Global Bookbinding Materials Market

Tamaño del mercado en miles de millones de dólares

Tasa de crecimiento anual compuesta (CAGR) :

%

USD

8.99 Billion

USD

11.47 Billion

2024

2032

USD

8.99 Billion

USD

11.47 Billion

2024

2032

| 2025 –2032 | |

| USD 8.99 Billion | |

| USD 11.47 Billion | |

| % | |

|

Segmentación del mercado global de materiales de encuadernación por tipo de encuadernación (adhesiva y mecánica), tipo de material (cubiertas de papel, cuero, adhesivos, tela o tela, y cartones), aplicación (libros de tapa dura y blanda, revistas y catálogos, e impresión bajo demanda), técnica de encuadernación (tapa dura, tapa blanda, hojas sueltas, anillas y encuadernación perfecta), sector de uso final (educación, industria editorial, impresión comercial, embalaje, bienes de consumo), grado (estándar, premium, archivo), tipo de disolvente (base disolvente, base agua y sin disolvente), tipo de resina (etileno acetato de vinilo, poliuretano y acrílico): tendencias del sector y pronóstico hasta 2032.

Tamaño del mercado de materiales de encuadernación

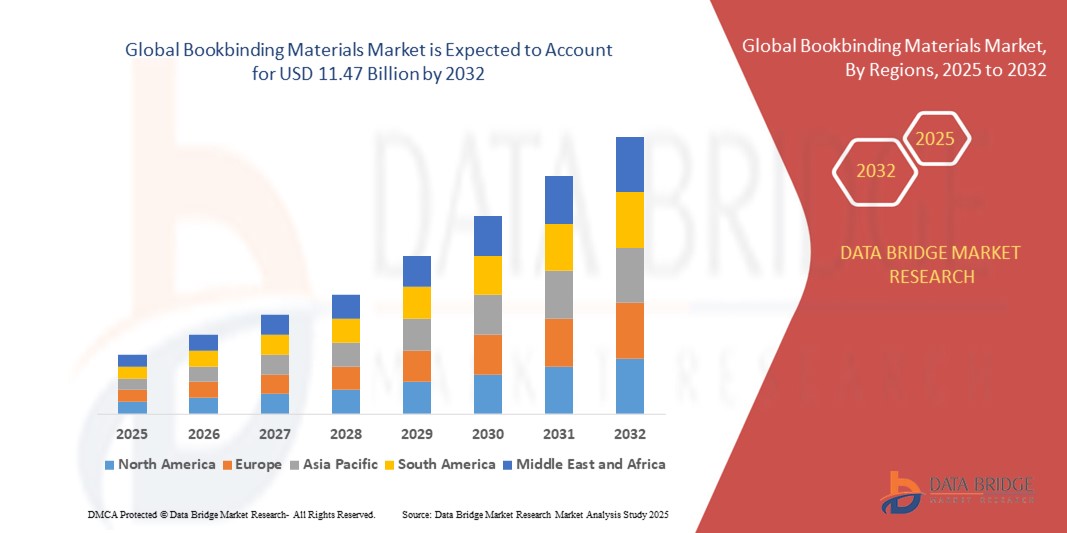

- El tamaño del mercado global de materiales de encuadernación se valoró en USD 8,99 mil millones en 2024 y se espera que alcance los USD 11,47 mil millones para 2032 , con una CAGR del 3,1% durante el período de pronóstico.

- El crecimiento del mercado está impulsado en gran medida por la creciente demanda de libros impresos en instituciones educativas, editoriales e imprentas comerciales, así como por los avances en materiales de encuadernación ecológicos y reciclables.

- El uso creciente de materiales de encuadernación en aplicaciones de embalaje, como cajas de lujo y materiales promocionales, también está apoyando la expansión del mercado al diversificar la demanda de uso final.

Análisis del mercado de materiales de encuadernación

- El mercado está experimentando un crecimiento constante debido al resurgimiento del interés en los libros físicos y la encuadernación premium para ediciones limitadas y publicaciones personalizadas.

- Los avances tecnológicos en materiales adhesivos y de recubrimiento, junto con un cambio hacia soluciones de unión sostenibles y duraderas, están contribuyendo a la expansión del mercado a largo plazo.

- Asia-Pacífico dominó el mercado de materiales de encuadernación con la mayor participación en los ingresos en 2024, impulsada por el sector educativo en expansión, la fuerte presencia de editoriales nacionales y capacidades de fabricación rentables.

- Se espera que la región de América del Norte sea testigo de la tasa de crecimiento más alta en el mercado mundial de materiales de encuadernación, impulsada por el resurgimiento de la publicación independiente, un mayor enfoque en materiales sostenibles e inversiones constantes en la producción de medios impresos de alta gama.

- El segmento de adhesivos obtuvo la mayor participación en los ingresos en 2024, impulsado por su uso generalizado en libros, revistas y catálogos de consumo masivo. Su rentabilidad y su capacidad para soportar líneas de producción de alta velocidad lo convierten en la opción preferida de impresores y editoriales comerciales. Además, los avances en las formulaciones de adhesivos han mejorado la resistencia y la durabilidad de la encuadernación, lo que refuerza aún más su dominio del mercado.

Alcance del informe y segmentación del mercado de materiales de encuadernación

|

Atributos |

Bookbinding Materials Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

• Rising Demand for Customized and Premium Binding Solutions |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Bookbinding Materials Market Trends

Sustainable and Eco-Friendly Binding Materials Gaining Traction

- The bookbinding materials market is witnessing a significant shift toward sustainable and eco-friendly products, driven by rising environmental awareness and stricter global regulations. Publishers, printers, and institutions are increasingly opting for biodegradable adhesives, recycled paper boards, and water-based coatings to reduce their carbon footprint and align with sustainability goals

- The demand for recyclable and non-toxic bookbinding materials is particularly strong in educational publishing and government-funded print initiatives. Institutions are encouraging vendors to comply with green procurement policies, which has boosted innovation in eco-certified raw materials

- Manufacturers are responding to this trend by investing in R&D to develop durable, green alternatives without compromising on performance. Bio-based polymers and renewable backing substrates are being adopted in mainstream production lines, increasing availability and lowering costs for sustainable bookbinding options

- For instance, in 2023, several leading bookbinding manufacturers in Europe launched FSC-certified product lines featuring 100% recycled board and low-VOC adhesives, targeting schools, libraries, and public sector publishers. These lines received positive feedback for both print quality and environmental compliance

- Although adoption is rising, success in this segment will require further innovation in material strength, print compatibility, and cost efficiency. Strong collaboration across supply chains is essential to scale sustainable bookbinding across global markets

Bookbinding Materials Market Dynamics

Driver

Revival of Print Media and Growth of Academic Publishing

• Despite digital disruption, print books continue to maintain a stronghold in educational and literary segments, fueling demand for bookbinding materials. Academic institutions and libraries are expanding their print collections, especially in regions where digital access is limited or costly. This has led to increased bulk orders for textbooks, journals, and academic resources requiring durable binding

• Consumers continue to value the tactile experience and longevity of printed materials, particularly in gift editions, limited prints, and premium publications. The durability and aesthetic appeal of hardcovers and sewn bindings are drawing attention in high-end and specialty publishing sectors

• Developing countries are experiencing a surge in literacy and educational infrastructure, creating steady demand for printed textbooks and learning materials. Governments are allocating budgets for public school resources, ensuring long-term support for the bookbinding industry

• For instance, in 2022, the Indian government’s National Education Policy emphasized textbook distribution across rural areas, prompting large-scale procurement of bound academic materials, boosting demand for board stock, cloth covers, and spine adhesives

• While digital platforms grow, the continued relevance of printed books in learning and reference contexts secures a solid foundation for the bookbinding materials market, especially in structured academic and public-sector applications

Restraint/Challenge

Volatility in Raw Material Prices and Supply Chain Disruptions

• Bookbinding materials such as paperboard, adhesives, and specialty fabrics are highly dependent on raw material costs, which have seen significant fluctuations due to global supply chain instability. Price volatility in pulp, resin, and chemical compounds impacts production planning and margins for manufacturers and converters

• The global logistics crisis, especially during post-pandemic recovery phases, has resulted in extended lead times and increased freight costs. These issues are particularly challenging for small and medium-scale bookbinders who depend on consistent material availability and pricing

• Environmental regulations and energy costs in major production hubs such as China and Europe have also affected the output and pricing of core inputs such as synthetic adhesives and coated boards, limiting supply and raising costs

• For instance, in 2023, several European bookbinding suppliers reported project delays due to disrupted imports of cover cloth and specialty glues from Asia, pushing clients to seek local but costlier alternatives

• To mitigate these risks, stakeholders must explore material substitution strategies, strengthen supplier diversification, and invest in local production capabilities. Technology-driven inventory planning and flexible sourcing will be key to minimizing disruptions in the bookbinding supply chain

Bookbinding Materials Market Scope

The market is segmented on the basis of binding type, material type, application, bookbinding technique, end-use sector, grade, solvent type, and resin type.

- By Binding Type

On the basis of binding type, the bookbinding materials market is segmented into adhesive bonded and mechanically bonded. The adhesive bonded segment held the largest revenue share in 2024, driven by its widespread use in mass-market books, magazines, and catalogs. Its cost-effectiveness and ability to support high-speed production lines make it the preferred choice for commercial printers and publishers. In addition, advancements in adhesive formulations have improved binding strength and durability, further supporting its market dominance.

The mechanically bonded segment is expected to witness the fastest growth rate from 2025 to 2032, fuelled by the rising demand for customization and durability in educational and corporate documentation. Mechanically bonded formats such as spiral and ring binding offer enhanced reusability and flexibility, making them ideal for training manuals, notebooks, and technical publications.

- By Material Type

On the basis of material type, the market is categorized into paper cover materials, leather, adhesives, cloth or fabric materials, and cover boards. The cover boards segment dominated the market in 2024 owing to their crucial role in providing structural integrity to hardcover books. These materials are extensively used across academic, archival, and luxury editions, offering rigidity and premium finish.

The adhesives segment is expected to witness the fastest growth rate from 2025 to 2032, supported by increased adoption of perfect binding and the development of high-performance, eco-friendly adhesives. Innovations in polymer technologies and growing interest in sustainable alternatives are contributing to segment expansion.

- By Application

On the basis of application, the market is segmented into hardcover and softcover books, magazines and catalogues, and print on demand. The hardcover and softcover books segment led the market in 2024, driven by continued demand from the education and publishing industries. The durability of hardcover formats and the affordability of softcover books together cater to a wide readership spectrum.

The print on demand segment is expected to witness the fastest growth rate from 2025 to 2032, supported by the rapid digitization of publishing and rising preference for self-publishing. This model allows publishers and authors to reduce inventory costs while catering to niche markets and customized orders.

- By Bookbinding Technique

On the basis of bookbinding technique, the market is segmented into hard case binding, soft case binding, loose-leaf binding, ring binding, and perfect binding. The perfect binding segment accounted for the largest market share in 2024, due to its suitability for mass production and attractive finish. It is widely used in paperback books, catalogs, and reports for its clean spine and efficient stacking.

Ring binding is expected to witness the fastest growth rate from 2025 to 2032, as it offers flexibility, ease of use, and the ability to update contents—making it highly popular in corporate training and educational materials.

- By End-use Sector

On the basis of end-use sector, the market is categorized into education, publishing industry, commercial printing, packaging, and consumer goods. The education segment held the largest market share in 2024, supported by the high volume demand for textbooks, workbooks, and reference materials. The segment continues to benefit from government initiatives, curriculum expansions, and student population growth.

The commercial printing segment is expected to witness the fastest growth rate from 2025 to 2032, driven by increased demand for customized, short-run printing jobs such as promotional booklets, manuals, and company brochures.

- By Grade

On the basis of grade, the market is segmented into standard grade, premium grade, and archival grade. The standard grade segment dominated the market in 2024 due to its extensive usage in mainstream publishing and education materials where cost-efficiency is essential.

The archival grade segment is expected to witness the fastest growth rate from 2025 to 2032, fueled by the increasing emphasis on document preservation across government archives, libraries, and museums.

- By Solvent Type

On the basis of solvent type, the market is segmented into solvent-based, water-based, and solvent-less adhesives. The solvent-based segment held the largest revenue share in 2024, due to its strong bonding capabilities and fast curing time, especially in high-speed printing operations.

The solvent-less adhesives segment i is expected to witness the fastest growth rate from 2025 to 2032, driven by growing environmental regulations, worker safety concerns, and the shift toward sustainable production practices.

- By Resin Type

On the basis of resin type, the market is segmented into ethylene vinyl acetate, polyurethane, and acrylic. Ethylene vinyl acetate dominated the market in 2024 due to its cost-effectiveness, ease of application, and strong adhesion properties in perfect binding processes.

The polyurethane segment is expected to witness the fastest growth rate from 2025 to 2032, attributed to its excellent resistance to heat, moisture, and mechanical stress—making it ideal for premium and archival-quality bookbinding.

Bookbinding Materials Market Regional Analysis

• Asia-Pacific dominated the bookbinding materials market with the largest revenue share in 2024, driven by the expanding education sector, strong presence of domestic publishers, and cost-effective manufacturing capabilities.

• Rapid urbanization, increasing literacy rates, and growing demand for printed educational and commercial content further accelerate market expansion across countries such as China, India, and Japan.

• The region's abundant raw material availability, large-scale printing hubs, and government support for educational infrastructure fuel the growth of both traditional and modern bookbinding solutions.

China Bookbinding Materials Market Insight

The China bookbinding materials market captured the largest revenue share within Asia-Pacific in 2024, supported by its dominant publishing industry and high consumption of educational and commercial printed materials. Strong domestic demand, coupled with increasing investments in digital printing technologies and aesthetic book presentation, drives growth. In addition, China’s role as a leading global manufacturing hub for binding materials ensures wide availability and competitive pricing across product segments.

Japan Bookbinding Materials Market Insight

The Japan bookbinding materials market is expected to witness the fastest growth rate from 2025 to 2032, supported by the country’s long-standing publishing traditions, high-quality print production, and emphasis on archival-grade materials. Demand is primarily driven by premium binding materials for literature, manga, and academic publishing. Japan’s focus on sustainability and innovation is encouraging the adoption of eco-friendly adhesives and recyclable cover materials in the bookbinding process.

North America Bookbinding Materials Market Insight

The North America bookbinding materials market is expected to witness the fastest growth rate from 2025 to 2032, led by increased demand for high-end and archival-grade products, particularly in the education and publishing sectors. The region's robust commercial printing industry, coupled with innovations in binding techniques and rising interest in artisanal and short-run publications, supports growth. Eco-conscious consumers and publishers are also influencing the shift toward sustainable binding materials and water-based adhesives.

U.S. Bookbinding Materials Market Insight

The U.S. bookbinding materials market held the majority share in North America in 2024, driven by a mature publishing industry, strong educational infrastructure, and demand for premium-quality binding solutions. Growth in on-demand publishing, self-publishing, and boutique book production has created new opportunities for advanced binding technologies and aesthetically appealing materials. U.S.-based manufacturers are also investing in digital transformation and sustainable product development to meet evolving consumer preferences.

Europe Bookbinding Materials Market Insight

The Europe bookbinding materials market is expected to witness the fastest growth rate from 2025 to 2032, supported by regulatory focus on sustainable packaging and the continued relevance of print in education and culture. Countries such as Germany, France, and the U.K. contribute significantly to market expansion through investments in academic publishing, art books, and hardcover productions. The region's commitment to quality, preservation, and innovation encourages the use of archival-grade adhesives and specialty cover materials.

Germany Bookbinding Materials Market Insight

The Germany bookbinding materials market is expected to witness the fastest growth rate from 2025 to 2032, driven by its well-established printing and publishing sectors, along with a strong tradition of bookmaking craftsmanship. Demand is high for premium binding materials used in literary, legal, and academic publications. Germany’s focus on environmental sustainability and product longevity is fostering the development of solvent-less adhesives and biodegradable binding solutions.

Bookbinding Materials Market Share

The Bookbinding Materials industry is primarily led by well-established companies, including:

- Henkel AG (Germany)

- H.B. Fuller Company (U.S.)

- Arkema (France)

- Dow Chemical Company (EE. UU.)

- UPM Global (Finlandia)

- BASF SE (Alemania)

- Henkel AG & Co. KGaA (Alemania)

- Compañía 3M (EE. UU.)

- Grupo Arkema (Francia)

- Dow Inc. (EE. UU.)

- Paramelt BV (Países Bajos)

- Evonik Industries AG (Alemania)

- HB Fuller Company (EE. UU.)

- Bostik (Francia)

- Ashland Global Holdings Inc. (EE. UU.)

Últimos avances en el mercado mundial de materiales de encuadernación

En julio de 2022, Arkema completó la adquisición de Permoseal, un destacado fabricante sudafricano de adhesivos, para ampliar su cartera de productos bajo la marca Bostik. Este desarrollo estratégico busca fortalecer la presencia de Arkema en los dinámicos mercados de adhesivos para la industria, la construcción y el bricolaje en Sudáfrica y África subsahariana. Se espera que la adquisición mejore la capacidad de fabricación local, amplíe su alcance de clientes e impulse el crecimiento en los mercados regionales emergentes. También refuerza el negocio global de adhesivos de Arkema al aprovechar nuevas oportunidades de crecimiento en las economías en desarrollo.

SKU-

Obtenga acceso en línea al informe sobre la primera nube de inteligencia de mercado del mundo

- Panel de análisis de datos interactivo

- Panel de análisis de empresas para oportunidades con alto potencial de crecimiento

- Acceso de analista de investigación para personalización y consultas

- Análisis de la competencia con panel interactivo

- Últimas noticias, actualizaciones y análisis de tendencias

- Aproveche el poder del análisis de referencia para un seguimiento integral de la competencia

Metodología de investigación

La recopilación de datos y el análisis del año base se realizan utilizando módulos de recopilación de datos con muestras de gran tamaño. La etapa incluye la obtención de información de mercado o datos relacionados a través de varias fuentes y estrategias. Incluye el examen y la planificación de todos los datos adquiridos del pasado con antelación. Asimismo, abarca el examen de las inconsistencias de información observadas en diferentes fuentes de información. Los datos de mercado se analizan y estiman utilizando modelos estadísticos y coherentes de mercado. Además, el análisis de la participación de mercado y el análisis de tendencias clave son los principales factores de éxito en el informe de mercado. Para obtener más información, solicite una llamada de un analista o envíe su consulta.

La metodología de investigación clave utilizada por el equipo de investigación de DBMR es la triangulación de datos, que implica la extracción de datos, el análisis del impacto de las variables de datos en el mercado y la validación primaria (experto en la industria). Los modelos de datos incluyen cuadrícula de posicionamiento de proveedores, análisis de línea de tiempo de mercado, descripción general y guía del mercado, cuadrícula de posicionamiento de la empresa, análisis de patentes, análisis de precios, análisis de participación de mercado de la empresa, estándares de medición, análisis global versus regional y de participación de proveedores. Para obtener más información sobre la metodología de investigación, envíe una consulta para hablar con nuestros expertos de la industria.

Personalización disponible

Data Bridge Market Research es líder en investigación formativa avanzada. Nos enorgullecemos de brindar servicios a nuestros clientes existentes y nuevos con datos y análisis que coinciden y se adaptan a sus objetivos. El informe se puede personalizar para incluir análisis de tendencias de precios de marcas objetivo, comprensión del mercado de países adicionales (solicite la lista de países), datos de resultados de ensayos clínicos, revisión de literatura, análisis de mercado renovado y base de productos. El análisis de mercado de competidores objetivo se puede analizar desde análisis basados en tecnología hasta estrategias de cartera de mercado. Podemos agregar tantos competidores sobre los que necesite datos en el formato y estilo de datos que esté buscando. Nuestro equipo de analistas también puede proporcionarle datos en archivos de Excel sin procesar, tablas dinámicas (libro de datos) o puede ayudarlo a crear presentaciones a partir de los conjuntos de datos disponibles en el informe.