Global Gastric Cancer Market

Tamaño del mercado en miles de millones de dólares

Tasa de crecimiento anual compuesta (CAGR) :

%

USD

7.24 Billion

USD

23.73 Billion

2025

2033

USD

7.24 Billion

USD

23.73 Billion

2025

2033

| 2026 –2033 | |

| USD 7.24 Billion | |

| USD 23.73 Billion | |

| % | |

|

Segmentación del mercado global del cáncer gástrico por tipo (adenocarcinoma, linfoma, tumor del estroma gastrointestinal, tumor carcinoide y otros), estadios (estadio I, estadio II, estadio III, estadio IV y otros), diagnóstico (endoscopia, biopsia, pruebas de imagen, cirugía exploratoria y otros), tratamiento (cirugía, radioterapia, quimioterapia, terapia dirigida, cuidados paliativos y otros), vía de administración (oral, parenteral y otras), usuarios finales (hospitales, atención domiciliaria, centros especializados y otros), canal de distribución (farmacia hospitalaria, farmacia en línea y farmacia minorista): tendencias y pronóstico de la industria hasta 2033.

Tamaño del mercado del cáncer gástrico

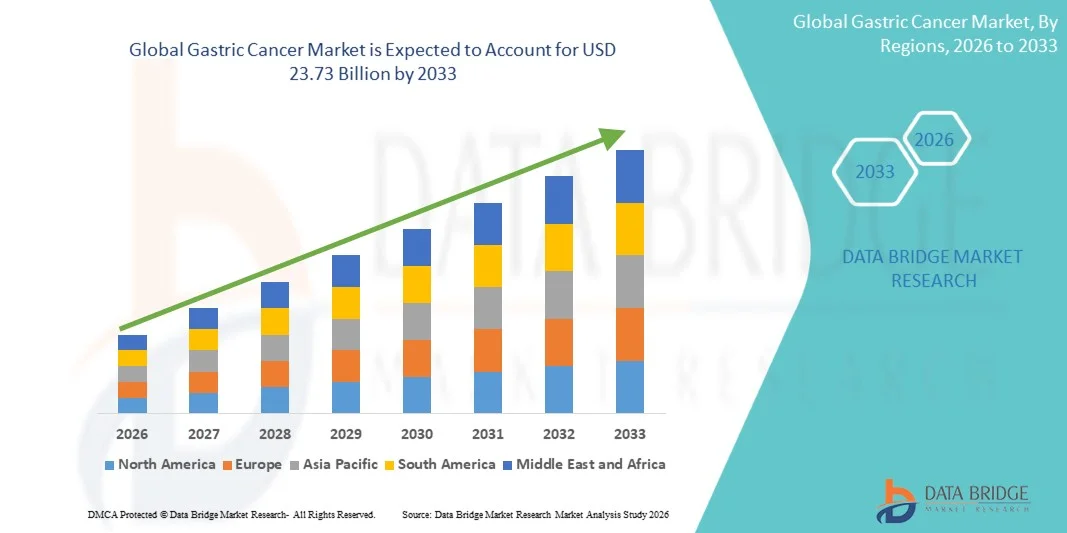

- El tamaño del mercado mundial del cáncer gástrico se valoró en 7.240 millones de dólares en 2025 y se espera que alcance los 23.730 millones de dólares en 2033 , con una tasa de crecimiento anual compuesta (CAGR) del 16,00% durante el período de pronóstico.

- El crecimiento del mercado se debe en gran medida a la creciente prevalencia del cáncer gástrico, la mayor concienciación sobre los métodos de detección precoz y los avances en terapias dirigidas y opciones de tratamiento mínimamente invasivas, que mejoran los resultados de los pacientes.

- Además, la expansión de la infraestructura sanitaria, la creciente adopción de nuevas inmunoterapias y el aumento de la inversión en investigación y desarrollo están posicionando las opciones de tratamiento avanzadas como la opción preferida para el manejo del cáncer gástrico. Estos factores convergentes están acelerando la adopción de terapias innovadoras, impulsando así significativamente el crecimiento de la industria.

Análisis del mercado del cáncer gástrico

- El cáncer gástrico, que engloba los tumores malignos del revestimiento del estómago, sigue siendo un problema de salud crítico a nivel mundial. El diagnóstico y el tratamiento se ven cada vez más respaldados por técnicas avanzadas de imagen, tecnologías endoscópicas y enfoques de medicina de precisión tanto en entornos clínicos como hospitalarios, debido a la mejora de los resultados de supervivencia y las opciones de terapia personalizada.

- El aumento de la prevalencia del cáncer gástrico se debe principalmente al envejecimiento de la población, a la creciente adopción de programas de detección precoz y a una mayor concienciación sobre factores de riesgo como la infección por H. pylori, los hábitos alimenticios y las predisposiciones genéticas.

- América del Norte dominó el mercado del cáncer gástrico con la mayor cuota de ingresos, un 37,5 % en 2025, caracterizada por un alto gasto en atención médica, una infraestructura oncológica avanzada y la adopción generalizada de opciones de detección temprana y tratamiento dirigido. Estados Unidos mostró un crecimiento sustancial en terapias dirigidas, inmunoterapias y procedimientos mínimamente invasivos, impulsado por la innovación tanto de compañías farmacéuticas establecidas como de empresas emergentes de biotecnología.

- Se prevé que la región de Asia-Pacífico sea la de mayor crecimiento en el mercado del cáncer gástrico durante el período de pronóstico, debido al mayor acceso a la atención médica, la creciente concienciación sobre el cáncer gástrico y la expansión de los programas de detección y tratamiento.

- El segmento de terapia dirigida dominó el mercado del cáncer gástrico en 2025, con una cuota de mercado del 43,2%, impulsado por su eficacia comprobada, su integración en las guías clínicas y la creciente preferencia de los oncólogos por los enfoques de oncología de precisión que mejoran los resultados de los pacientes.

Alcance del informe y segmentación del mercado del cáncer gástrico

|

Atributos |

Información clave sobre el mercado del cáncer gástrico |

|

Segmentos cubiertos |

|

|

Países incluidos |

América del norte

Europa

Asia-Pacífico

Oriente Medio y África

Sudamerica

|

|

Principales actores del mercado |

|

|

Oportunidades de mercado |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Gastric Cancer Market Trends

“Advancements in Precision Medicine and Targeted Therapies”

- A significant and accelerating trend in the global gastric cancer market is the increasing adoption of precision medicine approaches, including targeted therapies and biomarker-driven treatment strategies, which are enhancing treatment efficacy and personalization for patients

- For instance, trastuzumab-based therapies for HER2-positive gastric cancer enable oncologists to specifically target tumor cells, improving survival outcomes while minimizing systemic toxicity compared to conventional chemotherapy

- Integration of molecular diagnostics with treatment planning allows clinicians to tailor therapy regimens based on genetic mutations, tumor profiling, and patient-specific biomarkers, facilitating better response rates and fewer adverse effects

- Furthermore, combination therapies involving targeted agents and immunotherapies are gaining traction, offering new hope for patients with advanced or refractory gastric cancer, thereby reshaping standard-of-care protocols

- This trend towards personalized, biomarker-guided treatment is fundamentally transforming patient expectations and clinical approaches, with pharmaceutical companies such as Roche and Takeda developing next-generation therapies targeting specific gastric cancer subtypes

- The demand for targeted and precision-based therapies is growing rapidly across both early- and late-stage gastric cancer patient populations, as healthcare providers increasingly prioritize treatment effectiveness and reduced toxicity

- The growing focus on minimally invasive surgical techniques, such as laparoscopic and robotic-assisted gastrectomies, is improving patient recovery times and driving the adoption of advanced treatment protocols

Gastric Cancer Market Dynamics

Driver

“Increasing Incidence and Rising Awareness of Early Detection”

- The growing prevalence of gastric cancer worldwide, coupled with enhanced awareness and adoption of early detection and screening programs, is a significant driver for the rising demand for advanced treatment options

- For instance, national screening initiatives in countries such as Japan and South Korea have significantly improved early diagnosis rates, enabling timely intervention and better patient outcomes

- As patients and healthcare providers become more aware of risk factors such as H. pylori infection, dietary habits, and family history, early detection and preventive measures are increasingly emphasized, driving demand for diagnostics and treatment

- In addition, technological advances in endoscopy, imaging, and molecular testing are facilitating early-stage detection, contributing to improved survival rates and higher adoption of innovative therapies

- The growing prevalence of gastric cancer in both developed and developing regions, combined with patient demand for effective and personalized treatment solutions, is propelling market growth

- Rising investment in research and development by pharmaceutical and biotech companies is accelerating the discovery of novel drugs and combination therapies, further boosting market expansion

- Government initiatives and public-private partnerships promoting awareness campaigns, screening programs, and funding for oncology care are supporting increased early diagnosis and treatment adoption

Restraint/Challenge

“High Treatment Costs and Limited Access to Advanced Therapies”

- The high cost of targeted therapies, immunotherapies, and advanced diagnostics remains a significant challenge, limiting accessibility for patients, particularly in low- and middle-income regions

- For instance, the price of trastuzumab or ramucirumab-based regimens can be prohibitively expensive, restricting uptake despite proven clinical efficacy

- Limited healthcare infrastructure and uneven distribution of oncology centers in developing regions further constrain patient access to timely and effective treatment

- In addition, regulatory hurdles, complex clinical trial requirements, and slow approval processes for new drugs can delay market entry, impacting the availability of cutting-edge therapies

- While efforts are being made to introduce biosimilars and improve healthcare coverage, the combination of high costs and limited access continues to challenge widespread adoption of advanced gastric cancer treatments

- Patient hesitation and lack of awareness regarding advanced treatment options, particularly in rural areas, can delay care and limit market growth potential

- Variability in reimbursement policies and insurance coverage across regions further restricts patient access to high-cost therapies, impacting overall market penetration

Gastric Cancer Market Scope

The market is segmented on the basis of type, stages, diagnosis, treatment, route of administration, end-users, and distribution channel.

- By Type

On the basis of type, the gastric cancer market is segmented into adenocarcinoma, lymphoma, gastrointestinal stromal tumor (GIST), carcinoid tumor, and others. The adenocarcinoma segment dominated the market with the largest revenue share of 65% in 2025, driven by its high prevalence globally as it accounts for the majority of gastric cancer cases. Adenocarcinoma often requires multi-modal treatment approaches, including surgery, chemotherapy, and targeted therapy, increasing its market impact. The high incidence in regions such as East Asia and North America further reinforces its dominance. Rising awareness about early detection and improved diagnostic facilities for adenocarcinoma is also contributing to greater market adoption. Pharmaceutical companies prioritize the development of targeted therapies for adenocarcinoma due to the large patient population and potential for high treatment efficacy. Its established clinical protocols and strong research focus continue to sustain its leading market position.

The gastrointestinal stromal tumor (GIST) segment is anticipated to witness the fastest growth rate of 18.5% from 2026 to 2033, fueled by advancements in molecular-targeted therapies and growing awareness of rare gastric tumor subtypes. GISTs, though rare, respond well to targeted drugs such as imatinib, which has boosted market adoption. Increasing screening and molecular diagnostic capabilities are enabling earlier identification and treatment of GISTs. Growing R&D efforts in novel therapies and combination treatment regimens further drive growth. Rising investments by biotech companies in personalized treatment options for GISTs contribute to the accelerated adoption of these therapies. Furthermore, patient advocacy and awareness campaigns are enhancing diagnosis and treatment rates globally.

- By Stages

On the basis of stage, the market is segmented into Stage I, Stage II, Stage III, Stage IV, and others. The Stage III segment dominated the market with a revenue share of 37% in 2025, as patients in this stage typically require intensive treatment combining surgery, chemotherapy, and targeted therapy. Stage III gastric cancer presents significant clinical intervention opportunities, making it a key revenue-generating segment for pharmaceutical and diagnostic companies. Advanced diagnostic tools such as endoscopy and imaging tests are commonly utilized at this stage, boosting market adoption. Increasing survival rates due to early detection in preceding stages also expand the number of patients progressing to Stage III therapies. Pharmaceutical players focus on developing combination regimens for Stage III patients, further strengthening its market dominance. This stage also drives demand for hospital-based treatment infrastructure, increasing end-user market share.

The Stage I segment is expected to witness the fastest growth rate of 20.1% from 2026 to 2033, due to rising awareness of early detection programs, preventive screening, and minimally invasive treatment options. Early-stage gastric cancer allows for surgical resection and localized therapies, encouraging adoption of advanced diagnostics. Governments and healthcare organizations are promoting screening campaigns, increasing the patient pool for Stage I interventions. Technological advancements in imaging and endoscopic procedures support accurate early diagnosis. The growing preference for less aggressive, patient-friendly treatments further accelerates market growth.

- By Diagnosis

On the basis of diagnosis, the market is segmented into endoscopy, biopsy, imaging tests, exploratory surgery, and others. The endoscopy segment dominated the market with a revenue share of 42% in 2025, as it is the gold standard for detecting gastric cancer and enables both diagnosis and therapeutic intervention. Endoscopy provides real-time visualization and facilitates early detection, critical for improving survival rates. The procedure’s ability to perform biopsies simultaneously contributes to its high adoption. Increasing availability of advanced endoscopic technologies, including high-definition and AI-assisted scopes, further strengthens market dominance. Healthcare facilities prioritize endoscopy for its accuracy, cost-effectiveness, and widespread acceptance. Training programs for gastroenterologists and increased accessibility in hospitals further support adoption.

The imaging tests segment is anticipated to witness the fastest growth rate of 19.3% from 2026 to 2033, driven by technological advances such as PET-CT and MRI, which provide detailed tumor visualization and staging information. Imaging tests are increasingly integrated with AI and machine learning tools to improve diagnostic accuracy. Rising use of non-invasive diagnostics and patient preference for less discomfort contribute to market growth. Imaging enables precise treatment planning and monitoring, increasing adoption among hospitals and specialty centers. Research initiatives and clinical trials promoting imaging-based assessments further accelerate uptake.

- By Treatment

En función del tratamiento, el mercado se segmenta en cirugía, radioterapia, quimioterapia, terapia dirigida, cuidados paliativos y otros. El segmento de terapia dirigida dominó el mercado con una cuota del 43,2 % en 2025, impulsado por su eficacia en el tratamiento de subtipos específicos de cáncer gástrico, como los tumores HER2 positivos. Las terapias dirigidas mejoran los resultados de los pacientes, reducen la toxicidad sistémica y se integran bien con los enfoques de medicina personalizada. El creciente número de aprobaciones de nuevos productos biológicos y terapias combinadas refuerza aún más el dominio del mercado. La creciente concienciación entre oncólogos y pacientes sobre la oncología de precisión favorece su adopción. Las inversiones farmacéuticas en investigación y ensayos clínicos de nuevos fármacos dirigidos contribuyen al crecimiento del mercado. La disponibilidad de diagnósticos complementarios también refuerza la adopción de la terapia dirigida.

Se prevé que el segmento de inmunoterapia experimente el mayor crecimiento, del 22,5%, entre 2026 y 2033, impulsado por la creciente evidencia clínica que respalda su uso en el cáncer gástrico avanzado o refractario. Los inhibidores de puntos de control inmunitario, solos o en combinación con otras terapias, están ampliando las opciones de tratamiento. La creciente inversión de las empresas biotecnológicas y la actividad de los ensayos clínicos aceleran su adopción. Los pacientes con respuesta limitada a las terapias tradicionales optan cada vez más por la inmunoterapia. El respaldo de las aprobaciones regulatorias y la inclusión en las guías clínicas potencian aún más el potencial del mercado.

- Por vía administrativa

Según la vía de administración, el mercado se segmenta en oral, parenteral y otras. El segmento parenteral dominó el mercado con una cuota de ingresos del 51 % en 2025, impulsado por la administración intravenosa de quimioterapia, terapia dirigida y agentes de inmunoterapia, que garantizan una mayor biodisponibilidad y eficacia. La administración parenteral es la preferida para protocolos de tratamiento hospitalarios y pacientes en estadios avanzados. El monitoreo frecuente y los ajustes de dosis requieren supervisión clínica, lo que aumenta la dependencia hospitalaria. La creciente adopción de productos biológicos, anticuerpos monoclonales y regímenes combinados respalda el dominio del mercado. La innovación farmacéutica en formulaciones parenterales fortalece aún más su posición. Los hospitales y centros especializados prefieren la administración parenteral para obtener resultados de tratamiento controlados.

Se prevé que el segmento de administración oral experimente el mayor crecimiento, del 20,7%, entre 2026 y 2033, impulsado por el desarrollo de terapias dirigidas orales y agentes quimioterapéuticos. La administración oral ofrece comodidad al paciente, facilita el tratamiento domiciliario y mejora la adherencia. La creciente disponibilidad de formulaciones orales para el cáncer gástrico en etapas tempranas e intermedias fomenta su adopción. Las compañías farmacéuticas priorizan el desarrollo de fármacos orales por su facilidad de uso. La preferencia de los pacientes por opciones de tratamiento no invasivas impulsa aún más el crecimiento del mercado.

- Por los usuarios finales

En función de los usuarios finales, el mercado se segmenta en hospitales, atención domiciliaria, centros especializados y otros. El segmento de hospitales dominó el mercado con una cuota de ingresos del 58 % en 2025, ya que los hospitales ofrecen servicios integrales de diagnóstico y tratamiento para el cáncer gástrico, incluyendo cirugía, quimioterapia y terapia dirigida. Los hospitales también sirven como centros principales para ensayos clínicos y la administración de tratamientos avanzados. La concentración de especialistas en oncología, herramientas de diagnóstico e infraestructura en los hospitales impulsa la adopción. Las compras institucionales y los programas gubernamentales de salud refuerzan aún más el dominio del mercado. Los hospitales desempeñan un papel fundamental en la integración de terapias multimodales y la atención de seguimiento.

Se prevé que el segmento de atención domiciliaria experimente la tasa de crecimiento más rápida, del 19,8%, entre 2026 y 2033, impulsada por la creciente disponibilidad de terapias orales y opciones de cuidados paliativos que permiten el tratamiento en el domicilio del paciente. La creciente preferencia por la monitorización domiciliaria, la telemedicina y los servicios de cuidados paliativos favorece este crecimiento. La comodidad, el ahorro de costes y la reducción de las visitas al hospital fomentan su adopción. La pandemia de COVID-19 aceleró la adopción de servicios de atención domiciliaria para pacientes con cáncer. Las compañías farmacéuticas están desarrollando regímenes de tratamiento adaptados a las necesidades del paciente y adecuados para su administración en el hogar.

- Por canal de distribución

Según el canal de distribución, el mercado se segmenta en farmacias hospitalarias, farmacias en línea y farmacias minoristas. El segmento de farmacias hospitalarias dominó el mercado con una cuota de ingresos del 55 % en 2025, debido al acceso directo a los pacientes hospitalizados y a la adquisición centralizada de terapias de alto costo. Las farmacias hospitalarias garantizan la disponibilidad oportuna de medicamentos para la atención hospitalaria y ambulatoria. La colaboración con los departamentos de oncología y los programas de apoyo al paciente refuerza la adopción. Los acuerdos de compra al por mayor y la cobertura de seguros facilitan la asequibilidad y el acceso. Los hospitales brindan educación y asesoramiento sobre la administración de medicamentos, mejorando la adherencia del paciente al tratamiento.

Se prevé que el segmento de farmacias en línea experimente el mayor crecimiento, del 21,2%, entre 2026 y 2033, impulsado por la creciente penetración del comercio electrónico, la preferencia de los pacientes por la entrega a domicilio y el mayor conocimiento de las plataformas en línea que ofrecen medicamentos con receta y productos de apoyo. La comodidad, la accesibilidad y la privacidad son factores clave para la adopción de las farmacias en línea. La integración con la telemedicina y los servicios de atención domiciliaria acelera el crecimiento. Las farmacias en línea amplían su alcance de mercado a regiones remotas y desatendidas. Las iniciativas de marketing y las plataformas digitales aumentan la participación y el conocimiento de los pacientes.

Análisis regional del mercado del cáncer gástrico

- América del Norte dominó el mercado del cáncer gástrico con la mayor cuota de ingresos, un 37,5 % en 2025, caracterizada por un alto gasto en atención médica, una infraestructura oncológica avanzada y la adopción generalizada de opciones de detección temprana y tratamiento dirigido.

- Patients and healthcare providers in the region highly value access to targeted therapies, immunotherapies, minimally invasive surgical procedures, and comprehensive oncology care, which improve survival outcomes and quality of life

- This widespread adoption is further supported by government healthcare programs, strong R&D investment by pharmaceutical and biotech companies, and a well-established network of hospitals and specialty centers, establishing North America as a leading market for gastric cancer treatment

U.S. Gastric Cancer Market Insight

The U.S. gastric cancer market captured the largest revenue share of 32% in 2025 within North America, driven by advanced healthcare infrastructure, high awareness of early detection programs, and widespread adoption of targeted therapies and immunotherapies. Patients increasingly prioritize access to precision medicine, minimally invasive surgeries, and comprehensive oncology care. The growing integration of molecular diagnostics, AI-assisted imaging, and personalized treatment protocols further propels market growth. Moreover, government healthcare initiatives and substantial R&D investment by pharmaceutical and biotech companies continue to expand the availability and adoption of innovative gastric cancer therapies.

Europe Gastric Cancer Market Insight

The Europe gastric cancer market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising awareness of early screening programs, stringent healthcare regulations, and an increasing demand for advanced oncology treatments. Urbanization, improved healthcare infrastructure, and growing accessibility to innovative therapies are fostering market adoption. European patients are increasingly drawn to targeted therapies and minimally invasive surgical procedures. The region is witnessing notable growth across hospitals, specialty centers, and cancer clinics, with early-stage detection and precision medicine approaches being increasingly implemented.

U.K. Gastric Cancer Market Insight

The U.K. gastric cancer market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising adoption of advanced diagnostics, early detection programs, and targeted therapies. Growing concerns regarding cancer incidence and patient survival are encouraging both healthcare providers and patients to pursue personalized treatment approaches. The U.K.’s strong healthcare system, coupled with well-established oncology research initiatives, supports the introduction of novel therapies. Increased awareness campaigns, integration of molecular diagnostics, and accessibility to specialty care are expected to sustain market growth.

Germany Gastric Cancer Market Insight

The Germany gastric cancer market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of cancer prevention, advanced diagnostic facilities, and the demand for personalized treatment protocols. Germany’s well-developed healthcare infrastructure, emphasis on precision oncology, and robust hospital networks promote the adoption of advanced gastric cancer therapies. Integration of immunotherapy, targeted therapy, and minimally invasive surgery is increasingly prevalent. The focus on patient-centered care and government initiatives supporting cancer research also enhance market growth potential.

Asia-Pacific Gastric Cancer Market Insight

The Asia-Pacific gastric cancer market is poised to grow at the fastest CAGR of 18% during the forecast period of 2026 to 2033, driven by high gastric cancer prevalence in countries such as China, Japan, and South Korea. Rising awareness of early detection programs, increasing healthcare access, and technological advancements in diagnostics and treatments are key growth factors. The region’s growing emphasis on screening programs and government initiatives promoting cancer care are accelerating adoption. Furthermore, expanding hospital networks and specialty centers improve accessibility to advanced therapies for a larger patient population.

Japan Gastric Cancer Market Insight

The Japan gastric cancer market is gaining momentum due to the country’s high gastric cancer incidence, advanced healthcare infrastructure, and emphasis on early detection and prevention. Adoption of minimally invasive surgery, targeted therapies, and immunotherapies is increasing rapidly. Japan’s aging population further drives demand for effective and patient-friendly treatment options. Integration of molecular diagnostics and precision medicine into standard clinical practice enhances treatment outcomes. Government-led screening programs and well-established oncology centers continue to support market expansion.

India Gastric Cancer Market Insight

The India gastric cancer market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to increasing awareness of cancer prevention, expanding healthcare infrastructure, and growing adoption of targeted and supportive therapies. India’s rising incidence of gastric cancer, coupled with government initiatives promoting cancer screening and treatment accessibility, is driving market growth. Expansion of specialty hospitals, oncology centers, and affordable therapy options further supports adoption. Growing patient awareness and domestic pharmaceutical manufacturing contribute to the increasing availability of advanced therapies across residential and commercial healthcare settings.

Gastric Cancer Market Share

The Gastric Cancer industry is primarily led by well-established companies, including:

- Merck & Co., Inc. (U.S.)

- Bristol Myers Squibb Company (U.S.)

- Eli Lilly and Company (U.S.)

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- AstraZeneca (U.K.)

- Sanofi (France)

- Bayer AG (Germany)

- Celltrion, Inc. (South Korea)

- Daiichi Sankyo Company, Limited (Japan)

- Ono Pharmaceutical Co., Ltd. (Japan)

- Ipsen Pharma (France)

- Takeda Pharmaceutical Company Limited (Japan)

- GSK plc (U.K.)

- AbbVie Inc. (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Sun Pharmaceutical Industries Ltd. (India)

- Eisai Co., Ltd. (Japan)

What are the Recent Developments in Global Gastric Cancer Market?

- In November 2025, the U.S. Food and Drug Administration (FDA) granted approval to durvalumab (Imfinzi) plus FLOT chemotherapy as the first perioperative immunotherapy regimen for adults with resectable, early‑stage and locally advanced gastric and gastroesophageal junction (GEJ) cancers, marking a new standard of care that significantly improves survival outcomes in this setting

- In June 2025, Amgen announced positive Phase III results for its experimental targeted antibody bemarituzumab combined with chemotherapy, showing a statistically significant improvement in overall survival for patients with unresectable, locally advanced or metastatic FGFR2b‑positive gastric/GEJ cancer in the FORTITUDE‑101 trial, representing a potential advancement in targeted treatment option

- In August 2024, the UK’s Medicines and Healthcare products Regulatory Agency (MHRA) licensed a new targeted therapy, zolbetuximab (Vyloy), for adults with gastric or gastro‑oesophageal junction cancer whose tumors express the CLDN18.2 protein, expanding treatment options for biomarker‑defined patient subgroups

- In November 2023, the FDA amended the indication for pembrolizumab (Keytruda) in gastric or gastroesophageal junction adenocarcinoma, refining its use with trastuzumab and chemotherapy specifically for PD‑L1 (CPS ≥ 1) expressing tumors and approving a companion diagnostic to guide patient selection

- In April 2021, the FDA approved nivolumab (Opdivo) in combination with chemotherapy as the first immunotherapy‑based initial treatment for advanced or metastatic gastric, GEJ and related cancers, significantly extending median survival compared with chemotherapy alone and establishing immunotherapy as a key first‑line option

SKU-

Obtenga acceso en línea al informe sobre la primera nube de inteligencia de mercado del mundo

- Panel de análisis de datos interactivo

- Panel de análisis de empresas para oportunidades con alto potencial de crecimiento

- Acceso de analista de investigación para personalización y consultas

- Análisis de la competencia con panel interactivo

- Últimas noticias, actualizaciones y análisis de tendencias

- Aproveche el poder del análisis de referencia para un seguimiento integral de la competencia

Metodología de investigación

La recopilación de datos y el análisis del año base se realizan utilizando módulos de recopilación de datos con muestras de gran tamaño. La etapa incluye la obtención de información de mercado o datos relacionados a través de varias fuentes y estrategias. Incluye el examen y la planificación de todos los datos adquiridos del pasado con antelación. Asimismo, abarca el examen de las inconsistencias de información observadas en diferentes fuentes de información. Los datos de mercado se analizan y estiman utilizando modelos estadísticos y coherentes de mercado. Además, el análisis de la participación de mercado y el análisis de tendencias clave son los principales factores de éxito en el informe de mercado. Para obtener más información, solicite una llamada de un analista o envíe su consulta.

La metodología de investigación clave utilizada por el equipo de investigación de DBMR es la triangulación de datos, que implica la extracción de datos, el análisis del impacto de las variables de datos en el mercado y la validación primaria (experto en la industria). Los modelos de datos incluyen cuadrícula de posicionamiento de proveedores, análisis de línea de tiempo de mercado, descripción general y guía del mercado, cuadrícula de posicionamiento de la empresa, análisis de patentes, análisis de precios, análisis de participación de mercado de la empresa, estándares de medición, análisis global versus regional y de participación de proveedores. Para obtener más información sobre la metodología de investigación, envíe una consulta para hablar con nuestros expertos de la industria.

Personalización disponible

Data Bridge Market Research es líder en investigación formativa avanzada. Nos enorgullecemos de brindar servicios a nuestros clientes existentes y nuevos con datos y análisis que coinciden y se adaptan a sus objetivos. El informe se puede personalizar para incluir análisis de tendencias de precios de marcas objetivo, comprensión del mercado de países adicionales (solicite la lista de países), datos de resultados de ensayos clínicos, revisión de literatura, análisis de mercado renovado y base de productos. El análisis de mercado de competidores objetivo se puede analizar desde análisis basados en tecnología hasta estrategias de cartera de mercado. Podemos agregar tantos competidores sobre los que necesite datos en el formato y estilo de datos que esté buscando. Nuestro equipo de analistas también puede proporcionarle datos en archivos de Excel sin procesar, tablas dinámicas (libro de datos) o puede ayudarlo a crear presentaciones a partir de los conjuntos de datos disponibles en el informe.