Global Parallel Computing Market

Tamaño del mercado en miles de millones de dólares

Tasa de crecimiento anual compuesta (CAGR) :

%

USD

179.93 Billion

USD

281.42 Billion

2025

2033

USD

179.93 Billion

USD

281.42 Billion

2025

2033

| 2026 –2033 | |

| USD 179.93 Billion | |

| USD 281.42 Billion | |

| % | |

|

Global Parallel Computing Market Segmentation, By Component (Software, Hardware, and Services), Deployment (Cloud, On-Premises, and Hybrid), Vertical (BFSI, Healthcare & Life Sciences, Government, Manufacturing " Automotive, IT & Telecom, and Others), Technology (Programming Models & APIs, Accelerator Microarchicast

¿Cuál es la tasa de tamaño y crecimiento del mercado de computación paralela

- Según el Análisis de la Investigación del Mercado del Puente de Datos, el tamaño del mercado global de computación paralela fue valoradoUSD 179.93 billion in 2025y se espera que alcanceUSD 281.42 billion en 2033, aCAGR of 5.75%durante el período previsto

- El crecimiento del mercado se ve impulsado en gran medida por la creciente demanda de computadoras de alto rendimiento en aplicaciones de gran densidad de datos, comointeligencia artificial, aprendizaje automático y análisis de datos grandes

- El aumento de la adopción de computadoras en la nube, la aceleración de la GPU y los procesadores de múltiples núcleos en empresas e instituciones de investigación está impulsando el mercado paralelo de computación

Tamaño del mercado

- Valor mundial del mercado (2025):USD 179.93 billion in 2025

- Valor de mercado esperado (2033):USD 281.42 billion en 2033

- CAGR prefabricado (2026–2033):5.75%

Parallel Computing Market Analysis

- El mercado paralelo de computación es testigo de un crecimiento significativo debido a los avances tecnológicos en hardware y software, lo que permite un cálculo más rápido y una mayor eficiencia

- El enfoque creciente en el procesamiento de datos en tiempo real, análisis predictivo y simulaciones complejas en diversos sectores está fomentando la adopción de sistemas de computación paralelos

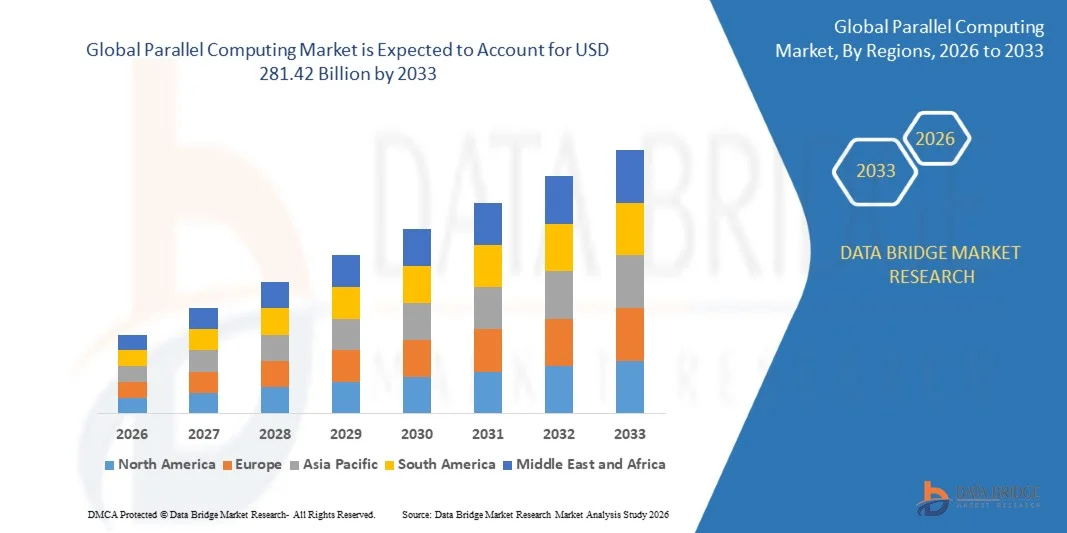

- América del Norte dominaba el mercado paralelo de computación con la mayor cuota de ingresos del 28,3% en 2025, impulsada por la pronta adopción de sistemas de computación de alto rendimiento y el aumento de las inversiones en inteligencia artificial, aprendizaje automático y análisis de datos en empresas

- Se espera que la región de Asia y el Pacífico sea testigo de la tasa de crecimiento más alta del mundocomputación paralelamercado, impulsado por la digitalización rápida, el aumento de las inversiones en infraestructura de IA y HPC, la expansión de los servicios en la nube y el surgimiento de centros tecnológicos en China, Japón e India

- El segmento de hardware mantuvo la mayor cuota de ingresos del mercado del 57% en 2025, impulsada por la creciente demanda de sistemas de computación de alto rendimiento y procesadores especializados que pueden manejar computaciones complejas de manera eficiente. Las soluciones de hardware, incluidas las GPU, las CPU y las FPGA, se adoptan ampliamente en todas las empresas e instituciones de investigación para acelerar el procesamiento de datos y mejorar el rendimiento general del sistema

Report Scope and Parallel Computing Market Segmentation

|

Atributos |

Parallel Computing Key Market Insights |

|

Segmentos cubiertos |

|

|

Países cubiertos |

América del Norte

Europa

Asia y el Pacífico

Oriente Medio y África

América del Sur

|

|

Principales jugadores del mercado |

|

|

Oportunidades de mercado |

|

|

Valor añadido Data Infosets |

Además de las ideas del mercado, como el valor de mercado, la tasa de crecimiento, los segmentos de mercado, la cobertura geográfica, los jugadores de mercado y el escenario de mercado, el informe del mercado comisariado por el equipo de Investigación del Mercado de Datos del Puente incluye análisis profundo de expertos, análisis de importaciones/exportaciones, análisis de precios, análisis de consumo de producción y análisis de plagas. |

¿Cuál es la tendencia clave en el mercado de computación paralelo

“Rising Adoption of High-Performance Computing and Big Data Analytics”

- La creciente dependencia de los sistemas de computación de alto rendimiento (HPC) y la analítica de datos grandes está formando significativamente el mercado paralelo de computación, ya que las organizaciones requieren cada vez más capacidades de procesamiento más rápidas para computaciones complejas. Las arquitecturas de computación paralela están ganando tracción debido a su capacidad de realizar múltiples tareas simultáneamente, reduciendo el tiempo de procesamiento y mejorando la eficiencia operacional. Esta tendencia fortalece su adopción en las industrias de TI, finanzas, salud e investigación científica, alentando a los proveedores a innovar con nuevas soluciones escalables y eficientes en la energía

- Increasing emphasis on artificial intelligence (AI), machine learning (ML), andcloud computingha acelerado la demanda de sistemas informáticos paralelos. Las empresas y las instituciones de investigación están aprovechando la computación paralela para procesar de manera eficiente grandes conjuntos de datos, lo que permite obtener información más rápida y mejorar la adopción de decisiones. La creciente integración de la informática paralela con los marcos de IA también fomenta las asociaciones entre proveedores de hardware y software para mejorar el rendimiento y la funcionalidad

- Las tendencias de despliegue y virtualización basadas en la nube influyen en las decisiones de compra, con empresas que buscan recursos de cálculo flexibles a pedido. Estos factores están ayudando a las organizaciones a optimizar los costos, aumentar la escalabilidad y acelerar el tiempo al mercado, al tiempo que impulsan la adopción de arquitecturas híbridas y multicloud. Los proveedores están promoviendo cada vez más capacidades de cálculo paralelas para poner de relieve los beneficios de eficiencia y rendimiento, apelando a los consumidores impulsados por la tecnología

- Por ejemplo, en 2024, IBM en los EE.UU. y Fujitsu en Japón amplió sus carteras de supercomputación integrando tecnologías avanzadas de computación paralela para simulaciones científicas y de inteligencia artificial. Estas mejoras fueron introducidas para satisfacer la creciente demanda de un procesamiento más rápido y una mayor precisión computacional, con el despliegue en plataformas empresariales, de investigación y de nube. Los productos también se comercializaron como soluciones energéticamente eficientes y de alto rendimiento, mejorando la adopción de clientes y la lealtad

- Si bien la demanda de computación paralela está creciendo, la expansión sostenida del mercado depende de diseños continuos de R–D, eficientes en la energía y de despliegue rentable. Los proveedores también se centran en mejorar la escalabilidad, la integración de software y la elaboración de soluciones innovadoras que equilibran el rendimiento, el costo y la sostenibilidad para una adopción más amplia

Dinámicas del mercado de computación paralela

Conductor

“Growing Demand for High-Performance Computing and Big Data Analytics”

- El aumento de los requisitos institucionales y de investigación para el procesamiento más rápido de datos y la computación de alto rendimiento es un factor importante para el mercado de computación paralelo. Las organizaciones están reemplazando cada vez más los sistemas informáticos tradicionales con arquitecturas paralelas para mejorar la eficiencia del procesamiento y reducir la latencia. Esta tendencia también fomenta la investigación en aceleradores especializados de hardware y algoritmos paralelos optimizados, apoyando la diversificación del mercado

- Ampliar aplicaciones en IA, machine learning, cloud computing, simulations científicos y modelado financiero están influenciando el crecimiento del mercado. El cálculo paralelo permite la ejecución simultánea de tareas, reduciendo el tiempo de computación manteniendo la precisión y fiabilidad. La creciente adopción de aplicaciones de gran densidad de datos a nivel mundial refuerza aún más esta tendencia

- Los proveedores de tecnología están promoviendo activamente soluciones de computación paralelas mediante la optimización de software, innovaciones de hardware y asociaciones de ecosistemas. Estos esfuerzos están respaldados por la creciente demanda empresarial de análisis en tiempo real y modelos predictivos, y también fomentan la colaboración entre desarrolladores de software y fabricantes de hardware para mejorar el rendimiento del sistema y la eficiencia energética

- Por ejemplo, en 2023, NVIDIA en los EE.UU. y Atos en Francia informó de un aumento del despliegue de marcos de computación paralelos en las simulaciones de capacitación de IA y alto rendimiento. Esta expansión siguió una mayor demanda de un procesamiento más rápido y escalabilidad computacional, la adopción empresarial y la diferenciación competitiva. Ambas empresas también hicieron hincapié en la eficiencia energética y la reducción de los costos operacionales en las campañas de marketing para fortalecer la confianza y el compromiso de los clientes

- Aunque las crecientes tendencias de HPC y AI apoyan el crecimiento, la adopción más amplia depende de la optimización de costos, los diseños eficientes en la energía y la compatibilidad con la infraestructura de TI existente. La inversión en sistemas escalables, el desarrollo avanzado de software y la integración con plataformas cloud serán fundamentales para satisfacer la demanda mundial y mantener una ventaja competitiva

Restraint/Challenge

“Sus costos de implementación y complejidad técnica”

- El costo relativamente alto de los equipos y programas informáticos paralelos en comparación con los sistemas convencionales sigue siendo un problema fundamental, lo que limita la adopción entre las empresas que tienen en cuenta los precios. Los procesadores especializados, las interconexiones y los marcos de software contribuyen a elevar los gastos de capital, lo que afecta a la penetración del mercado en las regiones emergentes. Las organizaciones pueden retrasar la adopción debido a las limitaciones presupuestarias y a las incertidumbres de la aplicación conjunta

- La complejidad técnica y la limitada mano de obra calificada también afectan el crecimiento del mercado, ya que la informática paralela requiere experiencia en modelos de programación, optimización de algoritmos e integración del sistema. La disponibilidad limitada de profesionales capacitados puede retrasar el despliegue, especialmente en los países en desarrollo donde la infraestructura informática sigue evolucionando

- Los requisitos de infraestructura y los retos del consumo de energía siguen afectando la adopción, ya que los sistemas paralelos de alto rendimiento exigen considerables recursos energéticos y de refrigeración. Los centros de datos necesitan optimizar el espacio físico, las redes y la gestión térmica, aumentando los costos operacionales

- Por ejemplo, en 2024, varias instituciones de investigación de Asia sudoriental y América Latina informaron de un despliegue más lento de grupos de computación paralelos debido a los elevados costos de hardware, las limitaciones de energía y los limitados conocimientos técnicos, que afectaban la utilización general del sistema y los plazos de los proyectos

- Para superar estos desafíos será necesario invertir en hardware rentable, diseños eficientes en energía y programas de capacitación para construir recursos técnicos cualificados. La colaboración con proveedores de servicios en la nube, instituciones educativas y socios tecnológicos puede ayudar a desbloquear el potencial de crecimiento a largo plazo del mercado global de computación paralela. Además, el desarrollo de soluciones híbridas y marcos fáciles de utilizar serán esenciales para la adopción generalizada

Parallel Computing Market Scope

El mercado se segmenta sobre la base de componentes, despliegue, vertical y tecnología.

- Por componente

Sobre la base del componente, el mercado paralelo de computación se segmenta en software, hardware y servicios. El segmento de hardware mantuvo la mayor cuota de ingresos del mercado del 57% en 2025, impulsada por la creciente demanda de sistemas de computación de alto rendimiento y procesadores especializados que pueden manejar computaciones complejas de manera eficiente. Las soluciones de hardware, incluidas las GPU, las CPU y las FPGA, se adoptan ampliamente en todas las empresas e instituciones de investigación para acelerar el procesamiento de datos y mejorar el rendimiento general del sistema.

Se espera que el segmento de software sea testigo de la tasa de crecimiento más rápida de 2026 a 2033, impulsada por la creciente necesidad de marcos de cálculo paralelos optimizados, modelos de programación y API que permitan una distribución eficiente del volumen de trabajo y la ejecución de tareas. Las soluciones de software facilitan la escalabilidad, reducen el tiempo de cálculo y permiten una integración perfecta con plataformas de nube, haciéndolos altamente valiosos para la IA, análisis de datos grandes y simulaciones científicas.

- Despliegue

Sobre la base del despliegue, el mercado se segmenta en nube, locales e híbridos. El segmento de la nube mantuvo la mayor parte en 2025, debido a su flexibilidad, escalabilidad y eficacia en función de los costos para las empresas que buscaban capacidades de computación de alto rendimiento sin invertir fuertemente en infraestructura física. El cálculo paralelo basado en la nube permite a las organizaciones acceder a recursos de gran alcance bajo demanda, apoyando un análisis más rápido y cargas de trabajo de IA.

Se espera que el segmento híbrido sea testigo del crecimiento más rápido de 2026 a 2033, alimentado por la creciente necesidad de que las organizaciones equilibren la infraestructura local con capacidades en la nube. El despliegue híbrido permite una gestión eficiente del volumen de trabajo, una mayor seguridad y una mejor optimización de los costos, lo que hace que sea una opción preferida para las empresas con necesidades informáticas complejas.

- Por Vertical

Sobre la base de la verticalidad, el mercado se segmenta en BFSI, ciencias de la salud " , gobierno, fabricación " automotriz, telecomunicaciones IT " y otros. El telecom vertical mantuvo la mayor cuota de mercado del 23,2% en 2025, impulsada por la alta adopción de computación paralela para centros de datos, aplicaciones impulsadas por IA y gestión de redes a gran escala. El cálculo paralelo permite a estos sectores procesar rápidamente conjuntos de datos masivos y mejorar la prestación de servicios.

Se espera que las ciencias de la salud y la vida sean testigos del crecimiento más rápido de 2026 a 2033, debido a la creciente necesidad de computación paralela en la genómica, el descubrimiento de drogas y las aplicaciones médicas de imagen. Las capacidades computacionales avanzadas ayudan a acelerar la investigación, reducir el tiempo de análisis y apoyar soluciones sanitarias personalizadas.

- By Technology

Sobre la base de la tecnología, el mercado se segmenta en modelos de programación " APIs, microarquitectura aceleradora/ISA, tecnologías de tela interconectadas " , orquestación " middleware, núcleos de bibliotecas " y otros. El segmento de microarquitectura/ISA acelerador mantuvo la mayor parte en 2025, alimentada por el creciente despliegue de GPU, TPU y FPGAs que mejoran significativamente la velocidad y eficiencia de la computación.

Se espera que los modelos de programación " segmento de API sean testigos de la tasa de crecimiento más rápida de 2026 a 2033, impulsada por la necesidad de instrumentos de desarrollo estandarizados y una distribución eficiente del volumen de trabajo en arquitecturas paralelas de cálculo. Estas tecnologías simplifican el desarrollo, mejoran el rendimiento y permiten una integración perfecta con entornos de nube y locales, apoyando aplicaciones de IA, ML y HPC.

¿Qué región posee la mayor parte del mercado de computación paralela

- América del Norte dominaba el mercado paralelo de computación con la mayor cuota de ingresos del 28,3% en 2025, impulsada por la pronta adopción de sistemas de computación de alto rendimiento y el aumento de las inversiones en inteligencia artificial, aprendizaje automático y análisis de datos en empresas

- La fuerte infraestructura de TI de la región, la presencia de los principales proveedores de tecnología y la alta demanda de servicios basados en la nube están impulsando el crecimiento

- Las empresas e instituciones de investigación dependen cada vez más de la informática paralela para simulaciones complejas, procesamiento de datos e investigación científica, estableciendo América del Norte como un centro clave para la expansión del mercado

U.S. Parallel Computing Market Insight

El mercado de computación paralela estadounidense capturó la mayor cuota de ingresos en 2025 dentro de América del Norte, apoyada por el liderazgo del país en informática en la nube, adopción de IA y infraestructura de supercomputación. Las organizaciones de todo el sector de BFSI, salud, fabricación y gobierno están integrando la computación paralela para mejorar la eficiencia computacional, reducir los tiempos de procesamiento y acelerar la innovación. La presencia de proveedores líderes de hardware y software, junto con las inversiones continuas de R plagaD, fortalece la posición de Estados Unidos en el mercado global de computación paralela.

Europe Parallel Computing Market Insight

Se espera que el mercado de computación paralelo de Europa sea testigo de la tasa de crecimiento más rápida de 2026 a 2033, impulsada por la digitalización creciente, el aumento de la IA y la adopción de grandes datos, y las iniciativas gubernamentales que apoyan la computación de alto rendimiento. La región se centra en la modernización de la infraestructura de TI en industrias, incluyendo la automoción, la salud y la fabricación. Las empresas europeas están implementando cada vez más sistemas de computación paralelos para mejorar la capacidad de procesamiento de datos, apoyar la investigación y optimizar las operaciones industriales.

U.K. Parallel Computing Market Insight

Se proyecta que el mercado de computación paralelo del Reino Unido crecerá rápidamente de 2026 a 2033, alimentado por avances en la adopción de IA, machine learning y cloud computing. Aumentar las inversiones en fintech, análisis sanitarios y programas de investigación gubernamentales están contribuyendo a la expansión del mercado. La integración de soluciones de computación paralela aumenta la velocidad, precisión y eficiencia computacionales, satisfaciendo la creciente demanda de toma de decisiones basada en datos y simulaciones avanzadas tanto en los sectores público como privado.

Alemania Mercado de computación paralelo

Se espera que el mercado de computación paralelo de Alemania experimente un crecimiento significativo entre el 2026 y el 2033, impulsado por robustas iniciativas de R plagaD, automatización industrial y demanda de computación de alto rendimiento en sectores manufactureros y automotrices. El ecosistema tecnológico bien desarrollado de Alemania y el enfoque en la innovación permiten a las empresas adoptar computación paralela para la optimización del proceso, la simulación y la analítica predictiva. La creciente adopción de soluciones basadas en la nube HPC acelera aún más la expansión del mercado en el país.

Asia-Pacific Parallel Computing Market Insight

Se espera que el mercado de computación paralela de Asia y el Pacífico sea testigo de la tasa de crecimiento más rápida de 2026 a 2033, alimentada por el aumento de las inversiones en IA, infraestructura en la nube y transformación digital en China, Japón, India y Corea del Sur. La región está experimentando una creciente demanda de computadoras de alto rendimiento en servicios de TI, instituciones de investigación y aplicaciones industriales. Además, el surgimiento de la APAC como centro de fabricación y tecnología para el hardware y el software informático está impulsando la accesibilidad y adopción de soluciones de computación paralelas.

Japan Parallel Computing Market Insight

Se prevé que el mercado de computación paralelo de Japón crecerá rápidamente de 2026 a 2033 debido al fuerte enfoque del país en las iniciativas de inteligencia artificial, robótica y supercomputación. Las empresas japonesas están aprovechando cada vez más la computación paralela para simulaciones avanzadas, investigación científica y aplicaciones de gran densidad de datos. Se espera que las inversiones en infraestructuras de HPC, informática basada en la nube y proyectos de I+D aumenten la expansión del mercado, especialmente en los sectores manufacturero, sanitario y de investigación gubernamental.

China Parallel Computing Market Insight

El mercado de computación paralelo de China representó la mayor cuota de ingresos en Asia y el Pacífico en 2025, impulsada por la infraestructura de TI en expansión del país, la digitalización rápida y la adopción creciente de sistemas informáticos basados en la nube y de alto rendimiento. El enfoque creciente en IA, análisis de datos grandes y automatización industrial apoya el crecimiento del mercado. Las fuertes iniciativas gubernamentales, la inversión en centros de supercomputación y la disponibilidad de equipos informáticos rentables están impulsando aún más el mercado en China.

¿Cuáles son las mejores empresas del mercado de computación paralelo

La industria de computación paralela está dirigida principalmente por empresas bien establecidas, incluyendo:

- Amazon Web Services, Inc.(U.S.)

- Apple Inc. (Estados Unidos)

- Atos SE(U.K.)

- Dell Inc. (U.S.)

- Fujitsu(U.K.)

- Hewlett Packard Enterprise Development LP (Estados Unidos)

- IBM Corporation (Estados Unidos)

- Intel Corporation (Estados Unidos)

- Microsoft (Estados Unidos)

- NVIDIA Corporation (Estados Unidos)

¿Cuáles son los desarrollos recientes en el mercado de computación paralelo

- En marzo de 2025, Quantum Machines lanzó el NVIDIA DGX Quantum Early Customer Program, introduciendo una plataforma de cálculo de tipo cuántico muy integrada. La solución combina el sistema modular de control cuántico OPX1000 de Quantum Machines con los superchips de GH200 Grace Hopper de NVIDIA, proporcionando una latencia ultra-bajo de menos de 4 microsegundos entre el control cuántico y los supercomputadores de IA. Esta innovación aumenta la eficiencia computacional para las cargas de trabajo cuánticas y de IA, posicionando a la empresa a la vanguardia de las soluciones de computación híbrida y fortaleciendo su presencia en mercados de computación de alto rendimiento

- En noviembre de 2024, Eviden, parte del Grupo Atos, dio a conocer BXI v3, la tecnología europea de redes de escala de tercera generación diseñada para la carga de trabajo de AI y HPC. Desarrollado con la Comisión Francesa de Energía Atómica (CEA), integra la descarga de tecnología SmartNIC y protocolo de aplicaciones para optimizar la utilización de CPU y GPU, mejorando la velocidad de ejecución de aplicaciones hasta en un 35%, al tiempo que reduce el costo total de propiedad. This development addresses networking bottlenecks, enhancing performance and efficiency for AI and high-performance computing applications

- En noviembre de 2023, Fujitsu introdujo una nueva tecnología para optimizar dinámicamente el uso de CPU y GPU en tiempo real, priorizando procesos con mayor eficiencia de ejecución. Integrada en un próximo corredor de carga de trabajo impulsado por AI, esta innovación ayuda a asignar recursos computacionales basados en factores tales como tiempo de cálculo, precisión y coste. La tecnología tiene por objeto aliviar la escasez mundial de GPU causada por la demanda creciente de la IA generativa y el aprendizaje profundo, potenciando el rendimiento y la eficiencia en todas las cargas de trabajo de la IA y el HPC, al tiempo que permite una gestión de recursos más eficaz en función de los costos

SKU-

Obtenga acceso en línea al informe sobre la primera nube de inteligencia de mercado del mundo

- Panel de análisis de datos interactivo

- Panel de análisis de empresas para oportunidades con alto potencial de crecimiento

- Acceso de analista de investigación para personalización y consultas

- Análisis de la competencia con panel interactivo

- Últimas noticias, actualizaciones y análisis de tendencias

- Aproveche el poder del análisis de referencia para un seguimiento integral de la competencia

Metodología de investigación

La recopilación de datos y el análisis del año base se realizan utilizando módulos de recopilación de datos con muestras de gran tamaño. La etapa incluye la obtención de información de mercado o datos relacionados a través de varias fuentes y estrategias. Incluye el examen y la planificación de todos los datos adquiridos del pasado con antelación. Asimismo, abarca el examen de las inconsistencias de información observadas en diferentes fuentes de información. Los datos de mercado se analizan y estiman utilizando modelos estadísticos y coherentes de mercado. Además, el análisis de la participación de mercado y el análisis de tendencias clave son los principales factores de éxito en el informe de mercado. Para obtener más información, solicite una llamada de un analista o envíe su consulta.

La metodología de investigación clave utilizada por el equipo de investigación de DBMR es la triangulación de datos, que implica la extracción de datos, el análisis del impacto de las variables de datos en el mercado y la validación primaria (experto en la industria). Los modelos de datos incluyen cuadrícula de posicionamiento de proveedores, análisis de línea de tiempo de mercado, descripción general y guía del mercado, cuadrícula de posicionamiento de la empresa, análisis de patentes, análisis de precios, análisis de participación de mercado de la empresa, estándares de medición, análisis global versus regional y de participación de proveedores. Para obtener más información sobre la metodología de investigación, envíe una consulta para hablar con nuestros expertos de la industria.

Personalización disponible

Data Bridge Market Research es líder en investigación formativa avanzada. Nos enorgullecemos de brindar servicios a nuestros clientes existentes y nuevos con datos y análisis que coinciden y se adaptan a sus objetivos. El informe se puede personalizar para incluir análisis de tendencias de precios de marcas objetivo, comprensión del mercado de países adicionales (solicite la lista de países), datos de resultados de ensayos clínicos, revisión de literatura, análisis de mercado renovado y base de productos. El análisis de mercado de competidores objetivo se puede analizar desde análisis basados en tecnología hasta estrategias de cartera de mercado. Podemos agregar tantos competidores sobre los que necesite datos en el formato y estilo de datos que esté buscando. Nuestro equipo de analistas también puede proporcionarle datos en archivos de Excel sin procesar, tablas dinámicas (libro de datos) o puede ayudarlo a crear presentaciones a partir de los conjuntos de datos disponibles en el informe.