Global Automotive Plastics Market

Marktgröße in Milliarden USD

CAGR :

%

USD

33.84 Billion

USD

79.13 Billion

2024

2032

USD

33.84 Billion

USD

79.13 Billion

2024

2032

| 2025 –2032 | |

| USD 33.84 Billion | |

| USD 79.13 Billion | |

| % | |

|

Global Automotive Plastics Market Segmentation, By Product Type (Polypropylene, Polyurethane,Polyvinyl ChlorideAcrylonitrile-Butadiene-Styrene(ABS), Polyamide,High-Density Polyethylene (HDPE), Polycarbonate, Polybutylene Terephthalate (PBT), and Others), Vehicle Type (Conventional Cars and Electric Cars), Application (Powertrain, Electrical Components, Interior Furnishings, Under-The-Hood Components, Chassis, and Others) - Industry Trends and Forecast to 2032

Automotive Plastics Market Size

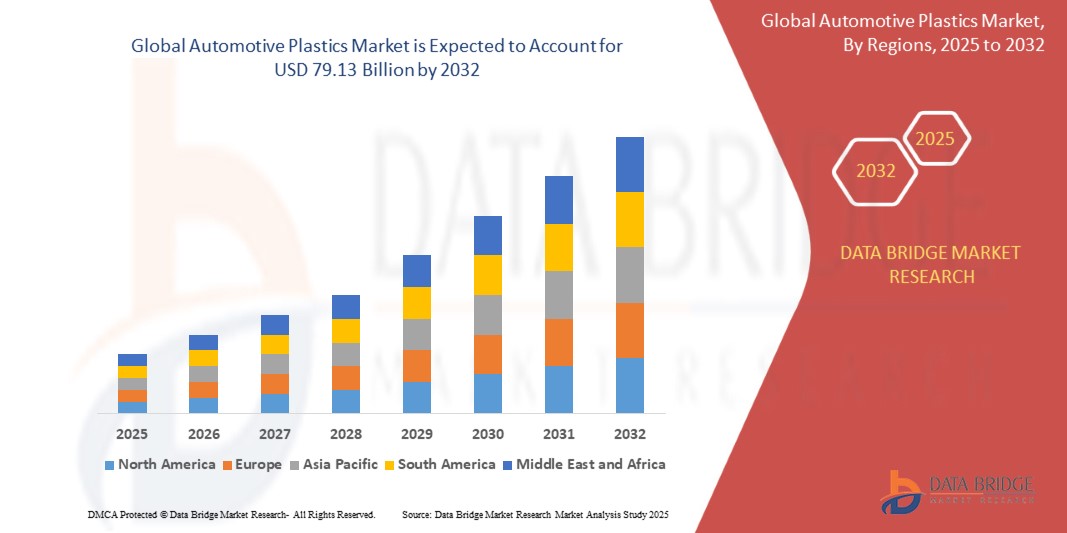

- The global automotive plastics market was valued atUSD 33.84 billion in 2024and is expected to reachUSD 79.13 billion by 2032

- During the forecast period of 2025 to 2032 the market is likely to grow at aCAGR of 11.20%,primarily driven by increasing demand for lightweight vehicles

- This growth is driven by the stringent government regulations on sustainability and the growing adoption of electric vehicles (EVs)

Automotive Plastics Market Analysis

- Automotive plastics has gained widespread acceptance due to its lightweight, durability, and high-performance characteristics, driving demand in vehicle manufacturing, electric vehicles (EVs), and sustainability initiatives. Its proven ability to enhance fuel efficiency, reduce carbon emissions, and improve crash safety has solidified its role in modern automotive engineering

- The market is primarily driven by increasing demand for lightweight materials, stringent government regulations on emissions, and the rising adoption of EVs. In addition, advancements in bio-based plastics and investments in automotive interiors are further accelerating market growth

- Asia-Pacific dominates the automotive plastics market due to its strong automotive manufacturing base, increasing vehicle production, and rapid adoption of sustainable materials

- For instance, inChina and India, the demand forlightweight plasticshas surged due to stringentfuel efficiencynorms and growingEV production, contributing to sustained market expansion

- Globally,automotive plasticscontinues to be acornerstoneinvehicle designandsustainability, with innovations such asrecyclable polymers,composite materials, andadvanced manufacturing techniquesdriving industry transformation and ensuring long-term market sustainability

Report Scope and Automotive Plastics Market Segmentation

|

Attributes |

Automotive Plastics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Automotive Plastics Market Trends

“Rising Integration of Automotive Plastics in Sustainable Vehicle Manufacturing”

- The increasing focus onsustainabilityis driving demand forautomotive plastics, widely recognized for its role inlightweight vehicle designandfuel efficiencyimprovement

- Automakersare expanding the use ofhigh-performance plasticsinelectric vehicles (EVs),interior components, andstructural applicationsto enhance durability and reduce overallcarbon footprint

- The rising adoption ofbio-based polymersandrecyclable materialsis accelerating the shift towardseco-friendly vehicle production, aligning with stringentgovernment regulationson emissions

For instance,

- InFebruary 2024,Teslaincorporatedadvanced polymer compositesin its latest EV model, enhancingbattery efficiencyand overallvehicle weight reduction

- InOctober 2023,Toyotaintroduced a newrecyclable plasticdashboard, reinforcing its commitment tosustainable automotive manufacturing

- InJuly 2023,BASFpartnered withleading automakersto developbio-based plasticsfor next-generationEV interiors, ensuring higher durability and lowerenvironmental impact

- As theautomotive industrycontinues to prioritizesustainability,automotive plasticswill play a crucial role invehicle innovation, driving efficiency, durability, and compliance with globalemission standards

Automotive Plastics Market Dynamics

Driver

“Growing Demand for Lightweight Vehicles”

- Increasingfuel efficiencyand reducingcarbon emissionsare key priorities for theautomotive industry, driving the adoption oflightweight plasticsas an alternative to metals.

- Automakersare incorporatinghigh-performance polymersinvehicle interiors, exteriors, and under-the-hood componentsto enhance durability, safety, and design flexibility

- The rising penetration ofelectric vehicles (EVs)further accelerates the need forlightweight materials, as reducing vehicle weight directly improvesbattery performance and driving range

For instance,

- InMarch 2024,Fordintegratedpolycarbonate-based componentsinto its new EV lineup to reduce vehicle weight and enhanceenergy efficiency

- InNovember 2023,General Motorspartnered withBASFto develophigh-strength plastic compositesfor structural applications, replacing traditional metal parts.

- InAugust 2023,Hyundaiannounced the use ofbio-based plasticsin its next-gen vehicle interiors, reinforcing its commitment tosustainable mobility

- With strictergovernment regulationsonfuel efficiencyandemissions, the demand forautomotive plasticswill continue to grow, driving innovation inlightweight vehicle designand sustainable manufacturing

Opportunity

“Expansion of Bio-Based and Recyclable Automotive Plastics”

- Growing environmental concerns and stringentgovernment regulationsare creating opportunities forbio-basedandrecyclable plastics, reducing reliance on fossil fuel-derived materials

- Automakersare investing insustainable plastic alternativesto meetcarbon neutrality goals, improveend-of-life recyclability, and enhancebrand sustainability efforts

- The increasing adoption ofcircular economy principlesinautomotive manufacturingis driving demand forrecycled polymers, minimizing waste and lowering production costs

For instance,

- InJanuary 2024,BMWlaunched a new initiative to incorporateocean-recycled plasticsinto its vehicle interiors, supporting itssustainability strategy

- InSeptember 2023,Volkswagenpartnered withbiopolymer manufacturersto integrateplant-based plasticsinto its upcoming EV models

- InJune 2023,Stellantiscommitted to using at least50% recycled plasticsin its next-generation vehicle components to reduceenvironmental impact

- As theautomotive industryaccelerates its shift towardseco-friendly materials,bio-based and recyclable plasticswill unlock new growth avenues, enhancingsustainability, innovation, and regulatory compliance

Restraint/Challenge

“Recycling Complexities in Automotive Plastics”

- Themulti-layered compositionofautomotive plastics, combined withadditives and reinforcements, makesrecycling difficultand limits the feasibility of acircular economyin the sector

- Automakersface challenges inseparating, sorting, and reprocessingplastic components fromend-of-life vehicles, increasingwaste management costs

- Strictergovernment regulationsonplastic waste disposalare pushing companies to invest inadvanced recycling technologies, further raisingoperational expenses

For instance,

- InMarch 2024,Renaultreported difficulties in recoveringcomposite plasticsfrom scrapped vehicles, impacting itssustainability goals

- Addressingrecycling inefficiencieswill be critical for theautomotive industry, ensuringcost-effective plastic reusewhile meetingglobal environmental regulations

Automotive Plastics Market Scope

The market is segmented on the basis of product type, vehicle type, and application.

|

Segmentation |

Sub-Segmentation |

|

By Product Type |

|

|

By Vehicle Type |

|

|

By Application |

|

Automotive Plastics Market Regional Analysis

“Asia-Pacific is the Dominant Region in the Automotive Plastics Market”

- Asia-Pacificleads the globalAutomotive Plasticsmarket, driven by rapidindustrialization, increasingautomobile production, and strong demand forlightweight materials

- ChinaandIndiadominate the region due to their expandingautomotive manufacturing, risingvehicle sales, and strong government incentives forfuel efficiency

- Advancements inpolymer technology, increasing adoption ofelectric vehicles (EVs), and rising consumer preference forsustainable materialshave further accelerated market growth

- In addition, the presence of majorautomotive suppliers, expandingOEM production, and growing investments inresearch & developmentcontribute to the region’s market leadership

“Asia-Pacific is projected to register the Highest Growth Rate”

- Asia-Pacificis expected to witness the highest growth rate in theautomotive plasticsmarket, driven by rapidurbanization, increasingvehicle production, and growing demand forlightweight components

- ChinaandIndiaare emerging as key markets due to strongautomotive manufacturing, supportive government policies, and rising investments inelectric mobility

- Chinaleads the region inautomotive plasticsproduction, with advancedpolymer processingtechnologies and increasing adoption ofsustainable materialsfor vehicle components

- Indiais experiencing strong market growth due to risingautomobile exports, expandingEV infrastructure, and growing consumer preference forfuel-efficient vehicles

- Stringentemission regulations, increasing R&D inbioplastics, and strategic collaborations betweenautomotive OEMsfurther contribute to Asia-Pacific’s market expansion

Automotive Plastics Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Magna International Inc. (Canada)

- Lear (U.S.)

- Adient plc (Ireland)

- BASF (Germany)

- Borealis AG (Austria)

- Covestro AG (Germany)

- Evonik Industries AG (Germany)

- SABIC (Saudi Arabia)

- Antolin (Spain)

- TOYOTA BOSHOKU CORPORATION (Japan)

- FORVIA HELLA (Germany)

- TOYODA GOSEI Co., Ltd. (Japan)

- Sage Automotive Interiors, Inc. (U.S.)

- DSM (Netherlands)

- Dow (U.S.)

- Momentive Performance Materials (U.S.)

- TEIJIN LIMITED (Japan)

- Solvay (Belgium)

- Akzo Nobel N.V. (Netherlands)

- CNR Group, LLC (U.S.)

Latest Developments in Global Automotive Plastics Market

- In June 2023,Borealis AGacquiredRialti S.p.A., a leadingpolypropylene (PP)compounding company specializing in recyclates in Italy’s Varese region. This acquisition strengthensBorealis'expertise and production capacity inPP compounding, particularly in increasing the volume of mechanically recycledPP compoundsto enhance its specialized and circular portfolios

- In May 2023,Learannounced plans to establish aconnection systems facilityin Morocco, aimed at manufacturing components for automakers, suppliers, and itsE-systemsandseating unitsto expand its automotive technology capabilities

- In November 2022,Covestro AGcollaborated withHASCO Visionto recyclepost-industrial plastics. Through this partnership,Covestrocollects used plastics fromHASCO'sproduction facilities, converts them into high-qualitypost-industrial recycled polycarbonatesandpolycarbonate blends, and supplies them back for manufacturing newautomotive components

- In June 2021,Lyondellbasellentered a long-term agreement withNesteto sourceNeste RE, a feedstock made entirely from renewable sources such as residue oils, fats, and waste. This material is processed atLyondellbasell'sWesseling, Germany, plant into polymers sold under theCirculenRenewbrand

- In May 2021,Lyondellbasellcommenced production ofvirgin-quality polymersusing raw materials derived from plastic waste at its Wesseling, Germany, facility. These raw materials are converted intopropyleneandethylene, which are further processed intopolypropylene (PP)andpolyethylene (PE)for plastics manufacturing

- In May 2021,ARKEMAcompleted the acquisition ofAgiplast, a company specializing in the regeneration ofhigh-performance polymers. This acquisition enablesARKEMAto become a fully integratedhigh-performance polymermanufacturer, focusing on bothrecycledandbio-based materialsto drive sustainability and circular economy initiatives

SKU-

Erhalten Sie Online-Zugriff auf den Bericht zur weltweit ersten Market Intelligence Cloud

- Interaktives Datenanalyse-Dashboard

- Unternehmensanalyse-Dashboard für Chancen mit hohem Wachstumspotenzial

- Zugriff für Research-Analysten für Anpassungen und Abfragen

- Konkurrenzanalyse mit interaktivem Dashboard

- Aktuelle Nachrichten, Updates und Trendanalyse

- Nutzen Sie die Leistungsfähigkeit der Benchmark-Analyse für eine umfassende Konkurrenzverfolgung

Forschungsmethodik

Die Datenerfassung und Basisjahresanalyse werden mithilfe von Datenerfassungsmodulen mit großen Stichprobengrößen durchgeführt. Die Phase umfasst das Erhalten von Marktinformationen oder verwandten Daten aus verschiedenen Quellen und Strategien. Sie umfasst die Prüfung und Planung aller aus der Vergangenheit im Voraus erfassten Daten. Sie umfasst auch die Prüfung von Informationsinkonsistenzen, die in verschiedenen Informationsquellen auftreten. Die Marktdaten werden mithilfe von marktstatistischen und kohärenten Modellen analysiert und geschätzt. Darüber hinaus sind Marktanteilsanalyse und Schlüsseltrendanalyse die wichtigsten Erfolgsfaktoren im Marktbericht. Um mehr zu erfahren, fordern Sie bitte einen Analystenanruf an oder geben Sie Ihre Anfrage ein.

Die wichtigste Forschungsmethodik, die vom DBMR-Forschungsteam verwendet wird, ist die Datentriangulation, die Data Mining, die Analyse der Auswirkungen von Datenvariablen auf den Markt und die primäre (Branchenexperten-)Validierung umfasst. Zu den Datenmodellen gehören ein Lieferantenpositionierungsraster, eine Marktzeitlinienanalyse, ein Marktüberblick und -leitfaden, ein Firmenpositionierungsraster, eine Patentanalyse, eine Preisanalyse, eine Firmenmarktanteilsanalyse, Messstandards, eine globale versus eine regionale und Lieferantenanteilsanalyse. Um mehr über die Forschungsmethodik zu erfahren, senden Sie eine Anfrage an unsere Branchenexperten.

Anpassung möglich

Data Bridge Market Research ist ein führendes Unternehmen in der fortgeschrittenen formativen Forschung. Wir sind stolz darauf, unseren bestehenden und neuen Kunden Daten und Analysen zu bieten, die zu ihren Zielen passen. Der Bericht kann angepasst werden, um Preistrendanalysen von Zielmarken, Marktverständnis für zusätzliche Länder (fordern Sie die Länderliste an), Daten zu klinischen Studienergebnissen, Literaturübersicht, Analysen des Marktes für aufgearbeitete Produkte und Produktbasis einzuschließen. Marktanalysen von Zielkonkurrenten können von technologiebasierten Analysen bis hin zu Marktportfoliostrategien analysiert werden. Wir können so viele Wettbewerber hinzufügen, wie Sie Daten in dem von Ihnen gewünschten Format und Datenstil benötigen. Unser Analystenteam kann Ihnen auch Daten in groben Excel-Rohdateien und Pivot-Tabellen (Fact Book) bereitstellen oder Sie bei der Erstellung von Präsentationen aus den im Bericht verfügbaren Datensätzen unterstützen.