الرئيسية في تقرير السوق. لمعرفة المزيد، يرجى طلب مكالمة محلل أو إرسال استفسارك.

منهجية البحث الرئيسية التي يستخدمها فريق بحث DBMR هي التثليث البيانات والتي تتضمن استخراج البيانات وتحليل تأثير متغيرات البيانات على السوق والتحقق الأولي (من قبل خبراء الصناعة). تتضمن نماذج البيانات شبكة تحديد موقف البائعين، وتحليل خط زمني للسوق، ونظرة عامة على السوق ودليل، وشبكة تحديد موقف الشركة، وتحليل براءات الاختراع، وتحليل التسعير، وتحليل حصة الشركة في السوق، ومعايير القياس، وتحليل حصة البائعين على المستوى العالمي مقابل الإقليمي. لمعرفة المزيد عن منهجية البحث، أرسل استفسارًا للتحدث إلى خبراء الصناعة لدينا.

التخصيص متاح

تعد Data Bridge Market Research رائدة في مجال البحوث التكوينية المتقدمة. ونحن نفخر بخدمة عملائنا الحاليين والجدد بالبيانات والتحليلات التي تتطابق مع هدفهم. ويمكن تخصيص التقرير ليشمل تحليل اتجاه الأسعار للعلامات التجارية المستهدفة وفهم السوق في بلدان إضافية (اطلب قائمة البلدان)، وبيانات نتائج التجارب السريرية، ومراجعة الأدبيات، وتحليل السوق المجدد وقاعدة المنتج. ويمكن تحليل تحليل السوق للمنافسين المستهدفين من التحليل القائم على التكنولوجيا إلى استراتيجيات محفظة السوق. ويمكننا إضافة عدد كبير من المنافسين الذين تحتاج إلى بيانات عنهم بالتنسيق وأسلوب البيانات الذي تبحث عنه. ويمكن لفريق المحللين لدينا أيضًا تزويدك بالبيانات في ملفات Excel الخام أو جداول البيانات المحورية (كتاب الحقائق) أو مساعدتك في إنشاء عروض تقديمية من مجموعات البيانات المتوفرة في التقرير.